Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

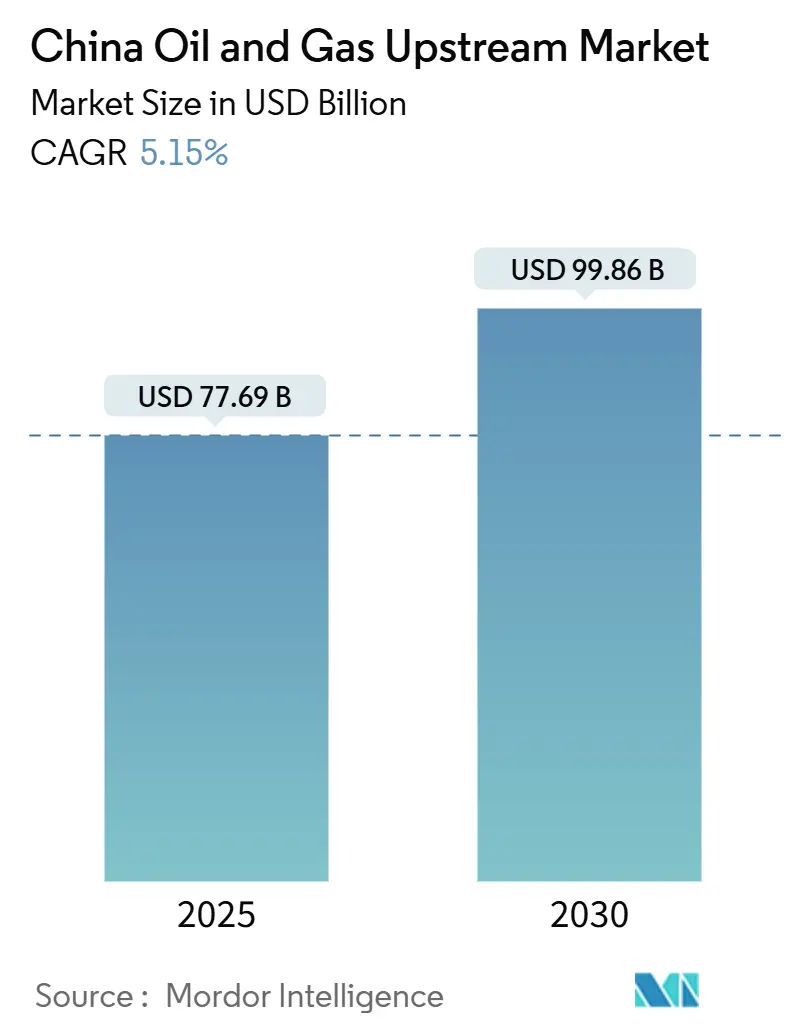

| Market Size (2025) | USD 77.69 Billion |

| Market Size (2030) | USD 99.86 Billion |

| Growth Rate (2025 - 2030) | 5.15% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Oil And Gas Upstream Market Analysis by Mordor Intelligence

The China Oil And Gas Upstream Market size is estimated at USD 77.69 billion in 2025, and is expected to reach USD 99.86 billion by 2030, at a CAGR of 5.15% during the forecast period (2025-2030).

Beijing’s drive for energy self-sufficiency, record upstream capital expenditure by national oil companies (NOCs), and sustained frontier discoveries give the Chinese oil and gas upstream market a strong near- to medium-term growth runway. Ultra-deep well successes in the Tarim and Sichuan basins, combined with digital-drilling rollouts that are trimming per-well costs by 15-20%, broaden the commercial reserve base and accelerate field development cycles. Government tax incentives, import-substitution mandates, and a supportive domestic pricing floor further reinforce investment appetite. Meanwhile, stricter methane-emission rules compel operators to retrofit mature assets, sparking a parallel surge in green technology spending. Together, these dynamics keep the Chinese oil and gas upstream market firmly on a positive trajectory despite global price volatility.

Key Report Takeaways

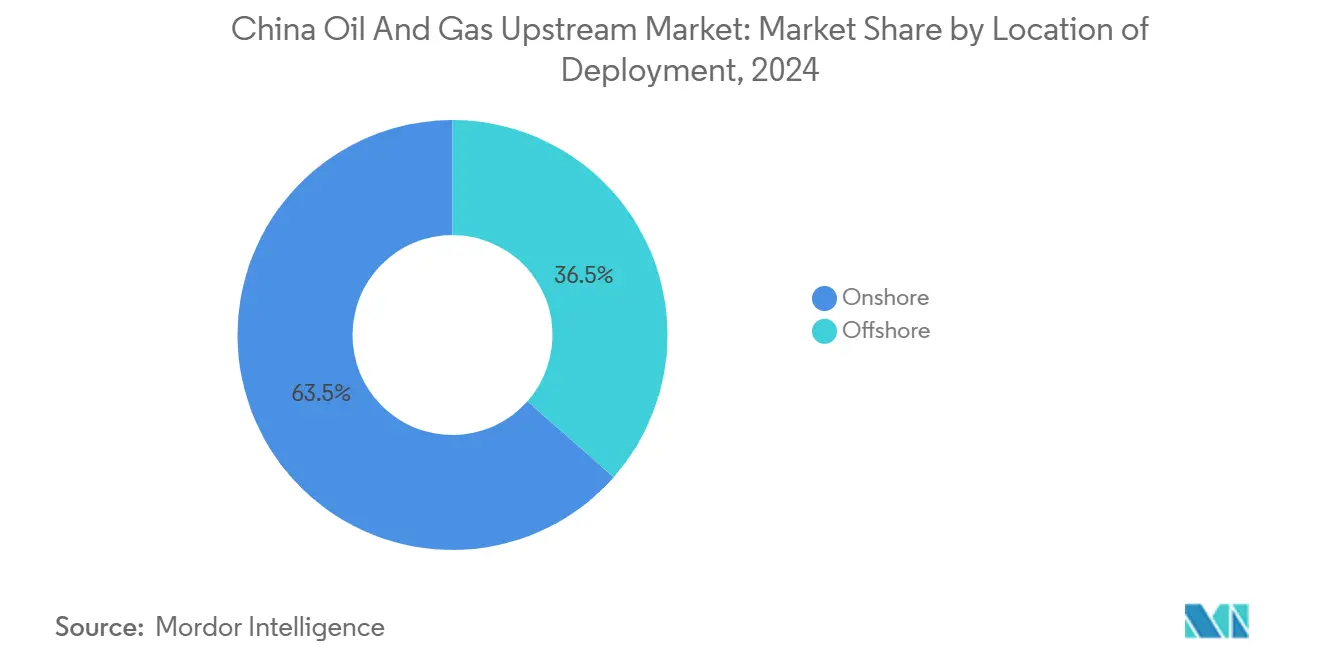

- By location of deployment, onshore operations led with 63.5% of the China oil and gas upstream market share in 2024, while offshore assets are projected to grow at a 6.1% CAGR through 2030.

- By resource type, crude oil accounted for a 56.7% share of the China oil and gas upstream market size in 2024; natural gas development is forecast to expand at a 5.9% CAGR to 2030.

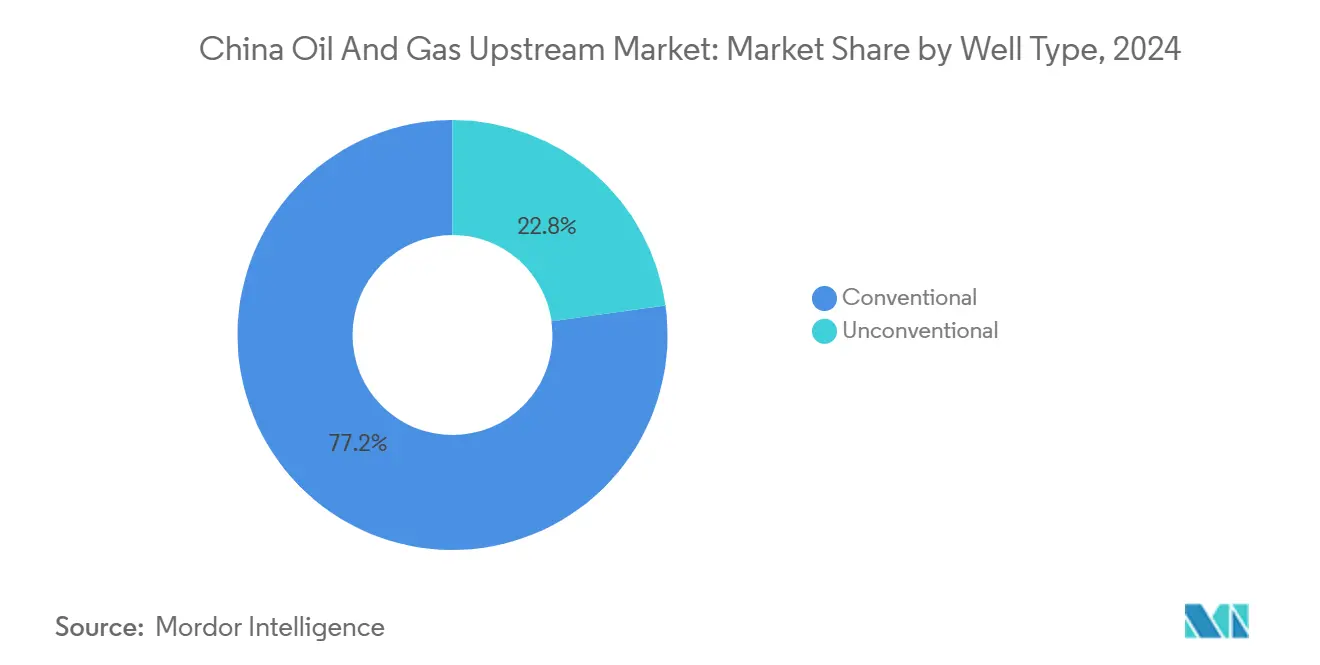

- By well type, conventional wells held 77.2% of the Chinese oil and gas upstream market share in 2024; unconventional drilling is expected to show the fastest growth at a 7.2% CAGR through 2030.

- By service, development and production dominated with 72.4% revenue share in 2024; decommissioning is advancing at a 7.8% CAGR to 2030.

- Regionally, Western provinces contributed 45% of the nation's natural-gas output in 2024 and are projected to record the highest 8.2% CAGR through 2030.

China Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis

| Discovery of new ultra-deep oil & gas fields (Tarim, Sichuan) | 1.5% | Western China, Xinjiang, Sichuan provinces | Medium term (2-4 years) |

|---|---|---|---|

| Rising upstream investment by Chinese NOCs | 1.2% | National, concentrated in major basins | Short term (≤ 2 years) |

| Government push for energy-security & import substitution | 0.8% | National policy implementation | Long term (≥ 4 years) |

| Digital-drilling & AI well-optimization programs | 0.7% | Major producing regions, technology hubs | Medium term (2-4 years) |

| CO₂-EOR & CCS integration improving field economics | 0.4% | Mature fields in Northeast and North China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Discovery of New Ultra-Deep Oil & Gas Fields

Large-scale discoveries in formations deeper than 6,000 meters have recalibrated the China oil and gas upstream market outlook. CNPC’s Fuman field achieved 2,000 barrels per day from 8,400-meter wells in the Tarim Basin, validating commercial recovery in extreme-depth reservoirs. Sichuan’s Anyue gas field added 500 billion m³ proven reserves in 2024, becoming the country’s single-largest unconventional gas asset. Together, these findings could reduce import dependence by nearly one-tenth by 2030, while exporting high-pressure drilling expertise to overseas markets. Regulatory momentum is visible: 15 exploration blocks were opened in Western China in 2024, signaling deeper resource monetization over the forecast horizon.[1]China Daily Editorial, “New exploration blocks approved in Western China,” China Daily, chinadaily.com.cn Equipment suppliers benefit from higher-spec rig demand, and regional governments anticipate new royalties that bolster local economies.

Rising Upstream Investment by Chinese NOCs

Capital outlays surged in 2024 as NOCs shield supply chains against geopolitical shocks. Sinopec lifted upstream spending 15% to USD 38 billion, channeling funds into enhanced-recovery pilots and digital infrastructure. CNOOC committed USD 22 billion to deepwater South China Sea and Bohai Bay projects, underscoring offshore growth ambitions.[2]Chong Koh Ping, “CNOOC deepwater investment South China Sea,” Wall Street Journal, wsj.com National project approvals worth USD 95 billion in 2024 further underscore policy support for domestic production expansion. Cost discipline is improving: standardized drilling platforms and modular surface facilities are lowering per-barrel development costs by up to 18%. The cash-flow uplift accelerates reinvestment cycles, reinforcing the growth pattern of the Chinese oil and gas upstream market.

Government Push for Energy Security & Import Substitution

Central planners aim to achieve 200 million tons of annual crude oil output by 2025 and 400 billion cubic meters of gas by 2030 under the 14th Five-Year Plan.[3]National Energy Administration, “14th Five-Year Plan energy targets,” nea.gov.cn The policy mix includes 15% depletion allowances, accelerated depreciation, and a 90-day strategic petroleum reserve requirement that favors domestic barrels. These measures cement long-term demand for local drilling and field-service capacity. Producers respond by increasing their resource-conversion ratios, while provincial agencies expedite permits for marginal fields and brownfield infill wells. Over the forecast window, import-substitution rules tighten the alignment between profitability and national energy objectives, underpinning the resilience of the Chinese oil and gas upstream market against external supply shocks.

Digital-Drilling & AI Well-Optimization Programs

Artificial-intelligence deployment is cutting non-productive time and narrowing well-cost curves. In 2024, PetroChina implemented machine-learning analytics across 2,500 wells, reducing downtime by 20% and increasing drilling speed by 15%. Sinopec operates a real-time digital twin network covering 180 fields, driving recovery factor gains of up to 12%. Automated directional drillers now place boreholes within 2-meter targets, slash human intervention by 60% and enhance worker safety. The Ministry of Industry and Information Technology’s USD 2.8 billion budget for oil and gas digitalization accelerates domestic software and sensor innovation. As these efficiencies mature, they widen the cost-advantage of leading NOCs, preserve margins during price swings, and solidify long-term competitiveness within the Chinese oil and gas upstream market.

Restraints Impact Analysis

| Price volatility & OPEC+ supply actions | -0.9% | Global market exposure, export-dependent regions | Short term (≤ 2 years) |

|---|---|---|---|

| Stricter national methane-emission regulations | -0.6% | National implementation, heavy emitting basins | Medium term (2-4 years) |

| Water scarcity for fracturing in arid Northwest China | -0.4% | Xinjiang, Inner Mongolia, Northwest provinces | Long term (≥ 4 years) |

| Seismic-safety curbs in earthquake-prone basins | -0.3% | Sichuan, Yunnan, seismically active regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility & OPEC+ Supply Actions

Oil-price swings create budgeting uncertainty, delay final-investment decisions, and pressure free cash flow. OPEC+ cuts in late-2024 lifted Brent toward USD 95 per barrel, boosting revenues but tightening domestic refining margins. Deepwater project hurdles remain: 12 developments await price stability above USD 70 per-barrel breakevens. Chinese NOCs hedge 40-60% of their production, yet shallow derivative markets limit their effectiveness. To soften shocks, regulators enforce a USD 60 per-barrel floor for domestic barrels, cushioning high-cost assets. Even so, cyclical uncertainty restrains spending on frontier plays and shapes a measured capital-allocation approach within the China oil and gas upstream market.

Stricter National Methane-Emission Regulations

New rules cap methane emissions at 0.2% of output and mandate leak-detection retrofits on 15,000 well sites, lifting compliance spend to roughly USD 150,000 per mature well. Operators must install zero-flaring designs in all new drilling, which adds up to 12% to initial capital expenditures. Bonded decommissioning funds, introduced in 2024, compel project owners to ring-fence closure costs, elevating working-capital requirements. Yet, a USD 3.2 billion green-finance program offsets some of these burdens through low-interest loans. Over time, tighter standards build operational resilience and environmental stewardship, but they also moderate returns, thereby trimming the medium-term growth rate of the China oil and gas upstream market.

Segment Analysis

By Location of Deployment: Onshore Footprint, Offshore Momentum

Onshore assets held 63.5% of the China oil and gas upstream market share in 2024, backed by entrenched infrastructure and lower lifting costs averaging USD 35-45 per barrel. Enhanced-recovery pilots in Daqing and Liaohe prolong plateau output, while revamped gathering systems shrink loss rates. In tandem, the offshore segment is projected to post a robust 6.1% CAGR to 2030 as deepwater technologies mature and policymakers encourage energy diversification. CNOOC's Bozhong 19-6 condensate field proved economically viable at a 1,500-meter water depth and led to follow-up exploration programs across Bohai Bay. Digital monitoring and unmanned platforms are cutting offshore operating costs by 25%, closing the historic cost gap with onshore fields and bolstering project sanction rates.

The Chinese oil and gas upstream market now views offshore acreage as the core frontier for large-scale oil and gas discoveries. Eight new blocks awarded in 2024 span 25,000 km² of prospective South China Sea acreage. Wider use of floating production storage and offloading (FPSO) units avoids long subsea tie-backs and accelerates first-oil timelines. Meanwhile, onshore operations bank on brownfield digitalization and chemical flooding to arrest decline. Over the forecast period, a balanced capital allocation emerges, with mature land assets providing low-risk cash flow and offshore projects delivering volume growth, thereby sustaining the broader China oil and gas upstream market's expansion.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Resource Type: Liquids Lead, Gas Ascends

Crude oil accounted for 56.7% of the Chinese oil and gas upstream market size in 2024, as refiners relied on domestic sweet blends to optimize their run rates. CO2 injection in Daqing and Shengli lifted recovery by 12-15% and extended field life cycles. Gas is the clear growth pillar, registering a 5.9% CAGR through 2030, mirroring government mandates to increase the fuel’s share in the national primary energy mix. The West-East Pipeline added 15 billion m³ capacity in 2024, enabling Xinjiang’s Tarim output to displace coastal LNG imports. Shale and tight-gas additions in Sichuan and Ordos underpin 40% of the incremental supply, feeding rising city-gas and petrochemical demand.

Environmental regulation prioritizes gas burnout over coal, driving higher pricing transparency that incentivizes upstream investments. Operators also benefit from cross-border pipeline opportunities in Central Asia, which allow for back-hauling surplus volumes. Over the long term, a diversified resource mix underpins security targets and keeps the Chinese oil and gas upstream market less exposed to crude market shocks. Nonetheless, liquids remain indispensable to domestic refineries and petrochemical complexes, ensuring balanced capital allocations between oil and gas portfolios.

By Well Type: Conventional Backbone, Unconventional Upswing

Conventional completions held 77.2% of the Chinese oil and gas upstream market share in 2024, thanks to decades of established infrastructure, a well-developed service ecosystem, and a proven understanding of reservoir behavior. Digital downhole sensors and electrical submersible pumps increased average flow rates by 8% year-over-year, thereby tightening decline curves. Unconventional drilling is expected to rise sharply at a 7.2% CAGR through 2030, spearheaded by the Changning shale gas field, which achieved an annual output of 6 billion m³ in 2024.[4]Joe Leahy, “China’s Tarim Basin oil discovery reshapes energy outlook,” Financial Times, ft.com Horizontal wells now expose 3-5× more pay-zone length than vertical counterparts, while multi-stage fracturing unlocks low-permeability zones.

Water-recycling loops and micro-seismic monitoring address environmental concerns and enhance fracture placement accuracy. Regulators granted 450 unconventional water permits in 2024, underscoring policy support for the segment. Looking ahead, knowledge transfer from U.S. shale plays and local ceramic-proppant capacity expansions reduces import reliance and unit-well costs. Combined, these improvements solidify unconventional resources as a critical growth lever, sustaining the China oil and gas upstream market's trajectory to 2030.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Service: Production Core, Decommissioning Wave Builds

Development and production services captured a 72.4% revenue share in 2024, reflecting an active rig fleet, a large work-over backlog, and comprehensive lifecycle requirements for thousands of producing wells. High-efficiency rigs and rotary-steerable systems are shortening average spud-to-completion times by 10 days. Meanwhile, decommissioning is outpacing all other service lines, with a 7.8% CAGR, as fields commissioned in the 1980s approach the end of their life. New regulations require cement-plug verification, groundwater protection, and surface restoration within 24 months, which will increase per-well budgets to USD 800,000-1.2 million.

National Energy Administration rules introduced mandatory bonding in 2024, creating a predictable funding pool for closure work and attracting specialized contractors. Exploration services remain steady, supported by 180,000 km² of 3D seismic shot in Western China during 2024. Moving forward, integrated service models that combine drilling, production optimization, and end-of-life solutions will gain share and foster recurring revenue streams, embedding service-sector resilience within the China oil and gas upstream market.

Geography Analysis

The Northeast, anchored by Daqing and Liaohe, remains the heritage hub, accounting for 35% of the nation's crude despite reservoir maturity. Enhanced-recovery pilots, corrosion-resistant tubulars, and real-time steam-flood control stabilize production and create incremental reserve bookings. Western provinces stand out as the strategic centerpiece, with the Tarim and Ordos basins accounting for 45% of national gas output in 2024 and growing at the fastest rate of 8.2% annually through ultra-deep and unconventional completions [CNPC]. Regional infrastructure build-out, including the USD 15 billion transmission package approved in 2024, ties these remote wells to the eastern demand center.

The Sichuan Basin emerges as the flagship unconventional gas cluster, yielding 25 billion cubic meters per year and accounting for 40% of incremental national gas growth. Investors favor the basin’s over-pressured geology and year-round weather advantages. Offshore domains add geographic diversification: South China Sea and Bohai Bay together contributed 15% of total hydrocarbons in 2024, but accounted for 60% of discoveries post-2024 as deepwater geophysical imaging improved. CNOOC lifted offshore output to 550 million boe in 2024 and lines up 1,200-meter targets for near-term sanction.

Regulation is region-specific: Eastern provinces impose stricter emissions thresholds due to their dense populations, which is accelerating the adoption of closed-loop gas capture and vapor recovery. Western basins, while less restrictive, face water scarcity constraints that prompt operators to adopt recycling systems. Collectively, these regional nuances shape capital allocation and service demand, weaving a multi-speed growth tapestry across the Chinese oil and gas upstream market.

Competitive Landscape

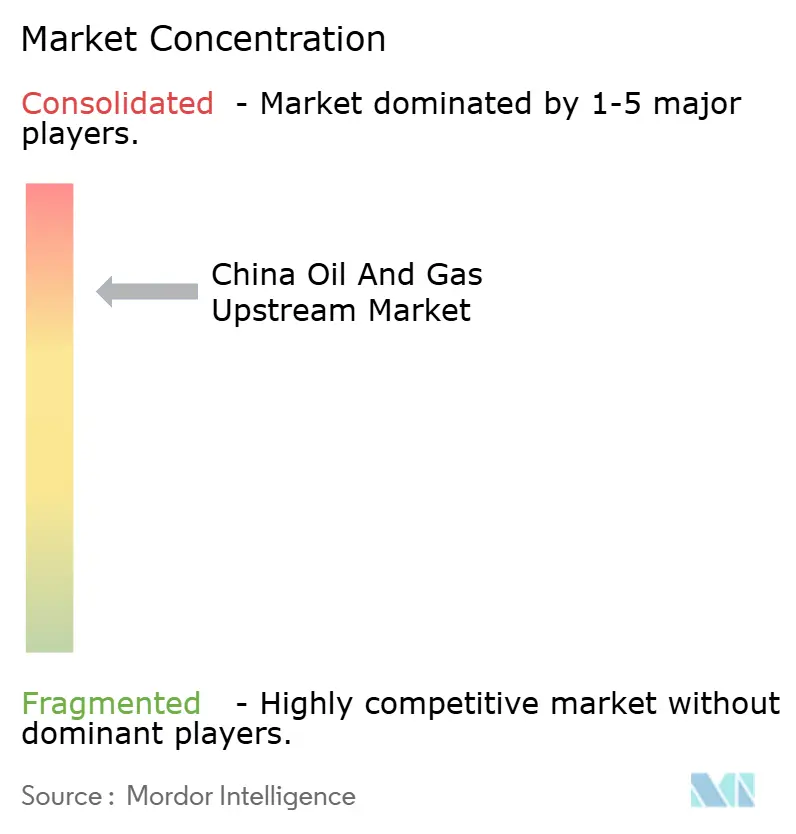

China’s upstream arena exhibits moderate concentration, with three state-owned producers accounting for roughly 75% of domestic volumes. However, internal competition over acreage, technology, and capital efficiency has intensified. CNPC achieved USD 12 per barrel reserves-addition cost in 2024 by standardizing drilling protocols and leveraging a local supplier base. Sinopec and CNOOC prioritize deepwater expansion and digital asset management to differentiate themselves. Proprietary AI algorithms reduce operating costs by 15-20% and enhance production forecasts, reinforcing scale advantages.

International majors participate through technical-service contracts and joint ventures, but tightened local content rules compress margins. Specialized domestic firms, such as Anton and Jereh, capture niches in well stimulation, integrated project management, and decommissioning. The Ministry of Natural Resources’ competitive bidding on exploration blocks widens entry, yet NOCs retain preferred access to strategic acreage. Technology alliances are forming around deepwater drilling packages, advanced subsea systems, and carbon management solutions, creating a layered competitive landscape that supports the ongoing expansion of the Chinese oil and gas upstream market.

China Oil And Gas Upstream Industry Leaders

-

China National Petroleum Corporation (CNPC)

-

China Petroleum & Chemical Corporation (Sinopec)

-

China National Offshore Oil Corporation (CNOOC)

-

PetroChina Co. Ltd.

-

Shell plc (via CNOOC JVs)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: CNPC announced a USD 8.5 billion Tarim Basin ultra-deep exploration program, targeting 15 wells that will exceed 8,000 meters in depth.

- December 2024: Sinopec acquired a 51% stake in a Bohai Bay deepwater project for USD 3.2 billion, adding sizable offshore reserves.

- November 2024: CNOOC commenced production at the Lufeng 13-1 field in the South China Sea with an initial 40,000 barrels per day.

- October 2024: The National Energy Administration approved 12 new Sichuan shale blocks totaling 8,500 km².

- September 2024: PetroChina launched a USD 2.1 billion digital-optimization drive across 3,000 wells.

China Oil And Gas Upstream Market Report Scope

Upstream oil and gas refers to the exploration and production industries for petroleum. This includes the processes involved in searching for potential underground or underwater crude oil and natural gas fields, drilling exploratory wells, and subsequently drilling and operating the wells that recover and bring the crude oil or raw natural gas to the surface.

The Chinese oil and gas upstream market is segmented by location of deployment. By location of deployment, the market is segmented into onshore and offshore. The report offers the market sizes and forecasts in value (USD) for the above segments.

By Location of Deployment

| Onshore |

| Offshore |

By Resource Type

| Crude Oil |

| Natural Gas |

By Well Type

| Conventional |

| Unconventional |

By Service

| Exploration |

| Development and Production |

| Decommissioning |

| By Location of Deployment | Onshore |

| Offshore | |

| By Resource Type | Crude Oil |

| Natural Gas | |

| By Well Type | Conventional |

| Unconventional | |

| By Service | Exploration |

| Development and Production | |

| Decommissioning |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the China oil and gas upstream market in 2025?

The China oil and gas upstream market size is estimated at about USD 77.69 billion in 2025, following steady growth from 2024’s baseline.

Which segment leads deployment in China’s upstream sector?

Onshore assets hold the largest 63.5% share, benefiting from existing pipelines and lower lifting costs.

What growth rate is projected for offshore developments?

Offshore projects are forecast to expand at a 6.1% CAGR through 2030 as deepwater technologies mature.

How fast are unconventional wells growing?

Unconventional drilling is advancing at a 7.2% CAGR, driven by shale-gas gains in Sichuan and tight-gas successes in Ordos.

What is driving natural-gas expansion in China?

Gas output is rising on the back of policy mandates, pipeline build-out and large new reserves in Western and Southwestern basins.

Why is decommissioning a high-growth service line?

Hundreds of 1980s-era wells face end-of-life closures, and new bonding rules fund systematic decommissioning at a 7.8% CAGR.

Page last updated on: