China Data Center Storage Market Size

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2030 |

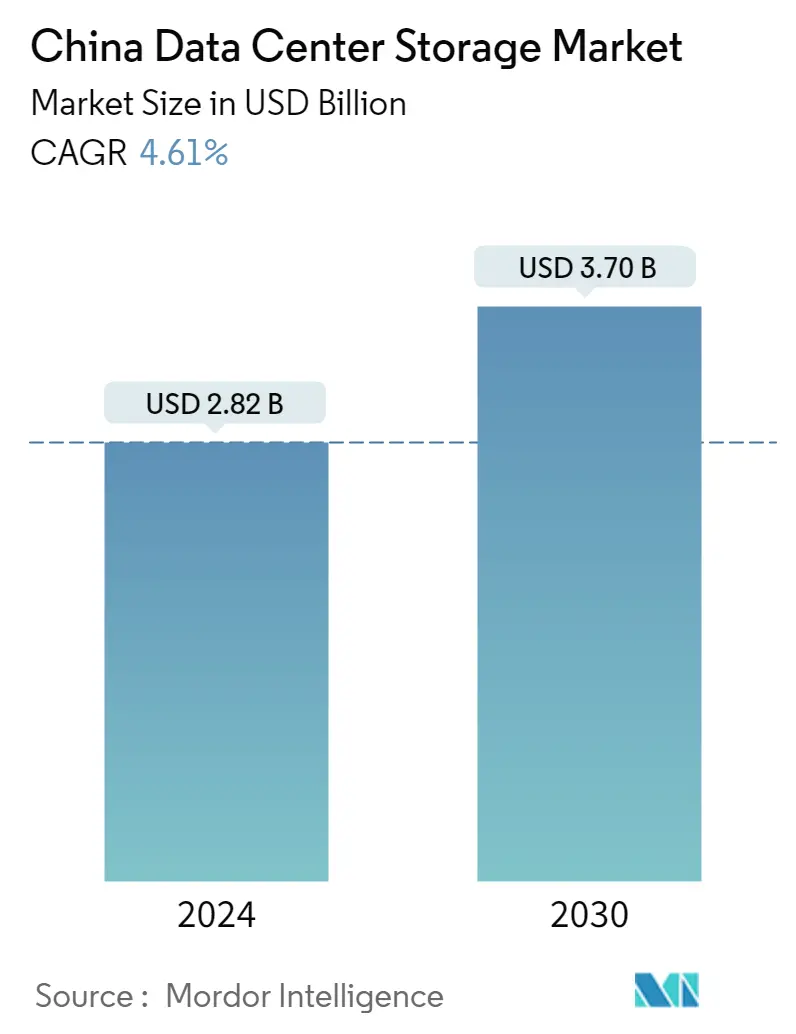

| Market Size (2024) | USD 2.82 Billion |

| Market Size (2030) | USD 3.70 Billion |

| CAGR (2024 - 2030) | 4.61 % |

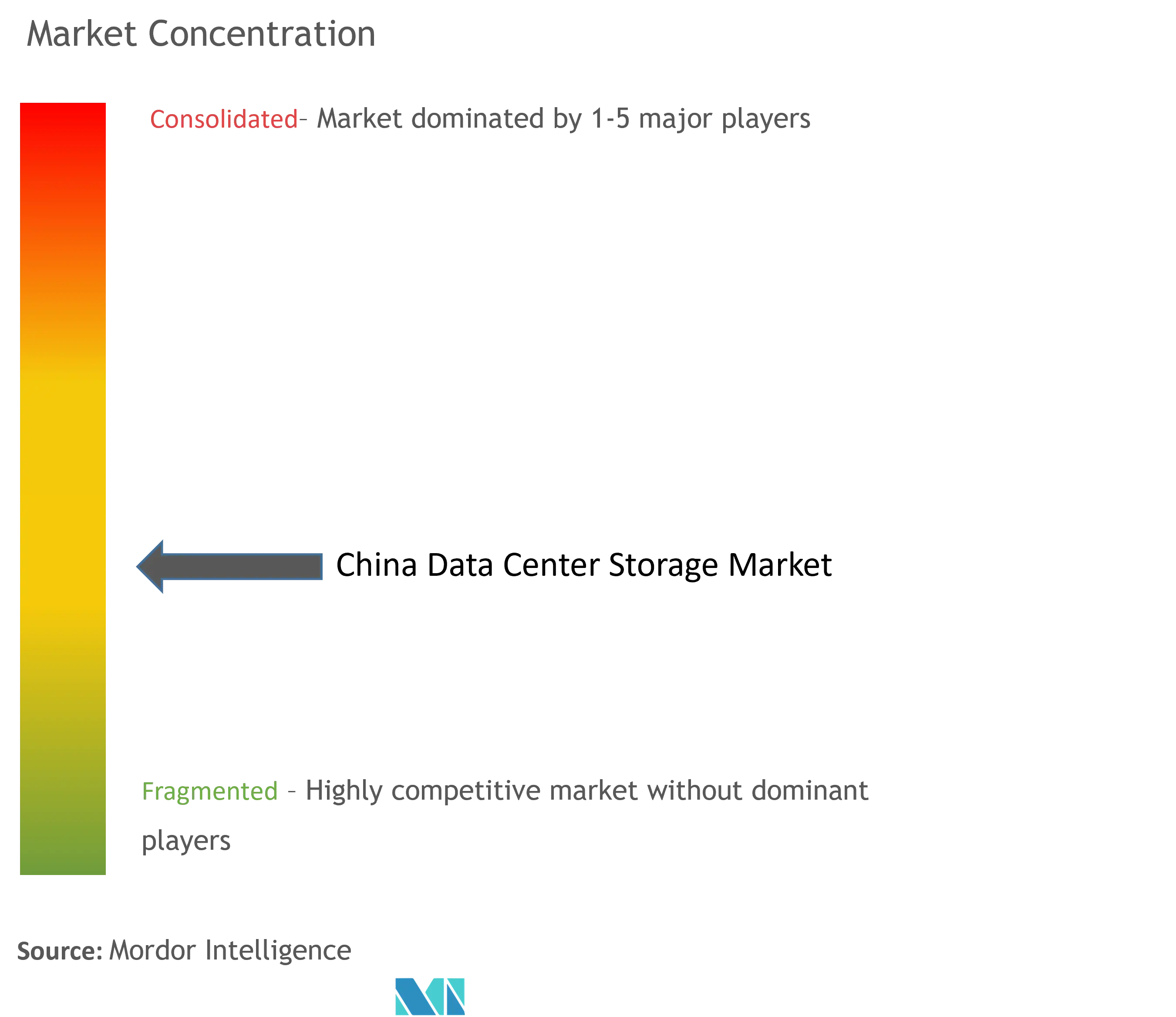

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

China Data Center Storage Market Analysis

The China Data Center Storage Market size is estimated at USD 2.82 billion in 2024, and is expected to reach USD 3.70 billion by 2030, growing at a CAGR of 4.61% during the forecast period (2024-2030).

The increasing demand for cloud computing among SMEs, government regulations for local data security, and the growing investment by domestic players are some of the major factors driving the demand for data centers in the country, leading to a growing need for data center storage equipment.

- The upcoming IT load capacity in the country is projected to cross 3,300 MW by 2029, boosting the demand for data center racks.

- The construction of raised floor areas for data centers in the country is expected to reach 11.9 million sq. ft by 2029 for under-construction raised floor space.

- The total number of racks to be installed in the country is expected to touch 600,000 units by 2029.

- Currently, four submarine cable projects are under construction in the country. One such submarine cable, estimated to start service in 2023, is Asia Direct Cable (ADC), stretching over 19,000 kilometers, with landing points in Chongming, Lantau Island, and Shantou for planned submarine cables.

China Data Center Storage Market Trends

IT & Telecommunication Segment to Hold Major Share in the Market

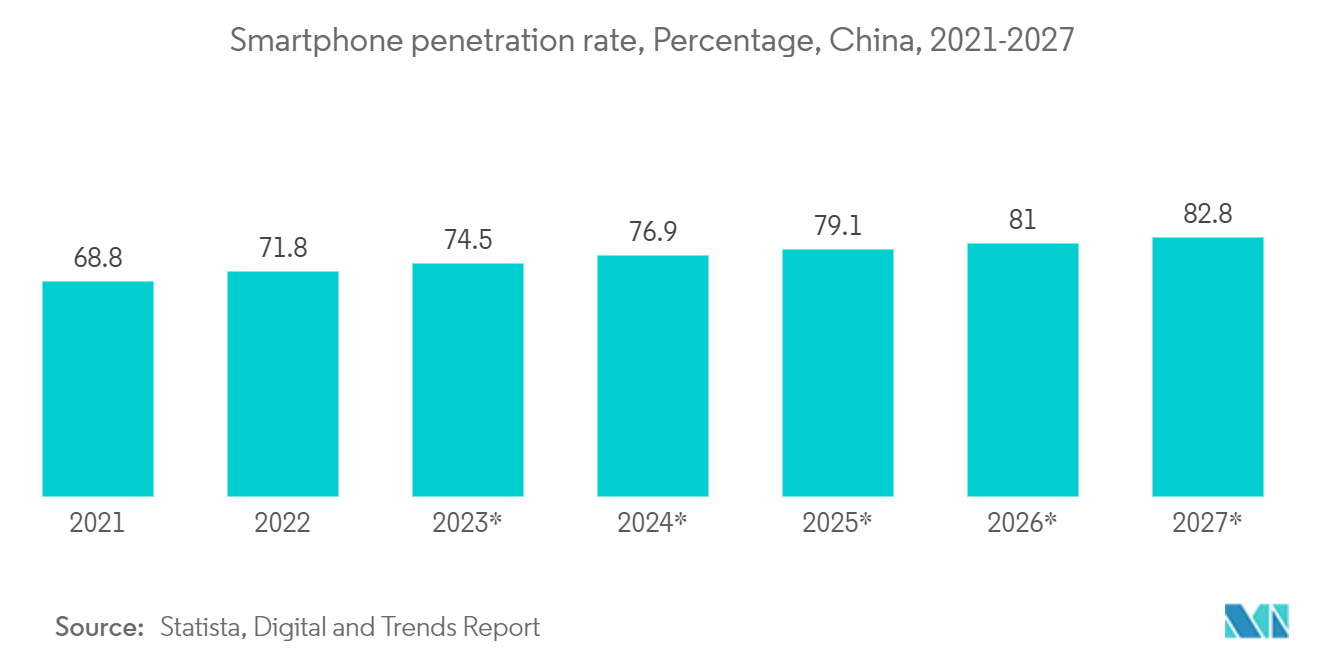

- Chinese smartphone companies are offering affordable smartphones with high-end features, leading to an increase in the number of smartphone users in the country. Around 50% of users replace their phones every 12-18 months, forcing companies to innovate their phones frequently. This increase in the number of smartphone users has positively impacted the growth of the data center market in the country. During the study period, when the number of smartphone users increased fivefold, the number of racks in data centers increased from around 70k in 2017 to 280k in 2021. This trend is expected to be witnessed during the forecast period as well. The increase in the number of data centers is directly related to the demand for storage devices in IT infrastructure. As the number of data centers increases, more storage devices are required to meet the growing computing needs.

- In 2022, internet use via smartphones in China was 99%, while via laptops and personal computers was 35% and 33%, making smartphones a primary mode of easy internet access. The weekly online screen-on time individually increased by 2.5 hours from 26 hours in 2020 to 28.5 hours in 2021. The growing demand for streaming services, online gaming, financial services, and social networking and the adoption of smart home automation applications have increased data consumption over the years. This data consumption positively impacts the increase in the number of data centers. As the number of data centers are increasing, more storage devices are required to meet the growing computing needs.

- Data centers are critical to national security, internet infrastructure, and economic performance. The country is experiencing rapid growth in its data center infrastructure, driven by a growing preference for the cloud and increased consumption and generation of data by increasing digital users. This increases the usage of data centers, and at the same time, increases the usage of storage devices in data centers, thus positively impacting the market.

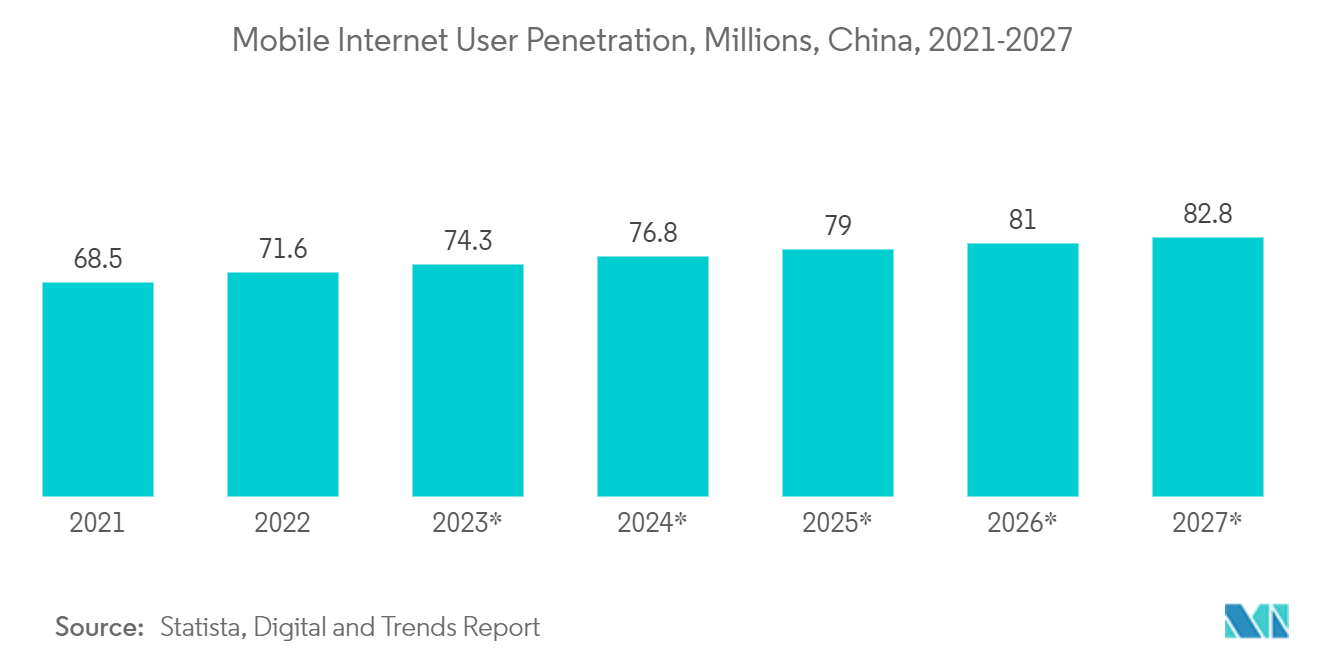

- Increased internet penetration, increased use of social networks, improved automation technology, smart city initiatives, and implementation of AI across industries are driving investment in data centers. As the number of data centers increases, so does the demand for data center storage in the country.

- In 2020, during the 14th Five-Year Plan Period, the Ministry of Industry and Information Technology announced a target of achieving 100% 5G availability in the urban regions and 80% in the rural regions by 2025. In 2022, China deployed 1.1 million 5G base stations, covering all cities, 97% of towns and 40% of villages, with a stable 5G network. It is expected to provide last-mile 5G connectivity in the country, boosting the growth of 5G during the forecast period. An increase in the penetration rate of the 5G network in the country is expected to lead to an increase in data generation, which may raise the need for more space for storing and processing these data. The need for more data processing and storing is expected to raise the occupancy rate in data centers in the coming years. As the number of data centers increases, more storage devices are required to meet the growing computing needs.

Hybrid Storage Expected To Hold Significant Share

- The combination of on-premises and cloud storage solutions is known as data center hybrid storage. This approach takes advantage of the best of both environments and provides the flexibility to store and manage data on-premises and in the cloud.

- Users opt for cloud services due to increased scalability, wherein they can increase the number of networks, storage, and servers based on the business requirement. For instance, during festivals such as China Singles Day, the attractive offers listed by the websites entice huge amounts of website traffic and financial transactions, which are easily managed, and the cloud infrastructure ensures performance. This increases the need for cloud services in the country. The increase in cloud functions, in combination with on-premise storage, enables efficient storage that helps to effectively utilize storage, reduce overall storage footprint, and optimize storage management. The growing demand for agile, cost-effective, and flexible computing is driving the demand for hybrid storage in the country.

- Initiatives such as the 14th Year Plan initiated by the Chinese government aim to promote digitalization services by encouraging research in 6G and integrated circuits and artificial intelligence in China. As part of digitalization, the adoption of technologies such as big data and IoT by SMEs has led to a significant increase in the procurement of all-flash and hybrid array systems.

- As businesses continue to grow, data centers are expanding and adapting to meet the growing connectivity needs of various industries and the increasing use of mobile internet. Businesses are increasingly relying on hybrid infrastructure and cloud capabilities as they seek flexibility, scalability, and remote work capabilities. The data traffic is also increasing the need for storage for businesses, thus boosting the market value for hybrid storage solutions.

- Several service providers are deploying advanced storage solutions to ensure data availability and access in hybrid clouds. The companies are offering optimized hybrid storage systems. For example, HPE GreenLake, an updated app and data product, also introduced platform upgrades and new cloud services in 2022. Therefore, this product portfolio is adopted by large enterprises with large data storage capacities. This demands hybrid storage capacitites in the country.

China Data Center Storage Industry Overview

The China Data Center Storage is moderately fragmented. The major players in this market hold the majority of the market share. Some significant players are Dell Inc., Hewlett Packard Enterprise, NetApp Inc., Hitachi Vantara LLC, and Huawei Technologies Co. Ltd. These companies leverage strategic collaborative initiatives to increase their market share and boost their profitability.

March 2022: Seagate and Phison expanded their SSD portfolio to assist data center customers in reducing the total cost of ownership. Both companies have entered a long-term partnership to reinforce the development cycle and distribution of enterprise-class SSDs.

September 2023: Pure Storage appointed Westcon-Comstor as its newest distributor in Australia. The partnership is an expansion of the existing agreements between the two companies in New Zealand, Singapore, Indonesia, Malaysia, China, Hong Kong, and the Philippines. The partnership accelerates the adoption of FlashStack – a software-defined hybrid cloud infrastructure from Pure and Cisco that integrates computing, networking, and storage.

China Data Center Storage Market Leaders

-

Dell Inc.

-

Hewlett Packard Enterprise

-

NetApp Inc.

-

Huawei Technologies Co. Ltd.

-

Hitachi Vantara LLC

*Disclaimer: Major Players sorted in no particular order

China Data Center Storage Market News

June 2023: Pure Storage Inc. delivered data storage technology and services, i.e., All-Flash Solutions for Every Storage. Pure Storage’s portfolio spans includes the expansion of Pure Storage’s disk replacement-focused Pure/E family of products, with the all-new FlashArray//E, Flasharray//X, and Flash array//C.

June 2023: Huawei launched the innovative data center and data infrastructure architecture F2F2X (Flash-to-Flash-to-Anything) at the Financial Data Storage Session, a part of the Huawei Intelligent Finance Summit 2023.

China Data Center Storage Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumption & Market Definition

1.2 Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Dynamics

4.1 Market Overview

4.2 Market Drivers

4.2.1 Expansion of IT Infrastructure to Increase Market Growth

4.2.2 Increased Investments in Hyperscale Data Centers To Increase Market Growth

4.3 Market Restraints

4.3.1 High Initial Investment Cost To Hinder Market Growth

4.4 Value Chain / Supply Chain Analysis

4.5 Industry Attractiveness - Porter's Five Forces Analysis

4.5.1 Threat of New Entrants

4.5.2 Bargaining Power of Buyers/Consumers

4.5.3 Bargaining Power of Suppliers

4.5.4 Threat of Substitute Products

4.5.5 Intensity of Competitive Rivalry

4.6 Assessment of COVID-19 Impact

5. MARKET SEGMENTATION

5.1 Storage Technology

5.1.1 Network Attached Storage (NAS)

5.1.2 Storage Area Network (SAN)

5.1.3 Direct Attached Storage (DAS)

5.1.4 Other Technologies

5.2 Storage Type

5.2.1 Traditional Storage

5.2.2 All-Flash Storage

5.2.3 Hybrid Storage

5.3 End User

5.3.1 IT & Telecommunication

5.3.2 BFSI

5.3.3 Government

5.3.4 Media & Entertainment

5.3.5 Other End Users

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Dell Inc.

6.1.2 Hewlett Packard Enterprise

6.1.3 NetApp Inc.

6.1.4 Huawei Technologies Co. Ltd

6.1.5 Hitachi Vantara LLC

6.1.6 Kingston Technology Company Inc.

6.1.7 Lenovo Group Limited

6.1.8 Fujitsu Limited

6.1.9 Oracle Corporation

6.1.10 Seagate Technology LLC

- *List Not Exhaustive

7. INVESTMENT ANALYSIS

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

China Data Center Storage Industry Segmentation

Data center storage refers to the devices, hardware, networking equipment, and software technologies that enable the storage of data and applications within data center facilities. It is used to store, manage, retrieve, distribute, and back up digital information within data center facilities.

The China Data Center Storage Market is Segmented by Storage Technology (Network Attached Storage (NAS), Storage Area Network (SAN), Direct Attached Storage (DAS)), by Storage Type (Traditional Storage, All-Flash Storage, Hybrid Storage), by End User (IT & Telecommunication, BFSI, Government, Media & Entertainment, and Other End User). The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

| Storage Technology | |

| Network Attached Storage (NAS) | |

| Storage Area Network (SAN) | |

| Direct Attached Storage (DAS) | |

| Other Technologies |

| Storage Type | |

| Traditional Storage | |

| All-Flash Storage | |

| Hybrid Storage |

| End User | |

| IT & Telecommunication | |

| BFSI | |

| Government | |

| Media & Entertainment | |

| Other End Users |

China Data Center Storage Market Research Faqs

How big is the China Data Center Storage Market?

The China Data Center Storage Market size is expected to reach USD 2.82 billion in 2024 and grow at a CAGR of 4.61% to reach USD 3.70 billion by 2030.

What is the current China Data Center Storage Market size?

In 2024, the China Data Center Storage Market size is expected to reach USD 2.82 billion.

Who are the key players in China Data Center Storage Market?

Dell Inc., Hewlett Packard Enterprise, NetApp Inc., Huawei Technologies Co. Ltd. and Hitachi Vantara LLC are the major companies operating in the China Data Center Storage Market.

What years does this China Data Center Storage Market cover, and what was the market size in 2023?

In 2023, the China Data Center Storage Market size was estimated at USD 2.70 billion. The report covers the China Data Center Storage Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the China Data Center Storage Market size for years: 2024, 2025, 2026, 2027, 2028, 2029 and 2030.

China Data Center Storage Industry Report

Statistics for the 2024 China Data Center Storage market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. China Data Center Storage analysis includes a market forecast outlook to for 2024 to 2030 and historical overview. Get a sample of this industry analysis as a free report PDF download.

China Data Center Storage Market Report Snapshots