Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 5.41 Billion |

| Market Size (2030) | USD 6.95 Billion |

| Growth Rate (2025 - 2030) | 5.13% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Crop Protection Chemicals Market Analysis by Mordor Intelligence

The China Crop Protection Chemicals Market size is estimated at 5.41 billion USD in 2025, and is expected to reach 6.95 billion USD by 2030, growing at a CAGR of 5.13% during the forecast period (2025-2030).

China has established itself as a global powerhouse in the agrochemical industry, serving as a primary producer of active ingredients that form the foundation for formulated crop protection chemicals worldwide. The country's agricultural sector faces significant challenges, with approximately 35.8 million hectares of crop fields heavily infested with weeds, resulting in substantial annual yield reductions ranging from 12.3% to 16.5%. This situation has catalyzed the development of a robust domestic manufacturing base for crop protection chemicals, with the country maintaining its position as one of the world's largest producers and exporters of these essential agricultural inputs.

The modernization of Chinese agriculture is driving significant changes in crop protection practices, particularly in application technologies and precision farming methods. The adoption of advanced application methods is evident in the dominance of foliar application, which accounted for 60.1% of the fungicide market in 2022. This trend reflects the agricultural sector's shift toward more efficient and targeted pest control methods, supported by the increasing integration of digital technologies and smart farming practices that enable precise application of crop protection chemicals.

The expansion of agricultural land under high-value crops is creating new opportunities and challenges for crop protection. The area under fruits and vegetables is projected to increase from 50.8 million hectares in 2022 to 58.9 million hectares by the end of the forecast period, while cotton cultivation is expected to expand from 8.4 million hectares to 9.4 million hectares. This expansion is accompanied by evolving pest pressures, with over 200 species of weeds infesting main crop fields, among which approximately 30 species are identified as major threats requiring sophisticated control measures, including integrated pest management strategies.

The Chinese crop protection industry is undergoing a significant transformation driven by sustainability initiatives and regulatory reforms. The Ministry of Agriculture and Rural Affairs (MARA) has implemented comprehensive guidelines for pesticide registration, labeling, and maximum residue limits, while emphasizing environmental protection and sustainable agricultural practices. This regulatory framework is complemented by industry efforts to develop more environmentally friendly formulations and application methods, as evidenced by the growing focus on integrated pest management approaches and the development of targeted, reduced-risk crop protection solutions.

China Crop Protection Chemicals Market Trends and Insights

IPM strategies and other pesticide reduction policies contributed to reduction in per hectare pesticides consumption

- Over the past few years, there has been a notable reduction in pesticide consumption per hectare in the country. During the historical period, there was a significant decline in pesticide usage to approximately 300 grams per hectare. In 2017, the consumption stood at 1,700 grams per hectare; however, by 2022, it had dropped to 1,400 grams per hectare.

- The considerable reduction in pesticide utilization per hectare can be largely attributed to the country's implementation of a stringent policy of zero growth in pesticide consumption.

- China has proactively promoted the adoption of Integrated Pest Management (IPM) strategies, encompassing a range of preventive measures, alternative techniques, and careful pesticide applications. As a result of this holistic approach, there has been a notable reduction in pesticide usage rates.

- China witnessed a significant decline in herbicide usage by 88.78 grams, primarily driven by the adoption of practices such as crop rotation by farmers. Crop rotation involves alternating different crops with varying growth patterns and nutritional requirements, effectively breaking the lifecycle of weeds. By implementing this practice, Chinese farmers have successfully disrupted weed growth cycles, resulting in reduced weed populations and a decreased reliance on herbicides.

- The other substantial decrease in pesticide usage per hectare was observed specifically in the category of insecticides, with a reduction of 58.31 grams from 2017 to 2022. This decline can be primarily attributed to government policies aimed at banning harmful insecticides and the adoption of transgenic crops.

- Other factors like setting limits on the maximum residue levels on the usage of pesticides reduced the per hectare consumption in the country.

Understand The Key Trends Shaping This Market

Download PDF

The active ingredients' prices are majorly influenced by factors like weather conditions, pest outbreaks, energy prices, and labor costs in the country

- China is one of the major producers of active ingredients that form the base of formulated crop protection chemicals. Insecticides constitute the major share of pesticide production.

- Cypermethrin is the most widely used pyrethroid pesticide to control many pests, such as fruit flies, borers, and mealy bugs in vegetables and fruits in China. It was valued at USD 20.9 thousand per metric ton in 2022.

- Atrazine is a herbicide widely used to control various broadleaved weeds and grasses. China consumes more than 16,000 ton (97% technical) of atrazine annually. Atrazine is mainly used to control annual weeds in corn or sugarcane fields. China is one of the major suppliers of atrazine worldwide. It was priced at USD 13.7 thousand per metric ton in 2022.

- Mancozeb is a broad-spectrum contact fungicide used to control a number of fungal diseases, such as anthracnose, Pythium blight, leaf spot, downy mildew, Botrytis, rust, and scab in oilseed rape, lettuce, wheat, apples, tomatoes, table grapes, wine grapes, bulb onions, carrot, parsnip, shallot, and durum wheat. It was priced at USD 7.7 thousand per metric ton in 2022.

- Glyphosate is an organophosphorus broad-spectrum systemic herbicide and crop desiccant, priced at USD 1.1 thousand per metric ton in 2022. Glyphosate is mainly used to control weeds like grasses, sedges, and broadleaves. China is the largest producer and exporter of glyphosate in the world. In 2017, China exported over 300,000 ton of glyphosate technical, which met more than half of the global glyphosate demand.

- Factors like weather conditions, pest outbreaks, energy prices, and labor costs in the country majorly influence the prices of active ingredients.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: Function

Herbicide Segment in China Crop Protection Chemicals Market

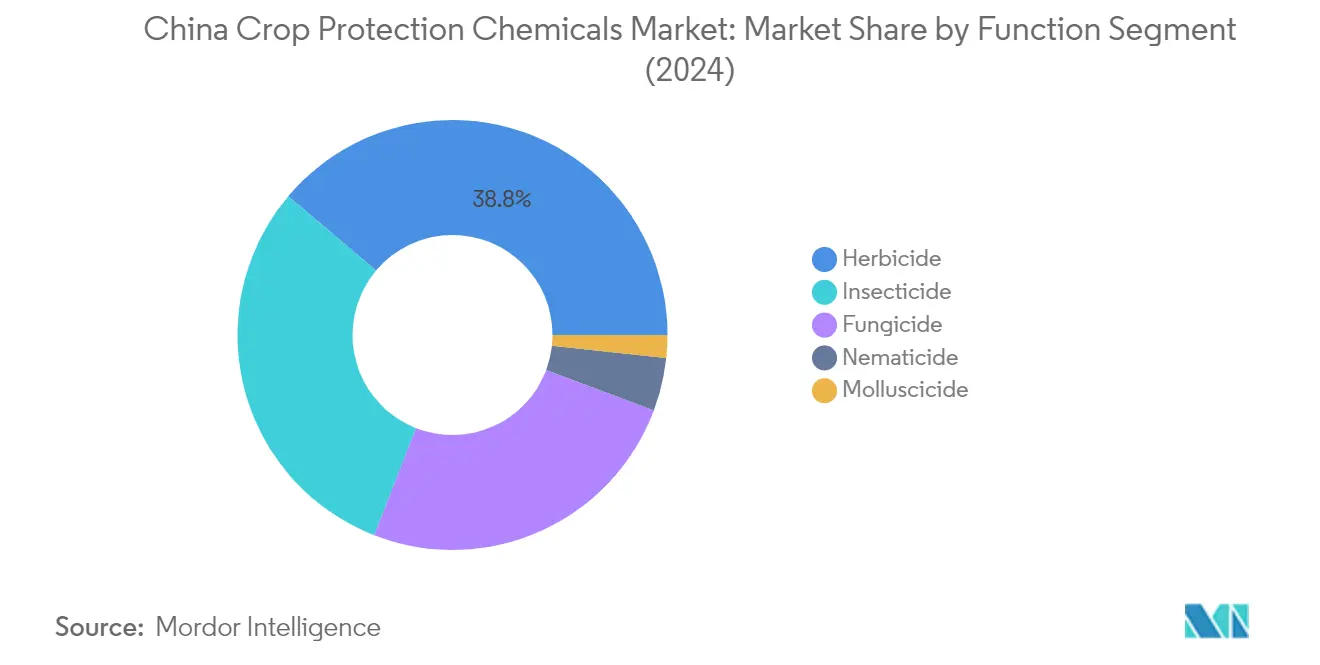

The herbicide segment dominates the China crop protection chemicals market, accounting for approximately 39% of the total market value in 2024. This significant market share is primarily driven by the extensive cultivation of major crops like rice, wheat, and corn, where weed management is crucial for maintaining crop yields. More than 200 species of weeds infest main crop fields in China, with approximately 30 species identified as major threats causing substantial crop yield losses. About 35.8 million hectares of crop fields are heavily infested with weeds, leading to annual yield reductions of 12-16%. The segment is experiencing robust growth and is projected to grow at around 6% during 2024-2029, driven by factors such as the increasing adoption of herbicide-tolerant crops, rising labor costs that make manual weeding less economical, and the continuous development of new herbicide formulations to combat evolving weed resistance.

Remaining Segments in Function Segmentation

The insecticide segment represents the second-largest category in the market, playing a crucial role in protecting crops from various pest infestations, particularly in regions experiencing increased pest pressure due to climate change. The fungicide segment maintains its significance in the market by providing essential protection against various fungal diseases that affect major crops, especially during humid conditions common in many agricultural regions of China. The nematicide and molluscicide segments, while smaller in market share, serve specific but critical purposes in crop protection, particularly in high-value crops and areas where these pest problems are prevalent. These segments continue to evolve with the introduction of new active ingredients and formulations that offer improved efficacy and environmental sustainability.

Segment Analysis: Application Mode

Foliar Segment in China Crop Protection Chemicals Market

The foliar application segment maintains its dominant position in China's crop protection chemicals market, commanding approximately 46% market share in 2024. This substantial market presence can be attributed to the segment's widespread adoption across various crop types, particularly in high-value crops and cash crops. Farmers increasingly recognize the advantages of foliar spraying, such as rapid absorption and quick action against pests and diseases. The method's popularity is further enhanced by its ability to provide targeted protection and its effectiveness in addressing immediate pest and disease pressures. The expanding cultivation of fruits, vegetables, and other specialty crops has significantly contributed to the segment's growth, as these crops often require precise and timely application of crop protection products. Additionally, the method's flexibility in application timing and its compatibility with various pesticide formulations have made it the preferred choice among Chinese farmers.

Soil Treatment Segment in China Crop Protection Chemicals Market

The soil treatment segment is emerging as the fastest-growing application method in China's crop protection chemicals market, projected to grow at approximately 6% CAGR during 2024-2029. This growth trajectory is primarily driven by increasing government initiatives focused on sustainable agriculture and soil management practices. The expansion of commercial farming, greenhouse cultivation, and precision agriculture in China has significantly boosted the demand for soil treatment methods. The segment's growth is further supported by its effectiveness in controlling soil-borne pests and diseases, promoting crop growth, and enhancing overall yield. Recent technological advancements in soil treatment products and application methods have improved the efficiency and effectiveness of these treatments, making them more attractive to farmers. The Ministry of Ecology and Environment's implementation of comprehensive soil protection policies and environmental governance measures in agriculture has also contributed to the segment's rapid growth.

Remaining Segments in Application Mode

The other application modes in China's crop protection chemicals market include chemigation, fumigation, and seed treatment, each serving specific agricultural needs. Chemigation has gained traction due to its integration with modern irrigation systems, offering efficient pesticide distribution while conserving water resources. Fumigation, though representing a smaller share, remains crucial for specific high-value crops and controlled environment agriculture. Seed treatment continues to be an important preventive measure, providing early-stage crop protection and establishing a strong foundation for plant growth. These application methods complement each other, offering farmers a comprehensive range of options for agricultural pest control based on their specific requirements, crop types, and local conditions.

Segment Analysis: Crop Type

Grains & Cereals Segment in China Crop Protection Chemicals Market

The Grains & Cereals segment dominates the Chinese crop protection chemicals market, commanding approximately 52% of the total market value in 2024. This significant market share is primarily attributed to the segment's extensive cultivation area, which accounts for about 63% of the total crop area in China. Rice, maize, and wheat represent 99% of the total Chinese cereal production, making them the most important crops in this segment. The dominance of this segment is further reinforced by the prevalence of various fungal diseases such as rust, powdery mildew, and leaf spot that affect cereal crops, along with major pest challenges including stem borers, aphids, armyworms, leafhoppers, and plant hoppers. The segment's substantial market share is also supported by China's strategic focus on grain security and self-sufficiency in cereal production.

Fruits & Vegetables Segment in China Crop Protection Chemicals Market

The Fruits & Vegetables segment is projected to exhibit the strongest growth trajectory in the Chinese crop protection chemicals market, with an anticipated CAGR of approximately 6% during 2024-2029. This robust growth is driven by several factors, including the expanding cultivation areas in key regions such as the Northern China Plain, Yangtze River Delta, Pearl River Delta, Yunnan Province, Xinjiang Province, and Hainan Province. The segment's growth is further fueled by the increasing need to protect high-value crops from various pests and diseases, particularly in intensive farming systems. The rising domestic demand for quality fruits and vegetables, coupled with the growing export opportunities, is compelling farmers to adopt advanced crop protection products to ensure better yields and product quality.

Remaining Segments in Crop Type

The other significant segments in the Chinese crop protection chemicals market include Commercial Crops, Pulses & Oilseeds, and Turf & Ornamental. The Commercial Crops segment, encompassing cotton, tea, tobacco, and sugarcane, plays a crucial role in China's agricultural exports and industrial raw material supply. The Pulses & Oilseeds segment, which includes important crops like soybean, groundnut, rapeseed, lentils, and mung beans, is vital for food security and vegetable oil production. The Turf & Ornamental segment, though smaller in comparison, serves specialized markets including golf courses, public spaces, and ornamental plant production, contributing to urban greenery and recreational facilities. The introduction of biopesticides in these segments is enhancing sustainability and reducing environmental impact.

Competitive Landscape

Top Companies in China Crop Protection Chemicals Market

The Chinese crop protection market features a mix of global agrochemical leaders and domestic players competing for market share. Companies are heavily focused on product innovation, particularly in developing new active ingredients and formulations tailored to specific crops and pest challenges. Operational agility is demonstrated through strategic partnerships and collaborations to enhance manufacturing capabilities and distribution networks. Market players are investing significantly in research and development to create sustainable and environmentally friendly solutions while expanding their product portfolios through strategic acquisitions. Companies are also strengthening their presence by establishing local manufacturing facilities, research centers, and expanding their distribution networks across different agricultural regions in China.

Moderate Consolidation with Strong Local Presence

The Chinese crop protection industry exhibits moderate consolidation with a blend of multinational corporations and domestic manufacturers. Global players like Bayer AG, BASF SE, and Syngenta Group leverage their advanced research capabilities and extensive product portfolios, while domestic companies such as Jiangsu Yangnong Chemical Co. Ltd and Wynca Group maintain strong local market positions through their understanding of regional farming practices and established distribution networks. The market structure is characterized by the presence of both diversified agricultural conglomerates offering comprehensive farming solutions and specialized agricultural chemicals manufacturers focusing on specific product segments.

The market has witnessed significant merger and acquisition activities as companies seek to strengthen their market positions and expand their technological capabilities. Global players are increasingly partnering with local companies to enhance their market reach and manufacturing capabilities in China. These strategic alliances help companies combine their technological expertise with local market knowledge, creating more effective and locally adapted crop protection solutions. The trend towards consolidation is driven by the need to achieve economies of scale, expand product portfolios, and strengthen research and development capabilities.

Innovation and Sustainability Drive Future Growth

Success in the Chinese crop protection market increasingly depends on companies' ability to develop innovative, sustainable solutions while maintaining strong distribution networks. Incumbent players must focus on developing environmentally friendly formulations, investing in digital farming technologies, and strengthening their research and development capabilities. Building strong relationships with local agricultural communities, offering comprehensive crop protection solutions, and maintaining cost competitiveness through efficient manufacturing processes are crucial strategies for maintaining market leadership. Companies must also adapt to evolving regulatory requirements and changing farmer preferences while maintaining product quality and safety standards.

For contenders looking to gain market share, focusing on niche market segments and developing specialized solutions for specific crop protection challenges presents significant opportunities. Building strategic partnerships with local distributors, investing in regional research and development facilities, and offering competitive pricing strategies are essential for market expansion. Companies must also consider the increasing emphasis on sustainable agriculture and organic farming practices while developing their product portfolios. Success in this market requires a balanced approach between innovation, sustainability, and cost-effectiveness, while maintaining strong relationships with key stakeholders in the agricultural sector.

China Crop Protection Chemicals Industry Leaders

BASF SE

Bayer AG

FMC Corporation

Jiangsu Yangnong Chemical Co. Ltd

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

- August 2022: BASF and Corteva Agriscience collaborated to provide soybean farmers with the weed control of the future. By working together, BASF and Corteva aim to satisfy farmers' demand for specialized weed control solutions that are distinct from those that are currently available or being developed.

- May 2022: UPL partnered with Bayer for Spirotetramat insecticide to develop new pest management solutions. Through this long-term global data access and supply agreement with Bayer, specifically for addressing farmer demands regarding resistance management and difficult-to-control sucking pests, UPL will develop, register, and distribute new unique solutions, including Spirotetramat, using its experience in insecticides and worldwide research and development network.

China Crop Protection Chemicals Market Report Scope

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.Function

| Fungicide |

| Herbicide |

| Insecticide |

| Molluscicide |

| Nematicide |

Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Need A Different Region or Segment?

Customize Now

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF