Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

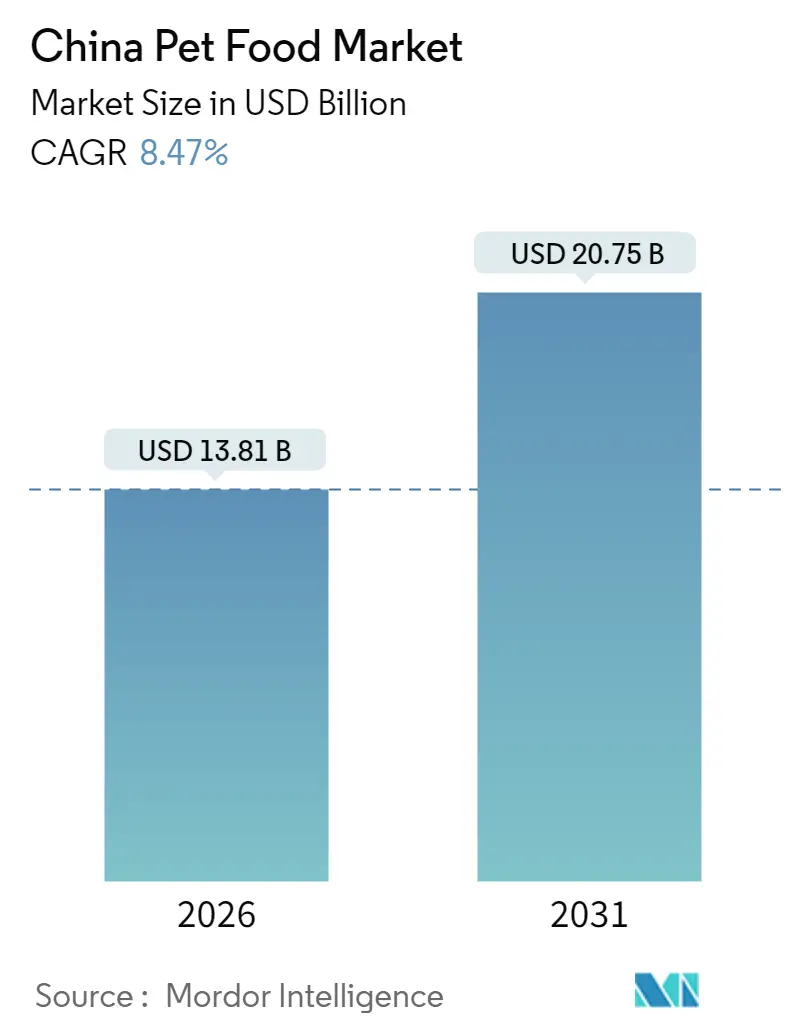

| Market Size (2026) | USD 13.81 Billion |

| Market Size (2031) | USD 20.75 Billion |

| Growth Rate (2026 - 2031) | 8.47% CAGR |

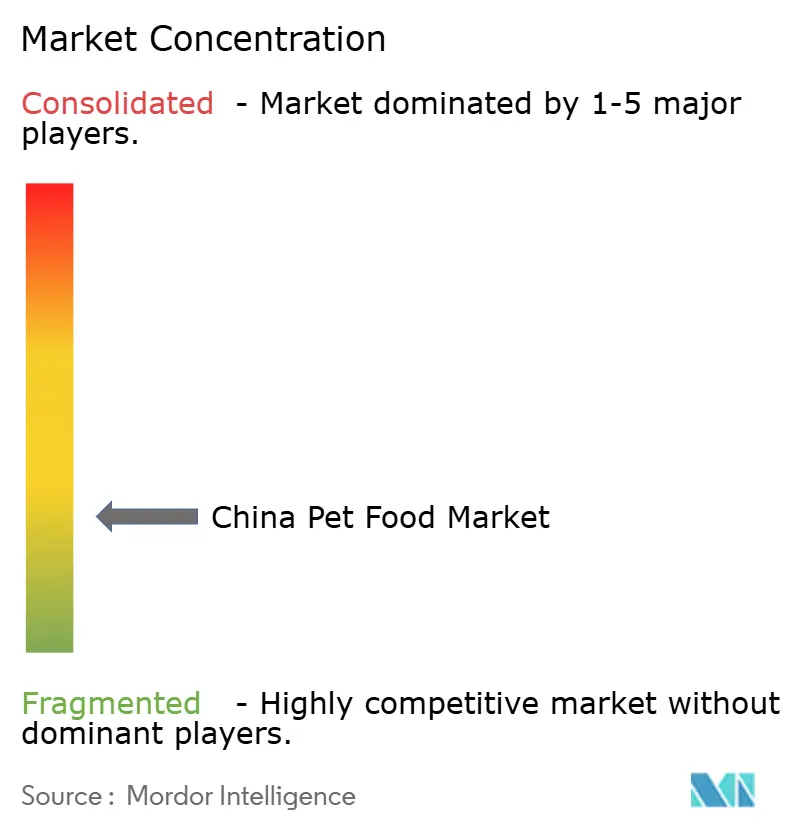

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Pet Food Market Analysis by Mordor Intelligence

The China pet food market was valued at USD 12.73 billion in 2025 and estimated to grow from USD 13.81 billion in 2026 to reach USD 20.75 billion by 2031, at a CAGR of 8.47% during the forecast period (2026-2031). Premium formulations, direct-to-consumer innovation, and functional positioning elevate average selling prices while urbanization and rising disposable income expand the pet-owning population. Domestic manufacturers scale freeze-dried capacity to capture value in high-margin treat formats, and livestreaming commerce compresses the path from product discovery to purchase, allowing niche brands to compete head-on with multinational incumbents. Regulatory tightening around labeling and ingredient traceability reinforces consumer trust, helping premium and therapeutic diets gain share even in price-sensitive Tier-3 markets. Raw material cost volatility and carbon-neutral compliance outlays temper margins but simultaneously spur technology upgrades and supply-chain diversification.

Key Report Takeaways

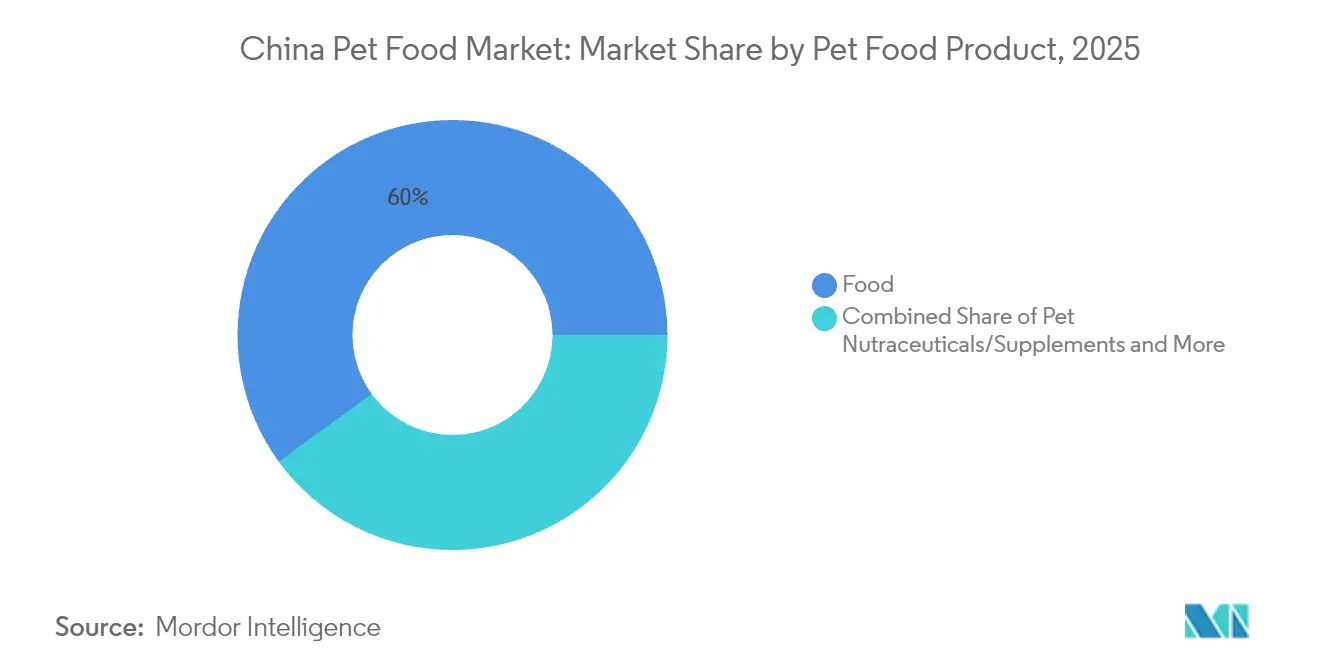

- By pet food product, food captured 60.02% of the China pet food market size in 2025 and is projected to expand at a 9.21% CAGR through 2031.

- By type, pets, dogs held a 42.25% share of the China pet food market size in 2025, while cats are forecast to grow at a 10.56% CAGR between 2026 and 2031.

- By distribution channel, online platforms accounted for a 59.10% share of the China pet food market size in 2025. The channel is forecast to grow at a 9.88% CAGR by 2031.

- The Chinese pet food market features a highly fragmented competitive landscape, comprising a mix of global multinational corporations and regional players. Global conglomerates such as Mars, Incorporated, Nestlé, ADM, Clearlake Capital Group, L.P. (Wellness Pet Company, Inc.), and General Mills maintain a significant market presence, accounting for an 11.05% share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Pet Food Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated premiumization of cat and dog diets | +2.1% | Tier-1 cities with spillover to Tier-2 markets | Medium term (2-4 years) |

| Rise of DTC (Direct-to-Customer) digital-native pet-food brands | +1.8% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Growth of functional/therapeutic nutrition positioning | +1.5% | Tier-1 and Tier-2 cities, veterinary channels | Long term (≥ 4 years) |

| Human-grade ingredient sourcing mandates from Tier-1 retailers | +1.2% | Major metropolitan areas, premium retail chains | Medium term (2-4 years) |

| Expansion of domestic freeze-dried capacity in Tier-3 cities | +0.9% | Shandong, Hebei, and Henan provinces | Long term (≥ 4 years) |

| Cross-border live-stream commerce for exotic pet diets | +0.6% | Tier-1 cities, affluent consumer segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Accelerated Premiumization of Cat and Dog Diets

Premium formats expanded 18-22% in 2024 as pet owners traded up to limited-ingredient, organic, and veterinary-endorsed formulas that command price premiums of 40-60% over standard kibble [1]Source: Shanghai Consumer Research Institute, “Premium Pet Food Consumer Survey 2024,” scri.org.cn. Tier-1 consumers tie product choice to food-safety credentials and novel proteins, such as insect- or plant-based sources, that support digestive and allergy management. Clearer feed-safety standards issued by the Ministry of Agriculture and Rural Affairs specify protein quality and traceability norms, giving retailers confidence to merchandise high-end lines. The premium wave lifts the China pet food market by raising average spend per pet and encourages manufacturers to invest in research and packaging upgrades that justify higher price points. Spillover into Tier-2 markets is already visible as household income growth narrows the affordability gap and social media accelerates trend diffusion. The premiumization narrative, therefore, underpins both volume stability and margin expansion for branded producers.

Rise of DTC (Direct-to-Customer) Digital-Native Pet-Food Brands

Digital-native players secured a roughly 12-15% share in 2024 by selling exclusively through Tmall, JD, and Xiaohongshu storefronts, where same-day delivery and data-driven personalization foster repeat purchases. Subscription bundles reduce inventory risk and deliver predictable cash flow, while interactive livestreams strengthen community engagement that traditional mass-media advertising cannot match. Consumer review ecosystems reward transparency and rapid product iteration, enabling start-ups to roll out new SKUs in as little as six weeks. Logistics partnerships with JD Logistics and Cainiao reduce last-mile costs and extend cold-chain coverage for fresh and raw food products. The China pet food market, therefore, experiences a structural shift as brand equity migrates from above-the-line campaigns to digital intimacy and customer lifetime value analytics. Established multinationals respond with joint ventures and minority investments to capture DTC (Direct-to-Consumer) know-how without diluting existing retail channels.

Growth of Functional/Therapeutic Nutrition Positioning

Functional diets targeting renal support, digestive care, or allergen management increased by 25-30% in 2024, driven by a veterinary network that now exceeds 15,000 hospitals nationwide. Clinical research partnerships validate ingredient efficacy, making health claims more defensible under guidelines from the State Administration for Market Regulation. Prescription-only formulas secure high loyalty because substitutions are discouraged during treatment protocols. As pets age, owners adopt preventive solutions such as joint-care kibble enriched with glucosamine or cognition-support treats fortified with medium-chain triglycerides. Functional positioning enables manufacturers to charge premiums that mitigate raw-material volatility, thereby sustaining China's pet food market expansion even when volume growth moderates. Innovation pipelines also benefit from proprietary ingredient supply agreements that raise entry barriers for similar brands.

Human-Grade Ingredient Sourcing Mandates from Tier-1 Retailers

Retailers, including Sam’s Club China and Costco China, require third-party certificates that confirm raw materials meet human food standards. Suppliers spend RMB 500,000-2 million (USD 70,000-280,000) annually on audits and laboratory testing, yet gain premium shelf visibility and export-market credentials. QR-coded traceability enables consumers to track the farm-to-bowl journey, reducing recall risk and reinforcing trust in domestic production. Compliance advantages concentrate sales among larger players with robust quality management systems, which in turn accelerates consolidation in the Chinese pet food market. Smaller factories are adopting lean manufacturing and co-manufacturing arrangements to offset certification costs and stay competitive with evolving retail scorecards. Over time, the mandate sharpens the differentiation between mass-market and premium tiers, raising the overall baseline for food safety.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility for poultry and fish meals | -1.4% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Rising regulatory scrutiny on labeling claims | -0.8% | National, stricter enforcement in Tier-1 cities | Medium term (2-4 years) |

| Intensifying competition from home-made fresh diets | -0.6% | Tier-1 and Tier-2 cities, educated consumers | Long term (≥ 4 years) |

| Carbon-neutral factory compliance costs | -0.4% | Industrial zones, manufacturing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility for Poultry and Fish Meals

Protein inputs fluctuated by 15-25% in 2024 due to disruptions from avian flu and uncertainty over fishing quotas, leading to selective retail price hikes that risk compromising demand elasticity. Poultry meal peaked at RMB 8,500 (USD 1,200) per metric ton before sliding to RMB 7,200 (USD 1,015), yet forward contracts remain scarce, compelling spot purchases. Fish meal reached RMB 16,000 (USD 2,255) at seasonal highs, squeezing manufacturers already investing in packaging upgrades. Brands diversify into insect protein and pea concentrate to hedge volatility, but reformulation cycles absorb R&D bandwidth. Although the Chinese pet food market retains its volume momentum, profit pools are compressing for value brands that cannot fully pass through their costs.

Rising Regulatory Scrutiny on Labeling Claims

SAMR (State Administration for Market Regulation) issued 847 violation notices and levied fines of RMB 23.4 million (USD 3.3 million) in 2024 for misleading health claims, prompting a wave of packaging revisions and legal reviews [2]Source: State Administration for Market Regulation, “Pet Food Regulatory Enforcement Report 2024,” samr.gov.cn . Companies must submit clinical trial evidence or peer-reviewed studies to substantiate statements around hip-joint support or allergen reduction. Compliance outlays of RMB 200,000-800,000 (USD 28,000-113,000) weigh heavily on start-ups with thin capital reserves. Tightened oversight raises consumer confidence but delays product launches and shortens marketing copy, constraining the premium perceptions. Non-compliant inventory faces recall risk, adding working-capital strain.

Segment Analysis

By Pet Food Product: Food Dominance Drives Market Foundation

Food products maintain commanding market leadership with a 60.02% China pet food market size in 2025, reflecting their essential role in daily pet nutrition and broad consumer accessibility across price points. This significant market position is primarily driven by the fact that the segment is a staple purchase for most pet owners, regardless of their pet's breed, size, or age.

The segment's 9.21% CAGR through 2031, benefits from premiumization trends as consumers upgrade from basic kibble to specialized formulations featuring novel proteins, functional ingredients, and life-stage targeting. Dry pet food, particularly kibble formats, represents the largest subsegment due to convenience, shelf stability, and cost-effectiveness for multi-pet households. Wet pet food experiences accelerating growth as urbanization increases demand for portion-controlled, palatability-enhanced options that appeal to finicky eaters and senior pets requiring softer textures.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Pet Type: Dogs Lead While Cats Accelerate Growth

Dogs command 42.25% of the Chine pet food market size in 2025, reflecting their historical dominance in Chinese pet ownership and higher average spending per animal on premium nutrition products. The growth differential reflects changing demographics and lifestyle preferences among Chinese pet owners, with cats gaining favor among millennials and Gen Z consumers who prioritize convenience and emotional companionship over traditional pet ownership models. Major pet food manufacturers in China have responded to this trend by offering premium products, including specialized veterinary diets and grain-free options, targeting urban pet owners who are more willing to spend on high-quality dog food products.

Cats demonstrate superior growth momentum with a 10.56% CAGR through 2031, driven by urban lifestyle compatibility and rising single-person household adoption rates in Tier-1 cities. Cat ownership appeals particularly to younger consumers who value lower maintenance requirements and apartment-friendly characteristics, creating sustained demand for specialized feline nutrition products, including hairball control, urinary health, and indoor lifestyle formulations.

By Distribution Channel: Online Dominance Reshapes Retail Landscape

Online channels dominate with 59.10 of % China pet food market size in 2025, growing at a 9.88% CAGR through 2031 as digital-native consumers embrace e-commerce convenience and subscription-based purchasing models. Tmall and JD.com lead platform sales, while emerging channels like Douyin (TikTok) and Xiaohongshu leverage livestreaming commerce and influencer marketing to drive product discovery and impulse purchases. The online advantage extends beyond convenience to include detailed product information, customer reviews, and personalized recommendations that traditional retail channels struggle to match.

Several factors, including the increasing digitalization of retail, the convenience of home delivery, and the wider product selection available to consumers, drive the supremacy of this channel. Major e-commerce platforms offer competitive pricing, detailed product information, and user reviews that help pet owners make informed purchasing decisions. The segment has particularly benefited from the growing preference among millennial and Gen Z pet owners who prefer digital shopping experiences. Additionally, many online platforms have introduced private label brands that offer quality products at competitive prices, further strengthening their market position.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

China's pet food market exhibits significant regional variations reflecting economic development patterns, urbanization levels, and cultural attitudes toward pet ownership across different geographic segments. Tier-1 cities, including Beijing, Shanghai, Guangzhou, and Shenzhen, account for approximately 35-40% of market value in 2025 despite representing less than 5% of the national population, demonstrating concentrated purchasing power and premium product adoption rates. These metropolitan areas drive premiumization trends, with average spending per pet reaching RMB 3,000-5,000 (USD 420-705) annually .

Tier-2 cities represent the fastest-growing geographic areas driven by rising disposable incomes, expanding middle-class populations, and increasing pet adoption rates among younger demographics. Cities like Hangzhou, Nanjing, Chengdu, and Xi'an demonstrate particular dynamism as regional economic centers with growing populations of educated professionals who view pet ownership as lifestyle enhancement. E-commerce penetration accelerates market development in these regions, enabling access to premium products and international brands previously available only in major metropolitan areas.

Tier-3 cities and rural areas remain underpenetrated but show emerging potential as economic development and urbanization progress throughout China's interior regions. These markets currently focus on basic nutrition products and value-oriented positioning, but demographic trends suggest future premiumization as local incomes rise and pet ownership becomes more culturally accepted. Manufacturing concentration in Tier-3 cities creates employment opportunities and local economic development that may accelerate pet adoption rates, while improved logistics infrastructure enables better product availability and competitive pricing.

Competitive Landscape

The Chinese pet food market exhibits a highly fragmented competitive landscape with a mix of global multinational corporations and regional players. Global conglomerates like Mars Incorporated, Nestlé, ADM, Clearlake Capital Group, L.P. (Wellness Pet Company, Inc.), and General Mills maintain significant market presence with a share of 11.4% in 2024 through their established brands and extensive distribution networks. These companies leverage their international expertise and research capabilities to introduce advanced nutritional products. Regional players, particularly those based in manufacturing hubs like Tianjin, are gaining prominence by offering products tailored to local preferences and maintaining competitive pricing strategies.

The market is witnessing increasing consolidation through strategic acquisitions and partnerships. Major global players, including Mars, Incorporated, General Mills Inc., ADM, Nestle (Purina), and Clearlake Capital Group, L.P. (Wellness Pet Company, Inc.) are acquiring local manufacturers to expand their manufacturing capabilities and distribution reach in China. Regional players are forming partnerships with international companies to access advanced technologies and expand their product portfolios. The competitive dynamics are further influenced by the emergence of private label brands from major e-commerce platforms, which are gaining market share by offering quality products at competitive prices.

Success in the Chinese pet food market increasingly depends on companies' ability to innovate and establish strong distribution networks. Incumbent players need to focus on developing premium products with specialized nutritional benefits while maintaining their mass-market offerings. Investment in research and development facilities within China is becoming crucial for understanding local consumer preferences and developing targeted products. Companies must also strengthen their omnichannel presence, particularly on e-commerce platforms, while maintaining relationships with traditional retail channels and veterinary clinics.

China Pet Food Industry Leaders

Mars, Incorporated

General Mills Inc.

ADM

Nestle (Purina)

Clearlake Capital Group, L.P. (Wellness Pet Company, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2023: Nestle Purina launched new cat treats under the Friskies "Friskies Playfuls - treats" brand. These treats are round in shape and are available in chicken and liver and salmon and shrimp flavors for adult cats.

- April 2023: Mars Incorporated opened its first pet food research and development center in Asia-Pacific. This new facility, called the APAC pet center, will support the company's product development.

- March 2023: Blue Buffalo, a subsidiary of General Mills Inc., launched its new high-protein dry dog food line, BLUE Wilderness Premier Blend. It is formulated with chicken and a blend of antioxidants, vitamins, and minerals.

China Pet Food Market Report Scope

Food, Pet Nutraceuticals/Supplements, Pet Treats, and Pet Veterinary Diets are covered as segments by Pet Food Product. Cats, Dogs, and other pets are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, and Supermarkets/Hypermarkets are covered as segments by the Distribution Channel.

Pet Food Product

| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft and Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Diabetes | ||

| Digestive Sensitivity | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary tract disease | ||||

| Obesity Diets | ||||

| Derma Diets | ||||

| Other Veterinary Diets |

Pets

| Cats |

| Dogs |

| Other Pets |

Distribution Channel

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft and Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Diabetes | |||

| Digestive Sensitivity | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary tract disease | |||||

| Obesity Diets | |||||

| Derma Diets | |||||

| Other Veterinary Diets | |||||

| Pets | Cats | ||||

| Dogs | |||||

| Other Pets | |||||

| Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

Need A Different Region or Segment?

Customize Now

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF