Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Volume (2025) | 15.14 Million tons |

| Market Volume (2030) | 18.65 Million tons |

| Growth Rate (2025 - 2030) | 4.26% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Plastic Packaging Market Analysis by Mordor Intelligence

The China plastic packaging market size is 15.14 million tons in 2025 and is projected to reach 18.65 million tons by 2030, translating to a 4.26% CAGR. Sustained e-commerce expansion, cold-chain penetration, and recycled-content mandates underpin the steady trajectory, while down-gauging techniques and digital printing bolster cost efficiency and brand agility. Stiffer provincial VOC rules raise compliance costs, but smart-factory investments in inland clusters cut freight lead-times and unlock new customers. Multinational majors and well-capitalized domestic players are therefore widening competitive moats, even as carbon-border measures reshape export flows. Overall, the China plastic packaging market balances regulatory rigor with innovation to remain resilient in a fast-evolving consumer economy.[1]China Packaging Federation, “Industry Development Report 2024,” CPP114.COM

Key Report Takeaways

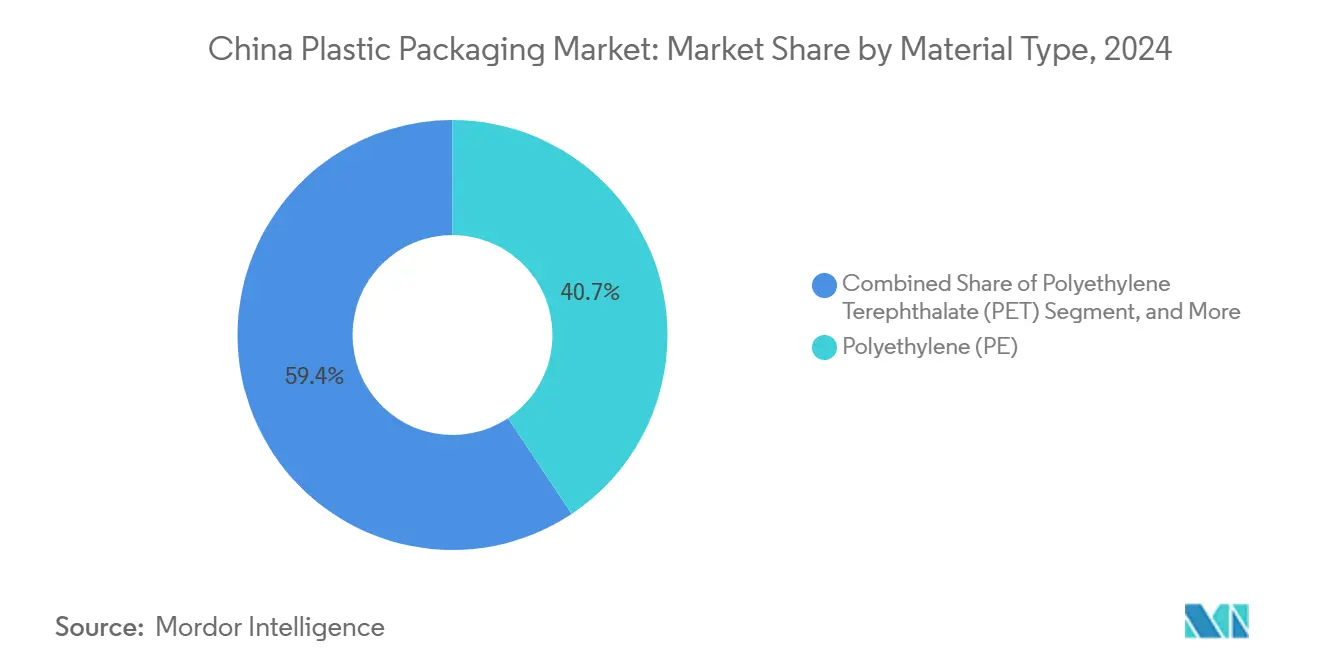

- By material type, polyethylene held 40.65% of the China plastic packaging market share in 2024, while polyethylene terephthalate is advancing at a 6.32% CAGR through 2030.

- By packaging type, flexible formats commanded 55.86% revenue share in 2024; the same segment is growing at a 6.75% CAGR to 2030.

- By product form, pouches and sachets accounted for 36.36% of the China plastic packaging market size in 2024 and films and wraps are expanding at a 5.21% CAGR through 2030.

- By end-user industry, food packaging led with 29.42% share in 2024, whereas cosmetics and personal care are forecast to climb at a 6.56% CAGR to 2030.

- By manufacturing process, extrusion held 27.43% share in 2024, while thermoforming is on track for a 5.78% CAGR to 2030.

China Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from e-commerce logistics and cold-chain food distribution | +1.2% | National – tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Mandatory recycled-content quotas in China’s 2025 Plastic-Pollution Action Plan | +0.8% | National – stricter in eastern provinces | Medium term (2-4 years) |

| Down-gauging and mono-material shift lowering resin costs for converters | +0.7% | National – coastal hubs | Medium term (2-4 years) |

| High-speed digital printing unlocking SKU proliferation for FMCG brands | +0.6% | Consumer-goods clusters nationwide | Short term (≤ 2 years) |

| Capital migration from coastal to inland smart-factory clusters cutting freight lead-times | +0.5% | Central and western China | Long term (≥ 4 years) |

| E-commerce logistics drive packaging innovation | +0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Logistics Drive Packaging Innovation

China’s online retail sales surpassed CNY 13 trillion (USD 1.8 trillion) in 2024, compelling converters to supply protective yet lightweight formats that survive automated sortation and long cross-country hauls.[2]National Bureau of Statistics, “E-commerce Transaction Volume 2024,” STATS.GOV.CN Cold-chain parcel volume grew 23% in 2024, spurring demand for high-barrier films and temperature-monitoring smart labels. Brands also seek packaging that elevates unboxing experiences, nudging suppliers toward mono-material laminate pouches compatible with recycling streams. As e-commerce platforms tighten sustainability targets, converters investing in thinner gauges and curbside-recyclable designs capture contracts from leading marketplaces. In parallel, investment in printed QR codes enables real-time traceability, strengthening consumer trust and supply-chain visibility.

Recycled-Content Mandates Reshape Material Flows

The 2025 Plastic-Pollution Action Plan requires 30% recycled content in most packaging by 2026, immediately tightening supply of food-grade rPET and rPE. Sinopec and CNPC committed over CNY 5 billion (USD 700 million) to chemical-recycling lines that upcycle post-consumer bottles into virgin-equivalent pellets. Price premiums for certified recycled resin reached 8-12% over virgin grades in 2024, pressuring converters’ margins yet rewarding vertically integrated players with captive recycling. Certifications under ISO 14855 on biodegradability gain traction as alternate compliance pathways, particularly for flexible films targeting fresh-food and snack markets. The policy environment effectively accelerates consolidation, given that small converters struggle to secure consistent recycled feedstock at viable prices.

Down-Gauging Technologies Reduce Material Consumption

Multi-layer co-extrusion and advanced resin formulations now allow converters to shave 15-20% thickness in common stand-up pouches without compromising oxygen or moisture barriers. Material savings translate into roughly 12-15% cost reduction per unit for high-volume SKUs. Mono-material laminates are gaining because they eliminate polyethylene-to-nylon adhesive layers, simplifying after-use recycling. Big converters are procuring precision dies and optical sensors that ensure tight gauge control, whereas smaller firms face capital constraints that limit adoption. International brands reward down-gauged packaging by allocating supply awards to converters that document material reduction under life-cycle-assessment frameworks, reinforcing the trend.

High-Speed Digital Printing Enables Mass Customization

Press speeds exceeding 120 m/min coupled with variable-data software let converters print batch-size-one jobs profitably. Cosmetics and personal-care brands leverage the capability to launch seasonal designs, QR-linked loyalty programs, and language-localized SKUs without plate-making delays. Food and beverage companies leverage digital presses certified for food contact to release limited-edition runs tied to sports events and festivals. The equipment also dovetails with Industry 4.0 workflows, allowing web-inspection AI to adjust color in real time. Resulting lead-time reductions improve inventory turnover and cut obsolete stock, a benefit that resonates with retailers demanding agile supply.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in polyolefin feedstock pricing linked to crude-oil cycles | -0.9% | Nationwide – import-dependent regions | Short term (≤ 2 years) |

| Stricter provincial VOC caps raising compliance capex for small converters | -0.6% | Eastern and southern provinces | Medium term (2-4 years) |

| EU CBAM and US green-tariff exposure eroding export competitiveness | -0.4% | Coastal exporters | Long term (≥ 4 years) |

| Feedstock price volatility pressures margins | -0.3% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility Pressures Margins

Polyolefin spot prices swung 25-30% during 2024, echoing crude-oil turbulence and periodic cracker shutdowns. While tier-one converters hedge through long-term supply contracts and financial derivatives, smaller players lack balance-sheet depth, forcing them to absorb cost spikes or cede orders. Volatility complicates fixed-price agreements with brand owners that insist on cost stability. Consequently, converters diversify into recycled resins and bio-based alternatives to buffer against petrochemical swings, though these materials remain costlier. Heightened input uncertainty may accelerate merger activities as financially stressed firms seek buyers with stronger procurement leverage.

Environmental Compliance Costs Burden Small Players

In 2024, eastern provinces cut VOC emission limits to 50 mg/m³ for flexographic and gravure printing, compelling installation of regenerative thermal oxidizers priced at CNY 2-5 million (USD 280,000-700,000) per line. Continuous monitoring and reporting further add OPEX complexity. Global majors with ISO 14001 systems absorb the spend, but family-owned converters often shut older lines, hastening industry consolidation. Some migrate to inland provinces with more lenient interim standards, yet local governments increasingly harmonize rules, narrowing arbitrage windows. Net-net, compliance requirements tilt competitive advantage toward scale players able to amortize environmental expenditures across high output volumes.

Segment Analysis

By Material Type: PET Recycling Drives Growth Acceleration

Polyethylene continued to command 40.65% of the China plastic packaging market size in 2024, underpinned by its processability and cost advantage across food pouches, stretch films, and commodity containers. Polyethylene terephthalate is the clear volume gainer, propelled by a 6.32% CAGR to 2030, as beverage bottlers embrace closed-loop recycling and cosmetics brands prefer transparent, premium-looking jar .

Multi-layer barrier coatings now elevate PET’s oxygen-scavenging properties, opening doors in medicine and high-value cosmetics. Chemical recycling platforms co-developed by Sinopec produce 100,000 tons per year of food-grade rPET pellets, directly feeding converters with secure supply. Conversely, polystyrene is losing share because dine-in chains shun foam clamshells to meet provincial bans. Bio-based PLA, PHA, and other niche resins gain pilot-scale traction in cutlery and snack wrappers, yet their collective volume remains below 2% of the market given higher cost and processing barriers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Packaging Type: Flexible Solutions Dominate Innovation

Flexible formats comprised 55.86% of the overall volume in 2024 and are forecast to outpace rigid alternatives at a 6.75% CAGR. Brands appreciate lower shipping costs, evolving from 20 g PET bottles to 8 g mono-PE spouted pouches for household cleaners. At the same time, recyclability gains as single-material laminates replace mixed-substrate snack bags.

Rigid packaging retains relevance in carbonated drinks, injectables, and heavy-duty industrial polymer drums where structural integrity is paramount. Lightweighting in blow-molded bottles has trimmed gram weights by 10% since 2023, but flexible stand-up pouches still undercut total packaging mass by at least 30%. Moreover, flexible form-fill-seal systems facilitate shorter production runs aligned with mass-customized marketing, whereas rigid lines demand higher changeover cost and downtime.

By Product Form: Films Drive E-Commerce Growth

Pouches and sachets led with 36.36% share in 2024 owing to portion-control convenience across condiments, nutraceuticals, and trial-size cosmetics. Yet, stretch and shrink films are expanding faster, riding a 5.21% CAGR as omnichannel retailers wrap mixed-SKU parcels and perishable food crates for cross-provincial shipping.

Advances in nano-clay and EVOH co-extrusion provide high oxygen barriers while preserving transparency, essential for ready-meal trays displayed through last-mile cold-chain. Films also benefit from post-industrial scrap recycling loops that are simpler than multi-layer pouches. Bottles remain the workhorse for beverages and OTC pharmaceuticals, but composite materials like PET-aluminum integrate foil layers, complicating recovery. Trays gain share in premium bakery and fresh-cut produce, especially when thermoformed from rPET sheets certified for direct food contact.

By End-User Industry: Cosmetics Accelerate Premium Trends

Food maintained a 29.42% lead in 2024, fueled by the spread of convenience retail formats and frozen meal uptake across urban centers. Yet cosmetics and personal-care products are sprinting ahead, rising at a 6.56% CAGR as Gen-Z consumers gravitate toward premium serums packaged in glossy, recyclable containers.

Sustainability messaging drives refill-and-reuse schemes for skin-care jars, often executed with mono-material PP inserts that snap into decorated outer shells. Beverage players push toward aseptic pouches for dairy and functional drinks, partly to cut cold-chain logistics. Pharmaceuticals rely on stringent ISO-class cleanroom packaging, cushioning demand for multilayer blister packs and injection vials. Industrial segments such as automotive lubricants and agrochemicals increasingly specify UN-certified drums molded from high-molecular-weight HDPE to satisfy hazardous-goods transit rules.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Manufacturing Process: Thermoforming Gains Precision Applications

Extrusion held a 27.43% share in 2024 on its ubiquity for film and sheet production that feeds bag-making, lamination, and thermoforming. Thermoforming, however, is growing fastest at 5.78% CAGR because retailers demand rigid trays with intricate geometry for shelf-ready presentation.

Modern servo-driven thermoformers cut cycle times while slashing trim waste, allowing thinner gauges and rPET content exceeding 60%. Injection molding supports fine-thread bottle necks and child-resistant caps for pharmaceuticals, whereas stretch-blow molding sustains light-weighted PET bottles. Industry 4.0 deployments integrate sensors and predictive analytics across extrusion, printing, and converting lines, enabling closed-loop process adjustments that boost yields and reduce off-grade scrap.

Geography Analysis

Eastern seaboard provinces Shanghai, Jiangsu, and Zhejiang produced roughly 60% of the China plastic packaging market in 2024, leveraging dense supplier parks, skilled labor, and port access. Pearl River Delta clusters in Guangdong specialize in export-oriented rigid containers and industrial sacks but face escalating wage bills and stringent emission controls.

Central megacities such as Chongqing, Chengdu, and Wuhan now attract greenfield investments with 30% lower land costs and newly commissioned high-speed rail lines that compress east-west transit to under 48 hours. Government tax breaks and renewable-power availability bolster project economics, prompting majors to relocate growth capacity inland. This inland pivot enables consumer-goods brands to replenish western store shelves faster, trimming stock-out risk.

Northern provinces including Hebei and Tianjin concentrate on medical, pharmaceutical, and frozen-food applications, benefitting from proximity to national drug manufacturers and grain processing hubs. Yet heightened air-quality campaigns enforce stricter VOC baselines, compelling converters to upgrade solvent-based ink lines or switch to water-based systems. Border regions adjoining ASEAN capture incremental demand by exporting laminates and wraps under the Regional Comprehensive Economic Partnership, though compliance with origin rules requires localized resin sourcing.

Competitive Landscape

The China plastic packaging market is moderately concentrated, with the top five groups controlling roughly 45-50% of domestic output. Amcor, Berry Global, and Huhtamaki retain technological leadership via high-barrier structures, digital printing assets, and food-grade recycling plants. Domestic challengers Zhuhai Zhongfu, COFCO Packaging, and Southern Packaging Group leverage agile decision-making and low overhead to under-price imports while meeting strict lead-times.[3]Shanghai Stock Exchange, “Listed Company Performance Analysis 2024,” SSE.COM.CN

Sustainability is a focal point of competition. COFCO’s chemical-recycling venture with Sinopec guarantees captive rPET supply, underpinning beverage contracts. Amcor’s Suzhou expansion lifts flexible-pack capacity by 40% and introduces solvent-free lamination that aligns with provincial emission caps. Berry Global’s 2024 buy-out of Guangdong Danjia adds rigid tubs and thin-wall IML know-how, broadening its FMCG portfolio.

Innovation intensity is rising: Chinese converters filed 34% more packaging patents in 2024 than 2023, with emphasis on barrier coatings, bio-based resins, and digital-workflow automation. Capital expenditure increasingly flows to robotics and AI-powered inspection, elevating consistent quality while mitigating labor shortages. Exporters, however, face looming EU CBAM levies that favor converters able to certify low-carbon footprints.

China Plastic Packaging Industry Leaders

-

Amcor plc

-

Huhtamaki Oyj

-

Sealed Air Corporation

-

Winpak Ltd.

-

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Amcor announced a CNY 800 million (USD 112 million) expansion of its Suzhou plant to lift flexible packaging capacity by 40%, including chemical-recycling and digital-printing modules.

- December 2024: Berry Global completed the CNY 1.2 billion (USD 168 million) acquisition of Guangdong Danjia Plastic Packaging to deepen rigid-pack exposure in southern China.

- November 2024: Huhtamaki invested CNY 600 million (USD 84 million) in a new thermoforming site in Chengdu aimed at food-service and ready-meal contracts in western China.

- October 2024: COFCO Packaging launched a CNY 500 million (USD 70 million) rPET joint venture with Sinopec to service beverage clients under recycled-content mandates.

China Plastic Packaging Market Report Scope

Plastics have been a dominant choice for packaging material because of their performance, cost-effectiveness, and durability. In China, industries such as food, beverage, and pharmaceuticals frequently opt for plastic packaging, valuing its benefits in safeguarding against contamination, ensuring preservation, and offering transportation flexibility. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The China plastic packaging market report is segmented by packaging type (flexible packaging (by product type (pouches, bags, films and wraps and other product types), and end-user industry (food, beverage, healthcare, cosmetics and personal care, household care, and other end-use industries (industrial, e-commerce among others)), rigid plastic packaging (by product type (bottles and jars, trays and containers, caps and closures, and other product types), and end-use industries (food, beverage, healthcare, cosmetics and personal care, household care, and other end-use industries (industrial, automotive among others))). The market sizing and forecasts are provided in terms of volume (tons) for all the above segments.

By Material Type

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Polystyrene and EPS |

| Other Material Types |

By Packaging Type

| Flexible Plastic Packaging |

| Rigid Plastic Packaging |

By Product Form

| Bottles and Jars |

| Trays and Containers |

| Pouches and Sachets |

| Bags and Sacks |

| Films and Wraps |

| Other Product Forms |

By End-User Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

By Manufacturing Process

| Extrusion |

| Injection Molding |

| Blow Molding |

| Thermoforming |

| By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polystyrene and EPS | |

| Other Material Types | |

| By Packaging Type | Flexible Plastic Packaging |

| Rigid Plastic Packaging | |

| By Product Form | Bottles and Jars |

| Trays and Containers | |

| Pouches and Sachets | |

| Bags and Sacks | |

| Films and Wraps | |

| Other Product Forms | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceuticals and Healthcare | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-user Industries | |

| By Manufacturing Process | Extrusion |

| Injection Molding | |

| Blow Molding | |

| Thermoforming |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast is the China plastic packaging market expected to grow through 2030?

Volume is projected to expand from 15.14 million tons in 2025 to 18.65 million tons by 2030, reflecting a 4.26% CAGR.

Which packaging format is expanding quickest in China?

Flexible solutions, especially stand-up pouches and high-barrier films, are leading growth at a 6.75% CAGR to 2030.

What role does recycled PET play in beverage packaging?

Recycled PET is gaining traction because the 2025 Plastic-Pollution Action Plan mandates 30% recycled content, prompting chemical-recycling investments and supply agreements with beverage bottlers.

Why are inland provinces attracting new packaging plants?

Lower land costs, improved rail links, and tax incentives cut freight lead-times and operating expenses, enticing converters to relocate capacity from the crowded coast.

How are converters mitigating feedstock price swings?

Larger players hedge long-term resin contracts, diversify into recycled materials, and invest in process efficiencies that reduce resin consumption by up to 20%.

Which end-user segment is set to outpace food in growth terms?

Cosmetics and personal care packaging is poised for a 6.56% CAGR, fueled by premium product launches and consumer preference for sustainable, visually appealing packs.

Page last updated on: