| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 89.86 Million |

| Market Size (2030) | USD 126.9 Million |

| CAGR (2025 - 2030) | 7.15 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

China Controlled Release Fertilizer Market Analysis

The China Controlled Release Fertilizer Market size is estimated at 89.86 million USD in 2025, and is expected to reach 126.9 million USD by 2030, growing at a CAGR of 7.15% during the forecast period (2025-2030).

China's agricultural sector is undergoing significant transformation with controlled release fertilizers (CRFs) emerging as a crucial component of modern farming practices. As of 2022, CRFs represented just 0.6% of China's specialty fertilizer market, indicating substantial room for growth and adoption. The country's position as the world's largest agricultural producer, contributing 16.7% of global crop production with 6.2 million metric tonnes, underscores the immense potential for CRF adoption. The agricultural sector's focus on sustainable practices and efficient nutrient management has led to increased interest in advanced fertilizer technologies, particularly in regions with intensive farming practices.

Technological innovations in coating materials and manufacturing processes are reshaping the CRF landscape. Polymer-coated fertilizers have emerged as the dominant technology, commanding a 75.9% market share in 2022, primarily due to their superior nutrient release control and environmental benefits. The industry is witnessing a notable shift towards bio-based coating materials, including polyurethane, epoxy resin, and polyolefin wax composites, which offer enhanced biodegradability and reduced environmental impact. Manufacturers are increasingly investing in research and development to improve coating technologies and develop more efficient nutrient delivery systems, contributing to the growth of enhanced efficiency fertilizer solutions.

The application patterns of CRFs across different crop segments reveal evolving market dynamics. In the field crops sector, which includes major staples like rice, corn, and wheat, the demand for nitrogen-efficient fertilizers is particularly strong, with nitrogenous fertilizers accounting for 59.7% of the polymer-sulfur-coated segment in 2022. The horticultural sector, which produced 602 million tonnes of vegetables in 2021, is showing increased adoption of specialized CRF formulations designed for high-value crops. Cotton cultivation, with production reaching 6.4 million metric tons in 2022, has become a significant consumer of slow release fertilizers due to the crop's specific nutrient requirements.

The industry's supply chain and manufacturing capabilities are expanding to meet growing demand. Alternative coating technologies, categorized under the "others" segment, represented 5.4% of the market in 2022, indicating diversification in manufacturing approaches. Local manufacturers are strengthening their production capabilities while international players are establishing strategic partnerships to enhance market presence. The industry is witnessing increased investment in automated production facilities and quality control systems to ensure consistent product performance and meet stringent environmental regulations. The focus on sustainable fertilizer practices is driving the adoption of environmentally friendly fertilizers, which align with global sustainability goals.

China Controlled Release Fertilizer Market Trends

The expansion of the cultivation area is driven by increasing demand for food and the country's goal to achieve self-sufficiency in staple food

- The cultivation area of field crops in China increased from 130.5 million ha in 2017 to 127.8 million ha in 2021, accounting for 71.4% of the total area under cultivation. Among field crops, corn occupied the maximum share of 34.2%, followed by rice and wheat, accounting for 23.6% and 18.3%, respectively. The rising area under cultivation is expected to increase the need for fertilizer usage in the country.

- The country usually grows field crops in two seasons: summer/spring (April-September) and winter. Spring crops mainly include early corn, early rice, early wheat, and cotton. Winter crops include winter wheat and rapeseed. However, rice and corn are the most important crops grown in China, accounting for one-third of the grain production in China. It is the world's largest rice producer and utilized 30 million hectares of land for rice farming in 2022, producing a harvest of 210 million tonnes. The major rice-producing regions in China include Heilongjiang, Hunan, Jiangxi, Hubei, Jiangsu, Sichuan, Guangxi, Guangdong, and Yunnan. Corn production in China for 2022-23 was expected to reach 277.2 million tonnes, which was 4.6 million tonnes higher than last year due to a better harvest. The major corn-growing regions are in the Northeast provinces of Heilongjiang, Jilin, and Inner Mongolia.

- Although spring is the main cropping season in the country, it is slightly affected by high heat in June and July. For instance, rice is the staple food for millions in China. High temperatures and low precipitation increase the loss of minerals in the soil, leading to the need for a higher application of fertilizers to the soil. These dry weather conditions may also limit the yield of the crops.

Understand The Key Trends Shaping This Market

Download PDF

About 28% of nitrous oxide emissions from cropland in the world are from Chinese agricultural lands

- Primary nutrients enhance biochemical processes such as enzyme activity in plants and promote plant cell growth. Deficiencies in primary nutrients can affect plant health, development, and crop production output. The average application rate of nitrogen, potassium, and phosphorus combined in field crops was 159.9 kg/hectare in 2022. The average primary nutrient application in field crops accounted for 65.23% nitrogen, 28.07% phosphorous, and 6.68% potassium.

- Nitrogen ranks first among primary nutrients, as it is essential for plant metabolism and is a component of chlorophyll and amino acids. Nitrogen had an average application rate of 279.65 kg/hectare. Potash followed with 105.3 kg/hectare and phosphorous with 94.9 kg/hectare in 2022. The contamination of surface and groundwater with nitrogen and phosphorus has been considered a result of inadequate advice given to farmers regarding fertilizer application rates. About 28% of nitrous oxide emissions from cropland in the world are from China's agricultural lands.

- In 2022, crops with the highest average nutrient application rates were cotton (255.41 kg/hectare), wheat (232.25 kg/hectare), corn (198.44 kg/hectare), and rice (157.76 kg/hectare). In 2022, cotton production accounted for 6.4 million metric tons, making China the world's largest producer, consumer, and importer of cotton. Around 20% of the cotton consumed worldwide is produced in China, and 84% of that production comes from Xinjiang.

- To meet the demands of a growing population, boosting crop production is essential; as a result, the application of primary nutrients in field crops is expected to grow between 2023 and 2030.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- The growing interest in fruits and vegetable cultivation due to better market opportunities

- Cabbage is a heavy feeder, and it quickly depletes the soil of nutrients

Segment Analysis: Coating Type

Polymer Coated Segment in China CRF Market

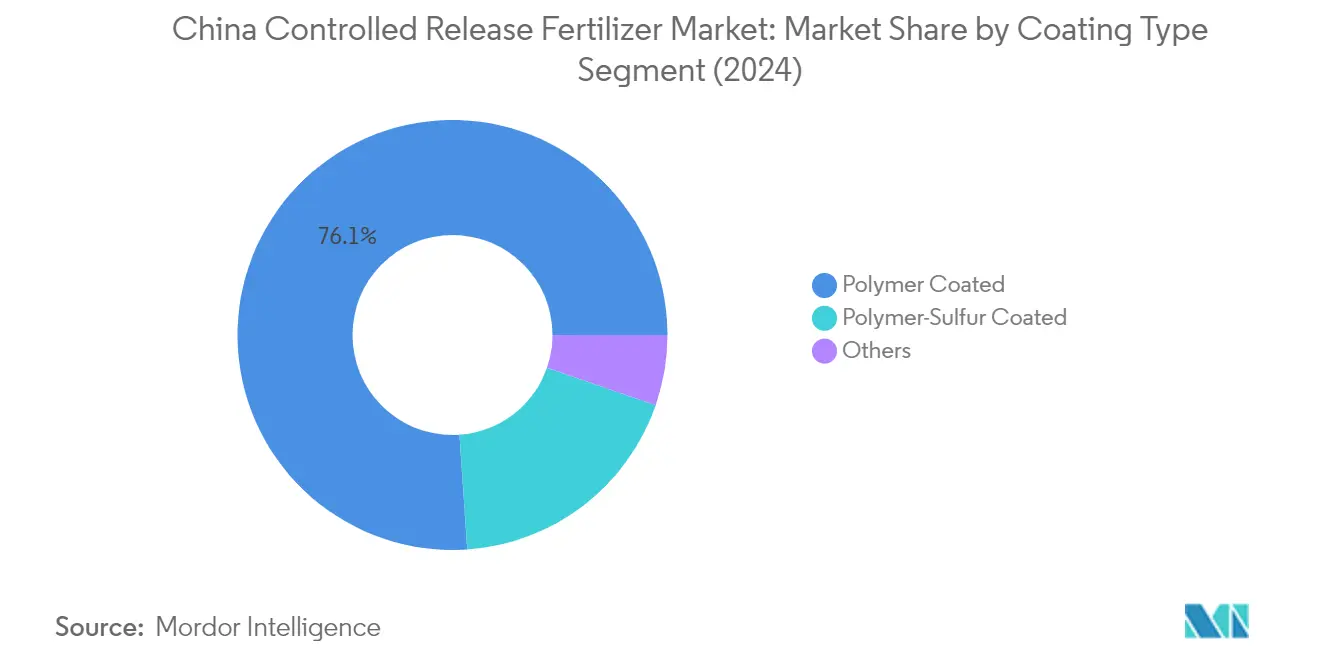

The polymer coated fertilizer segment dominates the Chinese controlled release fertilizer market, commanding approximately 76% market share in 2024. This segment's prominence stems from its superior ability to regulate nutrient release through tailored coating characteristics, thickness, and material ratios aligned with specific crop needs. Within this category, polymer coated fertilizer urea has emerged as the leading variant, particularly valued for its nitrogen efficiency and potential to reduce nitrogenous fertilizer usage by 30-40%. The segment's strong market position is further reinforced by its projected growth trajectory of around 7% CAGR through 2029, driven by increasing adoption in horticultural and ornamental crops, where precise nutrient release requirements and environmental considerations are paramount. The segment's success is also attributed to continuous innovations in coating technologies and materials, enabling manufacturers to offer products that effectively balance optimal yields with environmental preservation.

Polymer-Sulfur Coated Segment in China CRF Market

The sulfur coated fertilizer segment has established itself as a significant player in the Chinese controlled release fertilizer market, particularly valued for its dual benefits of controlled nutrient release and sulfur supplementation. This segment's growth is driven by its proven effectiveness in enhancing crop quality and resilience through the symbiotic relationship between sulfur and nitrogen, which notably boosts crop nitrate levels and overall crop quality. Within the nitrogenous sulfur coated fertilizer category, sulfur-coated urea has emerged as the preferred choice due to its ability to minimize nutrient losses through leaching, thereby reducing environmental impact and nitrogen contamination in subsurface water. The segment's expansion is further supported by ongoing technological advancements in coating processes and materials, though manufacturers continue to address challenges related to optimal sulfur application during the granule coating process to ensure efficient nutrient release.

Remaining Segments in Coating Type

The other coated fertilizer types segment encompasses various innovative solutions including resins, waterborne polyacrylate, biodegradable polymers, asphalt-based coatings, liquified wheat straw, polyurethane, epoxy resin, and polyolefin wax composites. This diverse category is particularly significant in the turf and ornamental sector, where specific nutrient release requirements and environmental considerations drive demand for specialized coating solutions. The segment is characterized by continuous innovation in bio-based coating materials, reflecting the industry's response to increasing environmental concerns and regulatory requirements. These alternative coating technologies offer unique advantages in terms of biodegradability, cost-effectiveness, and specialized application requirements, contributing to the overall diversification of the controlled release fertilizer market.

Segment Analysis: Crop Type

Field Crops Segment in China Controlled Release Fertilizer Market

Field crops represent the dominant segment in China's controlled release fertilizer market, commanding approximately 69% of the total market value in 2024. This substantial market share is primarily driven by the extensive cultivation area dedicated to field crops like corn, rice, and wheat across China. The segment's dominance is reinforced by the increasing adoption of encapsulated fertilizer in major grain-producing regions, particularly in provinces like Heilongjiang, Hunan, and Jiangxi. The use of timed release fertilizer in field crops has demonstrated significant benefits, including the potential to reduce overall fertilizer consumption by 20-30% while maintaining optimal yields. A single application of smart release fertilizer can effectively supply nutrients throughout the growing season, offering substantial labor and time savings for farmers cultivating large-scale field crops.

Horticultural Crops Segment in China Controlled Release Fertilizer Market

The horticultural crops segment is emerging as the fastest-growing major segment in China's controlled release fertilizer market, with a projected growth rate of approximately 8% from 2024 to 2029. This robust growth is driven by the increasing focus on high-value horticultural crops including fruits, vegetables, flowers, melons, tea, and traditional Chinese herbal medicines. The segment's growth is further supported by the rising adoption of precision farming techniques and the growing demand for premium quality produce in both domestic and export markets. The expansion of greenhouse cultivation and the increasing awareness among farmers about the benefits of controlled release fertilizers in improving crop quality and yield are also contributing to this segment's rapid growth. Additionally, the segment is benefiting from government initiatives promoting sustainable agriculture practices and the optimization of fertilizer use in horticultural production.

Remaining Segments in Crop Type Segmentation

The turf and ornamental segment, while smaller in market share, plays a significant role in China's controlled release fertilizer market, particularly in urban landscaping and recreational facilities. This segment primarily serves the growing demand from golf courses, public parks, and ornamental plant nurseries. The segment's importance is increasingly recognized in urban development projects where sustainable and efficient nutrient management is crucial for maintaining aesthetic appeal and environmental responsibility. The specialized nature of turf and ornamental applications requires precise nutrient release patterns, driving innovation in controlled release fertilizer formulations specifically designed for these applications.

China Controlled Release Fertilizer Industry Overview

Top Companies in China Controlled Release Fertilizer Market

The Chinese controlled release fertilizer market features a mix of domestic and international players, with companies like Hebei Woze Wufeng Biological Technology, Grupa Azoty, and Hebei Sanyuanjiuqi Fertilizer leading the segment. Product innovation has emerged as a key competitive strategy, with companies developing advanced coating technologies and specialized formulations tailored to specific crop needs. Operational agility is demonstrated through companies maintaining flexible production capabilities and robust distribution networks across different regions. Strategic partnerships have become increasingly important, particularly for expanding market reach and enhancing technological capabilities. Companies are actively pursuing geographical expansion through new trading subsidiaries, production facilities, and strategic alliances with local distributors to strengthen their market presence.

Fragmented Market with Strong Local Presence

The Chinese controlled release fertilizer market exhibits a fragmented structure, characterized by the strong presence of domestic manufacturers alongside international players. Local companies leverage their deep understanding of regional agricultural practices and established distribution networks to maintain competitive positions, while global players bring advanced technologies and international expertise. The market demonstrates a balanced mix of specialized fertilizer manufacturers and diversified agricultural input companies, with domestic players particularly strong in serving the field crops segment.

The competitive landscape shows limited consolidation activity, with companies primarily focusing on organic growth strategies rather than mergers and acquisitions. Market participants are increasingly emphasizing vertical integration to control quality and costs throughout the value chain. The presence of both state-owned enterprises and private companies creates a dynamic competitive environment, with different players adopting varied approaches to market penetration and customer engagement. International companies often enter the market through joint ventures or partnerships with local players to navigate regulatory requirements and establish market presence.

Innovation and Distribution Key to Growth

Success in the Chinese specialty fertilizer market increasingly depends on developing innovative coating technologies and efficient nutrient release mechanisms. Companies need to focus on building strong research and development capabilities while maintaining cost competitiveness through efficient production processes. Establishing comprehensive distribution networks, particularly in major agricultural regions, remains crucial for market penetration. Players must also invest in farmer education and demonstration programs to showcase the benefits of controlled release fertilizers over conventional alternatives.

Future market success will require companies to adapt to evolving environmental regulations and sustainable agriculture practices. Building strong relationships with agricultural cooperatives and large-scale farming operations can provide stable demand channels. Companies must also focus on developing products specifically tailored to local soil conditions and crop patterns. The ability to provide technical support and agronomic services alongside products will become increasingly important for maintaining market position. Players need to maintain price competitiveness while offering premium products, as farmers' purchasing decisions remain price-sensitive despite the growing recognition of environmentally friendly fertilizer benefits.

China Controlled Release Fertilizer Market Leaders

-

Grupa Azoty S.A. (Compo Expert)

-

Haifa Group

-

Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

-

Hebei Woze Wufeng Biological Technology Co., Ltd

-

Zhongchuang xingyuan chemical technology co.ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

China Controlled Release Fertilizer Market News

- February 2019: Haifa Group announced the opening of a new trading company in China. The establishment of the new Haifa subsidiary in China will enable the group to significantly expand its offerings to China agriculture sector.

- July 2018: Haifa Group introduced a novel range of coated micronutrients, enabling an all-season complete nutrition. Based on Multicote™ technology, the coated micronutrients provide your crops with all the benefits of controlled-release nutrition.

Free With This Report

Along with the report, We also offer a comprehensive and exhaustive data pack with 25+ graphs on area under cultivation and average application rate per hectare. The data pack includes Globe, North America, Europe, Asia-Pacific, South America, and Africa.

China Controlled Release Fertilizer Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

-

4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

-

4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

-

5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles

- 6.4.1 Grupa Azoty S.A. (Compo Expert)

- 6.4.2 Haifa Group

- 6.4.3 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.4 Hebei Woze Wufeng Biological Technology Co., Ltd

- 6.4.5 Zhongchuang xingyuan chemical technology co.ltd

- *List Not Exhaustive

7. KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- CULTIVATION OF FIELD CROPS IN HECTARE, CHINA, 2017 - 2022

- Figure 2:

- CULTIVATION OF HORTICULTURAL CROPS IN HECTARE, CHINA, 2017 - 2022

- Figure 3:

- CONSUMPTION OF PRIMARY NUTRIENTS BY FIELD CROPS IN KG/HECTARE, CHINA, 2022

- Figure 4:

- CONSUMPTION OF PRIMARY NUTRIENTS BY HORTICULTURAL CROPS IN KG/HECTARE, CHINA, 2022

- Figure 5:

- SPECIALITY FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 6:

- SPECIALITY FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 7:

- CRF CRF FERTILIZER CONSUMPTION BY COATING TYPE IN METRIC TON, CHINA, 2017 - 2030

- Figure 8:

- CRF CRF FERTILIZER CONSUMPTION BY COATING TYPE IN USD, CHINA, 2017 - 2030

- Figure 9:

- CRF CRF FERTILIZER CONSUMPTION VOLUME BY COATING TYPE IN %, CHINA, 2017 VS 2023 VS 2030

- Figure 10:

- CRF CRF FERTILIZER CONSUMPTION VALUE BY COATING TYPE IN %, CHINA, 2017 VS 2023 VS 2030

- Figure 11:

- POLYMER COATED CRF FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 12:

- POLYMER COATED CRF FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 13:

- POLYMER COATED CRF FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 14:

- POLYMER-SULFUR COATED CRF FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 15:

- POLYMER-SULFUR COATED CRF FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 16:

- POLYMER-SULFUR COATED CRF FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 17:

- OTHERS CRF FERTILIZER CONSUMPTION IN METRIC TON, CHINA, 2017 - 2030

- Figure 18:

- OTHERS CRF FERTILIZER CONSUMPTION IN USD, CHINA, 2017 - 2030

- Figure 19:

- OTHERS CRF FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2023 VS 2030

- Figure 20:

- CRF CRF FERTILIZER CONSUMPTION BY CROP TYPE IN METRIC TON, CHINA, 2017 - 2030

- Figure 21:

- CRF CRF FERTILIZER CONSUMPTION BY CROP TYPE IN USD, CHINA, 2017 - 2030

- Figure 22:

- CRF CRF FERTILIZER CONSUMPTION VOLUME BY CROP TYPE IN %, CHINA, 2017 VS 2023 VS 2030

- Figure 23:

- CRF CRF FERTILIZER CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2017 VS 2023 VS 2030

- Figure 24:

- CRF FERTILIZER CONSUMPTION BY FIELD CROPS IN METRIC TON, CHINA, 2017 - 2030

- Figure 25:

- CRF FERTILIZER CONSUMPTION BY FIELD CROPS IN USD, CHINA, 2017 - 2030

- Figure 26:

- FERTILIZER CONSUMPTION VALUE BY COATING TYPE IN %, CHINA, 2023 VS 2030

- Figure 27:

- CRF FERTILIZER CONSUMPTION BY HORTICULTURAL CROPS IN METRIC TON, CHINA, 2017 - 2030

- Figure 28:

- CRF FERTILIZER CONSUMPTION BY HORTICULTURAL CROPS IN USD, CHINA, 2017 - 2030

- Figure 29:

- FERTILIZER CONSUMPTION VALUE BY COATING TYPE IN %, CHINA, 2023 VS 2030

- Figure 30:

- CRF FERTILIZER CONSUMPTION BY TURF & ORNAMENTAL IN METRIC TON, CHINA, 2017 - 2030

- Figure 31:

- CRF FERTILIZER CONSUMPTION BY TURF & ORNAMENTAL IN USD, CHINA, 2017 - 2030

- Figure 32:

- FERTILIZER CONSUMPTION VALUE BY COATING TYPE IN %, CHINA, 2023 VS 2030

- Figure 33:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, CHINA, 2017 - 2030

- Figure 34:

- CHINA CONTROLLED RELEASE FERTILIZER MARKET, MOST ADOPTED STRATEGIES, 2018 - 2021

- Figure 35:

- MARKET SHARE OF MAJOR PLAYERS IN %, CHINA

China Controlled Release Fertilizer Industry Segmentation

Polymer Coated, Polymer-Sulfur Coated, Others are covered as segments by Coating Type. Field Crops, Horticultural Crops, Turf & Ornamental are covered as segments by Crop Type.| Coating Type | Polymer Coated |

| Polymer-Sulfur Coated | |

| Others | |

| Crop Type | Field Crops |

| Horticultural Crops | |

| Turf & Ornamental |

Need A Different Region or Segment?

Customize Now

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Urea & Complex

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF