Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 3.53 Billion |

| Market Size (2030) | USD 5.71 Billion |

| Growth Rate (2025 - 2030) | 10.08% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Organic Fertilizer Market Analysis by Mordor Intelligence

The China Organic Fertilizer Market size is estimated at 3.53 billion USD in 2025, and is expected to reach 5.71 billion USD by 2030, growing at a CAGR of 10.08% during the forecast period (2025-2030).

China's agricultural sector is undergoing a significant transformation toward sustainable farming practices, with organic fertilizers emerging as a cornerstone of this evolution. Organic fertilizers have established a dominant position in the agricultural biologicals market, accounting for 70.6% of the total market share in 2022. This transformation is being driven by the Chinese government's comprehensive approach to ecological civilization, which includes supply-side structural reforms and rural revitalization strategies. The government's initiatives are complemented by municipal-level policies that provide concrete incentives for farmers transitioning to organic farming inputs, creating a supportive ecosystem for market growth.

The market is characterized by a strong emphasis on traditional and innovative organic soil amendments, with manure-based products leading the sector. Traditional manure fertilizers, valued at USD 1.42 billion in 2022, continue to be the preferred choice for both organic and conventional farming due to their proven effectiveness in improving soil organic matter content and enhancing nutrient uptake. Alternative organic soil amendments, including fish guano, bat guano, fish emulsion, vermicompost, and molasses-based products, have also gained significant traction, with this segment reaching a substantial value of USD 832.2 million in 2022, demonstrating the market's diversification.

Consumer preferences and awareness are playing a pivotal role in shaping the organic fertilizers market landscape. A notable 73% of Chinese consumers have expressed willingness to pay premium prices for organic food products, despite organic vegetables commanding prices 3 to 15 times higher than conventional produce. This consumer sentiment is particularly strong among wealthy families and health-conscious individuals, creating a robust demand pull for organic farming practices and, consequently, organic plant nutrition.

The industry is witnessing a strategic shift in production and distribution methods, with manufacturers focusing on research and development to improve product efficacy and sustainability. Local governments are actively participating in market development by implementing region-specific organic agriculture inputs plans and providing technical support to farmers. This coordinated approach between government bodies, manufacturers, and agricultural communities is creating a more structured and efficient market ecosystem, facilitating the adoption of biological fertilizers across different farming segments and scales of operation.

China Organic Fertilizer Market Trends and Insights

Country’s zero growth in pesticides use and increasing exports under organic products driving the organic cultivation.

- According to the latest reports by FiBL and IFOAM, the market for organic food in China is growing at an annual rate of 25.0%. The shift from conventional to organic is a transformation toward a more sustainable food system within China, given the USD 2.91 billion of agri-food commodities exported from China each year.

- The size of organic farmland increased rapidly in China because more people started buying organic products due to increased incomes and the increasing importance of food safety. In the last three years, China's organic planting area increased by 10%, reaching 2.4 million hectares in 2020. National policies have been adopted to promote organic production, advocating the slogans that state, ″lucid waters and lush mountains are invaluable assets″ and ″green development".

- Organic farming in China is majorly export-oriented. The products that are both exported and imported are cereals, soybeans, and fruits, followed by some vegetables. Liaoning, Jilin, and Heilongjiang, China's three northeastern provinces, support the largest organic production nationally in terms of output, volume, and area. Most organic farms located in northern China (e.g., Shandong and Liaoning) supply organic vegetables and fruits to nearby cities. In addition, they export some products to Japan, South Korea, Europe, and the United States.

- With the increasing concerns of soil toxicity due to the overuse of synthetic fertilizers and pesticides, which lead to soil contamination, the demand for sustainable agriculture practices and organic food production is on the rise in China. This would moderately slow down yet increase the shift in cultivation practices. It also subsequently increases the demand for crop nutrition and protection products.

Understand The Key Trends Shaping This Market

Download PDF

The growing demand for organic products, approximately 73% of Chinese consumers are willing to have organic food

- China's organic food market is developing rapidly, and the potential demand for organic food among Chinese consumers is enormous. This is due to the growth of the wealthier middle classes and a greater awareness of the health implications. In 2021, organic food sales in China were about USD 77.54 billion.

- Due to various government laws that favor organic food over food safety and customer preferences for organic food over conventional food, the demand for organic food items considerably expanded. While prices of organic vegetables in China range from 3 to 15 times the cost of conventional produce, prices for organic vegetables are generally between 5 to 10 times the prices of their conventional counterparts. However, despite the price factor being a barrier, wealthy families and individuals with health problems are eager to increase their budget, with approximately 73% of Chinese consumers willing to pay extra for organic foods.

- The Chinese government is slowly aiming to become self-reliant in the organic food sector. For instance, the economy is slowly moving toward a green agriculture practice by encouraging farmers to scale back the use of chemical fertilizers and switch to bio-based alternatives. The China Chain Store and Franchise Association (CCFA) research in 2020 declared that organic awareness among the Chinese in developed cities was at 83% when it came to an understanding of the concept of sustainable food production. Although China's organic food sector is still quite small and falls far short of satisfying domestic and international consumer demand, it can be stated that organic food in China has enormous potential in both the domestic and foreign markets, considering the rise in domestic sales by 4.01% in 2021.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: Form

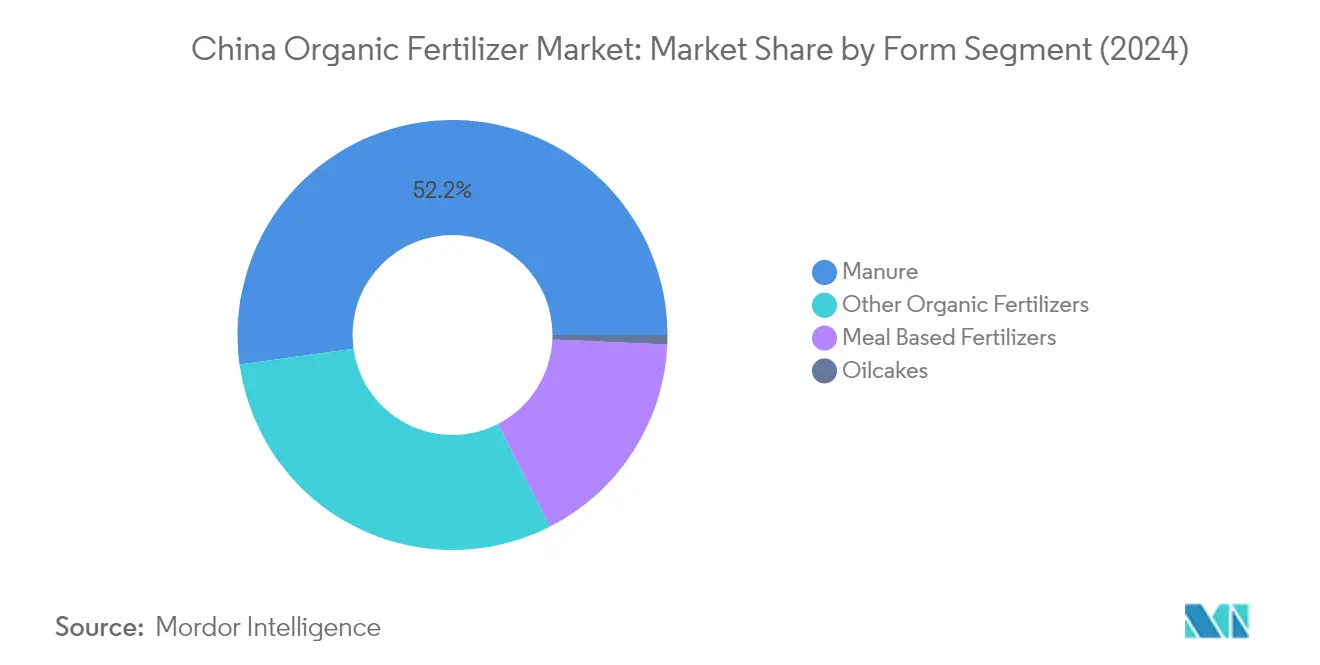

Manure Segment in China Organic Fertilizer Market

Manure dominates the Chinese organic fertilizer market, commanding approximately 52% market share in 2024, primarily due to its widespread usage in both organic and conventional farming practices. The segment's dominance is attributed to its easy availability, cost-effectiveness compared to other organic fertilizers, and traditional acceptance among farmers. Manure fertilizers are extensively used across all crop types, with particularly strong adoption in row crops due to their bulk application requirements and soil enrichment properties. The segment is experiencing robust growth driven by the Chinese government's initiatives to reduce chemical fertilizer usage and promote organic farming practices. The Ministry of Agriculture and Rural Affairs' goal to increase organic fertilizer usage by 5% by 2025 has particularly benefited the manure segment, as it represents the most accessible and economical transition path for farmers switching from chemical to organic fertilizers. Additionally, manure's effectiveness in improving soil structure, water retention capacity, and long-term soil health continues to drive its adoption across various agricultural applications.

Remaining Segments in Form Segmentation

The other segments in the Chinese organic fertilizer market include other organic fertilizers, meal-based fertilizers, and oilcakes, each serving specific agricultural needs and applications. Other organic fertilizers, including fish guano, bat guano, fish emulsion, vermicompost, and molasses, represent the second-largest segment, offering diverse nutrient profiles and specialized applications for different crop types. Meal-based fertilizers, comprising bone meal, blood meal, feather meal, and fish meal, are valued for their high nitrogen and phosphorus content, making them particularly effective for crops with specific nutrient requirements. The oilcakes segment, though smaller in market share, plays a crucial role in sustainable agriculture due to its slow-release nutrient properties and effectiveness in controlling soil-borne diseases, particularly in horticultural applications. These segments collectively complement the manure segment by providing farmers with specialized organic fertilizer options tailored to specific crop needs and soil conditions.

Segment Analysis: Crop Type

Row Crops Segment in China Organic Fertilizer Market

Row crops dominate the Chinese organic fertilizer market, commanding approximately 80% of the total market value in 2024. The segment's dominance is primarily attributed to its extensive cultivation area, which accounts for about 82% of the total crop area in the country. Major row crops cultivated in China include rice, wheat, corn, and millet, with the northeastern provinces of Liaoning, Jilin, and Heilongjiang supporting the largest organic production nationally in terms of output, volume, and area. The segment's strong market position is further reinforced by the increasing adoption of organic farming practices and the government's push toward sustainable agriculture. Most organic farms located in northern China, particularly in regions like Shandong and Liaoning, are focusing on supplying organic produce to nearby cities while also maintaining export relationships with Japan, South Korea, Europe, and the United States.

Cash Crops Segment in China Organic Fertilizer Market

The cash crops segment is experiencing the most rapid growth in the Chinese organic fertilizer market, with an expected growth rate of approximately 11% between 2024 and 2029. This impressive growth trajectory is driven by several factors, including the higher export potential of crops like cotton, sugarcane, and oilseeds. The segment's expansion is further supported by China's position as the world's largest cotton producer, consumer, and importer, with about 300 million people involved in cotton production. Additionally, there is a growing domestic demand for organic tea, particularly in major cities like Beijing, Shanghai, and Guangzhou, coupled with strong export opportunities to Europe, the United States, and Japan. The government's initiatives to decrease overall chemical use in agriculture and promote organic farming practices are expected to further accelerate the growth of organic fertilizer usage in cash crops.

Remaining Segments in Crop Type Segmentation

The horticultural crops segment plays a vital role in China's organic fertilizer market, focusing on crops such as apples, apricots, bananas, avocados, cabbage, lettuce, and pumpkin. This segment is particularly significant in the context of year-round cultivation practices, especially for fruits and vegetables. The segment's importance is enhanced by the increasing domestic demand for processed organic fruits and vegetables, with organic liquor derived from horticultural crops gaining significant market traction. The segment's growth is further supported by the suitability of specific organic fertilizers, particularly oil cake-based products, which are ideal for the slow-release nutrient requirements of horticultural crops.

Competitive Landscape

Top Companies in China Organic Fertilizer Market

The Chinese organic fertilizers market features several established players, including Genliduo Bio-tech, Suståne Natural Fertilizer, Biolchim SPA, and Qingdao Future Group, among others. Companies are increasingly focusing on research and development initiatives, particularly in developing specialized formulations for different crop types and soil conditions. Product innovation is centered around improving nutrient content, absorption rates, and soil enhancement properties of organic fertilizers. Operational strategies emphasize building robust distribution networks across agricultural regions and establishing partnerships with local farming communities. Companies are expanding their production capacities through new manufacturing facilities and investing in advanced processing technologies. Strategic moves in the market largely revolve around obtaining organic certifications, developing customized solutions for specific crop segments, and strengthening technical support services for farmers.

Fragmented Market with Strong Local Presence

The Chinese organic fertilizer market exhibits a highly fragmented structure with numerous local manufacturers and distributors operating across different regions. The market is characterized by a strong presence of domestic players who leverage their understanding of local agricultural practices and established relationships with farming communities. Regional players dominate specific geographical territories through their specialized product offerings and localized distribution networks. The market shows limited consolidation, with the top five players accounting for a minimal share of the total market value, indicating significant opportunities for market penetration and growth.

Merger and acquisition activities in the market remain relatively modest, with companies preferring organic growth strategies through capacity expansion and product development. Local manufacturers focus on building manufacturing facilities near agricultural hubs to ensure efficient distribution and reduce transportation costs. The market structure encourages competition based on product quality, price points, and technical support services. Companies are increasingly establishing research partnerships with agricultural universities and institutions to enhance their product development capabilities and market credibility.

Innovation and Distribution Key to Growth

Success in the Chinese organic fertilizer market increasingly depends on developing innovative products that address specific crop nutrition needs while maintaining cost-effectiveness. Companies need to invest in research and development to create differentiated products with improved nutrient profiles and absorption characteristics. Building strong relationships with agricultural extension services and farming communities is crucial for market penetration. Manufacturers must focus on establishing efficient supply chains and distribution networks to ensure product availability across different agricultural regions. Technical support capabilities and farmer education programs are becoming essential elements for building market presence.

Future growth opportunities lie in developing specialized biological fertilizer formulations for high-value crops and expanding into emerging agricultural regions. Companies need to address the challenge of price sensitivity while maintaining product quality and effectiveness. Regulatory compliance and obtaining necessary certifications will become increasingly important as the government strengthens organic farming standards. Building brand recognition through demonstration of product effectiveness and environmental benefits will be crucial for market success. Companies must also focus on developing sustainable sourcing practices for raw materials to ensure consistent product quality and supply chain reliability. Additionally, integrating organic soil amendments and organic plant nutrition into their offerings can enhance product appeal and effectiveness in the market.

China Organic Fertilizer Industry Leaders

-

Biolchim SPA

-

Genliduo Bio-tech Corporation Ltd

-

Hebei Woze Wufeng Biological Technology Co. Ltd

-

Qingdao Future Group

-

Suståne Natural Fertilizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

China Organic Fertilizer Market Report Scope

Manure, Meal Based Fertilizers, Oilcakes are covered as segments by Form. Cash Crops, Horticultural Crops, Row Crops are covered as segments by Crop Type.

Form

| Manure |

| Meal Based Fertilizers |

| Oilcakes |

| Other Organic Fertilizers |

Crop Type

| Cash Crops |

| Horticultural Crops |

| Row Crops |

| Form | Manure |

| Meal Based Fertilizers | |

| Oilcakes | |

| Other Organic Fertilizers | |

| Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops |

Need A Different Region or Segment?

Customize Now

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of organic fertilizers applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The crop nutrition function of agricultural biological consists of various products that provide essential plant nutrients and enhance soil quality.

- TYPE - Organic fertilizers are applied to provide essential crop nutrients and enhance the soil quality.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.

Get More Details On Research Methodology

Download PDF