| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 348.6 Million |

| Market Size (2030) | USD 534.6 Million |

| CAGR (2025 - 2030) | 8.93 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

China Biocontrol Agents Market Analysis

The China Biocontrol Agents Market size is estimated at 348.6 million USD in 2025, and is expected to reach 534.6 million USD by 2030, growing at a CAGR of 8.93% during the forecast period (2025-2030).

China's agricultural sector faces unique challenges and opportunities, as the country feeds approximately 20% of the world's population using just 7% of the planet's arable land. This resource constraint has driven significant innovation and policy changes in agricultural practices. The government has implemented comprehensive initiatives to promote sustainable agriculture, with municipal authorities at all levels developing localized organic agriculture plans. These initiatives are complemented by incentive programs designed to encourage producers to transition from conventional to organic farming methods, reflecting a systematic approach to agricultural modernization.

The shift toward sustainable agriculture is evidenced by the expanding organic farming sector, with China's organic planting area reaching 2.4 million hectares. The country's northeastern provinces, including Liaoning, Jilin, and Heilongjiang, have emerged as the primary organic production hubs, particularly for export-oriented products. The organic sector is experiencing robust growth, with the market for organic food expanding at an annual rate of 25%, driven by increasing domestic demand and export opportunities, particularly to Japan, South Korea, Europe, and the United States.

The Ministry of Agriculture and Rural Affairs has set ambitious targets for sustainable pest management, aiming to implement integrated pest management and green prevention methods across 55% of the total crop area by 2025. This initiative is part of a broader strategy that includes specific goals for different crop categories, including a 10% reduction in pesticide use for fruits, vegetables, and tea within a three-year timeframe. These targets demonstrate China's commitment to transforming its agricultural practices while maintaining its position as a global agricultural powerhouse.

The cotton and sugarcane sectors exemplify the scale of China's agricultural operations and the potential impact of biocontrol adoption. With China producing 6.4 million tons of cotton in 2022 and maintaining approximately 1.2 million hectares of sugarcane harvest area, these sectors represent significant opportunities for biocontrol implementation. The government's focus on reducing chemical pesticide usage, particularly in major cash crops, has created a favorable environment for the adoption of biological control alternatives, supported by research initiatives and technological advancements in pest management strategies. The integration of agricultural biologicals and biological pest management solutions further underscores the shift towards natural pest control methods in China.

China Biocontrol Agents Market Trends

Country’s zero growth in pesticides use and increasing exports under organic products driving the organic cultivation.

- According to the latest reports by FiBL and the IFOAM, the market for organic food in China is growing at an annual rate of 25.0%. The shift from conventional to organic is a transformation toward a more sustainable food system within China, given the USD 2.91 billion of agri-food commodities exported from China each year.

- The size of organic farmland increased rapidly in China because more people started buying organic products due to increased incomes and the increasing importance of food safety. In the last three years, China's organic planting area increased by 10%, reaching 2.4 million ha in 2020. In addition, national policies have been adopted to promote organic production, advocating the slogans that state, ″lucid waters and lush mountains are invaluable assets″ and ″green development".

- Organic farming in China is majorly export-oriented. The products that are both exported and imported include cereals, soybeans, fruits, and vegetables. China's three northeastern provinces (Liaoning, Jilin, and Heilongjiang) support the largest organic production nationally in terms of output, volume, and area. Most organic farms located in the northern part of China (e.g., Shandong and Liaoning) supply organic vegetables and fruits to nearby cities. In addition, they export some products to Japan, South Korea, Europe, and the United States.

- With the increasing concerns of soil toxicity due to the overuse of synthetic fertilizers and pesticides that lead to soil contamination, the demand for sustainable agriculture practices and organic food production is on the rise in China. This moderately slow yet increasing shift in cultivation practices has also subsequently increased the demand for crop nutrition and protection products.

Understand The Key Trends Shaping This Market

Download PDF

The growing demand for organic products, approximately 73% of Chinese consumers are willing to have organic food

- China's organic food market is developing rapidly, and the potential demand for organic food among Chinese consumers is enormous. This is due to the growth of the wealthier middle classes and a greater awareness of the health implications. In 2021, organic food sales in China amounted to about USD 77.54 billion.

- Due to various government laws that favor organic food over food safety and customer preferences for organic food over conventional food, the demand for organic food items has considerably expanded. While prices of organic vegetables in China range from 3 to 15 times the cost of conventional produce, prices for organic vegetables are generally between 5 and 10 times that of their conventional counterparts. However, despite the price factor being a barrier, wealthy families and individuals with health problems are eager to increase their budget, with approximately 73% of Chinese consumers willing to pay extra for organic foods.

- The Chinese government is slowly aiming to become self-reliant in the organic food sector. For instance, the economy is slowly moving toward a green agriculture practice by encouraging farmers to scale back the use of chemical fertilizers and switch to bio-based alternatives. The China Chain Store and Franchise Association (CCFA) research in 2020 declared that organic awareness among the Chinese population in developed cities was at 83% when it came to an understanding of the concept of sustainable food production. Although China's organic food sector is still quite small and falls far short of satisfying domestic and international consumer demand, it can be stated that organic food in China has enormous potential in both the domestic and foreign markets, considering the rise in domestic sales by 4.01% in 2021.

Segment Analysis: Form

Macrobials Segment in China Biocontrol Agents Market

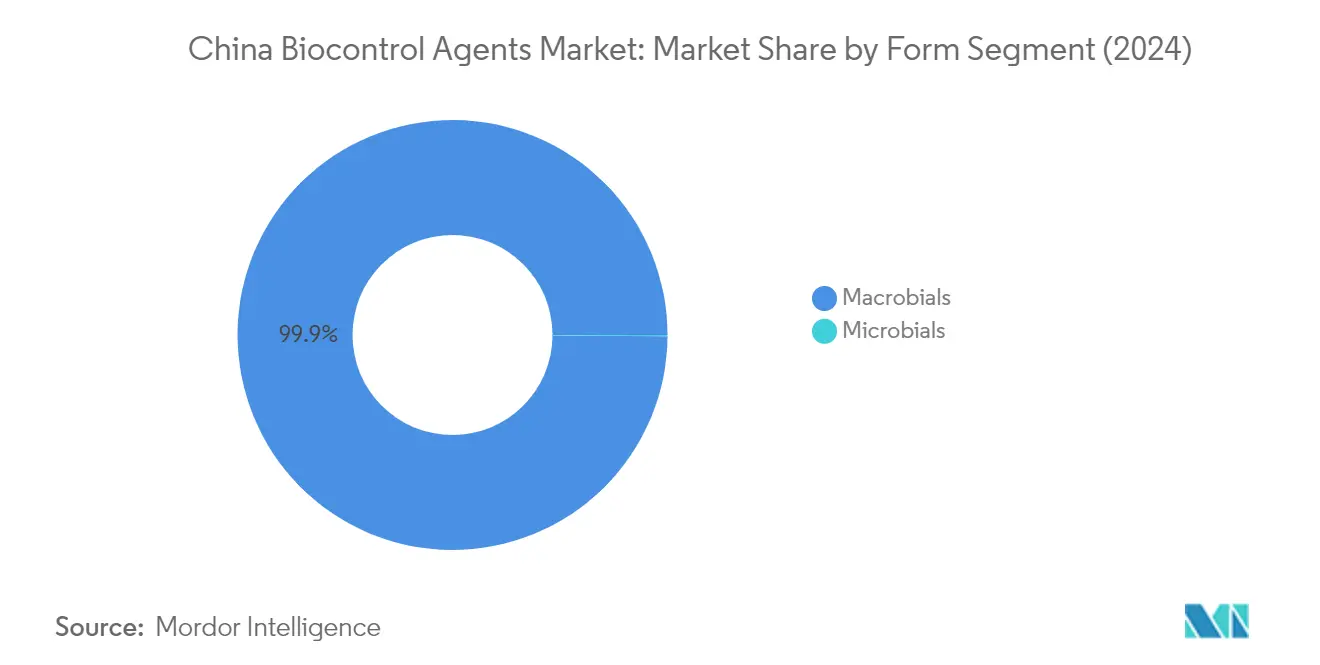

Macrobials dominate the Chinese biocontrol agents market, accounting for approximately 99.9% of the total market value in 2024. These natural enemies of pests, known as invertebrate biocontrol agents, include mites, predatory insects, parasitoids, and entomopathogenic nematodes (EPNs). The segment's dominance is primarily attributed to their effectiveness in controlling a wide range of agricultural pests through various mechanisms. Parasitoids and predatory insects are particularly significant within this segment, as they can attack different pest species at various stages of their life cycles. The segment is projected to maintain its market leadership while growing at around 9% CAGR from 2024 to 2029, driven by increasing awareness among farmers about the detrimental effects of chemical pesticides, government initiatives to reduce chemical pesticide usage, and the expanding trend in organic crop cultivation across China.

Microbials Segment in China Biocontrol Agents Market

The microbials segment, though smaller in market share, plays a crucial role in the Chinese biocontrol agents market. This segment encompasses bacterial, fungal, and other microbial agents that work through various mechanisms to protect plants against pathogens. Bacterial biocontrol agents dominate the microbials segment due to their rapid growth, ease of handling, and aggressive colonizing ability. These agents are particularly effective in controlling various plant diseases through direct or indirect interactions with pathogens. Fungal biocontrol agents are also significant within this segment, as they are rapidly evolving in crop protection and food production, offering complex modes of action that do not harm the environment or develop resistance in various types of pests and pathogens. The use of microbial pesticides and biological fungicides is becoming increasingly popular due to their effectiveness and environmental benefits.

Segment Analysis: Crop Type

Row Crops Segment in China Biocontrol Agents Market

Row crops dominate the Chinese biocontrol agents market, accounting for approximately 82% of the total market value in 2024. This significant market share is primarily attributed to the region's extensive organic cultivation area, with row crops representing over 82% of the total organic crop area. The major row crops in China include rice, barley, corn, millet, oat, sorghum, wheat, cottonseed, peanuts, rapeseed, soybean, and sunflower. The Chinese Ministry of Agriculture and Rural Affairs' goal to reduce chemical pesticide use in rice, corn, and wheat by 5% by 2025, with a focus on natural enemies such as insects for pest control, has been a key driver for the segment's dominance. The ministry aims to implement these "green" prevention methods on more than 55% of planted areas by 2025, which continues to strengthen the position of row crops in the biocontrol agents market.

Cash Crops Segment in China Biocontrol Agents Market

The cash crops segment is projected to exhibit the fastest growth in the Chinese biocontrol agents market between 2024 and 2029, with an expected growth rate of approximately 9%. This accelerated growth is primarily driven by the increasing export potential of cash crops like cotton, sugarcane, coffee, tea, oilseeds, and various spices. The segment's growth is further supported by China's position as the world's largest cotton producer, consumer, and importer, with about 300 million people involved in cotton production. The government's initiatives to decrease the overall use of chemical pesticides in cash crops, coupled with the rising trend in organic cultivation area, are expected to fuel the segment's rapid expansion. The increasing focus on sustainable agricultural practices and growing international demand for organic cash crops from China continues to drive the adoption of biocontrol agents in this segment.

Remaining Segments in Crop Type

The horticultural crops segment plays a vital role in the Chinese biocontrol agents market, encompassing a diverse range of fruits and vegetables. This segment includes major fruits like apples, pears, peaches, grapes, and various vegetables such as Chinese cabbage, bok choy, mustard greens, and winter radish. The Ministry of Agriculture and Rural Affairs' initiative to reduce pesticide use in fruits and vegetables by 10% within three years has created significant opportunities for biocontrol agents in this segment. The increasing organic horticultural cultivation area and growing domestic demand for organic fruits and vegetables continue to drive the adoption of biological control solutions in this segment. The use of antagonistic microorganisms is also gaining traction as a sustainable solution in this segment.

China Biocontrol Agents Industry Overview

Top Companies in China Biocontrol Agents Market

The key players in China's biocontrol agents market are demonstrating a strong commitment to innovation and market expansion through various strategic initiatives. Companies are increasingly focusing on research and development activities to develop cutting-edge biocontrol agents solutions, particularly for row crops and cash crops, which dominate the agricultural landscape. The market is witnessing a trend of strategic acquisitions and partnerships to strengthen regional positions and expand product portfolios. Players are investing in technical support teams and distribution networks to provide customized solutions and enhance customer reach. There is also a growing emphasis on developing products specific to different infection stages and crop types, while maintaining a strong focus on sustainability and environmental protection in line with government initiatives to reduce chemical pesticide usage.

Fragmented Market with Growing Consolidation Trends

The Chinese biocontrol agents market exhibits a highly fragmented structure, with the top players holding relatively small market shares while numerous smaller companies operate in specialized segments. The market is characterized by a mix of global players with extensive research capabilities and local companies with strong regional distribution networks. The presence of multiple small and medium-sized enterprises creates intense competition, particularly in specific crop segments and regional markets.

The industry is witnessing increasing consolidation through mergers and acquisitions, as larger companies seek to strengthen their market position and expand their product offerings. Companies are particularly focused on acquiring smaller players with innovative technologies or a strong regional presence. This consolidation trend is driven by the need to achieve economies of scale, enhance research and development capabilities, and expand geographic reach. The market is gradually moving towards a more consolidated structure as companies seek to build comprehensive product portfolios and establish stronger market positions.

Innovation and Distribution Key to Growth

Success in the Chinese biological control agents market increasingly depends on companies' ability to innovate and develop effective distribution networks. Market leaders are focusing on developing specialized products for different crop types and pest varieties, while also investing in research to improve product efficacy and shelf life. Companies are establishing strong technical support teams to provide customized solutions and building relationships with agricultural institutions and farmers to enhance product adoption.

Future growth opportunities lie in developing comprehensive product portfolios that address specific regional needs and crop requirements. Companies need to focus on building strong distribution networks, particularly in major agricultural regions, while also investing in farmer education and awareness programs. The regulatory environment is becoming more supportive of biopesticides and agricultural biologicals, creating opportunities for companies to expand their market presence. Success will also depend on companies' ability to maintain competitive pricing while ensuring product quality and effectiveness, particularly as the market faces competition from traditional chemical pesticides.

China Biocontrol Agents Market Leaders

-

Andermatt Group AG

-

Biobest Group NV

-

Henan Jiyuan Baiyun Industry Co. Ltd

-

Isagro SPA

-

Koppert Biological Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

China Biocontrol Agents Market News

- January 2022: The company announced the merger of Andermatt Biocontrol AG with Andermatt Group AG. After the merger, all companies report directly to Andermatt Group AG, increasing the effectiveness of the management and simplifying the company's structure.

- August 2021: Henan Jiyuan Baiyun Industry Co. Ltd released a new biocontrol agent, Trichogramma chilonis, a parasitic wasp to cover up to 333 hectares of paddy field to control Chilo suppressalis (Rice Stem Borer) in Xinyang of Henan Province, China.

- August 2021: Gowan Company acquired Isagro SpA in 2021. The acquisition helped Isagro reach a wider customer base across the world and leverage more commercial opportunities

Free With This Report

Along with the report, We also offer a comprehensive and exhaustive data pack on Areas under organic cultivation, one of the key trends that affect the market size of agricultural biologicals. This data pack also includes areas under cultivation by crop types, such as Row Crops (Cereals, Pulses, and Oilseeds), Horticultural Crops (Fruits and Vegetables), and Cash Crops in North America, Europe, Asia-Pacific, South America and Africa.

China Biocontrol Agents Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

-

4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Form

- 5.1.1 Macrobials

- 5.1.1.1 By Organism

- 5.1.1.1.1 Entamopathogenic Nematodes

- 5.1.1.1.2 Parasitoids

- 5.1.1.1.3 Predators

- 5.1.2 Microbials

- 5.1.2.1 By Organism

- 5.1.2.1.1 Bacterial Biocontrol Agents

- 5.1.2.1.2 Fungal Biocontrol Agents

- 5.1.2.1.3 Other Microbials

-

5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Andermatt Group AG

- 6.4.2 Biobest Group NV

- 6.4.3 Henan Jiyuan Baiyun Industry Co. Ltd

- 6.4.4 Isagro SPA

- 6.4.5 Koppert Biological Systems Inc.

7. KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- AREA UNDER ORGANIC CULTIVATION IN HECTARES, CHINA, 2017 - 2022

- Figure 2:

- PER CAPITA SPENDING ON ORGANIC PRODUCTS IN USD, CHINA, 2017 - 2022

- Figure 3:

- CHINA BIOCONTROL AGENTS MARKET, VOLUME, GRAM, 2017 - 2029

- Figure 4:

- CHINA BIOCONTROL AGENTS MARKET, VALUE, USD, 2017 - 2029

- Figure 5:

- BIOCONTROL AGENTS CONSUMPTION IN GRAM, CHINA, 2017 - 2029

- Figure 6:

- BIOCONTROL AGENTS CONSUMPTION IN USD, CHINA, 2017 - 2029

- Figure 7:

- BIOCONTROL AGENTS CONSUMPTION VOLUME BY FORM IN %, CHINA, 2017 VS 2023 VS 2029

- Figure 8:

- BIOCONTROL AGENTS CONSUMPTION VALUE BY FORM IN %, CHINA, 2017 VS 2023 VS 2029

- Figure 9:

- MACROBIALS CONSUMPTION IN GRAM, CHINA, 2017 - 2029

- Figure 10:

- MACROBIALS CONSUMPTION IN USD, CHINA, 2017 - 2029

- Figure 11:

- MACROBIALS CONSUMPTION VOLUME BY ORGANISM IN %, CHINA, 2017 VS 2023 VS 2029

- Figure 12:

- MACROBIALS CONSUMPTION VALUE BY ORGANISM IN %, CHINA, 2017 VS 2023 VS 2029

- Figure 13:

- ENTAMOPATHOGENIC NEMATODES CONSUMPTION IN GRAM, CHINA, 2017 - 2029

- Figure 14:

- ENTAMOPATHOGENIC NEMATODES CONSUMPTION IN USD, CHINA, 2017 - 2029

- Figure 15:

- ENTAMOPATHOGENIC NEMATODES CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2022 VS 2029

- Figure 16:

- PARASITOIDS CONSUMPTION IN GRAM, CHINA, 2017 - 2029

- Figure 17:

- PARASITOIDS CONSUMPTION IN USD, CHINA, 2017 - 2029

- Figure 18:

- PARASITOIDS CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2022 VS 2029

- Figure 19:

- PREDATORS CONSUMPTION IN GRAM, CHINA, 2017 - 2029

- Figure 20:

- PREDATORS CONSUMPTION IN USD, CHINA, 2017 - 2029

- Figure 21:

- PREDATORS CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2022 VS 2029

- Figure 22:

- MICROBIALS CONSUMPTION IN GRAM, CHINA, 2017 - 2029

- Figure 23:

- MICROBIALS CONSUMPTION IN USD, CHINA, 2017 - 2029

- Figure 24:

- MICROBIALS CONSUMPTION VOLUME BY ORGANISM IN %, CHINA, 2017 VS 2023 VS 2029

- Figure 25:

- MICROBIALS CONSUMPTION VALUE BY ORGANISM IN %, CHINA, 2017 VS 2023 VS 2029

- Figure 26:

- BACTERIAL BIOCONTROL AGENTS CONSUMPTION IN GRAM, CHINA, 2017 - 2029

- Figure 27:

- BACTERIAL BIOCONTROL AGENTS CONSUMPTION IN USD, CHINA, 2017 - 2029

- Figure 28:

- BACTERIAL BIOCONTROL AGENTS CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2022 VS 2029

- Figure 29:

- FUNGAL BIOCONTROL AGENTS CONSUMPTION IN GRAM, CHINA, 2017 - 2029

- Figure 30:

- FUNGAL BIOCONTROL AGENTS CONSUMPTION IN USD, CHINA, 2017 - 2029

- Figure 31:

- FUNGAL BIOCONTROL AGENTS CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2022 VS 2029

- Figure 32:

- OTHER MICROBIALS CONSUMPTION IN GRAM, CHINA, 2017 - 2029

- Figure 33:

- OTHER MICROBIALS CONSUMPTION IN USD, CHINA, 2017 - 2029

- Figure 34:

- OTHER MICROBIALS CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2022 VS 2029

- Figure 35:

- BIOCONTROL AGENTS CONSUMPTION IN GRAM, CHINA, 2017 - 2029

- Figure 36:

- BIOCONTROL AGENTS CONSUMPTION IN USD, CHINA, 2017 - 2029

- Figure 37:

- BIOCONTROL AGENTS CONSUMPTION VOLUME BY CROP TYPE IN %, CHINA, 2017 VS 2023 VS 2029

- Figure 38:

- BIOCONTROL AGENTS CONSUMPTION VALUE BY CROP TYPE IN %, CHINA, 2017 VS 2023 VS 2029

- Figure 39:

- BIOCONTROL AGENTS CONSUMPTION BY CASH CROPS IN GRAM, CHINA, 2017 - 2029

- Figure 40:

- BIOCONTROL AGENTS CONSUMPTION BY CASH CROPS IN USD, CHINA, 2017 - 2029

- Figure 41:

- BIOCONTROL AGENTS CONSUMPTION VALUE BY FORM IN %, CHINA, 2022 VS 2029

- Figure 42:

- BIOCONTROL AGENTS CONSUMPTION BY HORTICULTURAL CROPS IN GRAM, CHINA, 2017 - 2029

- Figure 43:

- BIOCONTROL AGENTS CONSUMPTION BY HORTICULTURAL CROPS IN USD, CHINA, 2017 - 2029

- Figure 44:

- BIOCONTROL AGENTS CONSUMPTION VALUE BY FORM IN %, CHINA, 2022 VS 2029

- Figure 45:

- BIOCONTROL AGENTS CONSUMPTION BY ROW CROPS IN GRAM, CHINA, 2017 - 2029

- Figure 46:

- BIOCONTROL AGENTS CONSUMPTION BY ROW CROPS IN USD, CHINA, 2017 - 2029

- Figure 47:

- BIOCONTROL AGENTS CONSUMPTION VALUE BY FORM IN %, CHINA, 2022 VS 2029

- Figure 48:

- CHINA BIOCONTROL AGENTS MARKET, MOST ACTIVE COMPANIES, BY NUMBER OF STRATEGIC MOVES, 2017-2022

- Figure 49:

- CHINA BIOCONTROL AGENTS MARKET, MOST ADOPTED STRATEGIES, 2017-2022

- Figure 50:

- CHINA BIOCONTROL AGENTS MARKET SHARE(%), BY MAJOR PLAYERS

China Biocontrol Agents Industry Segmentation

Macrobials, Microbials are covered as segments by Form. Cash Crops, Horticultural Crops, Row Crops are covered as segments by Crop Type.| Form | Macrobials | By Organism | Entamopathogenic Nematodes | |

| Parasitoids | ||||

| Predators | ||||

| Microbials | By Organism | Bacterial Biocontrol Agents | ||

| Fungal Biocontrol Agents | ||||

| Other Microbials | ||||

| Crop Type | Cash Crops | |||

| Horticultural Crops | ||||

| Row Crops | ||||

Need A Different Region or Segment?

Customize Now

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of biocontrol agents applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The Crop Protection function of agirucultural biological include products that prevent or control various biotic and abiotic stress.

- TYPE - Biocontrol agents are the natural predators and parasitoids used to control various pests. Biocontrol agents include both microbials (Microorganisms) and macrobials (Insects).

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.

Get More Details On Research Methodology

Download PDF