Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

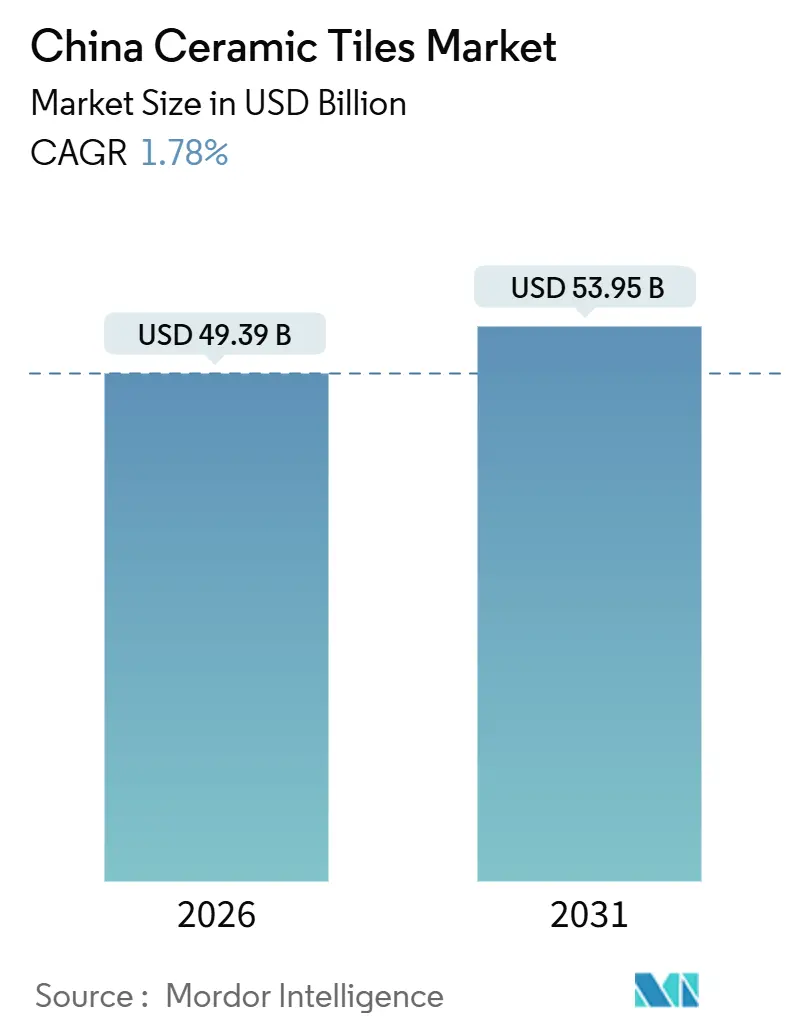

| Market Size (2026) | USD 49.39 Billion |

| Market Size (2031) | USD 53.95 Billion |

| Growth Rate (2026 - 2031) | 1.78% CAGR |

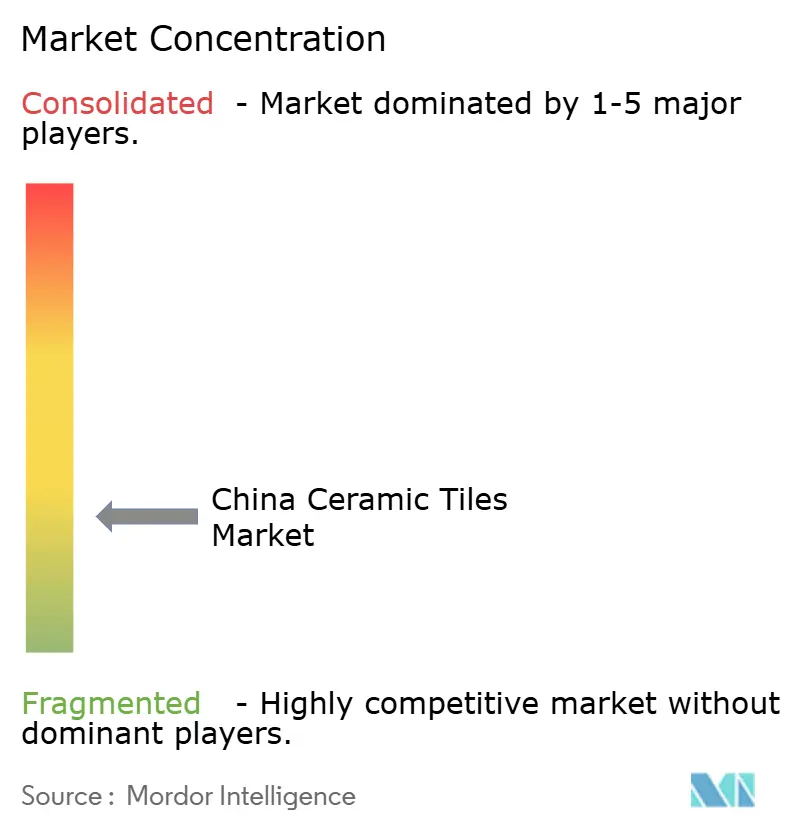

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Ceramic Tiles Market Analysis by Mordor Intelligence

The China Ceramic Tiles Market size is estimated at USD 49.39 billion in 2026, and is expected to reach USD 53.95 billion by 2031, at a CAGR of 1.78% during the forecast period (2026-2031).

The category scope spans product type, application, end-user, construction type, distribution channel, and geography, and is assessed in value terms. Domestic output fell to 5.91 billion square meters in 2024, with utilization at 48% of 12.21 billion square meters of installed capacity, highlighting an overcapacity overhang that is shaping pricing and consolidation dynamics[1]Editorial Team, “China’s tile industry and market continue decline,” Ceramic World Web, ceramicworldweb.com . Policy support provides a stabilizing backdrop as 25,800 old urban residential communities were renovated in the first eleven months of 2025, and urban renewal remains a defined priority. Quality-driven housing standards embedded in the 15th Five-Year Plan are reinforcing the shift to higher-spec materials, which supports porcelain adoption and green-certified tile demand in the China ceramic tiles market. Competitive behavior is evolving as manufacturers pivot from volume-led output to product innovation, omnichannel reach, and factory efficiency upgrades to recover margins after years of price compression. Trade barriers will continue to shape export mix and pricing strategies after the United States maintained antidumping and countervailing orders in late 2025.

Key Report Takeaways

- By product type, porcelain tiles led with 54.45% of the China ceramic tiles market share in 2025, while mosaic tiles are projected as the fastest growing at a 1.98% CAGR through 2031.

- By application, floor tiles accounted for 63.43% of the China ceramic tiles market share, and roofing is forecast to grow at a 1.86% CAGR to 2031.

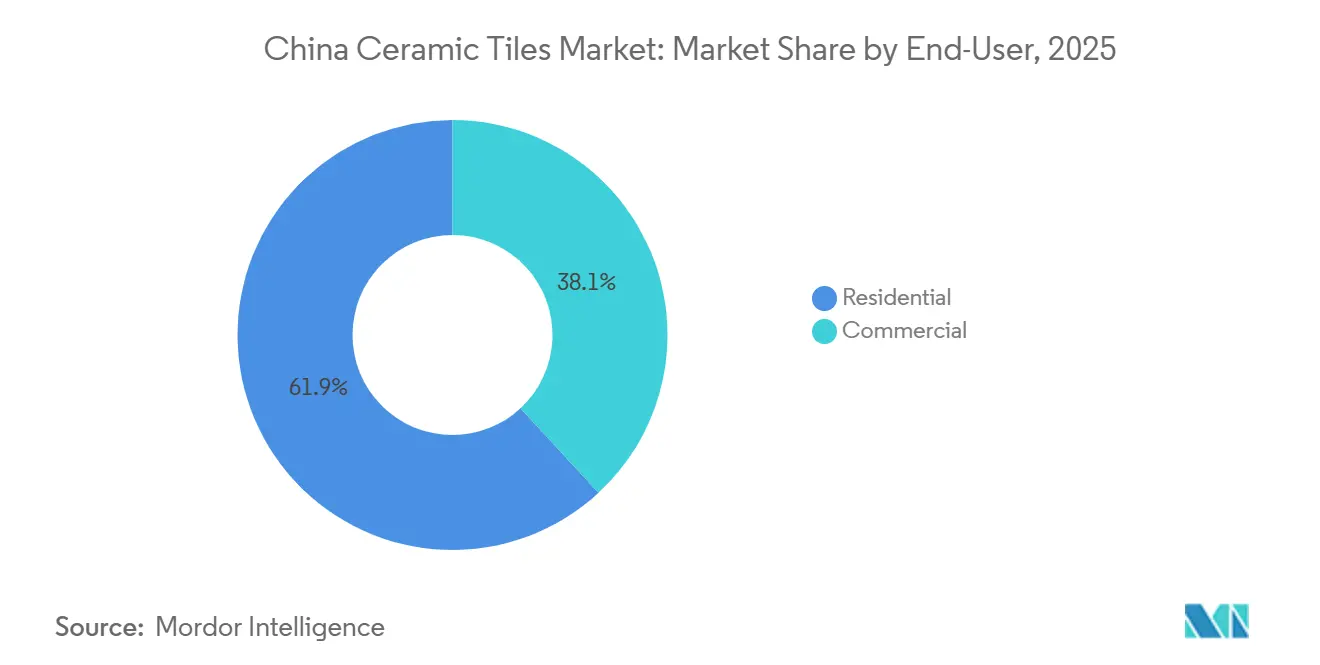

- By end-user, residential captured 61.89% of the China ceramic tiles market share in 2025 and is the fastest growing at a 2.19% CAGR through 2031.

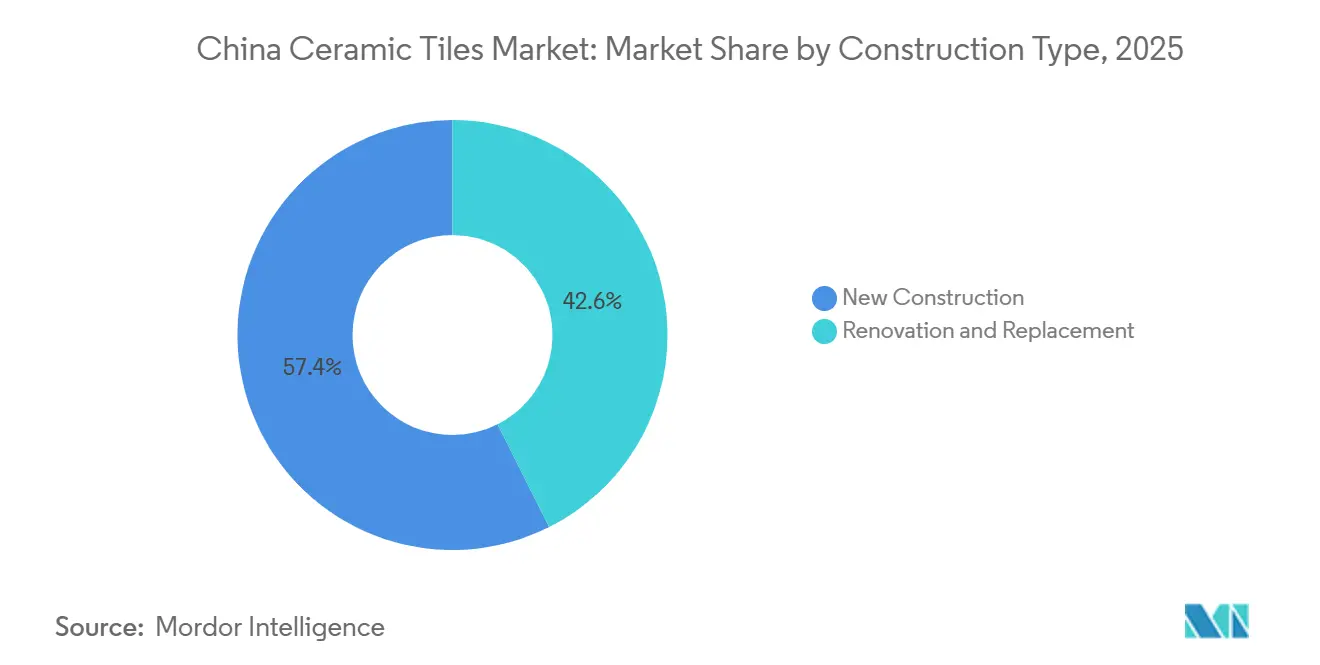

- By construction type, new construction held 57.42% of the China ceramic tiles market share of 2025 volumes, and renovation and replacement are expanding at a 1.92% CAGR to 2031.

- By distribution channel, specialty tile and stone stores retained a 40.72% of the China ceramic tiles market share, while online retail is the fastest growing at a 2.64% CAGR to 2031.

- By geography, East China led with a 32.11% of the China ceramic tiles market share in 2025, and North China is forecast as the fastest growing at a 2.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban-home upgrade & renovation boom | +0.6% | Global, the highest in East China, North China, and Central China | Medium term (2-4 years) |

| Government pushes for green-building tiles | +0.5% | National, with early gains in Beijing, Shanghai, Guangzhou, Shenzhen | Medium term (2-4 years) |

| E-commerce and live-stream tile retailing growth | +0.3% | National, strongest in Tier 1 and Tier 2 cities | Short term (≤ 2 years) |

| Digital printing for mass-customized décor | +0.2% | National, concentrated in Guangdong, Fujian, and Shandong | Medium term (2-4 years) |

| Export recovery to Belt-and-Road markets | +0.2% | Global; Asia, the Middle East, and Africa | Medium term (2-4 years) |

| Waste-heat-recovery kilns adoption | +0.1% | National, prioritized in Shandong, Sichuan, Guangdong | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban-Home Upgrade & Renovation Boom

China launched renovation projects at 25,800 old urban residential communities during January to November 2025, surpassing the annual target and reinforcing the policy commitment to urban renewal as a steady driver of household-quality improvements[3]Xinhua News Agency, “China initiates renovation projects at 25,800 urban residential communities from Jan-Nov,” State Council of the People’s Republic of China, gov.cn . Government communications in late 2025 emphasized urban renewal as a structural lever to optimize urban form, transform growth engines, and advance green living standards, which sets a multi-year demand runway for mid-grade and premium tiles in living spaces and sanitary areas. The scope of renovation, such as pipeline upgrades, community amenities, and accessibility improvements, naturally channels spend toward durable and hygienic surfaces that meet safety, ease-of-cleaning, and lifecycle cost expectations. Renovation aligns with kitchen and bathroom refresh cycles for urban households, which supports steady reorder volumes for wall and floor tiles even when new housing starts remain subdued.

Government Push for Green-Building Tiles

The General Code for Building Energy Conservation and Renewable Energy Utilization established mandatory carbon-intensity controls in buildings and tighter energy-saving thresholds, which steer project specifications toward low-emission materials, including tiles with environmental product declarations[2]Editorial Team, “China’s new green building regulations are here,” Aden Services, adenservices.com. The China Building Materials Federation launched a national carbon labelling and EPD project in March 2024 that includes ceramic tiles in trial operations and targets wider label issuance during the 14th Five-Year Plan, accelerating standardization and data disclosure. Lifecycle assessments for Eastern China show cradle-to-gate footprints dominated by the production phase, which prioritizes fuel switching, lower-temperature firing, and afterheat recovery interventions by tile producers. National energy and emission targets under the 14th Five-Year Comprehensive Work Plan reinforce a shift away from coal in ceramics, which raises the relevance of natural gas combustion, electricity-based processes, and eventual hydrogen readiness. As procurement systems start to reference carbon thresholds and documentation, manufacturers that invest in measurable reductions position themselves for bid advantages on public and private projects. The net effect is a nudge toward higher-spec porcelain and eco-aligned products in the China ceramic tiles market, especially in metro areas where green building adoption is most advanced.

E-Commerce & Live-Stream Tile Retailing Growth

Online retail is the fastest-growing distribution channel and is scaling due to the maturity of live-stream platforms and direct-to-professional experiences tailored to decorators, designers, and supervisors. Leading brands are building mini-app ecosystems to engage foreman networks through incentives and interactive programs, which is boosting small-business conversion and repeat purchasing. Live demonstrations of large-format slabs, antimicrobial features, and digital-printed textures are compressing decision cycles by enabling real-time product inspection and Q&A. Trade data from March 2025 shows sharp import growth via coastal hubs, signalling that online and cross-border channels are also widening access to premium European tiles in local markets. The integration of augmented reality previews within major marketplaces helps address tactile concerns, lower returns, and translate showroom browsing into digital confidence. This shift reshapes the China ceramic tiles market as suppliers blend offline experience centres with digital journeys to meet buyers where they research and transact.

Waste-Heat-Recovery Kilns Adoption

National policy targets for energy intensity and emissions are accelerating clean-fuel transitions and efficiency upgrades in ceramics, which positions waste-heat recovery and low-temperature firing as priority investments. Technical guidelines highlight major savings potential in firing and drying stages through regenerative burners, controlled dehumidification, and exhaust recirculation measures. Factories in gas-converted provinces are using these upgrades to meet tightening local standards while improving unit economics under fuel-cost volatility. Over time, technology pilots around cleaner combustion and hybrid systems can open pathways to carbon-label compliance and procurement preferences for green-certified tiles. This transition supports brand positioning for eco-performance in the China ceramic tiles market and may unlock access to climate-linked financing at the project level. The direction is clear as policy, procurement, and available equipment all nudge producers to capture efficiency gains that compound over the medium term.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged real estate slowdown and oversupply | -1.2% | National, most severe in Tier 1 and Tier 2 cities | Medium term (2-4 years) |

| Stricter environmental compliance costs | -0.4% | National, tighter in Beijing-Tianjin-Hebei, the Yangtze River Delta, the Pearl River Delta | Long term (≥ 4 years) |

| Anti-dumping duties on Chinese tile exports | -0.3% | Global, direct impact in North America and the European Union | Long term (≥ 4 years) |

| Rising competition from Indian and Vietnamese producers | -0.2% | Global export markets across Asia-Pacific, the Middle East, Africa, and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Real-Estate Slowdown and Oversupply

Domestic ceramic tile consumption declined in 2024 while installed capacity remained high, which kept utilization near 48% and intensified price competition. Global data for 2024 confirms output contraction and underscores how weak home sales and constrained developer liquidity continued to weigh on building materials. Producer counts and active production lines fell between 2022 and 2024, yet capacity reductions lagged due to line upgrades, so overhang and margin compression persisted. Asset auctions accelerated in 2025, creating opportunities for stronger players to acquire capacity and permits at discounts after repeated rounds. Despite policy signals to stabilize real estate and promote urban renewal from 2026, the timeline to normal absorption remains uncertain as market repair depends on inventory clearance and funding transmission to projects. The China ceramic tiles market, therefore, leans on renovation and public investment as bridges while residential sales cycles normalize.

Stricter Environmental Compliance Costs

The ceramic tiles market in China faces ongoing pressure from stricter environmental compliance costs through 2026, driven by the 14th Five-Year Plan's mandates for low-carbon kiln fuels and efficiency upgrades, which impose significant financial burdens, particularly on small and mid-sized plants lacking retrofit scalability. Lifecycle assessments show manufacturing stages dominate tile carbon footprints, which means meaningful reductions require investments in firing technology and heat recovery. Industry guidance underscores the need for rapid upgrades and data systems to support labelling and bidding compliance, which increases administrative and certification burdens. Technical best practices like regenerative burners and exhaust recirculation reduce fuel consumption but require upfront outlays and process control capabilities that not all producers possess. Firms with constrained balance sheets may defer upgrades, which risks non-compliance or loss of eligibility in green procurement, pressuring volumes and pricing power. Over the long term, early adopters can benefit from procurement preferences, but the near-term cost curve remains a restraint for the China ceramic tiles market.

Segment Analysis

By Product Type: Porcelain dominance meets mosaic micro-surge

Porcelain tiles held 54.45% of 2025 revenues, confirming their leadership in performance attributes and alignment with green-building specifications in the China ceramic tiles market. This position reflects low water absorption, high density, and durability that meet indoor and outdoor application needs for residential and commercial builds in major cities. Digital printing and glazing advances are enabling premium, stone-like finishes at scale while preserving cutover flexibility and controlling glaze consumption at precise levels. Producers are investing in color research and finish curation to support architects and designers with toolkits that raise the perceived value of porcelain assortments. This portfolio depth helps brands defend pricing amid overcapacity and reduces reliance on basic commodity lines in the China ceramic tiles industry.

Mosaic tiles are forecast to post a 1.98% CAGR through 2031, making them the fastest-growing product type in the China ceramic tiles market. Growth is tied to customized design demand in high-end hospitality and luxury residential spaces, where accent walls and feature installations allow small-format and pattern-rich designs. As digital workflows streamline short-run production, manufacturers can offer broader palettes without inventory risk and respond faster to design briefs. Sanitary and antimicrobial features add further use cases in wet zones, reinforcing the role of mosaics in bathrooms, spas, and commercial kitchens. These attributes, combined with omnichannel merchandising, support steady share gains for decorative formats that benefit from visual storytelling and tactile experiences.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Floors anchor, roofing awakens

Floor tiles captured 63.43% of 2025 application revenues, and roofing applications are projected to record a 1.86% CAGR through 2031, highlighting the continued dominance of heavy-duty surfaces in the China ceramic tiles market. Floors remain the default in living areas, retail, and public spaces due to durability and hygiene benefits that align with updated codes and property-management standards. Urban renewal is adding steady replacement demand in older homes, where upgrading floors and wet-area walls is central to quality-of-life improvements. Transport and civic projects continue to specify large-format porcelain slabs to reduce grout lines and maintenance, which pushes up average selling prices in commercial jobs. Roofing tiles are expanding as municipalities standardize outdoor-rated materials on public structures to extend lifecycle value and unify urban aesthetics.

Wall tiles hold a significant secondary share and benefit from design-led upgrades as 3D textures, metallic glazes, and extra-large panels migrating from high-end hospitality into mainstream residential formats in the China ceramic tiles market. Digital printing allows realistic stone and wood effects for feature walls in bathrooms and lobbies that require visual impact with high cleanability. Roof applications benefit from the same firing and glaze technologies that increase UV resistance and thermal stability, creating durable surfaces for pergolas and public shelters. Specialty uses like pool linings and exterior facades add variety, with demand skewed to warmer provinces and commercial complexes upgrading visitor amenities. Collectively, these application trends support a steady shift toward value-added specifications within the China ceramic tiles industry.

By End-User: Residential leads, commercial rebounds

Residential accounted for 61.89% of 2025 consumption and is the fastest-growing end-use at a 2.19% CAGR, reflecting policy-led renovation momentum in the China ceramic tiles market. National renovation programs continue to refresh legacy housing stock, which directly drives purchases of wall and floor tiles in kitchens, bathrooms, and living areas. Hygiene features and low-maintenance properties add to the appeal in busy urban households that prioritize durable finishes. These factors reinforce steady residential throughput across Tier 1 to Tier 3 cities, even as new-home completions vary by locality.

Commercial demand is recovering in tandem with investments in public buildings, retail refits, hospitality, and transport nodes, which prize large-format slabs and specialized finishes. Antimicrobial and slip-resistant products are gaining traction in hotels and healthcare to reduce maintenance and support infection-control protocols. Offices and institutions retrofits favor consistent colorways and cleanability for high-traffic corridors, shifting specifications toward heavy-duty porcelain. As the commercial project pipeline normalizes, specification-led orders help manufacturers lean into value tiers where design and performance outweigh pure price decisions. This mix supports steady improvement in margin structure for brands focused on solutions and project service in the China ceramic tiles industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Construction Type: New builds lead, renovation accelerates

New construction captured 57.42% of 2025 volumes, while renovation and replacement are growing at a 1.92% CAGR to 2031 in the China ceramic tiles market. New residential and commercial projects still specify ceramic tiles as standard for code compliance, cleanability, and lifecycle value in common areas and wet rooms. Even with uneven developer funding, public-sector builds, fit-outs, and infrastructure projects sustain baseline demand. Gas conversion and efficiency mandates in certain provinces also favor domestic sourcing that meets local emission requirements. This supports steady pipeline execution for factories aligned to regulatory expectations within priority regions.

Renovation demand is widening due to large-scale community upgrades, with 25,800 communities renovated during January to November 2025, and further emphasis is set for the plan period. Homeowners often upgrade to porcelain or large-format slabs when replacing tiles, which lifts average selling prices and service content. Revised codes effective in recent years have increased the use of performance tiles that can meet energy and durability targets in existing buildings. This reinforces renovation as a long-run contributor to the China ceramic tiles market, balancing volatility in new starts. Manufacturers building service capabilities for tear-out, logistics, and installation support will be best placed to capture the growing retrofit opportunity.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Specialty stores hold ground, online surges

Specialty tile and stone stores retained 40.72% of 2025 revenues, while online retail is the fastest-growing channel at a 2.64% CAGR to 2031 in the China ceramic tiles market. Large showrooms allow tactile evaluation and full-swatch comparisons for mid- and high-end buyers, which keeps this channel relevant for complex projects. At the same time, brands are building omnichannel systems that pair digital discovery with appointment-based store visits to close sales efficiently. Digital initiatives such as mini-apps for contractor engagement are turning small-business networks into repeat customers with programmatic incentives. Cross-border e-commerce is also deepening access to premium imports via coastal hubs, which expands consumer choice in metropolitan areas.

Direct sales to contractors are a structural component of commercial and infrastructure orders, where volume pricing and coordinated logistics matter more than retail experience. Online platforms have started to add offline experience centres in major cities to address tactile needs while keeping digital pricing and inventory transparency. Specialty stores are digitizing appointment booking and product visualization to match the convenience of e-commerce while maintaining advisory value. The China ceramic tiles industry is therefore converging toward blended models that meet consumers and project buyers across research, selection, and fulfillment steps. This evolution supports wider assortment visibility and higher conversion across tiers of the China ceramic tiles market.

Geography Analysis

East China led the China ceramic tiles market with a 32.11% consumption share in 2025, supported by dense urban centres, higher disposable incomes, and strong renovation activity. Shanghai and surrounding cities continue to specify large-format porcelain in commercial and hospitality spaces, reflecting a preference for modern aesthetics and durability. Zhejiang’s surge in import value in March 2025 highlights the role of e-commerce and logistics infrastructure in diversifying assortments for local retailers. The region’s supply chain efficiency lowers lead times and supports upgrade cycles in both residential and non-residential projects. South China remains a core manufacturing hub centred on Foshan, with robust export connectivity through Shenzhen and Guangzhou that supports regional and overseas shipments.

North China is the fastest-growing region at a 2.15% projected CAGR, aided by integrated development plans and winter-heating retrofits that require floor and wall upgrades. Strong public-sector procurement in Beijing favours domestic, green-aligned tiles, which underpins factory planning and investment in compliant technologies. Provincial policies to curb coal use and increase gas penetration in ceramics support cleaner production, aligning local supply with public project specifications. Central China serves as a strategic logistics corridor where rising urbanization in key cities is supporting steady residential renovation and public works spending. These dynamics help smooth regional demand variance and maintain throughput across factories serving inland markets.

The Rest of China, including the Northeast, Southwest, and Northwest provinces, shows differentiated trajectories that collectively balance the national picture for the China ceramic tiles market. Southwest provinces benefit from infrastructure and tourism-related projects that expand demand for public-facing installations, which favor slip-resistant and high-durability tiles. Environmental compliance progress in Sichuan supports local producers in winning tenders that prioritize cleaner processes, reinforcing regional supply strengths. In the Northwest, ongoing urban investments in key cities sustain incremental tile needs for administrative and service buildings. Across these regions, channel mixes vary as cost considerations lead to a greater reliance on home-improvement chains and direct sales for project-based orders.

Competitive Landscape

The China ceramic tiles market features a large number of manufacturers and persistent overcapacity, which keeps pricing competitive and margins sensitive to production efficiency. Producer and line counts decreased between 2022 and 2024 as weaker operators exited or consolidated, but capacity remained elevated due to equipment upgrades. In response, leading brands are focusing on performance attributes, color systems, and format expansion to differentiate and secure project pipeline visibility. The balance of channel power is shifting as digital initiatives create direct lines to supervisors and designers, which helps compress sales cycles and stabilize volumes. These actions support a gradual transition away from pure price competition toward solution selling and lifecycle value propositions.

Monalisa Group opened an industry-first ceramic tile color centre in March 2025 with a research institute partner, designed to systematize chromatic analysis and enable differentiated product curation. Dongpeng introduced antimicrobial tiles with embedded protection against E. coli and S. aureus, aimed at hospitality and healthcare applications that value durable hygiene performance. Marco Polo Holdings was listed on the Shenzhen Stock Exchange in October 2025, raising funds for intelligent and green manufacturing upgrades and strengthening its capital-market profile. The combination of product innovation, operational enhancements, and capital access is a recurring theme among market leaders, who seek to defend share while improving unit economics. As specification-led orders expand, these players are well placed to compete on performance and service alongside cost.

Consolidation pressures remain visible through asset auctions that offer capacity and permits at discounts after repeated bidding rounds, leading to industry restructuring opportunities. Technology deployment is accelerating as exhibitors at Ceramics China 2025 showcased AI-integrated production workflows and compact, eco-friendly equipment to reduce costs and improve quality control. Export strategies continue to evolve under sustained trade remedies in the United States and extended duties in the European Union, which is redirecting volumes to Asia and the Middle East. Enforcement cases in late 2025 reinforced legal exposure around transshipment, further sharpening compliance practices for cross-border trade. These conditions are catalyzing a shift toward higher-value design, greener manufacturing, and tighter operational discipline in the China ceramic tiles market.

China Ceramic Tiles Industry Leaders

Dongpeng Ceramic

Marco Polo Holdings

Monalisa Group

New Pearl Ceramics

Ceramics China

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: The United States Department of Justice announced indictments alleging a scheme to evade customs duties, including antidumping and countervailing duties on ceramic tiles, by using false Malaysian origin claims, highlighting enforcement risks for transshipment schemes.

- October 2025: Marco Polo Holdings Co., Ltd. debuted on the Shenzhen Stock Exchange, raising USD 228.6 million. The funds will support production modernization, green initiatives, and capacity expansion. Operating five production bases and 8,276 retail outlets, the company invests USD 41.7 million annually in research and development and holds 825 patents, marking a significant milestone for Guangdong’s ceramic industry.

- June 2025: Ceramics China 2025, the 39th edition of the world’s largest annual event for ceramic equipment and materials, concluded in Guangzhou in June 2025 with 786 exhibitors from 21 countries and regions and 80,240 professional visits from 94 countries and regions over four days, showcasing AI-enabled production, eco-friendly equipment, digital manufacturing, and end-to-end service systems.

- March 2025: Monalisa Group established the industry’s first ceramic tile color centre in collaboration with the Color Research Institute of Tsinghua Qingdao Academy of Art and Science Innovation to drive innovation-driven color research, promote interdisciplinary integration of color science and material technology, and support sustainable transformation, including the development of color tools for distributors and designers.

China Ceramic Tiles Market Report Scope

Ceramic tiles, composed of natural materials such as clay and sand, are shaped and fired at high temperatures to create durable and versatile surface coverings. These tiles are commonly used for floors, walls, and backsplashes. Compared to stone, ceramic tiles are easier to cut and install but are less dense and more porous than porcelain, making them suitable for indoor applications. However, they require sealing in wet areas. Kiln-fired for enhanced durability, ceramic tiles offer resistance to water, moisture, and fire. Additionally, they are a cost-effective alternative to other flooring materials, making them a popular choice in the market.

The China Ceramic Tiles Market report is segmented by product type (porcelain tiles, glazed ceramic tiles, unglazed ceramic tiles, mosaic tiles, others), application (floor, wall, roofing), end-user (residential, commercial), construction type (new construction, renovation and replacement), distribution channel (specialty tile & stone stores, home improvement & DIY stores, online retail, direct sales to contractors), and geography (East China, South China, North China, Central China, Rest of China). The market forecasts are provided in terms of value (USD).

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| East China (Shanghai, Jiangsu, Zhejiang, Anhui) |

| South China (Guangdong, Guangxi, Hainan) |

| North China (Beijing, Tianjin, Hebei, Shanxi, Inner Mongolia) |

| Central China (Henan, Hubei, Hunan) |

| Rest of China (Northeast, Southwest,Northwest) |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | East China (Shanghai, Jiangsu, Zhejiang, Anhui) | |

| South China (Guangdong, Guangxi, Hainan) | ||

| North China (Beijing, Tianjin, Hebei, Shanxi, Inner Mongolia) | ||

| Central China (Henan, Hubei, Hunan) | ||

| Rest of China (Northeast, Southwest,Northwest) | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and projected growth of the Chinese ceramic tiles market?

The China ceramic tiles market size is USD 49.39 billion in 2026 and is projected to reach USD 53.95 billion by 2031 at a 1.78% CAGR.

Which product types lead and which are growing fastest in the China ceramic tiles market?

Porcelain tiles lead with 54.45% revenue share in 2025, while mosaic tiles post the fastest growth at a 1.98% CAGR through 2031.

Which sales channels are expanding fastest for tiles in China?

Specialty tile and stone stores hold the largest share, while online retail is the fastest-growing channel with a 2.64% CAGR as live streaming and AR tools lift conversions.

Which regions contribute most to demand and growth in China?

East China leads with 32.11% of 2025 consumption, while North China is set to expand the fastest through 2031 with a 2.15% CAGR on infrastructure and retrofit programs.

How are green-building policies affecting tile demand in China?

Mandatory energy and carbon standards linked to the 14th Five-Year Plan are boosting demand for low-carbon and certified tiles, favouring producers that adopt EPDs and efficient kilns.

How do the United States and EU trade measures affect the China ceramic tiles market?

United States duties and renewed EU anti-dumping measures constrain shipments, pushing exporters to prioritize Belt-and-Road destinations and focus on value-added products to sustain volumes.