Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

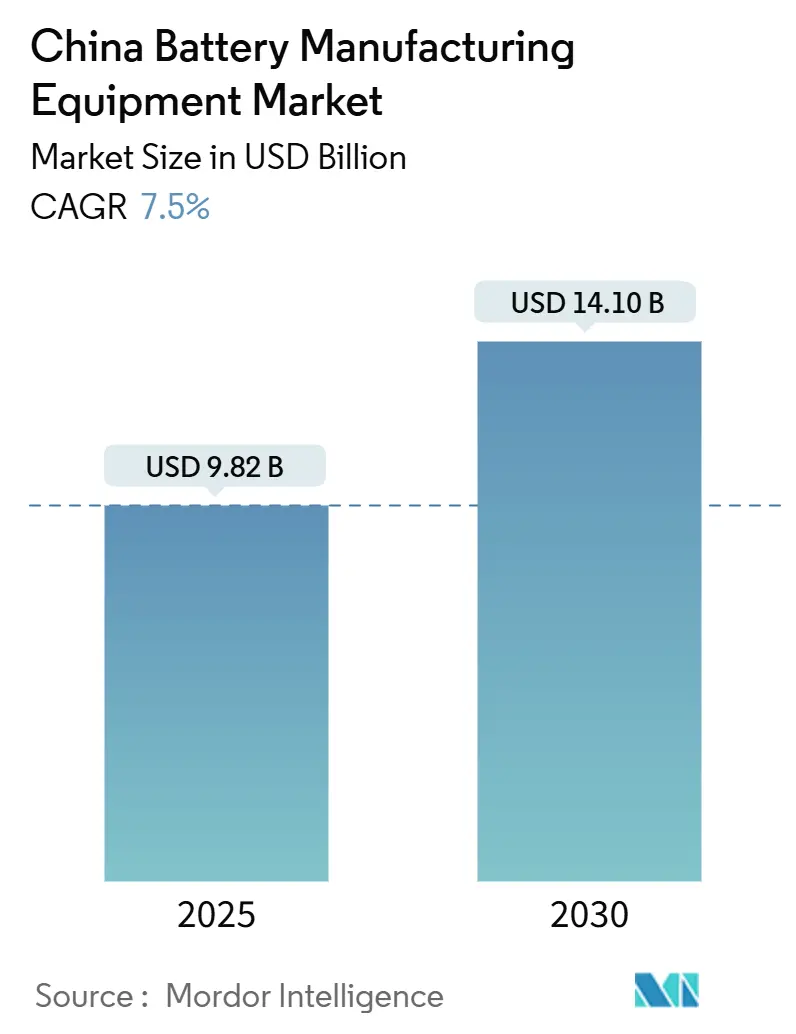

| Market Size (2025) | USD 9.82 Billion |

| Market Size (2030) | USD 14.10 Billion |

| Growth Rate (2025 - 2030) | 7.50% CAGR |

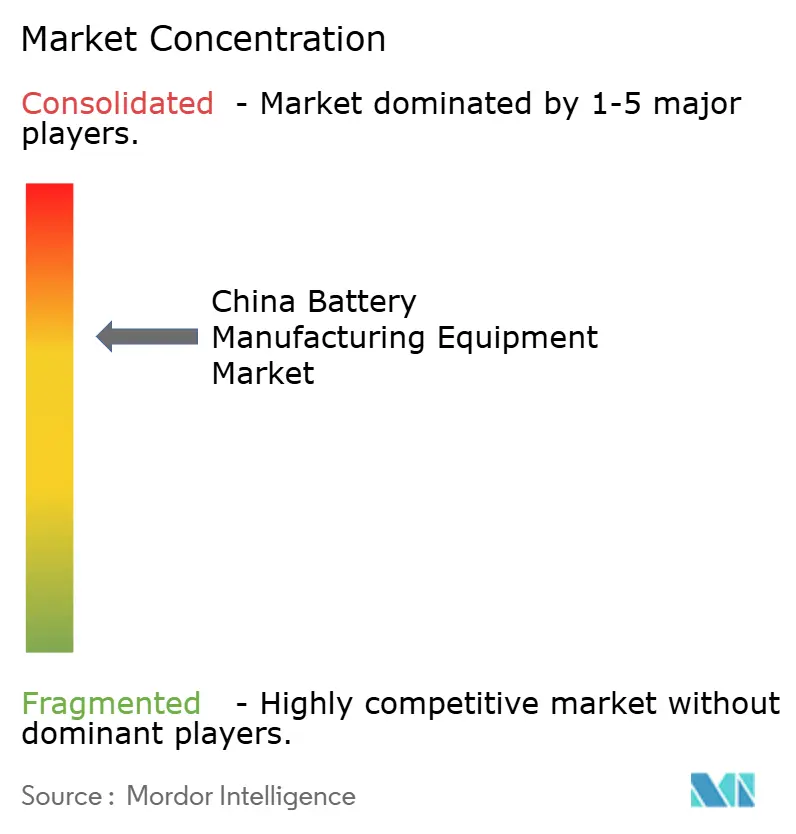

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Battery Manufacturing Equipment Market Analysis by Mordor Intelligence

The China Battery Manufacturing Equipment Market size is estimated at USD 9.82 billion in 2025, and is expected to reach USD 14.10 billion by 2030, at a CAGR of 7.5% during the forecast period (2025-2030).

Demand is shifting from commodity lithium-ion lines toward high-margin solid-state and sodium-ion pilot systems as domestic policy discourages pure capacity expansion and rewards quality upgrades. Firms offering AI-supervised automation, turnkey delivery within 12–18 months, and localized after-sales support continue to win bids from Tier-1 cell makers. Regional equipment clusters in Jiangsu and Guangdong reduce logistics costs, while emerging hubs in Sichuan and Inner Mongolia leverage low-cost renewable energy. Price wars triggered by 2023-2024 overcapacity have compressed gross margins, yet software-bundled “lights-out” lines help vendors defend pricing as clients seek the 2–3 percentage-point yield gains they deliver.

Key Report Takeaways

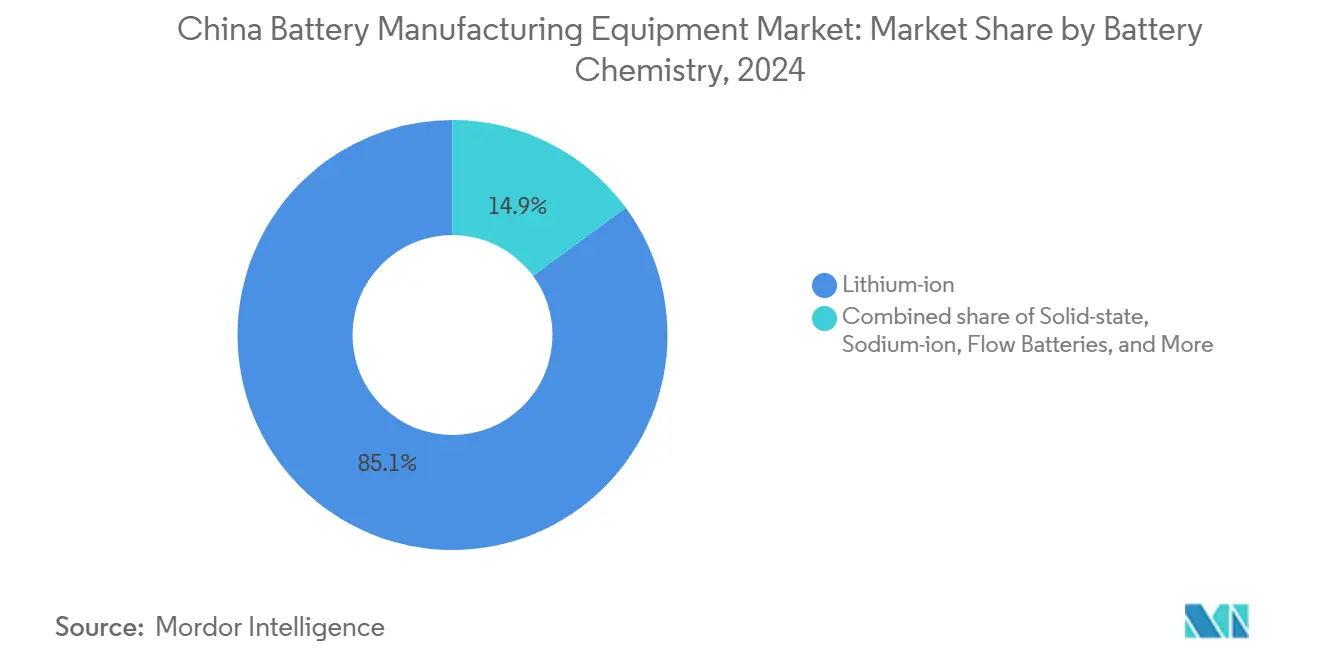

- By battery chemistry, lithium-ion held 85.1% of the China battery manufacturing equipment market share in 2024, whereas solid-state equipment is advancing at a 31.5% CAGR through 2030.

- By machine type, coating and drying systems contributed 20.5% of 2024 revenue, while assembly and handling robots posted the fastest 16.8% CAGR to 2030.

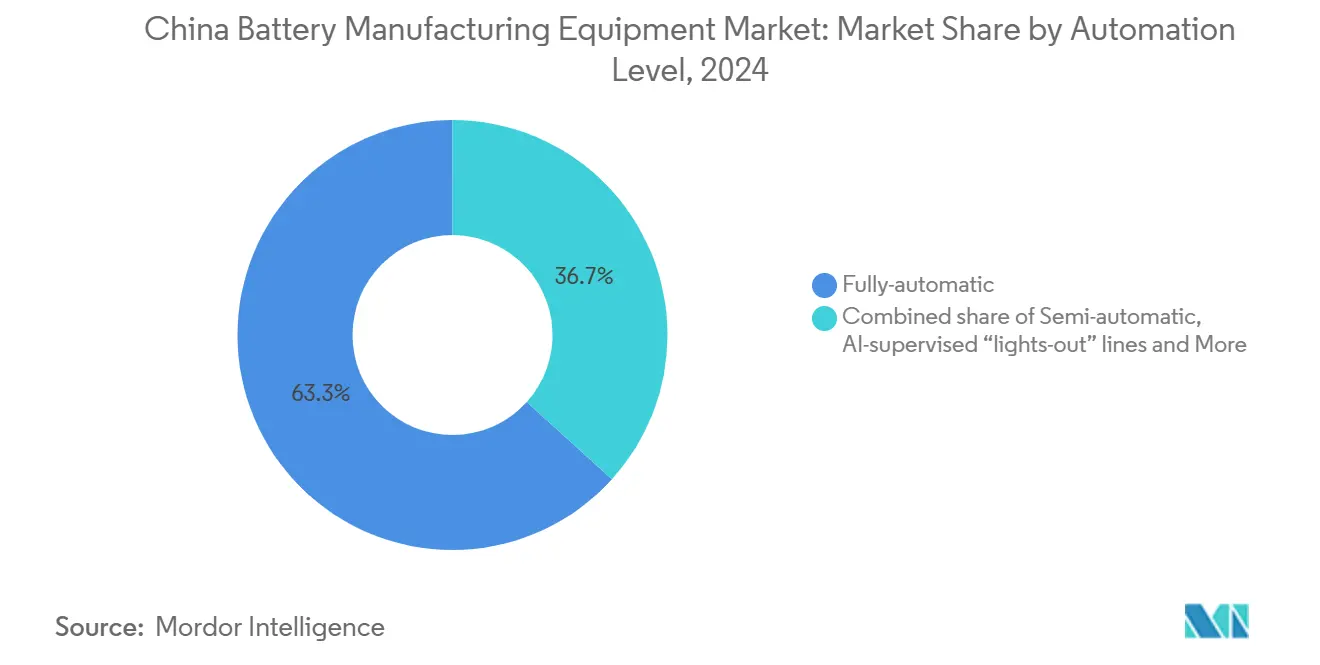

- By automation level, fully automatic lines represented 63.3% of 2024 installations, whereas AI-supervised “lights-out” facilities are scaling at an 18.6% CAGR.

- By end-user, automotive OEMs and Tier-1 suppliers accounted for 59.9% of spending in 2024, while energy storage system integrators registered the highest 19.2% CAGR.

China Battery Manufacturing Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV-led gigafactory expansion | 2.10% | Jiangsu, Guangdong, Sichuan | Short term (≤ 2 years) |

| Government “Made-in-China 2025” automation subsidies | 1.30% | Yangtze River Delta, Pearl River Delta | Medium term (2-4 years) |

| Vertical integration by Tier-1 cell makers | 0.90% | National | Medium term (2-4 years) |

| Solid-state pilot-line investments | 0.70% | Beijing, Shanghai, Shenzhen | Long term (≥ 4 years) |

| AI-driven yield-improvement software bundling | 0.60% | Tier-1 gigafactories nationwide | Short term (≤ 2 years) |

| Surging demand for sodium-ion pilot equipment | 0.50% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid EV-Led Gigafactory Expansion

China produced 9.5 million electric vehicles in 2024, spurring CATL to add 200 GWh of annual capacity by 2026 and BYD to plan 150 GWh over the same horizon. Each gigafactory wave requires USD 3-4 billion of fresh machinery, favoring suppliers able to deliver turnkey lines within 12-18 months. Jiangsu, Guangdong, and Sichuan host dense supply chains, enabling just-in-time installation that entrenches local vendors. Provincial incentives further accelerate deployments by offsetting up to 30% of qualifying equipment costs. As a result, the Chinese battery manufacturing equipment market enjoys near-term order visibility despite nationwide capacity utilization below 50%.

AI-Driven Yield-Improvement Software Bundling

Bundling machine-vision analytics with hardware lifts average selling prices 15-20% and locks customers into multi-year service contracts.[1]Wuxi Lead Intelligent Equipment, “AI Production Line Performance,” leadchina.cn Wuxi Lead reports first-pass yields of 96-97% on AI-supervised lines versus 92-93% on conventional systems, translating into USD 8-10 million in annual savings for a 10 GWh plant. Real-time defect detection shrinks downtime, while data feedback loops inform cell chemistry tweaks, deepening vendor-client ties. Suppliers lacking native software capabilities must acquire startups or license algorithms, both of which dilute margins and reinforce the competitive moat of full-stack integrators.

Surging Demand for Sodium-Ion Pilot Equipment

CATL’s sodium-ion-powered Sehol E10X debuted in 2024, proving commercial viability and prompting BYD to plan 30 GWh of sodium-ion capacity by 2026.[2]CATL, “Annual Report 2024,” catl.com Sodium-ion uses much of the lithium-ion tool set, yet electrolyte filling and sealing require moisture-proof redesigns. Vendors pitch retrofit kits delivering 70-80% output efficiency on repurposed lithium-ion lines, an attractive path for second-tier players short on capex. Sodium-ion is expected to capture 5-8% of China’s cell output by 2030, with equipment sales concentrating in Jiangsu and Guangdong, where brownfield capacity is plentiful.

Solid-State Pilot-Line Investments

The State Council allocated CNY 6 billion (USD 830 million) in 2024 for solid-state R&D, prompting partnerships such as Wuxi Lead-WeLion on dry-electrode pilot lines. Solid-state production demands vacuum deposition, high-pressure calendaring, and solvent-free coating, areas where vendors co-develop bespoke machinery alongside battery chemists. A 31.5% CAGR for solid-state equipment through 2030 presumes 3-5 GWh of pilot capacity online by 2026 and hinges on resolving interfacial resistance that limits cycle life to 500-700 cycles. Equipment makers banking on the transition are embedding upgrade paths into today’s lithium-ion lines, preserving option value for clients wary of stranded assets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Equipment over-capacity after 2023-24 capex spree | –1.2% | Jiangsu, Anhui clusters | Short term (≤ 2 years) |

| Intensifying price-cut wars among Chinese OEMs | –0.8% | Nationwide | Short term (≤ 2 years) |

| Scarcity of senior automation engineers | –0.4% | Tier-1 cities | Medium term (2-4 years) |

| Export-control risks on US/EU process IP | –0.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Equipment Over-Capacity After 2023-24 Capex Spree

Nationwide utilization fell to 47% in 2023 after a two-year installation boom, leaving vendors with idle inventory and forcing discounts that sliced working-capital buffers. Commodity mixers, slitters, and coaters face the deepest glut, while MIIT guidelines now discourage fresh builds unless tied to quality upgrades. Provincial enforcement remains uneven because local authorities still prioritize employment, prolonging oversupply and intensifying competition within the Chinese battery manufacturing equipment market.

Intensifying Price-Cut Wars Among Chinese OEMs

Average selling prices for fully automatic coating lines slid 18-22% between 2023 and 2024 as vendors fought for share. Margins for mid-tier suppliers now hover at 22-25%, down from 30-35% in 2021. Multi-vendor tenders and lengthened payment terms pressure cash flows, limiting R&D budgets for next-gen chemistries and potentially ceding future precision niches back to European or Japanese rivals.

Segment Analysis

By Battery Chemistry: Solid-State Bets Reshape Equipment Pipelines

Solid-state equipment revenues are projected to climb at a 31.5% CAGR, reflecting China’s CNY 6 billion commitment to pilot builds that could reach 3-5 GWh by 2026.[3]Ministry of Industry and Information Technology, “Battery Sector Capacity Utilization Notice,” miit.gov.cn In contrast, lithium-ion retained 85.1% of the Chinese battery manufacturing equipment market share in 2024 due to entrenched EV and consumer electronics demand. Sodium-ion demand is accelerating as retrofit-friendly tooling appeals to budget-conscious producers, while flow batteries gain traction in grid-scale storage. Lead-acid and nickel-based chemistries remain niche but stable, serving industrial and aerospace use cases.

Strong policy backing and co-development alliances between Wuxi Lead, Putailai, and Tier-1 cell makers underpin rapid solid-state adoption. Equipment designs feature solvent-free coating, vacuum deposition, and high-pressure calendaring that few vendors presently master, making early movers well-positioned to capture the next wave of China battery manufacturing equipment market expansion.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Machine Type: Robotics Surge as Labor Costs Climb

Coating and drying systems generated 20.5% of 2024 revenue, reflecting their capital intensity and precision requirements. Assembly and handling robots, however, post the quickest 16.8% CAGR as producers automate labor-heavy stacking and packaging to offset wage inflation. The Chinese battery manufacturing equipment market size for robots, therefore, expands rapidly alongside cell format diversification.

Laser notching and high-precision cutting benefit from large-format cell architectures that demand tighter dimensional control. Formation and testing lines integrate AI diagnostics to catch early-life defects, reducing warranty provisions for EV makers. Meanwhile, recycling and black-mass processing equipment gains policy tailwinds from the 95% material-recovery mandate effective 2028, broadening revenue opportunities beyond primary battery production.

By Automation Level: Lights-Out Lines Command Premium Pricing

Fully automatic lines accounted for 63.3% of 2024 installations, underpinning a mature baseline within the China battery manufacturing equipment market size for factory-wide automation. AI-supervised lights-out facilities, however, are outgrowing legacy systems at an 18.6% CAGR as battery makers chase 2-3 percentage-point yield gains. Subsidies covering up to 30% of qualifying spend further tilt purchasing decisions toward premium configurations.

Vendors with integrated software platforms capture recurring analytics revenue that cushions margin erosion in mechanical hardware. Conversely, semi-automatic and manual options persist among pilot lines where flexibility outweighs throughput. The adoption curve suggests lights-out architecture could equip 40-50% of new gigafactory builds by 2030, raising the overall sophistication of the China battery manufacturing equipment market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: ESS Integrators Drive Next Wave of Demand

Automotive OEMs and Tier-1 suppliers consumed 59.9% of equipment in 2024, yet energy storage system integrators now deliver 19.2% CAGR growth as grid operators embrace 4-8 hour discharge solutions. The China battery manufacturing equipment market size allocated to ESS lines is therefore expanding faster than the automotive portion.

Modular containerized production lines shorten project cycles, letting integrators scale capacity alongside provincial renewable-energy rollouts. Consumer electronics remains a steady but modest buyer, while aerospace and defense procure specialty tooling with higher margins. Diversification across end-users cushions vendors against the cyclical nature of EV demand.

Geography Analysis

Jiangsu and Guangdong together hosted more than 60% of installed equipment value in 2024, leveraging electronics and auto supply-chain density to attract both domestic champions and foreign precision firms. Their port proximity lowers logistics costs and accelerates commissioning, reinforcing their status as core clusters within the China battery manufacturing equipment market.

Sichuan and Inner Mongolia are fast-growing nodes, drawing on low-cost hydropower and vast land availability for gigafactory campuses. Inner Mongolia’s wind-solar mix aligns with policy aimed at pairing renewable generation with storage, driving dedicated flow and sodium-ion line orders. These inland provinces also benefit from central directives that rebalance industrial growth away from coastal hot spots, gradually diffusing equipment demand across a broader geographic footprint.

Secondary hubs such as Anhui and Hubei specialize in AI-oriented control systems and automation subsystems, leveraging lower real estate and labor expenses. Their local governments experiment with innovative subsidy schemes and environmental standards that could inform national policy refinements. The evolving map of installations underscores the geographically diversified yet still cluster-centric nature of the Chinese battery manufacturing equipment market.

Competitive Landscape

Domestic champions Wuxi Lead, Putailai, HangKe, and Shenzhen Yinghe jointly held roughly 60% of 2024 revenue, supported by short lead times and government procurement preferences that stipulate domestic content thresholds. Their tight integration with local clients facilitates rapid customization and robust after-sales support, reinforcing market dominance even amid price pressure.

Foreign incumbents Dürr, Schuler, Manz, and Andritz retain niche strongholds in ultra-precision coaters, laser systems, and vacuum tools where sub-10-micron tolerances remain demanding. Export-control headwinds, however, force them to localize production or establish joint ventures, such as Dürr’s 2025 AI-coater alliance, to preserve addressable share.

White-space in solid-state, sodium-ion, and recycling lines attracts smaller domestic innovators offering modular, rapidly prototypeable machines. Meanwhile, vertical integration by CATL and BYD trims third-party demand for standard lines by an estimated 8-10%. Competitive intensity is therefore expected to consolidate around software-enabled differentiation and next-gen chemistry readiness within the Chinese battery manufacturing equipment market.

China Battery Manufacturing Equipment Industry Leaders

-

Wuxi Lead Intelligent Equipment Co Ltd

-

HangKe Technology

-

Shenzhen Yinghe Technology

-

Putailai (PTL) Intelligent Equipment

-

Shenzhen Colibri Technologies

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Wuxi Lead commissioned an AI-supervised battery assembly line for CATL’s new Sichuan gigafactory.

- September 2025: Dürr and a Chinese automation partner launched a JV to localize AI-driven coating systems.

- August 2025: Putailai secured a USD 120 million solid-state pilot-line contract with WeLion.

- July 2025: BYD broke ground on a 30 GWh sodium-ion plant in Guangdong.

China Battery Manufacturing Equipment Market Report Scope

Battery manufacturing equipment covers machines and equipment used in the production of raw materials, as well as the processing and assembly of batteries. Dosing machines, mixing and coating machines, and so on are necessary for raw material processing, whereas assembling process equipment comprises electrode stacking and cutting machines, heat sealing, and liquid injection machines. For each segment, the market sizing and forecasts have been done based on revenue (USD billion). The Chinese battery manufacturing equipment market report includes:

By Battery Chemistry

| Lithium-ion |

| Solid-state |

| Sodium-ion |

| Lead-acid |

| Nickel-based |

| Flow Batteries (Zn-Br, Vanadium etc.) |

By Machine Type

| Coating and Drying Systems |

| Calendaring Presses |

| Mixing and Homogenizers |

| Slitting Machines |

| Laser Notching and Cutting |

| Electrode Stacking |

| Vacuum Drying and Degassing |

| Electro-lyte Filling |

| Assembly and Handling Robots |

| Formation and Testing Lines |

| Packaging and Sealing |

| Recycling and Black-mass Processing Equipment |

By Automation Level

| Manual/Lab-scale |

| Semi-automatic |

| Fully-automatic |

| AI-supervised “lights-out” lines |

By End-User

| Automotive OEMs and Tier-1s |

| Energy Storage System Integrators |

| Consumer Electronics |

| Industrial and Power Tools |

| Aerospace and Defense |

| Other End Users |

| By Battery Chemistry | Lithium-ion |

| Solid-state | |

| Sodium-ion | |

| Lead-acid | |

| Nickel-based | |

| Flow Batteries (Zn-Br, Vanadium etc.) | |

| By Machine Type | Coating and Drying Systems |

| Calendaring Presses | |

| Mixing and Homogenizers | |

| Slitting Machines | |

| Laser Notching and Cutting | |

| Electrode Stacking | |

| Vacuum Drying and Degassing | |

| Electro-lyte Filling | |

| Assembly and Handling Robots | |

| Formation and Testing Lines | |

| Packaging and Sealing | |

| Recycling and Black-mass Processing Equipment | |

| By Automation Level | Manual/Lab-scale |

| Semi-automatic | |

| Fully-automatic | |

| AI-supervised “lights-out” lines | |

| By End-User | Automotive OEMs and Tier-1s |

| Energy Storage System Integrators | |

| Consumer Electronics | |

| Industrial and Power Tools | |

| Aerospace and Defense | |

| Other End Users |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the China battery manufacturing equipment market?

The sector generated USD 9.82 billion in 2025 and is forecast to reach USD 14.10 billion by 2030.

Which segment is growing fastest within Chinese battery machinery demand?

Solid-state battery equipment posts the quickest 31.5% CAGR through 2030 as pilot lines transition toward commercialization.

Why are AI-supervised “lights-out” lines gaining traction?

They improve first-pass yields by 2–3 percentage points and reduce labor costs by more than 60%, enabling sub-three-year paybacks.

How will sodium-ion chemistry influence equipment procurement?

Retrofit-friendly kits allow existing lithium-ion lines to produce sodium-ion cells at 70-80% efficiency, fueling 19.2% CAGR demand from ESS integrators.

Which provinces dominate China’s battery equipment clusters?

Jiangsu and Guangdong together host more than 60% of installed value, while Sichuan and Inner Mongolia are emerging challengers.

What impact do U.S. and EU export controls have on Chinese equipment vendors?

Restrictions on precision coaters and laser welders add supply-chain risk, prompting accelerated domestic substitution but only shave 0.3 percentage points off forecast CAGR.

Page last updated on: