Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 38.27 Billion |

| Market Size (2031) | USD 51.87 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Office Furniture Market Analysis by Mordor Intelligence

The China Office Furniture Market size is estimated at USD 38.27 billion in 2026, and is expected to reach USD 51.87 billion by 2031, at a CAGR of 6.27% during the forecast period (2026-2031).

The growth path aligns with policy-led demand for green-certified products in public procurement and a wider shift toward healthier and more functional workspaces that blend home and office needs. Manufacturers with credible environmental credentials and robust engineering pipelines, such as firms reporting large patent portfolios and enterprise-grade references, are positioned to consolidate share as compliance becomes a procurement gatekeeper. The market absorbs momentum from omnichannel models leveraging national logistics, where average courier delivery is shortened to 56.42 hours in key regions by 2023 (down over two hours from prior years), and same-day service norms prevail in major clusters amid USD 175 billion annual parcels,124 per person. At the same time, the China office furniture market benefits from rising interest in ergonomic and smart seating that ties posture, health monitoring, and sustainability attributes together in a single purchase decision.

Key Report Takeaways

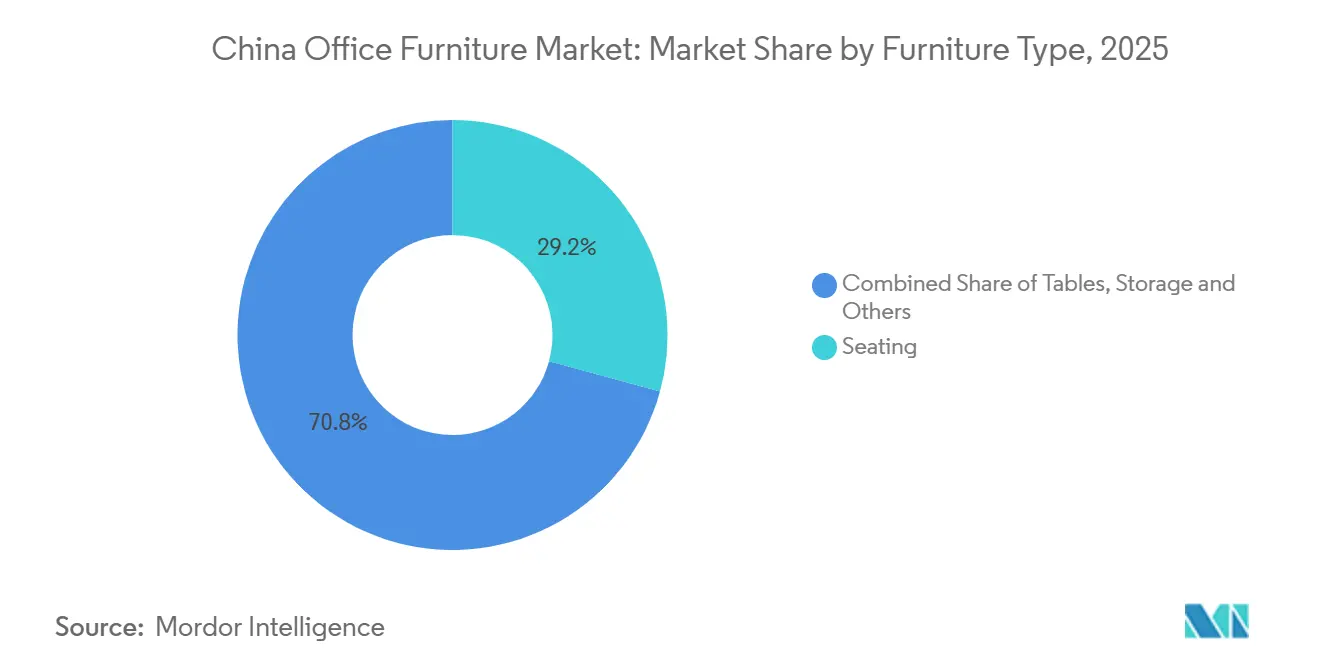

- By furniture type, seating led with 29.24% of the China office furniture market share in 2025 and is forecast to expand at an 8.84% CAGR to 2031.

- By distribution channel, B2B/direct-from-manufacturer accounted for 71.37% of the China office furniture market share in 2025, while B2C/retail is projected to record the fastest 12.37% CAGR through 2031.

- By geography, East China captured 37.74% of the China office furniture market share in 2025, while South China is expected to post the highest 11.37% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Office Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flight-to-quality office upgrades and fit-outs | +1.2% | Spill-over gains in Shanghai, Beijing, Shenzhen Grade A districts | Medium term (2-4 years) |

| Ergonomics and employee health investments (sit-stand desks, monitor arms) | +1.4% | National, early gains in tech hubs (Hangzhou, Shenzhen), spillover to tier-2 | Short term (≤ 2 years) |

| Omnichannel procurement acceleration (JD/Tmall, enterprise platforms) | +0.9% | National, concentrated in East/South China e-commerce corridors | Short term (≤ 2 years) |

| Smart/IoT-integrated office furniture adoption | +0.8% | Tier-1 cities (Beijing, Shanghai, Guangzhou), expanding to Chengdu, Wuhan | Medium term (2-4 years) |

| Green product certification and procurement preference (China GP/eco-label) | +1.1% | National, compliance-driven in government/SOE procurement | Medium term (2-4 years) |

| Manufacturing clusters enable rapid customization and DTC scale (Anji, Foshan) | +0.8% | Regional (Zhejiang, Guangdong), export impact global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Flight-to-Quality Office Upgrades Propel Premium Fit-Out Spend Despite Vacancy Overhang

Corporate landlords and tenants are investing in higher-quality amenities and greener fit-outs to secure occupancy and support hybrid work policies, even as leasing markets adjust. Procurement cycles now favor solutions that combine embodied carbon transparency and human-wellbeing benefits to align with project certification targets, including WELL-aligned interiors and low-VOC finishes. Public-sector demand reinforces this preference because agency buyers are guided by national action plans that promote green construction materials and certified products in tendering. Suppliers that can document life-cycle impacts and meet tighter testing indicators under updated green product evaluation standards improve their eligibility for projects. Within this backdrop, the China office furniture market shows growing interest in products that raise day-one functionality and lower lifetime environmental impact, which helps premium fit-outs defend budgets during rental renegotiations.

Ergonomic Investments Surge as Hybrid Work Redefines Office Beyond CBD Towers

A larger share of buyers views ergonomic seating and height-adjustable desks as preventive health tools that support productivity in both homes and corporate sites. Health research and industry case studies have spotlighted musculoskeletal risks from prolonged sitting, which is pushing organizations and individuals to upgrade chairs, monitor arms, and sit-stand solutions. Smart seating has moved from concept to commercial reality, with models that capture posture and user biometrics to generate app-based guidance and alerts. For instance, in product launches at CIFF Guangzhou 2025, Sunon showcased dynamic sitting lines with IoT biometrics. Brands active in Asia-Pacific report that carbon-neutral certified ergonomic lines that pair recycled materials with high adjustability are gaining customer preference, which reinforces the link between health outcomes and sustainability performance[1]Source: Steelcase, “Steelcase Carbon-Neutral Certified Ergonomic Chair Honored as 2025 China Green Point Annual Sustainable Practice Case,” Steelcase, steelcase.com.

Omnichannel Procurement Acceleration Elevates Access, Speed, and Brand Discovery

Enterprise procurement and consumer purchasing in China’s office furniture market are increasingly converging on omnichannel platforms that combine nationwide delivery coverage, standardized assortments, and reliable after-sales service. Major e-commerce marketplaces such as JD.com and Tmall now support next-day or two-day delivery to more than 300 Chinese cities, significantly shortening fulfillment timelines for standardized office furniture SKUs. Leading domestic and international brands have expanded flagship stores on these platforms, using curated digital showrooms, installation guarantees, and transparent service SLAs to replicate in-store purchasing confidence online. On the supply side, manufacturers and distributors are investing in regional distribution centers and bonded warehouses across East China, South China, and the Chengdu–Chongqing economic zone, reducing average delivery windows for large furniture orders from 7–10 days to 3–5 days in tier-1 and tier-2 cities. Cross-border brands supplying premium ergonomic seating and modular systems increasingly rely on China-based inventory pools to manage customs risk and returns, which has helped lower perceived risk for higher-value purchases.

Green Product Certification and Procurement Preference Reshape Buying Criteria

Government procurement rules direct buyers to prioritize certified green products across categories that include office interiors, which channels steady demand toward suppliers that meet the new thresholds. Public communications have also highlighted the role of procurement in supporting green construction, which raises the relevance of furniture with documented emissions profiles and carbon-footprint reporting. Certification programs aligned with national standards, together with implementation rules overseen by accredited bodies, set expectations for testing methods, quality assurance, and ongoing compliance[2]Source: CTI, “Furniture Green Product Certification,” CTI, cti-cert.com. Companies that invest in environmental product declarations, recycled content, and renewable energy in production can compete more effectively in tenders and corporate ESG programs. This direction favors firms that integrate design, manufacturing, and compliance management, which differentiates bids beyond price alone in the China office furniture market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High office vacancy and rent declines in Tier-1 cities | -1.3% | Tier-1 cities (Beijing, Shanghai, Shenzhen, Guangzhou, Chengdu) | Medium term (2-4 years) |

| Raw-material cost volatility and supply chain shocks | -0.7% | National, concentrated impact on Guangdong/Zhejiang manufacturers | Short term (≤ 2 years) |

| Trade policy friction & tariff risk affecting export demand | -0.8% | Export-oriented regions (Coastal provinces) | Short–Medium term (≤4 years) |

| Structural industry constraints (OEM dependence, limited design/IP innovation) | -0.3% | Nationwide, more acute for SMEs | Medium–Long term (2–4+ years) |

| Source: Mordor Intelligence | |||

Tier-1 Office Vacancy and Cautious Leasing Slow New Fit-Out Cycles

Weak leasing conditions in select large-city submarkets encourage tenants to renegotiate terms, lengthen decision cycles, and downsize space. These behaviors reduce the pace of new buildouts and delay refreshes that would otherwise activate larger orders for desks, seating, and storage systems. Suppliers respond by emphasizing retrofit-ready solutions and value-engineered packages, but discretionary upgrades can still slip into later budget periods. Landlords focus on incentives tied to renovation allowances and service quality to preserve occupancy, which narrows the window for premium pricing in the near term. In this context, the China office furniture market relies more on project selectivity and account retention strategies while it waits for stronger demand signals to support full-scale fit-outs.

Raw-Material Inflation and Trade Actions Pressure Margins for Export-Oriented Manufacturers

Furniture suppliers that rely on aluminum alloys, engineered wood, and specialty coatings have faced bouts of input cost volatility that are hard to pass through during competitive bidding. Export-facing producers must also navigate United States trade actions that remain in force on specific categories, including continued orders on wooden cabinets and vanities and a complex layer of tariffs on related furniture goods. Policymaker reports and official reviews continue to monitor China’s WTO compliance and related practices, which add procedural steps and documentation to trade flows. Other economies have signaled tariff responses as part of broader trade positions, reinforcing the need for diversified production footprints to serve key end markets. These factors compress margins for smaller exporters and encourage larger players to invest in nearshoring and overseas warehousing to keep lead times and landed costs under control.

Segment Analysis

By Furniture Type: Seating Dominance Reinforced by AI Health Monitoring and Modular Fit-Out Demand

Seating captured 29.24% of the China office furniture market share in 2025 and is set to expand at the segment’s fastest 8.84% CAGR through 2031, supported by health-centric ergonomics and smart features. Smart and sensor-enabled seating has moved beyond pilot deployments. Commercially available AI-enabled chairs, such as Unigamer’s BC03P smart chair, first launched in China in 2023, integrate pressure sensors and posture-recognition algorithms into mass-market SKUs rather than research prototypes. Performance validation is supported by peer-reviewed evidence: a 2025 posture-monitoring study found smart chairs achieved 94.78% posture detection accuracy, with 97.59% of users correcting posture within 3.27 seconds after alerts, demonstrating quantifiable ergonomic impact rather than anecdotal benefit. Height-adjustable desk ecosystems and compatible seating are co-specified more frequently to ensure full-range adjustability and correct body positioning across tasks. The China office furniture market continues to reward platforms that demonstrate measurable environmental gains, such as carbon-neutral claims supported by life-cycle assessments and increased use of recycled inputs in seating frames and components.

Beyond seating, desks and tables benefit from hybrid work and modular planning needs that emphasize space reconfiguration without major structural changes. Configurable elements that allow quick shifts from individual to collaborative modes are common in contemporary fit-outs and support frequent team resizing. The China office furniture market also favors storage that integrates access control and environment monitoring to safeguard documents and equipment in open-plan settings. Vendors that build ecosystems instead of standalone items can cross-sell over longer cycles and create unified experiences across chairs, desks, and accessories. Certification readiness and emissions testing compliance are now table stakes for project bids in government and regulated sectors, which pushes even entry-level lines to step up materials and finishes.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: B2C/Retail Surges as E-Commerce Platforms Democratize Premium Brands

B2B and direct-from-manufacturer routes commanded 71.37% of the China office furniture market size in 2025 on the strength of enterprise frameworks and public tenders, while B2C/retail is projected to deliver the fastest 12.37% CAGR through 2031. The rapid scale-up of flagship stores on major e-commerce platforms has extended national reach for global and local brands, with logistics partners enabling deliveries that match big-box retail service levels. For buyers, omnichannel access blends digital discovery with physical touchpoints, which supports higher-ticket decisions in seating and workstation categories. Online discovery tools like AR previews and configurable options help reduce returns and increase confidence in remote ordering across both consumer and small-business customers. The China office furniture market is also seeing more collaborative programs where brands integrate platform services with their own service centers to close service gaps.

Within B2B, government procurement frameworks and enterprise agreements continue to favor suppliers that can meet compliance, service, and scale requirements across regions. Overseas warehousing and cross-border logistics investments help export-oriented Chinese brands maintain delivery speed for international customers, which strengthens their reputations at home and abroad. At the same time, B2C expansion on national marketplaces is drawing more premium brands into curated online assortments that focus on value-for-money and consistent quality. The China office furniture industry is adapting to this mix by standardizing spare parts availability, setting clear warranty terms, and offering in-home or on-site assembly options supported by platform partners. This blend of channel capabilities supports steady share gains for online-driven cohorts while B2B remains the backbone for large-scale replacement cycles.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

East China accounted for 37.74% of the China office furniture market share in 2025, reflecting the region’s concentration of design, manufacturing, and logistics resources, while South China is expected to grow at 11.37% CAGR through 2031 on rising branded exports and direct-to-consumer models. Zhejiang’s established seating and ergonomic clusters underpin a mature supplier base that serves global and domestic accounts, supported by R&D capabilities and strong patent activity across key players. Proximity to major ports and a dense ecosystem of component makers enable shorter lead times and faster new-product iteration cycles for office seating, desks, and accessories. Industry associations continue to facilitate global buyer engagement through factory tours and industrial-belt events that connect export programs with digital marketplace initiatives. This foundation supports East China’s sustained leadership in the China office furniture market while leaving room for new niches that emphasize sustainability and AI-enabled ergonomics.

South China’s growth trajectory reflects the transition from OEM-only operations toward brand-forward sales models that leverage international logistics and omnichannel retail. South China, led by Guangdong, remains the country’s largest furniture production base by output value, with districts such as Shunde historically exporting over 80% of locally produced furniture, underscoring the region’s export orientation. Global furniture exports from leading South China manufacturing regions are projected to reach USD 9.6 billion in 2025, representing roughly 27% of China’s total furniture exports, driven in part by digital buyer acquisition and platform-based sales.

Outside the coastal hubs, North China and select central provinces maintain roles in government procurement and public-institution fit-outs, which lean on compliance and lifecycle value. Inbound interest from Belt and Road markets helps sustain export orders for inland factories connected to rail and bonded-zone logistics corridors. Trade dynamics and tariff risk have pushed several exporters to establish overseas production bases and distribution footprints to serve North America and Europe more efficiently. This shift allows headquarters teams in China to retain control over design and intellectual property while localizing assembly and warehousing closer to end customers. The China office furniture market continues to balance regional strengths by matching product specialization with the right channel strategy and compliance posture for each geography.

Competitive Landscape

The competitive field remains fragmented, with leading brands using different strategies to defend share and capture new demand as compliance and service become decisive factors. Companies with enterprise credentials and comprehensive Environmental, Social, and Governance (ESG) reporting are using those assets to differentiate in tenders and global account programs that emphasize lifecycle impacts. Export leaders that invested early in overseas warehouses report improvements in delivery speed and cost control, which supports higher customer satisfaction and repeat orders across major routes. China’s “High-Quality Development Plan for the Furniture Industry” (actively implemented through 2024–2025) explicitly supports scale expansion and brand upgrading, with incentives aimed at cultivating 50 internationally competitive furniture brands and strengthening advanced manufacturing capacity across core provinces such as Zhejiang and Guangdong. This framework has encouraged suppliers to consolidate production into fewer, more automated plants rather than fragmented workshops.

Product innovation has centered on ergonomic seating, height-adjustable desks, and modular systems that support a range of activity-based settings. Smart chairs with integrated sensors and AI-enabled posture guidance now anchor premium ranges, as demonstrated by high-profile launches at national fairs. Cross-border warehouse programs that target sub-three-day delivery in the United States illustrate how logistics capabilities have become a strategic differentiator for Chinese suppliers expanding globally. Meanwhile, flagship showrooms and collaborative concept spaces created by international brands display hybrid collections that blur lines between living and working environments. The China office furniture market rewards brands that integrate engineering depth, supply chain control, and clear environmental disclosures across their portfolios.

Partnerships with marketplaces and curated digital storefronts have opened new routes to premium buyers across more cities, improving discovery and service while reinforcing brand credibility[3]Source: JD.com, “JD.com Brings Scandinavian Design and Quality to Hundreds of Millions of Chinese Consumers with Launch of IKEA Official Flagship Store,” JD Corporate Blog, jdcorporateblog.com. Companies that publish environmental product declarations and lifecycle assessments are finding a smoother path into government and State-Owned Enterprise (SOE) projects that prioritize certified content. Those that pair product advances with international nearshoring or assembly bases are also mitigating tariff exposure while holding lead times steady. With these shifts, the China office furniture market continues to prize compliance, service, and total cost of ownership over headline discounts when buyers make mid-cycle refresh and replacement decisions.

China Office Furniture Industry Leaders

Herman Miller, Inc.

New Qumun Group

Red Apple Furniture

Zhejiang Huafeng Furniture

Aurora China Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Steelcase announced that its carbon-neutral certified chairs received a 2025 China Green Point award, with Asia-Pacific sales momentum noted for these models.

- August 2025: IKEA China opened an official flagship store on JD.com in August 2025, complementing its existing channels and leveraging JD Logistics to extend service to hundreds of cities nationwide.

- May 2025: After 22 years in the Chinese market, KOKUYO and Lamex opened a joint flagship showroom in Shanghai in May 2025, showcasing collections designed for the future of work in a blended living and working context.

China Office Furniture Market Report Scope

Office furniture refers to furnishings designed for use in workplace environments, including desks, chairs, workstations, storage units, and conference furniture. It supports employee productivity, comfort, organization, and efficient use of office space across corporate, institutional, and home-office settings.

The China office furniture market is segmented by furniture type, distribution channel, and geography. By furniture type, the market is segmented into seating, tables, storage, desks, and other office furniture types. By distribution channel, the market is segmented into B2B/direct, B2C/retail, comprising home centres, specialty stores, online, and others. By Geography, the market is segmented into East China, North China, Northeast China, Central China, and the Rest of China. The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

By Furniture Type

| Seating |

| Tables |

| Storage |

| Desks |

| Other Furniture Type (Desk Divider, Office Sofas, Bookcases, Benches, Stools etc.) |

By Distribution Channel

| B2B/Directly from Manufacturer | |

| B2C/Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channel |

By Geography

| East China |

| North China |

| Northeast China |

| Central China |

| Rest of China |

| By Furniture Type | Seating | |

| Tables | ||

| Storage | ||

| Desks | ||

| Other Furniture Type (Desk Divider, Office Sofas, Bookcases, Benches, Stools etc.) | ||

| By Distribution Channel | B2B/Directly from Manufacturer | |

| B2C/Retail | Home Centers | |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channel | ||

| By Geography | East China | |

| North China | ||

| Northeast China | ||

| Central China | ||

| Rest of China | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the China office furniture market?

The China office furniture market size is USD 38.27 billion in 2026 and is projected to reach USD 51.87 billion by 2031 at a 6.27% CAGR.

Which product category is growing fastest within the China office furniture market?

Seating leads with 29.24% in 2025 and is expected to post the fastest 8.84% CAGR through 2031, supported by smart ergonomics and health-oriented features.

How are channels shifting in the China office furniture market?

B2B remains dominant, while B2C is expanding fastest due to omnichannel platforms and improved logistics coverage across hundreds of cities.

What role does green procurement play in the China office furniture market?

National procurement guidance prioritizes certified green products, which elevates suppliers with lifecycle documentation, testing credentials, and carbon transparency.

Which regions lead demand in the China office furniture market?

East China holds the largest share due to mature clusters and export infrastructure, while South China is the fastest growing on branding and omnichannel expansion.

What differentiates leading suppliers in the China office furniture market?

Leaders combine ESG documentation, smart ergonomics, and logistics capabilities such as overseas warehouses and omnichannel programs to win enterprise and consumer demand.