Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

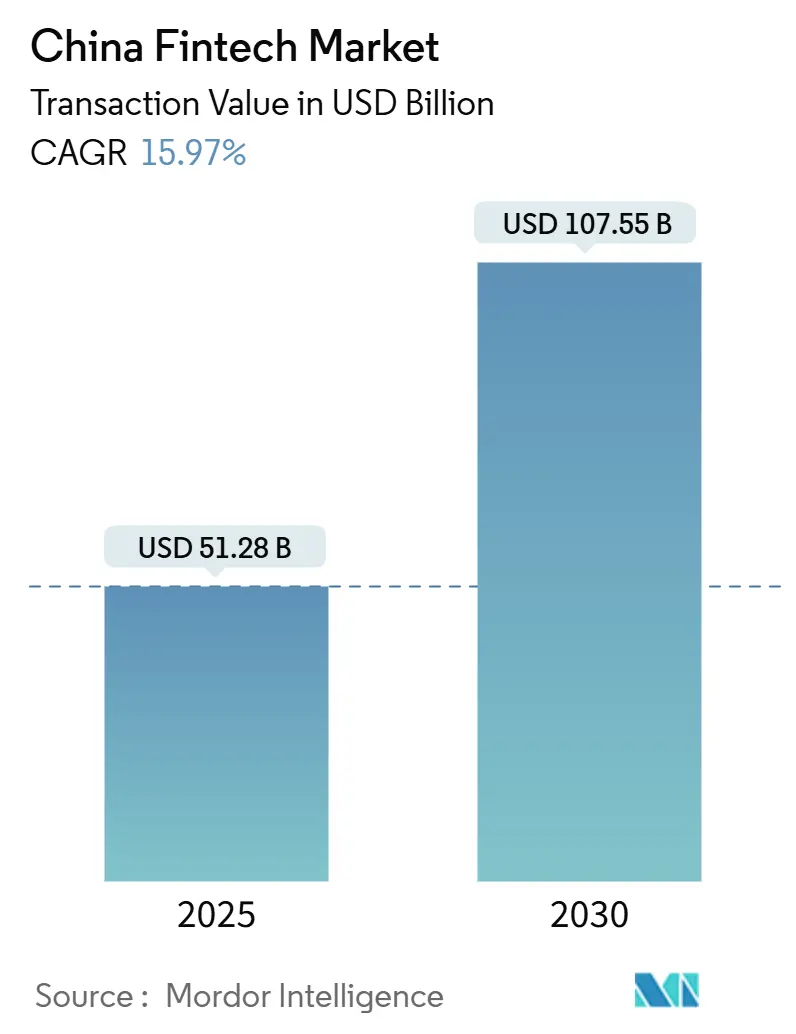

| Market Size (2025) | USD 51.28 Billion |

| Market Size (2030) | USD 107.55 Billion |

| Growth Rate (2025 - 2030) | 15.97% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Fintech Market Analysis by Mordor Intelligence

The China fintech market is valued at USD 51.28 billion in 2025 and is on track to climb to USD 107.55 billion by 2030, advancing at a 15.97% CAGR. Momentum comes from three converging forces: (1) nationwide rollout of the digital yuan, which is triggering a new payment rail beyond traditional mobile wallets; (2) a pivot by incumbent banks toward cloud-native architecture that unlocks bank-as-a-service revenue; and (3) fast-maturing regulation that replaced volume-chasing tactics with sustainable, API-driven growth. Competitive pressure is shifting from customer acquisition to data-layer integration such as credit scoring, robo-advice, and underwriting all move onto AI engines. New distribution corridors in tier-2/3 cities are lifting transaction volumes without the physical branch networks that previously capped reach. Meanwhile, international payment interoperability through UnionPay and Mastercard is widening the addressable cross-border pool for the Chinese fintech market.

Key Report Takeaways

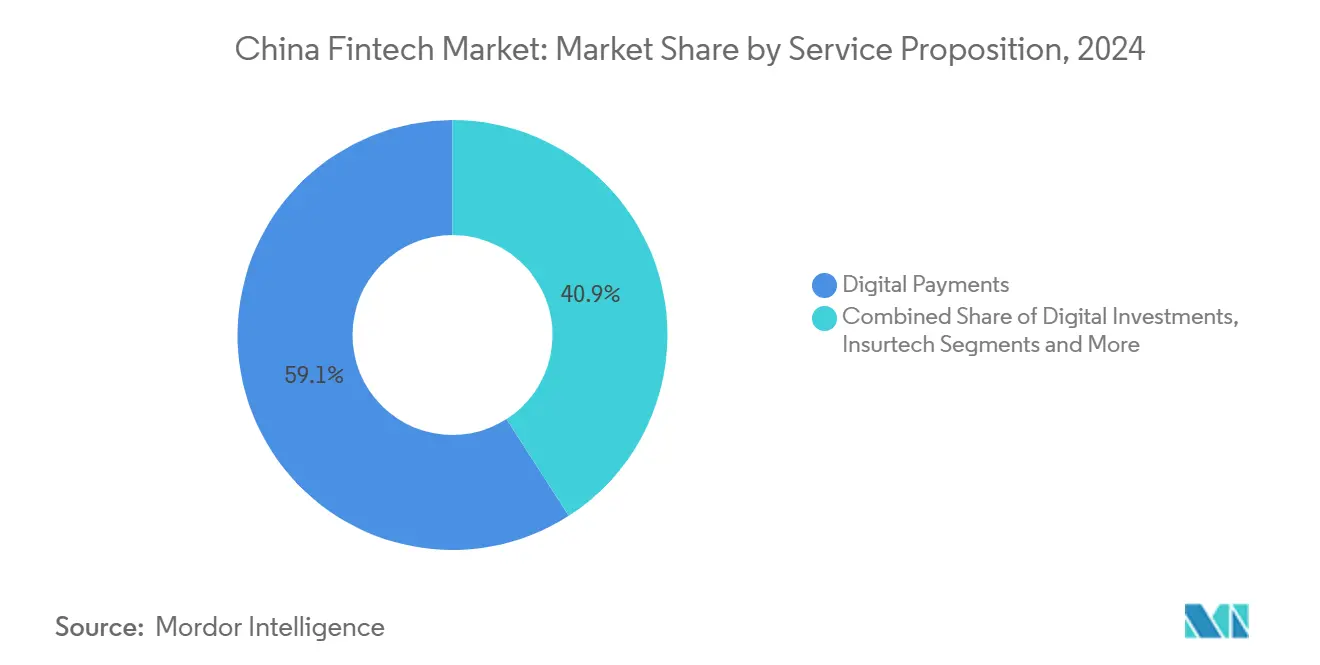

- By service proposition, digital payments led with 59.1% of the China fintech market share in 2024, while neobanking is projected to expand at a 19.63% CAGR through 2030.

- By end-user, the retail segment accounted for 68.2% of the China fintech market size in 2024 and is expected to grow at 17.14% CAGR to 2030.

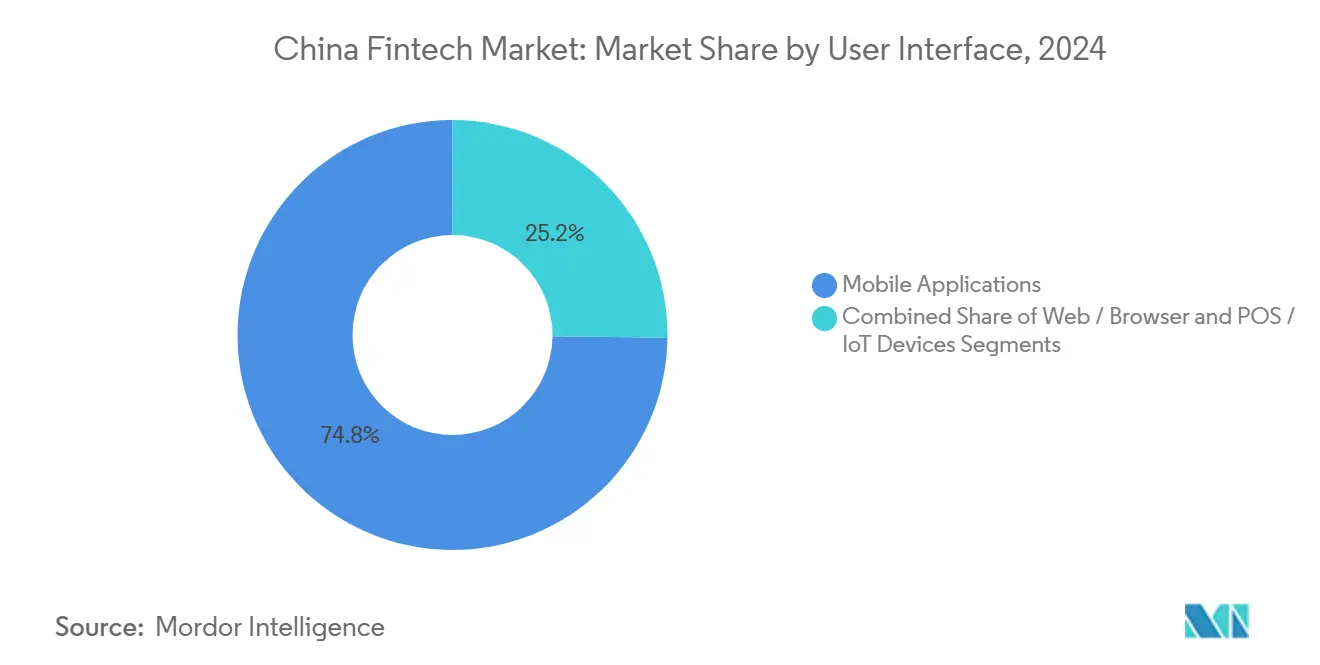

- By user interface, the mobile applications segment captured 74.8% share of the China fintech market size in 2024; the POS/IoT devices segment is projected to record the fastest forecast growth at an 18.65% CAGR.

China Fintech Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| e-CNY deployment in tier-2/3 cities | +2.1% | National, tier-2/3 focus | Medium term (2–4 years) |

| NetsUnion clearing mandate for third-party wallets | +1.8% | National | Short term (≤ 2 years) |

| SME financing gap fuelling supply-chain platforms | +1.5% | Eastern provinces | Medium term (2–4 years) |

| Wealth Management Connect lifting robo-advisors | +1.2% | Greater Bay Area | Medium term (2–4 years) |

| Commercial health-insurance tax incentives driving InsurTech | +0.9% | National, early gains in tier-1 cities | Long term (≥ 4 years) |

| Cloud-native core upgrades expanding BaaS/API consumption | +1.3% | National, concentrated in financial centers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

PBOC e-CNY roll-out accelerating digital payments adoption

Transaction value on the digital yuan chain experienced significant growth by May 2024, showcasing a substantial increase compared to the previous year[1]World Economic Forum, “Central Bank Digital Currencies in Emerging Economies,” weforum.org. The wallet’s tiered design permits card-based usage on basic handsets, removing the smartphone requirement that limited earlier wallets. As a result, 15.3% of rural internet users reported e-CNY usage by April 2024, unlocking a fresh cohort of consumers. Commercial banks distribute the currency under a PBOC dual-layer model, effectively converting legacy branches into fintech nodes and reinforcing digitalization throughout the China fintech market.

NetsUnion clearing mandate boosting third-party payment volumes

Centralized clearing lowered merchant integration costs, aiding smaller providers and boosting consumer confidence. PBOC data shows a 46% jump in users aged 60+ adopting mobile payments in 2024. Uniform fraud-monitoring rules now let platforms turn resources toward value-added services rather than basic settlement, lifting overall wallet throughput across the China fintech market.

SME financing gap driving P2P & supply-chain fintech platforms

Asia’s supply-chain finance volume hit USD 486 billion in 2023, up 17% YoY, with China holding the largest slice. Each 1% rise in supply-chain finance correlates with a 0.1894% efficiency gain for SRNI SMEs, illustrating why alternative lenders capture short-term liquidity demand quickly. Big-tech lenders now price unsecured SME loans at 14.6% average interest yet realize repayment at 46% of contractual maturity, limiting balance-sheet risk.[2]Princeton University, “Big-Tech Lending Risk Study,” csr.princeton.edu

Wealth Management Connect schemes fueling robo-advisor uptake

Eligibility expansion in January 2024 opened the Wealth Management Connect channel to a broader investor base. Parallel tax incentives helped drive 72.8 million voluntary pension accounts by November 2024. Banks respond by embedding AI advisory modules; China Merchants Bank’s “Family Trust Cloud” and ICBC Private Banking’s enhanced Intelligent Investment Advisory exemplify how digital portfolios migrate upmarket.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Security Law constraining cross-border SaaS | -1.2% | National | Short term (≤ 2 years) |

| Rising micro-lending NPL ratios | -0.8% | Tier-2/3 cities | Medium term (2–4 years) |

| Mobile-payment saturation in tier-1 cities | -0.6% | Tier-1 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Security Law tightening cross-border data transfers

New Network Data Security Management Regulations, effective January 2025, require domestic security reviews before external data transfers. Although March 2024 adjustments raised exemptions to 100,000 records per year, SaaS fintech’s must still segment datasets and stage audits[3]Cyberspace Administration of China, “Cross-Border Data Transfer Q&A,” cac.gov.cn. Compliance overhead diverts engineering talent away from front-end innovation, trimming the near-term growth slope for the China fintech market.

Rising NPL ratio in micro-lending elevating capital-adequacy burdens

Delinquency for big-tech consumer loans sits at 2.6%, above traditional loan books. Regulators now oblige platforms to retain larger capital buffers, tightening available lending capacity just as demand from first-time borrowers swells. Liquidity squeeze is most acute outside tier-1 hubs, slowing loan origination volumes that underpin rural fintech spending.

Segment Analysis

By Service Proposition: Dominance of payments versus acceleration of neobanking

Digital Payments held a 59.1% share of the market in 2024, giving the category the largest stake in the China fintech market size. Alipay and WeChat Pay collectively process a major share of mobile wallet flows, a concentration that cements their scale economics. Cross-border expansion through Alipay+ across 70 markets further extends reach. Nevertheless, penetration in tier-1 cities is flattening, and incremental growth is tilting toward value-added micro-insurance and investment modules housed within the same wallets.

Neobanking is projected to record a 19.63% forecast CAGR through 2030, the fastest in the sector. WeBank now serves 300 million account holders while maintaining an operating cost-to-asset ratio well below joint-stock banks. Cloud-native cores mean the marginal cost of new products approaches zero, accelerating the neobank flywheel. The shift also raises the competitive bar for regional banks that still run legacy mainframes, nudging them toward BaaS partnerships as a defensive posture within the China fintech market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Retail ecosystem dominance backed by super-apps

Retail users generated 68.2% of 2024 revenues, thanks to frictionless financial integration in e-commerce checkouts, ride-hailing, and grocery delivery. Super-apps funnel consumers from social chat to savings without leaving a single interface, locking in retention rates that exceed traditional branch banking by wide margins. Uptake of digital yuan in daily shopping and new credit-card rules enabling Hong Kong issuers to roam onshore both inject additional payment volume, extending the retail grip on the China fintech market share.

Corporate adoption lags but is climbing via supply-chain finance APIs that mesh with enterprise resource planning suites. Regionally, exporters in the Yangtze River Delta rely on real-time treasury dashboards to bridge CNH collection and USD settlement, an area where fintech margins remain attractive. Government policy pushing green-finance disclosure also nudges mid-market firms toward fintech channels for low-carbon supply-chain data, sowing new revenue pockets over the forecast horizon.

By User Interface: Mobile primacy as POS/IoT scales

Mobile applications own 74.8% of front-end touchpoints in 2024, underscoring China’s long-running mobile-first preference. Average session length rose from 6.1 to 6.4 minutes while day-1 retention nudged up to 24%, securing wallet stickiness. Super-app ecosystems mean that payments, lending, insurance, and investment co-exist in a unified UX, bolstering engagement across product lines within the China fintech market.

POS/IoT terminals exhibit an 18.65% forecast CAGR through 2030. Shoppers increasingly tap NFC-enabled kiosks that auto-switch between e-CNY, Alipay, UnionPay QuickPass, or card networks. Hardware vendors ride China’s 21% YoY rise in cellular IoT module shipments, embedding QR acceptance in everything from vending machines to electric-vehicle chargers. Browser interfaces remain useful for enterprise dashboards, but are losing ground as mobile screens enlarge and 5G speeds make detailed analytics viable on handhelds.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

East China commands the largest regional slice of the China fintech market, anchored by Shanghai’s finance cluster and supported by dense venture-capital networks. Open banking pilots flourish here, and the Yangtze River Delta’s logistics backbone feeds supply-chain finance volumes that surpass any other district. Local regulators maintain sandboxes that reduce time-to-market for new robo-advisory modules, encouraging rapid iteration cycles.

North China, centered on Beijing, benefits from proximity to the PBOC and the State Council, giving platforms an early sight of regulatory drafts. The digital-yuan pilot seeded local acceptances that retail chains rapidly scaled. Corporate fintech firms exploit the concentration of headquarters in Zhongguancun’s tech park, offering CFO dashboards that marry cash-flow analytics with instant financing.

South China around Shenzhen blends hardware prowess with software agility. Tencent, Ping An, and WeBank all originate here, carrying the region’s innovation signature into payments, insurtech, and blockchain verification layers. Cross-border linkages to Hong Kong underpin Wealth Management Connect traffic, routing affluent investors into onshore ETFs and robo-advisory baskets powered by AI. The Greater Bay Area’s regulatory bridge accelerates testing of multi-currency wallets that later migrate inland, reinforcing the circular growth loop across the China fintech market.

Competitive Landscape

Industry structure resembles a barbell: super-platforms dominate payment rails while clusters of specialist firms fill product niches. Alipay and WeChat Pay hold a major share of the transaction volume, extracting network advantages that new entrants find hard to erode. In wealth management and SME lending, however, the field fragments; robo-advisors align with retail banks and wealth units of securities houses, diluting individual provider scale.

Regulatory resets after the Ant Group fine steered capital away from indiscriminate customer subsidies toward platform efficiency. China Merchants Bank’s “Yi Zhao” AI model signals a fresh phase of technology arms race among incumbents, focusing on personalized credit-risk modelling and cross-sell triggers. Meanwhile, Douyin Pay leverages social-commerce stickiness to chip at the duopoly, using video as a conversion gateway.

White spaces include climate-linked lending, where banks such as the Agricultural Bank of China channel preferential rates to green projects, and cross-border SME payments, where XTransfer acquires licences in Canada and Singapore. Cloud-service spend is rising fastest among joint-stock banks, translating into a surge in BaaS API calls that third parties consume to embed credit, FX, and compliance modules directly in merchant platforms across the China fintech market.

China Fintech Industry Leaders

-

Ant Group (Alipay)

-

Tencent Holdings (Tenpay)

-

WeBank Co. Ltd.

-

Lufax Holding Ltd.

-

JD Technology (JD Digits)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: ZhongAn Online P & C Insurance’s ZA Bank began cryptocurrency trading, broadening digital banking income streams.

- May 2025: Alipay and WeChat Pay saw foreign-user transaction volumes double during Labour Day holidays on the back of new tax-rebate rules.

- April 2025: CAC issued Q&A on cross-border data to allow group entities consolidated security-assessment filings valid for three years.

- January 2025: Hong Kong-Mainland Wealth Management Connect widened eligibility, boosting cross-border wealth flows

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines China's fintech market as the annual gross revenue generated by domestic providers of digitally delivered financial services across payments, lending, investment, insurance, and neobanking that rely on internet or mobile-first interfaces and are regulated by the People's Bank of China or other state financial watchdogs.

Scope exclusion: Pure technology outsourcing for overseas financial institutions is kept outside the study.

Segmentation Overview

- By Service Proposition

- Digital Payments

- Digital Lending and Financing

- Digital Investments

- Insurtech

- Neobanking

- By End-User

- Retail

- Businesses

- By User Interface

- Mobile Applications

- Web / Browser

- POS / IoT Devices

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured discussions with executives at domestic payment firms, digital lenders, regional banks, and policy advisers across Beijing, Shanghai, Shenzhen, and Chengdu. These interviews helped validate pricing spreads, user acquisition costs, and saturation levels that are not disclosed in public data, and they sharpened our assumptions around near-term regulatory pacing.

Desk Research

Our analysts began with authoritative statistical portals such as the People's Bank of China, China Banking and Insurance Regulatory Commission, China Internet Network Information Center, and the World Bank, which outline user bases, payment volumes, and financial inclusion ratios. Trade association white papers from the National Internet Finance Association and working papers from the Bank for International Settlements provided guardrails on regulatory shifts and CBDC pilots. Company filings, IPO prospectuses, and reputable news archives accessed through Dow Jones Factiva and D&B Hoovers enriched firm-level revenue splits and product rollouts. This list is illustrative; many additional open and licensed sources were scrutinized to cross-check figures and narrative signals.

Market-Sizing & Forecasting

The baseline revenue pool is first built top down from central bank payment fee data, outstanding digital credit balances, AUM held on robo platforms, and written premium flows in online insurance, which are then aligned with penetration rate benchmarks drawn from household surveys. Supplier roll-ups and sampled average service fees provide a selective bottom-up check before totals are frozen. Key variables tracked include smartphone penetration, e-CNY pilot coverage, small-business credit demand, AML compliance spend, and average merchant discount rates; each variable is projected with an ARIMA model that feeds our five-year multivariate forecast. Where bottom-up inputs are sparse, gaps are bridged through guided interpolation approved during peer review.

Data Validation & Update Cycle

Outputs run through variance checks against historic CAGR bands, counterpart indices, and preceding editions. Any variance above two standard deviations reopens analyst review, followed by supervisor sign-off. Reports refresh annually, and material policy moves trigger an interim update so clients receive the latest vetted view.

Why Our China Fintech Baseline Commands Reliability

Published numbers diverge because firms choose dissimilar revenue versus transaction metrics, include foreign outsourcing work, or apply unsupported uptake curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 51.28 B (2025) | Mordor Intelligence | - |

| USD 76.50 B (2024) | Regional Consultancy A | Bundles cloud outsourcing and overseas remittance hubs that our scope excludes |

| USD 4.59 T (2024) | Trade Journal B | Reports transaction value, not revenue, and assumes uniform 90% adoption without device cost checks |

Taken together, the comparison shows that Mordor's disciplined scope setting, mixed-method modeling, and annual refresh cadence offer investors and planners a stable, decision-ready baseline.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the China fintech market?

The market currently stands at USD 51.28 billion in 2025 and is on course to reach USD 107.55 billion by 2030, reflecting a 15.97% CAGR.

Which service segment is expanding the fastest within China’s fintech ecosystem?

Neobanking leads with a forecast 19.63% CAGR through 2030, powered by cloud-native platforms and Tencent-driven customer acquisition.

How is the digital yuan (e-CNY) reshaping fintech usage patterns?

E-CNY transaction value has significantly increased, enabling underbanked users in tier-2/3 cities to make cash-less payments even without smartphones.

What recent regulation most directly affects cross-border fintech operations?

The Network Data Security Management Regulations, effective January 2025, require domestic security reviews for outbound data transfers, though smaller volumes now qualify for exemptions.

Which region holds the highest concentration of fintech activity in China?

East China—especially the Yangtze River Delta anchored by Shanghai—leads owing to dense venture funding and open-banking sandboxes.

What primary challenge could temper near-term growth for fintech lenders?

Rising non-performing loan ratios in micro-lending are boosting capital-adequacy requirements, tightening credit supply in many tier-2/3 markets.

Page last updated on: