| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 614.8 Million |

| Market Size (2030) | USD 866.1 Million |

| CAGR (2025 - 2030) | 7.10 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

China Micronutrient Fertilizer Market Analysis

The China Micronutrient Fertilizer Market size is estimated at 614.8 million USD in 2025, and is expected to reach 866.1 million USD by 2030, growing at a CAGR of 7.10% during the forecast period (2025-2030).

China's agricultural sector is undergoing significant transformation driven by the imperative to enhance productivity and ensure food security for its vast population. The country's position as the world's largest producer of vegetables, with an output of 800 million tons in 2022, underscores the scale of its agricultural operations and the corresponding demand for micronutrient fertilizers. Agricultural intensification efforts are particularly evident in the irrigation infrastructure development, with regions like Xinjiang, Shandong, Hebei, and Henan leading the way in advanced irrigation practices. This intensification has led to increased scrutiny of soil micronutrient health and nutrient management practices, as farmers seek to optimize yield while maintaining soil fertility.

The micronutrient fertilizer landscape in China is characterized by a significant disparity between conventional and specialty fertilizers, with conventional fertilizers commanding a dominant 95.3% market share in 2022. This predominance reflects the current market maturity and farmer preferences, though a gradual shift towards specialty fertilizers is emerging, driven by environmental concerns and the push for more efficient nutrient delivery systems. The market is witnessing increased adoption of advanced application methods, particularly in high-value horticultural crops, where precision farming techniques are gaining traction.

A critical challenge facing the sector is the widespread soil micronutrient deficiency in Chinese agricultural soils, with over 48.6 million hectares of land, primarily in northern China's calcareous regions, experiencing deficiencies in zinc and manganese. The eastern regions face particular challenges with molybdenum and boron deficiencies, necessitating targeted intervention through specialized fertilizer applications. This situation has spurred innovation in fertilizer formulations and application technologies, with manufacturers developing products specifically tailored to address regional soil deficiency patterns.

The horticultural sector represents a significant growth opportunity for micronutrient fertilizers, with horticultural crops accounting for 28.7% of China's total cultivation area in 2022. The sector's expansion is driven by increasing domestic demand for high-quality fruits and vegetables, particularly in urban areas where consumer preferences are shifting towards premium produce. This trend has catalyzed the development of more sophisticated fertilizer products, especially those designed for greenhouse cultivation and precision farming systems, where optimal crop nutrition management is crucial for achieving desired quality standards and yield targets.

China Micronutrient Fertilizer Market Trends

The expansion of the cultivation area is driven by increasing demand for food and the country's goal to achieve self-sufficiency in staple food

- China's cultivation area for field crops expanded marginally from 126.6 million ha in 2018 to 127.8 million ha in 2022, representing 70.8% of the total cultivated land. In 2022, Corn dominated the field crop landscape, commanding a 34.2% share, trailed by rice at 23.6% and wheat at 18.3%. This increase in cultivation area is poised to drive up fertilizer demand in the nation.

- China's field crop calendar revolves around two seasons: spring/summer (April-September) and winter. Spring crops encompass early corn, early rice, early wheat, and cotton, while winter crops center around winter wheat and rapeseed. Yet, it's rice and corn that take the spotlight, contributing to a third of China's grain output. As the world's leading rice producer, China dedicated 30 million hectares to rice farming in 2022, yielding a bountiful 210 million tons. Key rice-growing regions span Heilongjiang, Hunan, Jiangxi, Hubei, Jiangsu, Sichuan, Guangxi, Guangdong, and Yunan. Looking at corn, China was set to produce 277.2 million tons in 2022-2023, a 4.6 million ton surge from the previous year, buoyed by a robust harvest. The Northeast provinces of Heilongjiang, Jilin, and Inner Mongolia stand out as the corn powerhouses.

- While spring dominates China's cropping season, it grapples with heat spikes in June and July. Rice, a dietary staple for millions, bears the brunt. These scorching temperatures, coupled with meager rainfall, exacerbate mineral depletion in the soil, necessitating higher fertilizer application. Such arid conditions can also curtail crop yields.

Understand The Key Trends Shaping This Market

Download PDF

In China, rapeseed or canola is applied with large amounts of micronutrients compared to other field crops

- Micronutrients play a vital role in crop nutrition and growth, and their deficiency significantly impacts yields. Field crops typically receive an average application rate of 5.2 kg/hectare for micronutrient fertilizers. Among these, manganese takes the lead, with an application rate of 9.8 kg/hectare in 2022, despite being the eleventh most abundant micronutrient in the earth's crust. However, when the soil pH reaches seven or higher, chemical and microbial oxidation occur, leading to the immobilization of plant-available Mn2+. This, in turn, triggers manganese deficiency in plants.

- Following manganese, copper took the market lead with an application rate of 7.3 kg/hectare, trailed by zinc at 4.1 kg/hectare, and iron at 3.3 kg/hectare in 2022.

- In China, rapeseed or canola stands out for its higher micronutrient application rates compared to other field crops. It receives an average of 10.79 kg/hectare of micronutrient fertilizers, given the significant impact of micronutrient deficiency on oil yield. Notably, foliar application of manganese and molybdenum has shown a 1% increase in oil content in the seeds.

- Micronutrient deficiencies in soil can arise from excessive phosphate fertilization and other natural factors. Phosphate, in particular, can limit the availability of iron, zinc, and copper to crops. In China, a strategy was adopted to enhance field crop yields by reducing phosphate fertilization while simultaneously increasing zinc fertilization.

- Optimally applying micronutrient fertilizers can enhance plant efficiency in absorbing primary nutrients from the soil, thereby reducing the overall fertilizer requirement in vegetable crops.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- The growing interest in fruit and vegetable cultivation due to better market opportunities

- In China, irrigated croplands occupy a major portion, constituting about half of the total cropland area

- According to Chinese Ministry of Agriculture, over 48.6 million hectares of soil in China exhibit deficiencies in zinc and manganese

Segment Analysis: Product

Copper Segment in China Micronutrient Fertilizer Market

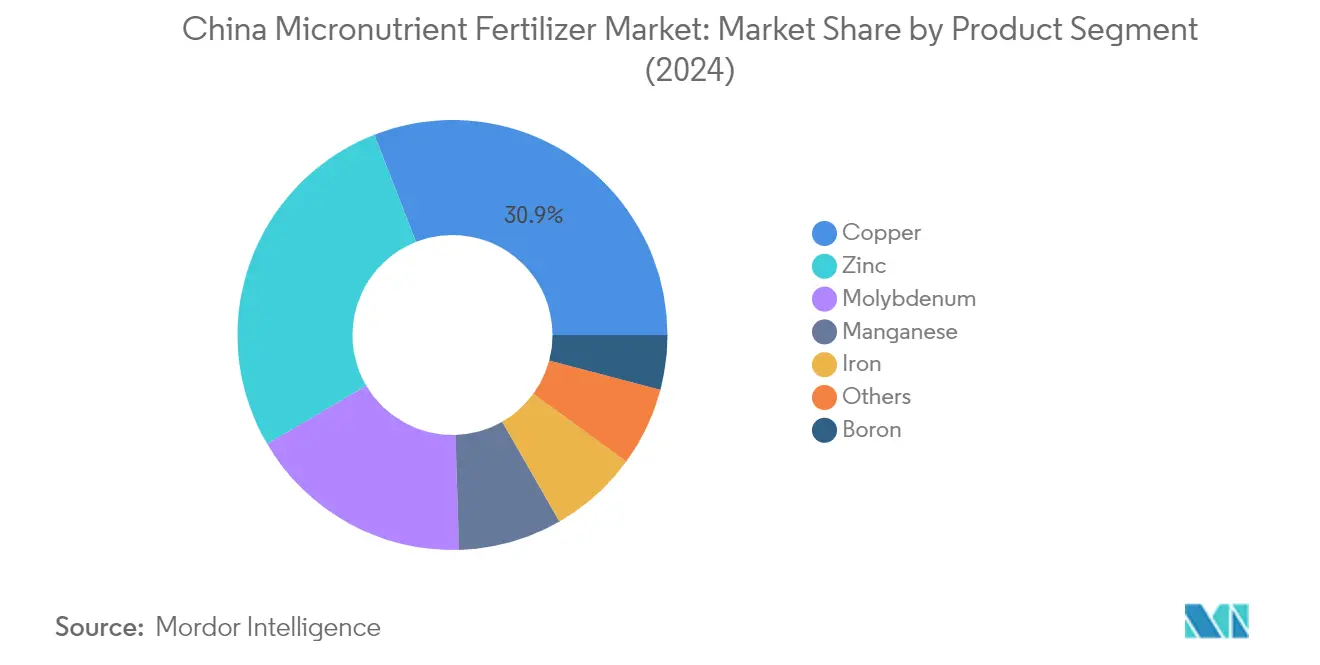

Copper has emerged as the dominant segment in China's micronutrient fertilizer market, commanding approximately 31% market share in 2024. This significant market position can be attributed to copper fertilizer's crucial role in multiple enzyme processes and chlorophyll formation in plants. The conventional copper fertilizers, particularly copper sulfate, maintain a strong presence due to their widespread availability and cost-effectiveness compared to specialty alternatives. The liquid form of copper fertilizer has shown particularly strong performance, with manufacturers focusing on developing enhanced formulations that improve nutrient absorption and plant protection against fungal diseases. Additionally, copper's dual functionality as both a vital plant nutrient and a protective agent against plant diseases has further cemented its position as the leading micronutrient fertilizer in the Chinese market.

Molybdenum Segment in China Micronutrient Fertilizer Market

The molybdenum segment is demonstrating remarkable growth potential in China's micronutrient fertilizer market, with projections indicating an impressive growth trajectory of approximately 8% during 2024-2029. This accelerated growth is primarily driven by molybdenum's increasing significance in crop production, particularly in regions with predominant deficiencies such as Eastern China, Central China, Southern China, and the Yangtze River Basin. The segment's growth is further supported by the rising adoption of specialty molybdenum fertilizers, which offer precise nutrient control and delivery mechanisms. The fertigation method of application has gained particular traction, as it allows for uniform distribution of molybdenum and helps mitigate the risk of localized nutrient deficiencies, making it increasingly popular among Chinese farmers.

Remaining Segments in Product Segmentation

The other significant segments in China's micronutrient fertilizer market include zinc fertilizer, iron fertilizer, manganese, boron fertilizer, and other trace elements. Zinc holds substantial importance due to its role in enzyme co-factors and protein structures, while iron is crucial for photosynthesis and overall plant health. Manganese plays a vital role in photosynthesis and chlorophyll production, and boron is essential for cell division and plant growth regulation. Each of these segments serves specific agricultural needs and contributes to the overall market dynamics. The market has seen increasing innovation in formulation technologies across these segments, with manufacturers developing specialized products that cater to specific crop requirements and soil conditions prevalent in different regions of China.

Segment Analysis: Application Mode

Soil Application Segment in China Micronutrient Fertilizer Market

The soil application segment dominates China's micronutrient fertilizer market, commanding approximately 95% market share in 2024, valued at over USD 550 million. This overwhelming preference for soil application can be attributed to Chinese farmers' familiarity with conventional granular fertilizers, which are exclusively applied through soil. The segment's dominance is further strengthened by the widespread availability and adoption of conventional fertilizers, coupled with their cost-effectiveness compared to other application methods. The soil application method has proven particularly effective for key micronutrients like boron fertilizer and zinc fertilizer, which commanded shares of 26.6% and 25.7%, respectively, when applied through soil. Additionally, the persistent need to enhance soil fertility and the comprehensive distribution network for soil-applied fertilizers across China's agricultural regions has helped maintain this segment's market leadership.

Fertigation Segment in China Micronutrient Fertilizer Market

The fertigation segment is emerging as the fastest-growing application method in China's micronutrient fertilizer market, projected to grow at approximately 7% CAGR from 2024 to 2029. This growth is primarily driven by fertigation's superior efficiency in delivering nutrients directly to the plant's root zone, particularly beneficial in high moisture and waterlogging conditions where certain micronutrients like zinc can become unavailable to plants. The segment's growth is further supported by the increasing adoption of modern irrigation systems and the method's compatibility with water-soluble fertilizers, which accounted for about 57% of fertigation applications. The expansion of greenhouse cultivation and precision farming practices across China has also contributed to the rising popularity of fertigation, as it allows for precise nutrient delivery while minimizing waste and environmental impact.

Remaining Segments in Application Mode

The foliar application segment represents a crucial component of China's micronutrient fertilizer market, particularly valued for its effectiveness in addressing immediate nutrient deficiencies in crops. This method has gained traction among farmers due to its ability to bypass soil-related limitations and deliver nutrients directly to plant tissues. Foliar application has proven especially effective for immobile nutrients and in situations where rapid nutrient uptake is required. The method's popularity is particularly notable in intensive farming systems and high-value crop production, where precise nutrient management is critical for optimal yield and quality.

Segment Analysis: Crop Type

Field Crops Segment in China Micronutrient Fertilizer Market

Field crops dominate China's micronutrient fertilizer market, commanding approximately 70% of the total market share in 2024. This segment's prominence can be attributed to China's vast agricultural landscape, where field crops like rice, wheat, maize, peanuts, and cotton occupy over 131 million hectares of cultivable land. The segment's dominance is particularly evident in regions with intensive farming practices, where micronutrient deficiencies are common due to continuous cropping. Among micronutrients, boron fertilizer and zinc emerge as the most in-demand nutrients for field crops, accounting for over half of the total consumption, followed by iron, manganese, and copper. This substantial market share reflects the critical role of micronutrients in enhancing field crop yields, especially in areas with nutrient-depleted soils and regions practicing intensive agriculture.

Turf & Ornamental Segment in China Micronutrient Fertilizer Market

The turf and ornamental segment is experiencing remarkable growth in China's micronutrient fertilizer market, projected to expand at approximately 10% CAGR from 2024 to 2029. This impressive growth trajectory is driven by several factors, including the rising popularity of indoor aesthetic plants, expanding home gardens, and the flourishing nursery industry. The segment's growth is particularly notable in urban areas where there's increasing demand for landscaping and ornamental plants. Boron has emerged as the leading micronutrient in this segment, followed closely by zinc, as these elements prove crucial for enhancing turf grasses' resilience against both biotic and abiotic stresses. The segment's expansion is further supported by the growing trend of urban greening initiatives and the increasing focus on creating sustainable urban landscapes across Chinese cities.

Remaining Segments in Crop Type

The horticultural crops segment represents a significant portion of China's micronutrient fertilizer market, playing a crucial role in the country's agricultural diversity. This segment encompasses a wide range of fruits and vegetables, with particular emphasis on high-value crops grown in advanced settings like greenhouses. The segment's importance is magnified by China's position as the world's largest producer of fruits and vegetables, with major growing regions spread across South China, Southwest China, the Yangtze River Area, and other key agricultural zones. The segment's performance is closely tied to the increasing consumer demand for high-quality produce and the growing emphasis on nutritional value in fruits and vegetables, driving the need for balanced micronutrient application.

China Micronutrient Fertilizer Industry Overview

Top Companies in China Micronutrient Fertilizer Market

The Chinese micronutrient fertilizer market is characterized by significant product innovation and strategic expansion initiatives among key players. Companies are increasingly focusing on developing specialized formulations, including water-soluble and controlled-release variants, to meet evolving agricultural needs. Digital platforms and expert systems are being deployed to support customized fertilization programs and enhance customer engagement. Strategic partnerships, particularly with local players, are becoming prevalent to strengthen distribution networks and manufacturing capabilities. Companies are also expanding their presence through new trading entities and production facilities, while simultaneously investing in research and development to create environmentally sustainable solutions. The industry witnesses continuous efforts to improve product efficiency through technologies like chelated micronutrients and coating, alongside developments in application methods such as fertigation and foliar spraying.

Market Led by Global Players, Local Growth

The competitive landscape is dominated by established global players who leverage their extensive research capabilities and international experience to maintain market leadership. These multinational corporations typically operate through local subsidiaries and joint ventures, combining global expertise with local market knowledge. The market structure shows a mix of large diversified agricultural input companies and specialized fertilizer manufacturers, with global leaders maintaining significant market share through their established brands and distribution networks.

The market exhibits moderate consolidation, with the top players controlling a substantial portion of the market while numerous smaller local players serve regional markets. Strategic partnerships and collaborations between international and domestic companies are increasingly common, particularly in manufacturing and distribution. Local companies are gradually strengthening their position through technological partnerships and product innovations, though they primarily compete in specific regional markets or product segments. The industry sees steady merger and acquisition activity, primarily focused on expanding geographical presence and acquiring technological capabilities.

Innovation and Distribution Drive Market Success

Success in the Chinese agricultural micronutrients market increasingly depends on developing innovative, efficient delivery systems and maintaining strong distribution networks. Companies need to focus on creating specialized products for specific crops and soil conditions while ensuring cost-effectiveness. Building strong relationships with agricultural cooperatives and local farming communities has become crucial for market penetration. Investment in research and development, particularly in areas of nutrient efficiency and environmental sustainability, is becoming a key differentiator for market success.

Market players must navigate complex regulatory requirements while adapting to changing environmental regulations and sustainability demands. Companies need to develop comprehensive digital platforms and technical support services to assist farmers in optimal product usage. The ability to provide integrated nutrient management solutions, rather than standalone products, is becoming increasingly important. Success also depends on building robust supply chains that can ensure product availability across China's diverse agricultural regions while maintaining product quality and competitive pricing. Future growth opportunities lie in developing eco-friendly formulations and precision agriculture solutions that align with government initiatives for sustainable agriculture.

China Micronutrient Fertilizer Market Leaders

-

Coromandel International Ltd.

-

Hebei Monband Water Soluble Fertilizer Co. Ltd

-

ICL Group Ltd

-

Sociedad Quimica y Minera de Chile SA

-

Yara International ASA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

China Micronutrient Fertilizer Market News

- February 2019: Haifa Group announced the opening of a new trading company in China. The establishment of the new Haifa subsidiary in China will enable the group to significantly expand its offerings to China agriculture sector.

- November 2018: ICL Fertilizers developed a new line of premium fertilizers that help farmers feed their crops precisely. Polysulphate, ICLPotashpluS, and ICLPKpluS are manufactured from polyhalite, a mineral extracted at the ICL mine in Boulby, United Kingdom, to meet the agricultural need for balanced, targeted nutrition.

- July 2018: Haifa Group introduced a novel range of coated micronutrients, enabling an all-season complete nutrition. Based on Multicote™ technology, the coated micronutrients provide your crops with all the benefits of controlled-release nutrition.

Free With This Report

Along with the report, We also offer a comprehensive and exhaustive data pack with 25+ graphs on area under cultivation and average application rate per hectare. The data pack includes Globe, North America, Europe, Asia-Pacific, South America, and Africa.

China Micronutrient Fertilizer Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

-

4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

-

4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

-

5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

-

5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles

- 6.4.1 Coromandel International Ltd.

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 Hebei Monband Water Soluble Fertilizer Co. Ltd

- 6.4.5 ICL Group Ltd

- 6.4.6 Sociedad Quimica y Minera de Chile SA

- 6.4.7 Yara International ASA

- *List Not Exhaustive

7. KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- CULTIVATION OF FIELD CROPS IN HECTARE, CHINA, 2017 - 2022

- Figure 2:

- CULTIVATION OF HORTICULTURAL CROPS IN HECTARE, CHINA, 2017 - 2022

- Figure 3:

- CONSUMPTION OF MICRONUTRIENTS BY FIELD CROPS IN KG/HECTARE, CHINA, 2022

- Figure 4:

- CONSUMPTION OF MICRONUTRIENTS BY HORTICULTURAL CROPS IN KG/HECTARE, CHINA, 2022

- Figure 5:

- AGRICULTURAL LAND EQUIPPED FOR IRRIGATION IN HECTARE, CHINA, 2022

- Figure 6:

- MICRONUTRIENTS FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 7:

- MICRONUTRIENTS FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 8:

- MICRONUTRIENTS FERTILIZER CONSUMPTION BY PRODUCT IN METRIC TON, CHINA, 2017 - 2030

- Figure 9:

- MICRONUTRIENTS FERTILIZER CONSUMPTION BY PRODUCT IN USD, CHINA, 2017 - 2030

- Figure 10:

- MICRONUTRIENTS FERTILIZER CONSUMPTION VOLUME BY PRODUCT IN %, CHINA, 2017 VS 2023 VS 2030

- Figure 11:

- MICRONUTRIENTS FERTILIZER CONSUMPTION VALUE BY PRODUCT IN %, CHINA, 2017 VS 2023 VS 2030

- Figure 12:

- BORON FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 13:

- BORON FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 14:

- BORON FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 15:

- COPPER FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 16:

- COPPER FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 17:

- COPPER FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 18:

- IRON FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 19:

- IRON FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 20:

- IRON FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 21:

- MANGANESE FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 22:

- MANGANESE FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 23:

- MANGANESE FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 24:

- MOLYBDENUM FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 25:

- MOLYBDENUM FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 26:

- MOLYBDENUM FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 27:

- ZINC FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 28:

- ZINC FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 29:

- ZINC FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 30:

- OTHERS FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 31:

- OTHERS FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 32:

- OTHERS FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 33:

- MICRONUTRIENTS MICRONUTRIENTS FERTILIZER CONSUMPTION BY APPLICATION MODE IN METRIC TON, CHINA, 2017 - 2030

- Figure 34:

- MICRONUTRIENTS MICRONUTRIENTS FERTILIZER CONSUMPTION BY APPLICATION MODE IN USD, CHINA, 2017 - 2030

- Figure 35:

- MICRONUTRIENTS MICRONUTRIENTS FERTILIZER CONSUMPTION VOLUME BY APPLICATION MODE IN %, CHINA, 2017 VS 2023 VS 2030

- Figure 36:

- MICRONUTRIENTS MICRONUTRIENTS FERTILIZER CONSUMPTION VALUE BY APPLICATION MODE IN %, CHINA, 2017 VS 2023 VS 2030

- Figure 37:

- FERTIGATION APPLICATION OF MICRONUTRIENTS FERTILIZER IN METRIC TON, CHINA, 2017 - 2030

- Figure 38:

- FERTIGATION APPLICATION OF MICRONUTRIENTS FERTILIZER IN USD, CHINA, 2017 - 2030

- Figure 39:

- FERTIGATION APPLICATION OF MICRONUTRIENTS FERTILIZER IN VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 40:

- FOLIAR APPLICATION OF MICRONUTRIENTS FERTILIZER IN METRIC TON, CHINA, 2017 - 2030

- Figure 41:

- FOLIAR APPLICATION OF MICRONUTRIENTS FERTILIZER IN USD, CHINA, 2017 - 2030

- Figure 42:

- FOLIAR APPLICATION OF MICRONUTRIENTS FERTILIZER IN VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 43:

- SOIL APPLICATION OF MICRONUTRIENTS FERTILIZER IN METRIC TON, CHINA, 2017 - 2030

- Figure 44:

- SOIL APPLICATION OF MICRONUTRIENTS FERTILIZER IN USD, CHINA, 2017 - 2030

- Figure 45:

- SOIL APPLICATION OF MICRONUTRIENTS FERTILIZER IN VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 46:

- MICRONUTRIENTS MICRONUTRIENTS FERTILIZER CONSUMPTION BY CROP TYPE IN METRIC TON, CHINA, 2017 - 2030

- Figure 47:

- MICRONUTRIENTS MICRONUTRIENTS FERTILIZER CONSUMPTION BY CROP TYPE IN USD, CHINA, 2017 - 2030

- Figure 48:

- MICRONUTRIENTS MICRONUTRIENTS FERTILIZER CONSUMPTION VOLUME BY CROP TYPE IN %, CHINA, 2017 VS 2023 VS 2030

- Figure 49:

- MICRONUTRIENTS MICRONUTRIENTS FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2017 VS 2023 VS 2030

- Figure 50:

- MICRONUTRIENTS FERTILIZER CONSUMPTION BY FIELD CROPS IN METRIC TON, CHINA, 2017 - 2030

- Figure 51:

- MICRONUTRIENTS FERTILIZER CONSUMPTION BY FIELD CROPS IN USD, CHINA, 2017 - 2030

- Figure 52:

- MICRONUTRIENTS FERTILIZER CONSUMPTION VALUE BY PRODUCT IN %, CHINA, 2023 VS 2030

- Figure 53:

- MICRONUTRIENTS FERTILIZER CONSUMPTION BY HORTICULTURAL CROPS IN METRIC TON, CHINA, 2017 - 2030

- Figure 54:

- MICRONUTRIENTS FERTILIZER CONSUMPTION BY HORTICULTURAL CROPS IN USD, CHINA, 2017 - 2030

- Figure 55:

- MICRONUTRIENTS FERTILIZER CONSUMPTION VALUE BY PRODUCT IN %, CHINA, 2023 VS 2030

- Figure 56:

- MICRONUTRIENTS FERTILIZER CONSUMPTION BY TURF & ORNAMENTAL IN METRIC TON, CHINA, 2017 - 2030

- Figure 57:

- MICRONUTRIENTS FERTILIZER CONSUMPTION BY TURF & ORNAMENTAL IN USD, CHINA, 2017 - 2030

- Figure 58:

- MICRONUTRIENTS FERTILIZER CONSUMPTION VALUE BY PRODUCT IN %, CHINA, 2023 VS 2030

- Figure 59:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, CHINA, 2017 - 2030

- Figure 60:

- CHINA MICRONUTRIENT FERTILIZER MARKET, MOST ADOPTED STRATEGIES, 2018 - 2021

- Figure 61:

- MARKET SHARE OF MAJOR PLAYERS IN %, CHINA

China Micronutrient Fertilizer Industry Segmentation

Boron, Copper, Iron, Manganese, Molybdenum, Zinc, Others are covered as segments by Product. Fertigation, Foliar, Soil are covered as segments by Application Mode. Field Crops, Horticultural Crops, Turf & Ornamental are covered as segments by Crop Type.| Product | Boron |

| Copper | |

| Iron | |

| Manganese | |

| Molybdenum | |

| Zinc | |

| Others | |

| Application Mode | Fertigation |

| Foliar | |

| Soil | |

| Crop Type | Field Crops |

| Horticultural Crops | |

| Turf & Ornamental |

Need A Different Region or Segment?

Customize Now

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Micronutients: Zn, Mn, Cu, Fe, Mo, B, and Others

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF