Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

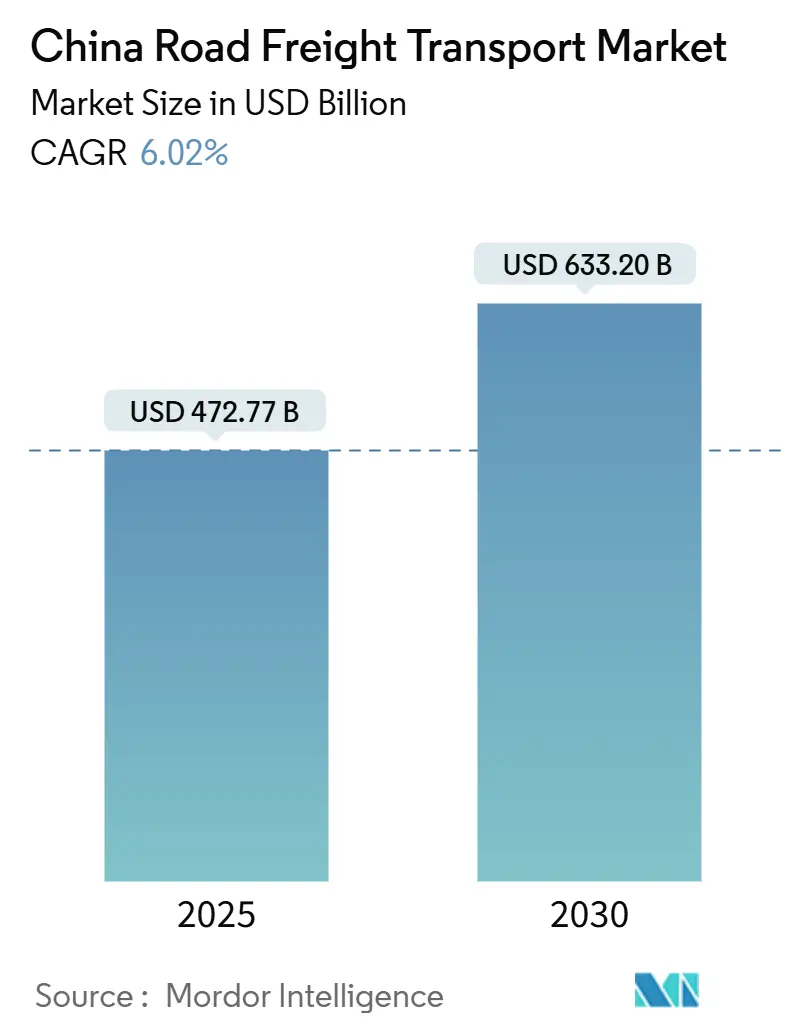

| Market Size (2025) | USD 472.77 Billion |

| Market Size (2030) | USD 633.20 Billion |

| Growth Rate (2025 - 2030) | 6.02% CAGR |

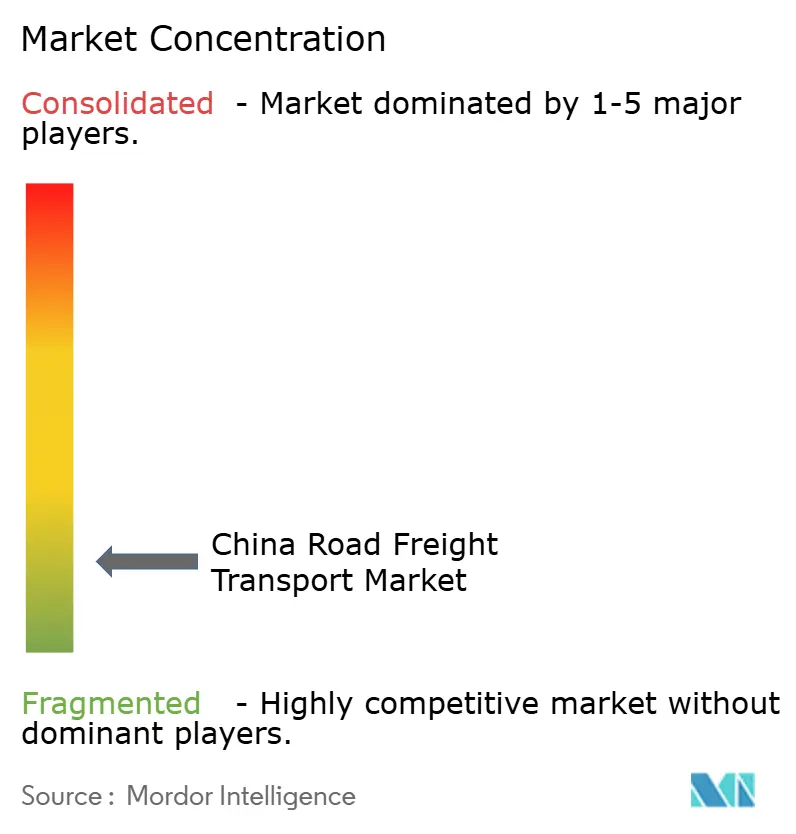

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Road Freight Transport Market Analysis by Mordor Intelligence

The China road freight transport market size is estimated at USD 472.77 billion in 2025, and is expected to reach USD 633.20 billion by 2030, at a CAGR of 6.02% during the forecast period (2025-2030). Strong e-commerce demand, a resurgent manufacturing base, and continuous expressway expansion are the principal catalysts powering this trajectory. Explosive parcel volumes, which hit 174.5 billion packages in 2024, require dense last-mile delivery networks and specialized vehicles. Export diversification toward Vietnam, India, and Russia sustains outbound freight even as geopolitical frictions reshape trade lanes. Digital freight platforms raise load factors by trimming empty backhaul mileage, while battery-electric trucks gain traction as operating costs converge with diesel alternatives. Regulatory initiatives that target RMB 300 billion in logistics savings and mandate fleet renewal reinforce structural efficiencies across the China road freight transport market.

Key Report Takeaways

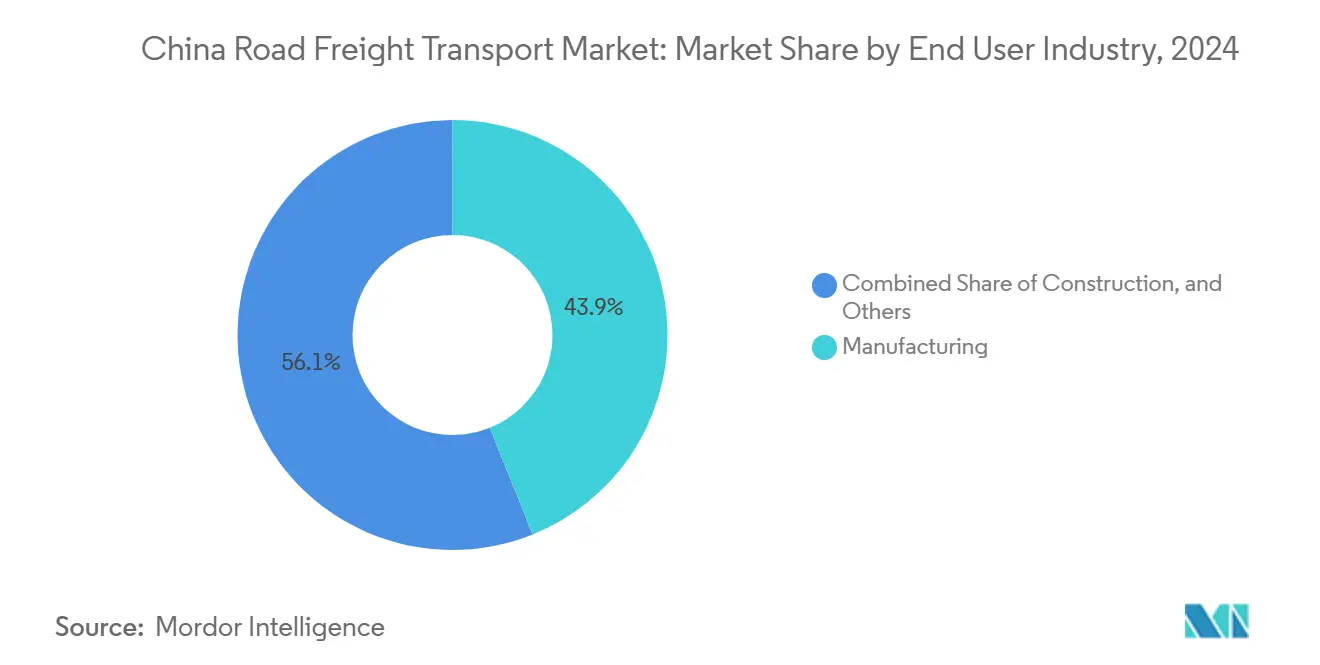

- By end user industry, manufacturing held 43.92% of the China road freight transport market share in 2024, whereas wholesale and retail trade is forecast to grow the fastest at a 6.92% CAGR between 2025-2030.

- By destination, domestic freight accounted for 63.48% of the China road freight transport market size in 2024, while international freight is expected to expand at a 7.02% CAGR during 2025-2030.

- By truckload specification, FTL services commanded 79.10% of the revenue share in 2024, yet the LTL segment is projected to register the highest growth at a 6.74% CAGR between 2025-2030.

- By containerization, non-containerized cargo dominated with an 85.44% revenue share of the market in 2024, but containerized freight is poised to rise at a 6.14% CAGR between 2025-2030.

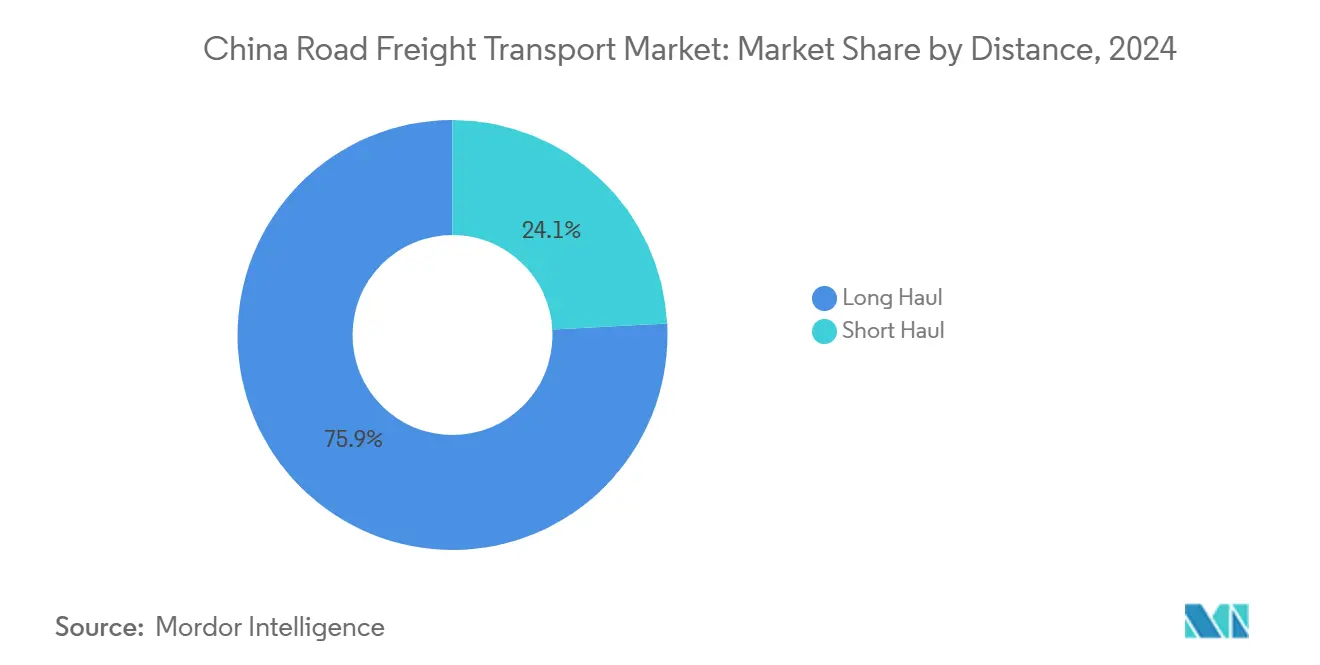

- By distance, long-haul operations controlled 75.86% of the revenue share in 2024 and also deliver the fastest growth at a 6.32% CAGR between 2025-2030.

- By goods configuration, solid goods captured 72.13% of revenue share in 2024, whereas fluid goods are forecast to post a 6.48% CAGR between 2025-2030.

- By temperature control, non-temperature-controlled freight represented 94.33% of the revenue share in 2024, while temperature-controlled shipments are set to advance at a 6.62% CAGR between 2025-2030.

China Road Freight Transport Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth in B2C e-commerce parcel volumes | +1.8% | Tier 1-2 cities with rural spillover | Short term (≤ 2 years) |

| Manufacturing-sector rebound and export diversification | +1.5% | Guangdong, Jiangsu, Zhejiang; inland hubs | Medium term (2-4 years) |

| Continuous expansion of the national expressway and highway network | +1.2% | National priority corridors | Long term (≥ 4 years) |

| AI-powered digital freight platforms boosting load factors | +0.9% | Higher adoption in developed regions | Medium term (2-4 years) |

| Cost competitiveness of battery-electric and LNG heavy trucks | +0.7% | Urban areas, green corridors | Long term (≥ 4 years) |

| “Road-Rail Multimodal” incentives creating new feeder-road demand | +0.6% | Logistics hubs and rail terminals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Explosive Growth in B2C E-Commerce Parcel Volumes

E-commerce parcel throughput of 174.5 billion packages in 2024 equates to nearly 100 consignments per capita, reshaping last-mile logistics footprints. Urban delivery fleets have scaled rapidly, and niche segments such as fresh-produce distribution jumped from CNY 195 billion (USD 27.50 billion) in 2018 to CNY 642.8 billion (USD 90.66 billion) in 2023. Consolidated distribution centers lower unit transport costs, while rural e-commerce penetration spurs new county-level routes. Government programs permitting passenger-freight integration extend service coverage to remote areas. In parallel, overseas warehouses run by platform firms create two-way freight flows that bolster the China road freight transport market[1]“Alibaba to Cut Stake in YTO Express as It Scales Back Non-Core Investments,” Caixin Global, caixinglobal.com .

Manufacturing-Sector Rebound and Export Diversification

China posted USD 240 billion in bilateral trade with Russia in 2023, up 26.3% year over year. Exports to Vietnam and India more than doubled between 2014 and 2024, adding fresh corridors for long-haul trucking. “China + 1” strategies keep domestic plants busy shipping intermediate goods to nearby economies, while new export-control regimes concentrate high-value materials in secure supply chains that demand specialized vehicles. Mature clusters in Guangdong, Jiangsu and Zhejiang still dominate, but inland factories now secure a larger slice of the China road freight transport market[2]“U.S.-China 2025 Annual Economic Report,” Cathay Bank, cathaybank.com.

Continuous Expressway and Highway Expansion

Expressway mileage reached 184,000 km in 2023, with 50,000 km laid during the past decade. Funding guidance under the 2024 infrastructure mandate prioritizes trunk-and-branch connectivity. New corridors linking the Yangtze River Delta and Pearl River Delta slash transit times and enhance route reliability. As a result, long-haul services already 75.86% of freight tonnage in 2024 benefit from lower per-kilometer costs and tighter delivery windows. Border highways that anchor the Belt and Road Initiative improve overland access to Central Asia, expanding the reach of the China road freight transport market.

AI-Powered Digital Freight Platforms Boosting Load Factors

Platforms such as Manbang process millions of orders daily, shrinking empty-haul ratios that historically hovered between 15% and 40%. Artificial intelligence matches shipments with available capacity in seconds, raising truck utilization and trimming fuel waste. Government data-sharing protocols underpin interoperability among disparate systems, and IoT sensors feed real-time location and maintenance data into predictive dashboards. Small carriers gain network scale, and shippers enjoy dependable service all strengthening the China road freight transport market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of qualified truck drivers and double-digit wage inflation | -1.4% | More severe in eastern regions | Short term (≤ 2 years) |

| Volatile diesel prices and uncertain surcharge pass-through | -0.8% | National | Short term (≤ 2 years) |

| Stringent low-emission zones restricting older Euro III/IV diesel trucks | -0.6% | Major cities, expanding to tier-2 | Medium term (2-4 years) |

| Persistent empty-backhaul problem on fragmented long-haul corridors | -0.4% | Long-haul inter-regional routes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Qualified Truck Drivers and Double-Digit Wage Inflation

Vacancies affect 16% of the 17 million-strong driver workforce, and 82% are older than 35. Nearly three-quarters report health issues linked to long hours, fueling turnover and higher wage demands. Despite pay rises, 74.91% state that real incomes fell in 2024 as cost-of-living climbed. Government-sponsored “drivers’ homes” improve rest conditions, yet supply remains tight, pushing fleet operators to automate processes and rely on digital platforms. The labor crunch narrows margins across the China road freight transport market[3]"Management Measures for Key Project Funds in the Transportation Sector,” WAIZI, waizi.org.cn.

Volatile Diesel Prices and Uncertain Surcharge Pass-Through

The national price for No.0 diesel averaged CNY 7.13 (USD 1)per liter in March 2025 after swinging between CNY 8.68 (USD 1.22) and CNY 5.09 (USD 0.71) since 2020. Regional spreads top 0.78 RMB per liter, complicating route economics. Smaller carriers struggle to negotiate fuel clauses, leading to earnings volatility. Fleet managers hedge prices and invest in fuel-saving tech, yet uncertainty continues to pressure the China road freight transport market[4]“Research on the Construction of Hunan Regional Logistics Public Service Base,” Atlantis-Press, atlantis-press.com.

Segment Analysis

By End User Industry: Freight Demand Diversification Under a Manufacturing Core

Manufacturing contributed 43.92% of the China road freight transport market size in 2024, fueled by component inflows and finished-goods deliveries to export gateways. Wholesale and retail trade is the pace-setter, expanding at a 6.92% CAGR between 2025-2030 as omnichannel retailers demand frequent replenishment and hyperlocal delivery networks. Agriculture, fishing, and forestry move steadily on government rural logistics programs, and cold-chain upgrades lift perishable cargo tonnage. Construction cycles link directly with infrastructure outlays and urbanization, while energy and mining cargoes grow on resource security initiatives. Emerging sectors such as pharmaceuticals and automotive aftermarket parts enrich cargo diversity across the China road freight transport market.

Increasing manufacturing exports to Southeast Asia preserve high truck utilization rates. E-commerce-driven wholesale flows need rapid transfer between regional fulfillment centers, intensifying short-haul frequency. Cold-chain deployments push specialized reefer adoption, and project cargo for renewable energy installations broadens demand for modular trailers. All told, downstream diversity cushions cyclical swings and strengthens resilience for the China road freight transport market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Destination: Domestic Bulwark with Faster International Lanes

Domestic hauls formed 63.48% of revenue in 2024, anchored by vast inter-provincial commerce. Industrial belts in the Yangtze River Delta and Pearl River Delta send regular truckloads inland and northward, and rural revitalization programs steer goods into county-town-village networks. Meanwhile, international flows post the quicker 7.02% CAGR between 2025-2030 as exporters pivot to alternative trading partners.

Overland routes to Russia and Central Asia benefit from upgraded border highways and streamlined customs, shortening lead times by three to five days compared with maritime options. Cross-border e-commerce to ASEAN markets leans on bonded warehouses and trucking shuttles, enlarging the international slice of the China road freight transport market. Document compliance and trucking permits add complexity, which favors providers with dedicated cross-border expertise.

By Truckload Specification: FTL Remains King while LTL Consolidates

Full-truck-load services captured 79.10% of the China road freight transport market share in 2024. High-volume industrial consignments and bulk building materials justify vehicle-dedicated runs and direct routing. Less-than-truck-load volumes, however, increase at a 6.74% CAGR between 2025-2030 thanks to parcelized e-commerce and batch-size fragmentation in modern manufacturing.

LTL remains atomized; the top 20 carriers collectively hold under 2%, illustrating scope for consolidation. Digital hubs increase cross-docking density, pushing small firms to join platform alliances to stay competitive. Over time, better network design should raise LTL profitability and rebalance the China road freight transport market.

By Containerization: Specialized Non-Containerized Strength, Rising Box Traffic

Non-containerized cargo comprised 85.44% of revenue in 2024, spanning coal, steel, cement and oversized machinery. Custom rigs and flexible scheduling meet the unique handling demands of these loads. Containerized traffic expands at a 6.14% CAGR between 2025-2030 as pallet standardization and returnable packaging gain favor. Port-to-door intermodal services give shippers end-to-end visibility, enhancing uptake in electronics and apparel exports.

With the government targeting 40% pallet standardization by 2027, container penetration should continue to climb within the China road freight transport market.

By Distance: Long-Haul Mileage Edge with Urban Short-Haul Acceleration

Long-haul trips accounted for 75.86% of 2024 revenue and grow at 6.32% CAGR between 2025-2030 on robust expressway expansion that links inland factories to seaports. Fuel-efficient tractors and relay-driver models optimize long-run economics. Yet short-haul mileage inside mega-cities grows quickly, propelled by same-day delivery promises and refined inventory positioning.

Tight delivery windows and congestion restrictions spark demand for smaller electric vans, diversifying vehicle mixes across the China road freight transport market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Goods Configuration: Solid Goods Majority, Fluid Goods Niche Upturn

Solid goods made up 72.13% of revenue in 2024, reflecting China’s manufacturing and construction heft. Standard curtainsiders, stake trucks and flatbeds dominate this arena. Fluid goods move at a faster 6.48% CAGR between 2025-2030, driven by chemicals, LNG and refined-fuel logistics.

Specialized tankers and stringent hazmat credentials create barriers that let qualified carriers secure premium yields while enlarging their role in the China road freight transport market.

By Temperature Control: Ambient Prevalence, Cold-Chain Momentum

Ambient freight accounted for 94.33% in 2024 owing to the dominance of dry pallets and bulk commodities. Cold-chain lanes climb at a 6.62% CAGR between 2025-2030 on stricter food-safety regulation and greater demand for fresh produce and biologics.

Government targets that call for 25% fruit and 45% meat cold-chain circulation by 2027 trigger heavy investment in reefers, telematics and insulated depots. Higher service premiums offset equipment outlays, solidifying growth within the China road freight transport market.

Geography Analysis

Eastern provinces remain the logistical heartland, with Jiangsu alone generating CNY 32.88 trillion (USD 4.63 trillion) in total social logistics value in 2024, the nation’s top rank. Guangdong leverages its manufacturing depth and seaport cluster to anchor an intricate mesh of inter-provincial truck lanes. Zhejiang’s entrepreneurial base drives express delivery intensity, and the Yangtze River Delta integrates these hubs into a seamless megaregion.

Western freight prospects brighten as Belt and Road corridors unlock trucking potential toward Central Asia and Europe. Bilateral trade with Russia surged 26.3% in 2023, channeling fresh volumes through Xinjiang checkpoints. Improved expressways in Sichuan and Chongqing guide electronics and auto parts toward coastal ports, tightening inland-coastal linkages inside the China road freight transport market.

Rural logistics programs prioritize county-town-village distribution grids. Subsidized transshipment centers and “last-mile couriers” extend parcel coverage to 95% of administrative villages as of 2025. Coupled with e-commerce’s march into lower-tier cities, these initiatives widen freight demand footprints and diversify revenues across the China road freight transport market.

Competitive Landscape

The industry is structurally fragmented: more than 700,000 trucking firms operate fewer than five vehicles each, and the top 20 LTL carriers capture under 2% of segment revenue. JD Logistics’ USD 892 million purchase of Kuayue Express in December 2024 signals a shift toward scale-seeking consolidation. SF Express channels over USD 200 million into overseas warehouses to capture outbound e-commerce freight, and ZTO Express invests USD 150 million to push deeper into rural markets.

Digital freight marketplaces act as equalizers, giving small operators instant visibility to national loads. The largest platform, Manbang, claims over 30 million drivers and 6 million shippers on its network, granting it sizable sway in pricing power. Fleet modernization also splits the field: operators that adopt electric or LNG trucks earlier gain entry to urban low-emission zones, while laggards face access penalties.

Government rules on driver rest facilities and service-area amenities further encourage structured fleets, nudging the China road freight transport market toward gradual consolidation.

China Road Freight Transport Industry Leaders

-

Deppon Logistics Co., Ltd.

-

SF Express (KEX-SF)

-

Shanghai YTO Express (Logistics) Co., Ltd.

-

STO Express Co., Ltd. (Shentong Express)

-

ZTO Express (Cayman) Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2024: JD Logistics completed the acquisition of Kuayue Express for USD 892 million, enlarging its nationwide freight footprint.

- November 2024: SF Express opened cross-border facilities in Southeast Asia and Europe with a USD 200 million outlay, reinforcing export parcel lanes.

- October 2024: ZTO Express forged partnerships with regional carriers and earmarked USD 150 million for rural network expansion.

- September 2024: STO Express inaugurated automated sorting centers in multiple tier-2 cities at a cost of USD 120 million to raise parcel processing capacity.

China Road Freight Transport Market Report Scope

Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, Others are covered as segments by End User Industry. Domestic, International are covered as segments by Destination. Full-Truck-Load (FTL), Less than-Truck-Load (LTL) are covered as segments by Truckload Specification. Containerized, Non-Containerized are covered as segments by Containerization. Long Haul, Short Haul are covered as segments by Distance. Fluid Goods, Solid Goods are covered as segments by Goods Configuration. Non-Temperature Controlled, Temperature Controlled are covered as segments by Temperature Control.

End User Industry

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

Destination

| Domestic |

| International |

Truckload Specification

| Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) |

Containerization

| Containerized |

| Non-Containerized |

Distance

| Long Haul |

| Short Haul |

Goods Configuration

| Fluid Goods |

| Solid Goods |

Temperature Control

| Non-Temperature Controlled |

| Temperature Controlled |

| End User Industry | Agriculture, Fishing, and Forestry |

| Construction | |

| Manufacturing | |

| Oil and Gas, Mining and Quarrying | |

| Wholesale and Retail Trade | |

| Others | |

| Destination | Domestic |

| International | |

| Truckload Specification | Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) | |

| Containerization | Containerized |

| Non-Containerized | |

| Distance | Long Haul |

| Short Haul | |

| Goods Configuration | Fluid Goods |

| Solid Goods | |

| Temperature Control | Non-Temperature Controlled |

| Temperature Controlled |

Need A Different Region or Segment?

Customize Now

Market Definition

- Agriculture, Fishing, and Forestry (AFF) - This end user industry segment captures the external (outsourced) logistics expenditure incurred by the AFF industry players on road freight transport service. The end user players considered are the establishments primarily engaged in growing crops, raising animals, harvesting timber, harvesting fish & other animals from their natural habitats and providing related support activities. Herein, across the value chain, Logistics Service Providers (LSPs) play a crucial role in acquisition, storage, handling, transportation, and distribution activities for the optimal & continuous flow of inputs (seeds, pesticides, fertilizers, equipment, and water) from manufacturers or suppliers to the producers and smooth flow of output (produce, agro-goods) to distributors/ consumers. This includes both termperature controlled and non-temperature controlled logistics, as and when required according to the shelf life of goods being transported or stored.

- Construction - This end user industry segment captures the external (outsourced) logistics expenditure incurred by the construction industry players, on road freight transport service. The end user players considered are the establishments primarily engaged in constructing, repairing and renovating residential & commercial buildings, infrastructure, engineering works, subdividing and developing land. Logistics Service Providers (LSPs) play a crucial role in increasing profitability of construction projects by maintaing the inventory of raw materials & equipment, time-critical supplies and by providing other value added services for effective project management.

- Containerized Road Freight Transport - The segment captures the external (outsourced) logistics expenditure incurred by the road freight transport service end users on Full-Truck-Load (FTL) services. FTL road freight transport is characterized as a full single load not combined with other shipments. It comprises of shipments (i) devoted to the goods of a single shipper (ii) taken directly from a point of origin to one or more destination points (iii) comprising of bulk mail truck transportation (iv) comprising of both Container (Full Container Load, FCL)/Non-Container trucking services (v)comprsing of goods requiring temperature controlled or non-temperature controlled transportation services (vi) comprising of bulk liquid tankering (vii) invoving trucking of waste (viii) hazardous material trucking. Related value added services (VAS) of sorting, consolidation, deconslidation are included in the other services segment of freight and logistics market.

- Export Trends and Import Trends - Overall logistics performance of an economy is positively and significantly (statistically) correlated to its trade performance (exports and imports). Hence, in this industry trend, total value of trade, major commodities/ commodity groups and the major trade partners, for the studied geography (country or region as per the scope of report) have been analysed alongside the impact of major trade/logistics infrastructure investments & regulatory environment.

- Fluid Goods - The segment captures the external (outsourced) logistics expenditure incurred by the road freight transport service end users for the transport of bulk liquids, that are often used in extraction, manufacturing, food processing, agriculture industries among others. It includes transportation of liquids like (i) Chemicals/ hazardous goods (for instance acids) (ii) Water (potable as well as waste) (iii) Oil and gas (upstream as well as downstream like gasoline, fuel, crude oil, or propane), (iv) Food grade bulk liquids (like milk, or juice), (v) Rubber, (vi) Agrichemical products, among others. These goods are generally transported through tanker trucking.

- Fuel Price - Fuel price spikes can cause delays and diruption for logistics service providers (LSPs), while drops in the same can result in higher short-term profitability and increased market rivalry to offer consumers with the best deals. Hence, the fuel price variations have been studied over the review period and presented along with the causes as well as market impacts.

- Full-Truck-Load (FTL) Road Freight Transport - The segment captures the external (outsourced) logistics expenditure incurred by the road freight transport service end users on Full-Truck-Load (FTL) services. FTL road freight transport is characterized as a full single load not combined with other shipments. It comprises of shipments (i) devoted to the goods of a single shipper (ii) taken directly from a point of origin to one or more destination points (iii) comprising of bulk mail truck transportation (iv) comprising of both Container (Full Container Load, FCL)/Non-Container trucking services (v)comprsing of goods requiring temperature controlled or non-temperature controlled transportation services (vi) comprising of bulk liquid tankering (vii) invoving trucking of waste (viii) hazardous material trucking. Related value added services (VAS) of sorting, consolidation, deconslidation are included in the other services segment of freight and logistics market.

- GDP Distribution by Economic Activity - Nominal Gross Domestic Product and distribution of the same, across major economic sectors in the geography studied (country or region as per scope of the report) have been studied and presented in this industry trend. As GDP is positively related to the profitability and growth of logistics industry, this data has been used in adjunction to the input-output tables/ supply-use tables for analyzing the potential major contributing sectors towards the logistics demand.

- GDP Growth by Economic Activity - Growth of Nominal Gross Domestic Product across major economic sectors, for the geography studied (country or region as per scope of the report) have been presented in this industry trend. This data has been utilized for assessing the growth of logistics demand from all the market end users (economic sectors considered here).

- Inflation - Variations in both Wholesale Price Inflation (YoY change in producer price index) and Consumer Price Inflation have been presented in this industry trend. This data has been used to assess the inflationary environment as it plays a vital role in smooth functioning of the supply chain, directly impacting the logistics operational cost components e.g., pricing of tyres, driver wages & benefits, energy/fuel prices, maintenace costs, toll charges, warehousing rents, custom brokerage, forwarding rates, courier rates etc. hence impacting the overall freight and logistics market.

- Key Industry Trends - The report section named "Key Industry Trends" include all the key variables/parameters studied to better analyze the market size estimates and forecasts. All the trends have been presented in the form of data points (time series or latest available data points) along with analysis of the paramter in the form of concise market relevant commentary, for the geography studied (country or region as per the scope of report).

- Key Strategic Moves - The action taken by a company to differentiate from its competitor or used as a general strategy is referred to as a key strategic move (KSM). This includes (1) Agreements (2) Expansions (3) Financial Restructuring (4) Mergers and Acquisitions (5) Partnerships, and (6) Product Innovations. Key players (Logistics Service Providers, LSPs) in the market have been shortlisted, their KSM have been studied and presented in this section.

- Less than-Truck-Load (LTL) Road Freight Transport - The segment captures the external (outsourced) logistics expenditure incurred by the road freight transport service end users on Less than-Truck-Load (LTL) services. LTL road freight transport is characterized as multiple shipments combined onto a single truck for multiple deliveries within a network. It comprises of establishments (i) primarily engaged in general and specialized freight trucking of less than complete truck-loads, (ii) characterized by the use of terminals to consolidate shipments, generally from several shippers, into a single truck for haulage between a load assembly terminal and a disassembly terminal, where the load is sorted and shipments are re-routed for delivery (iv) Less than-Container-Load (LCL) shipping/ Groupage Shipping in case of trucking services. The activities in scope include (i) local pick-up, (ii) line-haul, and (iii) local delivery. Related value added services (VAS) of sorting, consolidation, deconslidation are included in the other services segment of freight and logistics market.

- Logistics Performance - Logistics Performance and Logistics Costs are the backbone of trade, and influences trade costs, making countries compete globally. Logistics performance is influenced by market wide adopted supply chain management strategies, government services, investments & policies, fuel/ energy costs, inflationary environment etc. Hence, in this industry trend, the logistics performance of the geography studied (country/ region as per the scope of report) has been analysed and presented over the review period.

- Major Truck Suppliers - Market share of truck brands is influenced by factors like geographical preferences, portfolio of truck types, truck prices, local production, truck repair & maintenance service peneteration, customer support, technological innovations (like electric vehicles, digitalization, autonomous trucks), fuel efficiency, financing options, annual maintenance costs, availability of substitutes, marketing startegies etc. Hence, the distribution (share % for base year of the study) of truck sales volume for leading truck brands and commentary on current market scenario & market anticipation over the forecast period have been presented in this industry trend.

- Manufacturing - This end user industry segment captures the external (outsourced) logistics expenditure incurred by the Manufacturing industry players, on road freight transport service. The end user players considered are the establishments primarily engaged in the chemical, mechanical or physical transformation of materials or substances into new products. Logistics Service Providers (LSPs) play a crucial role in maintaining a smooth flow of raw materials across the supply chain, enabling timely delivery of finished goods to distributors or end customers and storing & supplying the raw materials to clients for just-in-time manufacturing.

- Modal Share - Freight Modal Share is influenced by factors like modal productivity, government regulations, containerization, distance of shipment, temperature control requirements, type of goods, international trade, terrain, speed of delivery, shipment weight, bulk shipments, etc. Also, modal share by tonnage (tons) and modal share by freight turnover (ton-km) differ as per average distance of shipments, weight of major commodity groups transported in the economy and number of trips. This industry trend represents the distribution of freight transported by mode of transport (tons as well as ton-km), for the study base year.

- Oil and Gas, Mining and Quarrying - This end user industry segment captures the external (outsourced) logistics expenditure incurred by the extraction industry players, on road freight transport service. The end user players considered are the establishments that extract naturally occurring mineral solids, such as coal and ores; liquid minerals, such as crude petroleum; and gases, such as natural gas. Logistics Service Providers (LSPs) covers entire phases from upstream to downstream and plays a crucial role in the transportation of machinery, drilling equipments, extracted minerals, crude oil & natural gas and refined/ processed products from one place to another.

- Other End Users - Other end user segment captures the external (outsourced) logistics expenditure incurred by the financial services (BFSI), real estate, educational services, healthcare, and professional services (administrative, waste management, legal, architectural, engineering, design, consulting, scientific R&D), on road freight transport service. Logistics Service Providers (LSPs) plays a crucial role in the reliable movement of supplies and documents to/from these industries such as transporting any equipment or resources required, shipping confidential documents and files, movement of medical goods & supplies (surgical supplies and instruments, including gloves, masks, syringes, equipment) to name a few.

- Producer Price Inflation - It indicates inflation from viewpoint of the producers viz. the average selling price received for their output over a period of time. Annual change (YoY) of producer price index is reported as wholesale price inflation in the "Inflation" industry trend. As WPI captures dynamic price movements in most comprehensive way, it is widely used by governments, banks, industry, business circles and is deemed important in formulation of trade, fiscal and other economic policies. The data has been used in adjunction to consumer price inflation for better understanding the inflationary environment.

- Road Freight Pricing Trends - Freight pricing by mode of transport (USD/tonkm), over the review period, has been presented in this industry trend. The data has been used in assessing the inflationary environment, impact on trade, freight turnover (tonkm), road freight transport market demand and hence the road freight transport market size.

- Road Freight Tonnage Trends - Freight tonnage (weight of goods in tons) handled by mode of transport, over the review period, has been presented in this industry trend. The data has been used as one of the parameters apart from average distance per shipment (km), freight volume (tonkm), and freight pricing (USD/tonkm) to assess the freight transport market size.

- Road Freight Transport - Hiring a road freight transport logistics service provider (LSP) or haulier (outsourced logistics), for the transport of commodities constitutes road freight transport market. The scope of study includes (i) road transport of goods reported by hauliers registered in the reporting countries (ii) transport of raw materials or manufactured goods (solids as well as fluids) (iii) transport using commerical motor vehicles (rigid trucks or tractor-trailers, (iv) Full-Truck-Load (FTL) or Less than-Truck-Load (LTL) transport (v) containerized or non-containerized transport (vi) temperature controlled or non-temperature controlled trasnport, (vii) short haul or long haul (Over-the-road, OTR) transport, (viii) used office or household goods transport (movers and packers), (ix) other specialized cargo transport (dangerous goods, oversized cargo) and (x) outsourced first mile/ middle mile/last mile delivery shipments undertaken by road freight transport players. The scope does not include (i) transport undertaken by hauliers registered in other countries (ii) last mile meal delivery market (iii) grocery delivery market (iv) transportation via road network undertaken/ reported by Courier, Express, and Parcel (CEP) players.

- Road Length - As infrastructure plays a vital role in an economy's logistics performance, variables like length of roads, distribution of road length by surface category (paved v/s unpaved), distribution of road length by road classification (expressways v/s highways v/s other roads), have been analysed and presented in this industry trend.

- Segmental Revenue - Segmental Revenue has been triangulated or computed and presented for all the major players in the market. It refers to the road freight transport market specific revenue earned by the company, over the base year of study, in the geography studied (country or region as per the scope of report). It is computed through the study and analysis of major parameters like financials, service portfolio, employee strength, fleet size, investments, number of countries present in, major economies of concern, etc. that have been reported by the company in its annual reports, webpage. For companies having scarce financial disclosures, paid databases like D&B Hoovers, Dow Jones Factiva have been resorted to and verified through industry/expert interactions.

- Short Haul Road Freight Transport - The segment captures the external (outsourced) logistics expenditure incurred by the road freight transport service end users on local trucking (less than 100 miles). It includes the road transport of goods (i) within a single administrative area and its hinterland, (ii) by smaller trucks and pickup trucks (iii) via containerized as well as dry bulk services (iv) intermodal from ports, container terminals or airports, and (v) outsourced first mile/ last mile delivery shipments undertaken by road freight transport players.

- Transport and Storage Sector GDP - Value and growth of Transport and Storage Sector GDP has a direct relation to the freight and logistics market size, and hence road freight transport market size. Therefore, this variable has been studied and presented over the review period, in value terms (USD) and as share % of total GDP, in this industry trend. The data has been supported by concise and relevant commentary around the investments, developments, and current market scenario.

- Trends in E-Commerce Industry - Enhanced internet connectivity and boom in smartphone penetration, coupled with increasing disposable incomes, has led to a phenomenal growth in the e-commerce market globally. Online shoppers require fast and efficient delivery of their orders leading to an increase in the demand for logistics services especially e-commerce fulfilment services. Hence, the Gross Merchandise Value (GMV), historial and projected growth, breakup of major commodity groups in e-commerce industry for the studied geography (country or region as per scope of the report) have been analysed and presented in this industry trend.

- Trends in Manufacturing Industry - Manufacturing industry involves the transformation of raw materials into finished products, while logistics industry ensures the efficient flow of raw materials to the factory, and the transport of manufactured products to the distributors & consumers. Demand-Supply of both industries are highly cross-linked and critical for a seamless supply chain. Hence, the Gross Value Added (GVA), breakup of GVA into major manufacturing sectors, and growth of manufacturing industry over the review period have been analysed and presented, in this industry trend.

- Trucking Fleet Size By Type - Market share of truck types is influenced by factors like geographical preferences, major end user industries, truck prices, local production, truck repair & maintenance service peneteration, customer support, technological disruptions (like electric vehicles, digitalization, autonomous trucks) etc. Hence, the distribution (share % for base year of study) of truck parc volume by type of truck, market disruptors, truck manufacturing investments, truck specifications, truck use & import regulations, and market anticipation over the forecast period have been presented in this industry trend.

- Trucking Operational Costs - The prime reasons for measuring/ benchmarking logistics performance of any trucking company are to reduce operational costs and increase profitability. On the other hand, measuring operational costs helps to identify whether and where to make operational changes to control expenses and identify areas for improved performance. Hence, in this industry trend, trucking operational costs and the variables involved viz. driver wages & benefits, fuel prices, repairs & maintenance costs, tyre costs etc. have been studied over the base year of study, and presented for the geography studied (country or region as per the scope of report).

- Wholesale and Retail Trade - This end user industry segment captures the external (outsourced) logistics expenditure incurred by the wholesalers and retailers, on road freight transport service. The end user players considered are the establishments primarily engaged in wholesaling or retailing merchandise, generally without transformation, and rendering services incidental to the sale of merchandise. Logistics Service Providers (LSPs) plays a crucial role in the reliable movement of supplies to and finished products from production houses to the distributors and finally to the end customer covering activites like material sourcing, transportation, order fulfillment, warehousing & storage, demand forecasting, inventory management etc.

| Keyword | Definition |

|---|---|

| Cabotage | Road transport by a motor vehicle registered in a country performed on the national territory of another country. |

| Cross Docking | Cross docking is a logistics procedure where products from a supplier or manufacturing plant are distributed directly to a customer or retail chain with marginal to no handling or storage time. Cross docking takes place in a distribution docking terminal; usually consisting of trucks and dock doors on two (inbound and outbound) sides with minimal storage space. The name ‘cross docking’ explains the process of receiving products through an inbound dock and then transferring them across the dock to the outbound transportation dock. |

| Cross Trade | International road transport between two different countries performed by a road motor vehicle registered in a third country. A third country is a country other than the country of loading/embarkation and than the country of unloading/disembarkation. |

| Dangerous Goods | The classes of dangerous goods carried by Road are those defined by the fifteenth revised edition of the UN Recommendations on the Transport of Dangerous Goods, United Nations, Geneva 2007. They include Class 1: Explosives; Class 2: Gases; Class 3: Flammable Liquids; Class 4: Flammable solids- substances liable to spontaneous combustion; substances which, on contact with water, emit flammable gases; Class 5: Oxidizing substances and organic peroxides; Class 6: Toxic and infectious substances; Class 7: Radioactive material and Class 8: Corrosive substances, Class 9: Miscellaneous dangerous substances and articles. |

| Direct Shipment | Direct shipment is a method of delivering goods from the supplier or the product owner to the customer directly. In most cases, the customer orders the goods from the product owner. This delivery scheme reduces transportation and storage costs, but requires additional planning and administration. |

| Drayage | A drayage is a form of trucking service that connects the different modes of shipping (intermodal), such as ocean freight or air freight. It’s a short-haul trip that transports goods from one place to another, usually before or after its long-haul shipping process. Drayage trucks move cargo to and from various destinations, such as container ships, storage lots, order fulfillment warehouses, and rail yards. Typically, drayage only transports goods in short distances and operates only in one metropolitan area. It also requires only one trucker in a single shift. But despite this, but it plays an important role in long-haul shipping because it gets the goods to the cargo and vice versa. It makes intermodal transport much more efficient and enables the seamless transfer of goods to the end customer. |

| Dry van | A dry van is a type of semi-trailer that's fully enclosed to protect shipments from outside elements. Designed to carry palletized, boxed or loose freight, dry vans aren't temperature-controlled (unlike refrigerated “reefer” units) and can't carry oversized shipments (unlike flatbed trailers). |

| Final Demand | Final demand includes all types of commodities (goods as well as services) consumed as final use and might include personal consumption, or consumption by government, by businesses as capital investment, and as exports. includes all types of commodities (goods as well as services) consumed as final use and might include personal consumption, or consumption by government, by businesses as capital investment, and as exports. |

| Flatbed Truck | A flatbed truck is a type of truck with rigid design. It has a back body that is flatly shaped for easy loading and unloading of goods. The flatbed truck is mostly used to transport heavy, oversized, wide and indelicate goods such as machinery, building supplies or equipment. Due to the truck open body, the goods transported with it must not be vulnerable to rain. By functionality, the flatbed truck is comparable to a flatbed trailer. |

| Inbound Logistics | Inbound logistics is the way materials and other goods are brought into a company. This process includes the steps to order, receive, store, transport and manage incoming supplies. Inbound logistics focuses on the supply part of the supply-demand equation. |

| Intermediate Demand | Intermediate demand includes goods, services, and maintenance and repair construction sold to businesses, excluding capital investment. |

| International Loaded | Place of loading of goods in reporting country (i.e., country in which the vehicle performing the transport is registered) and place of unloading in a different country. |

| International Unloaded | Place of unloading of goods in reporting country (i.e., country in which the vehicle performing the transport is registered) and place of loading in a different country. |

| OOG cargo | Out of Gauge (OOG) cargo is any cargo that can not be loaded into six-sided shipping containers simply because it is too large. The term is a very loose classification of all cargo with dimensions beyond the maximum 40HC container dimensions. That is a length beyond 12.05 meters – a width beyond 2.33 meters – or a height beyond 2.59 meters. |

| Pallets | Raised platform, intended to facilitate the lifting and stacking of goods. |

| Part load | A part load describes goods which only fills a truck partially. In essence, the quantity of the shipment is bigger than the Less Than Truckload (LTL) shipment. Also, the shipment cannot fully occupy a truck i.e. its capacity is much lower than a Full Truckload (FTL) shipment. |

| Paved Road | Road surfaced with crushed stone (macadam) with hydrocarbon binder or bituminized agents, with concrete or with cobblestone. |

| Reverse Logistics | Reverse logistics comprises of the sector of supply chains that process anything returning inwards through the supply chain or traveling ‘backward’ through the supply chain. |

| Road Freight Transport Service | Hiring a trucking agency for transport of commodities (raw materials or manufactured goods including both solids and liquids) form the origin to a destination within the country (domestic) or cross-border (international) constitutes road freight transport market. The service might be Full-Truck-Load or Less than-Truck-Load, containerized or non-containerized, temperature controlled or non temperature controlled, short haul or long haul. |

| Tautliner vehicle | Tautliner and curtainsider are used as generic names for curtain sided trucks/trailers. The curtains are permanently fixed to a runner at the top and detachable rails/poles at front and rear, allowing the curtains to be drawn open and forklifts used all along the sides for easy and efficient loading and unloading. When closed for travel, vertical load restraint straps are attached to a rope rail beneath the truck bed, connecting the truck bed and curtain along both sides. Winches at either end of the curtain tension it, hence the 'Tautliner' name. This stops the curtain from flapping or drumming in the wind and can also help retain light loads from slipping sideways. |

| Transport for hire or reward | The carriage for remuneration of goods. |

| Unpaved Road | Road with a stabilized base not surfaced with crushed stone, hydrocarbon binder or bituminized agents, concrete or cobblestone. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is considered to be a part of the pricing, and the average selling price (ASP) is varying throughout the forecast period for each country

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF