Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

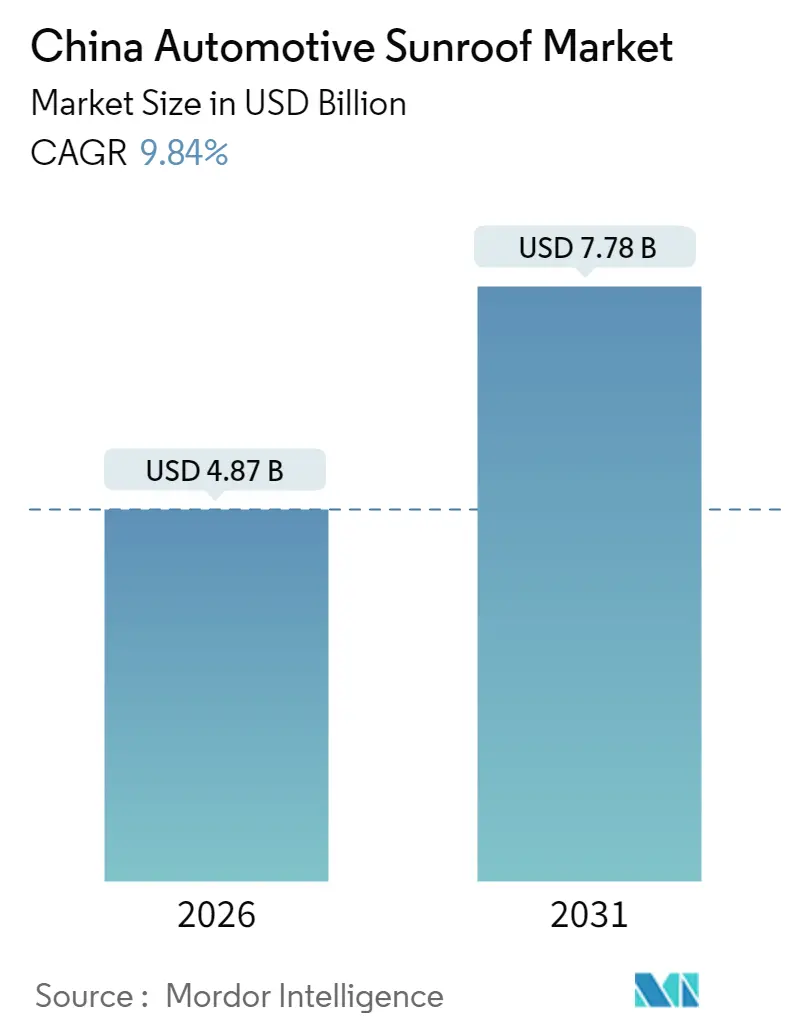

| Market Size (2026) | USD 4.87 Billion |

| Market Size (2031) | USD 7.78 Billion |

| Growth Rate (2026 - 2031) | 9.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Automotive Sunroof Market Analysis by Mordor Intelligence

The Chinese automotive sunroof market is expected to grow from USD 4.43 billion in 2025 to USD 4.87 billion in 2026 and is forecast to reach USD 7.78 billion by 2031 at 9.84% CAGR over 2026-2031. New energy vehicles (NEVs) are being rapidly adopted, SUV sales are strong, and consumers increasingly desire premium cabin features. These trends have driven installation rates to levels significantly surpassing the global average. OEMs are now prominently showcasing large glass roofs as technological highlights. Meanwhile, government dual-credit regulations ensure BEV models remain a focal point. The trade balance has been notably affected by exports, with a substantial number of roof modules sent abroad compared to a minimal quantity imported. This disparity highlights the maturity of the domestic supply chain. A moderate concentration in the market empowers local suppliers to rival global players, capitalizing on vertical integration, cost benefits, and strategies aimed at expanding into Europe.

Key Report Takeaways

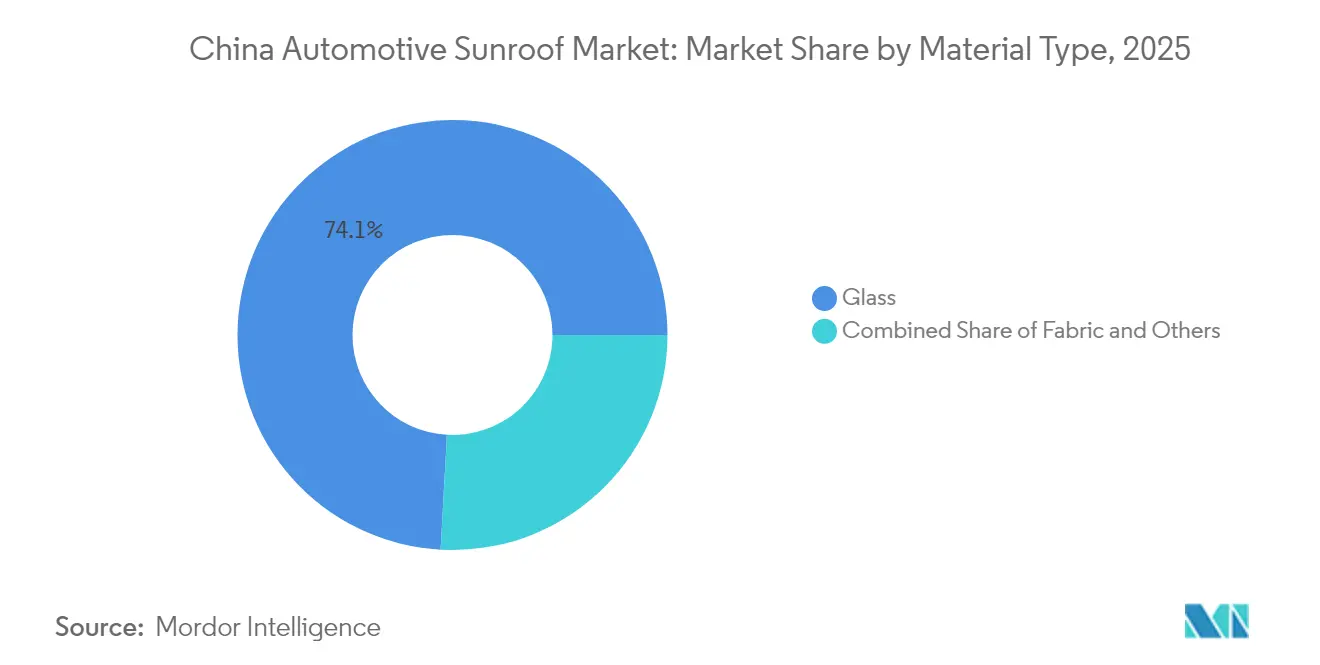

- By material, glass maintained leadership with 74.12% of the Chinese automotive sunroof market share in 2025, while fabric alternatives are projected to climb at a 9.86% CAGR through 2031.

- By sunroof system type, panoramic configurations led with a 56.05% revenue share in 2025; the segment is projected to advance at a 9.89% CAGR to 2031.

- By operation type, electric mechanisms controlled 82.95% of the Chinese automotive sunroof market share in 2025, and it is also expected to record the highest projected CAGR at 9.94% through 2031.

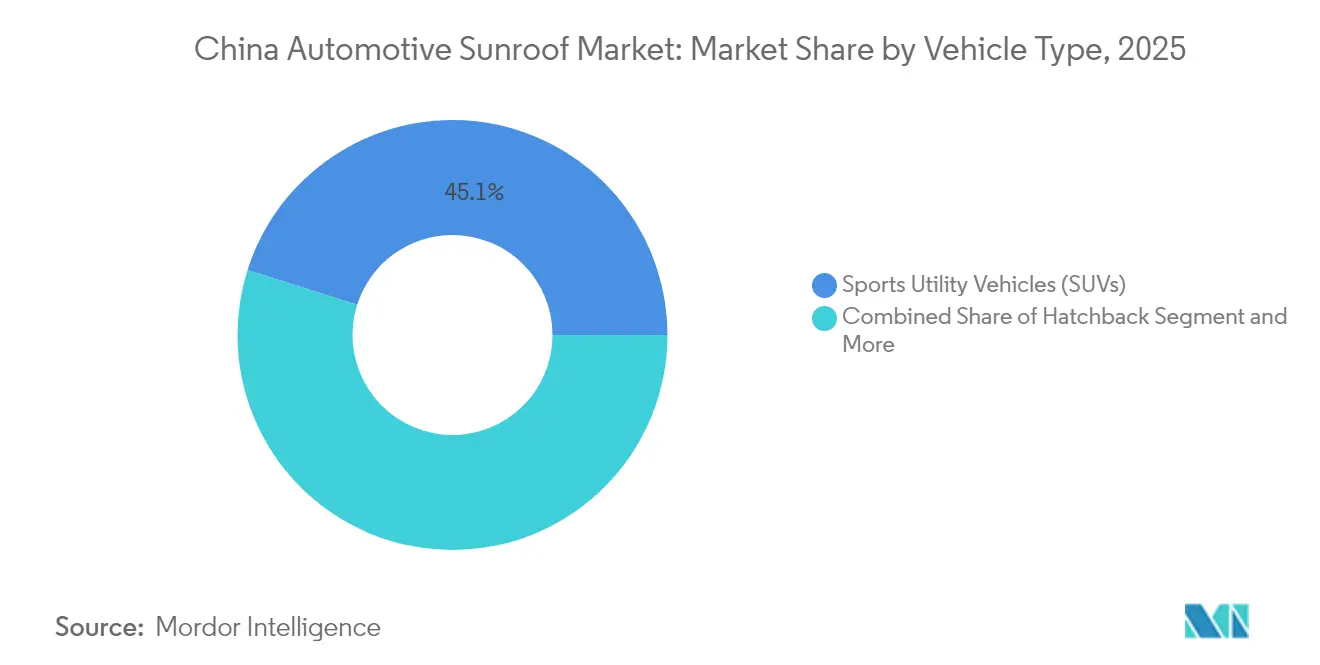

- By vehicle type, sports utility vehicles accounted for 45.12% of the China automotive sunroof market size in 2025 and are set to grow at a 9.91% CAGR between 2026 and 2031.

- By propulsion, internal combustion engine cars held 60.74% of the Chinese automotive sunroof market size in 2025, but BEVs are forecast to register a 9.95% CAGR to the end of the decade.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Automotive Sunroof Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Demand | +2.8% | National, with early gains in Tier-1 cities | Medium term (2-4 years) |

| SUV Body-Style Proliferation | +2.1% | National, strongest in urban markets | Short term (≤ 2 years) |

| Government NEV Incentives | +1.9% | National, with policy concentration in major cities | Long term (≥ 4 years) |

| OEM Differentiation | +1.6% | National, with premium segment focus | Medium term (2-4 years) |

| Low-E & Solar Glass Lowering Cabin Heat Load | +1.2% | National, with southern China emphasis | Long term (≥ 4 years) |

| Tier-2 Vertical Integration Cutting Module Costs | +0.4% | National, with manufacturing hub concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Premium Vehicle Features

A significant majority of EV customers in China are willing to pay additional costs for panoramic roofs. This trend, reflecting rising disposable incomes, is particularly pronounced among younger urban residents who cherish an open-cabin ambiance. Mainstream brands like BYD and Geely are now equipping their volume models with rail-to-rail glass, leading to a notable increase in overall adoption rates when this feature is standard. This shift in consumer behavior, once confined to luxury segments, is now benefiting OEMs with higher margins and ensuring stable volume growth for suppliers in China's sunroof market.

SUV Body-Style Proliferation with High Sunroof Penetration

In 2024, SUVs constitute a significant portion of unit demand and are experiencing robust growth, driven by their roofline design that accommodates larger openings. Premium SUV trims demonstrate much higher penetration rates compared to their sedan counterparts. Domestic manufacturers prioritize panoramic integration during the platform design stage, resulting in cabins that feel more spacious and brighter. A shift in consumer preferences towards family-oriented features continues to support the strong demand in China's automotive sunroof market.

Government New Energy Vehicle (NEV) Incentives Favouring Panoramic Glass Roofs

China’s dual-credit system and purchase subsidies push OEMs to upscale EV interiors and differentiate through visible technology cues. Panoramic roofs, especially those with solar harvesting films, align with national carbon goals and qualify for supplemental local incentives in megacities such as Shanghai and Shenzhen [1]“NEV Dual-Credit Policy 2025 Update,” Ministry of Industry and Information Technology, miit.gov.cn . The resulting pull effect magnifies BEV penetration and cements demand momentum over the long term.

OEM Differentiation Via Comfort and Aesthetics

From NIO to SAIC-Volkswagen, brands rely on panoramic glazing to stand out in crowded segments. Electrochromic dimming, ambient lighting, and integrated solar cells enable premium pricing without requiring redesign of major mechanical systems. The strategy enhances customer satisfaction scores, boosts repeat-purchase intent, and strengthens the company's competitive position in the Chinese automotive sunroof market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sunroof Shatter/Leakage Recalls | -1.8% | National, with premium segment concentration | Short term (≤ 2 years) |

| Weight Penalty Reducing EV Range | -1.2% | National, with BEV segment focus | Medium term (2-4 years) |

| Panoramic Windshield Designs | -0.8% | National, with luxury segment concentration | Medium term (2-4 years) |

| Stricter GB/T Glazing Standards | -0.6% | National, with SME supplier impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sunroof Shatter/Leakage Recalls Harming OEM Trust

High-profile incidents, such as the Polestar 3 glass detachment and drainage failures in FAW-Volkswagen Golf models, have eroded consumer confidence. China’s State Administration for Market Regulation has tightened enforcement of glazing norms under GB 9656-2021, increasing recall risk and warranty costs for automakers [2]“Recall Management Measures for Automobile Products,” State Administration for Market Regulation, samr.gov.cn . Reputational damage can hinder adoption in premium tiers and impact overall growth.

Weight Penalty Reducing EV Range and Fuel Efficiency

As battery energy density improvements plateau, the additional weight from panoramic modules becomes a significant concern. This weight is particularly critical for compact BEVs aimed at city commuters; even a small reduction can diminish the rated range and jeopardize government subsidy eligibility. While lightweight frames and composite panes have been introduced, they still haven't reached economies of scale in China's automotive sunroof sector.

Segment Analysis

By Material Type: Glass Dominance Drives Premium Positioning

Glass commanded a 74.12% share in 2025, anchoring a premium image and benefiting from the rapid adoption of Low-E. This material contributed significantly to the China automotive sunroof market size in 2025, underlining its commercial importance. Fuyao Glass's intensive investment helps meet escalating OEM demand while reducing per-unit costs. Advanced electrochromic sheets, mass-produced through a cooperation between Ambilight and NIO, offer a 40-fold dimming range, reinforcing their leadership in the glass industry.

Fabric roofs cater to cost-sensitive buyers, expanding at a 9.86% CAGR, yet still representing a minority share. They offer lighter weight and lower install cost, making them viable for compact EVs. Composite and hybrid substrates remain exploratory but show promise in integrating solar cells and switchable opacity layers, potentially reshaping future demand curves within the Chinese automotive sunroof market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sunroof System Type: Panoramic Systems Lead Innovation Wave

Panoramic units held a 56.05% share in 2025, translating into over 4 million installations. Their 9.89% CAGR outpaces all other formats as consumers seek expansive views and improved ventilation. New-generation rail-to-rail mechanisms provide nearly full-roof transparency without compromising torsional rigidity, thereby fulfilling the updated GB 26134-2024 crush standards.

Built-in and tilt-n-slide variants remain relevant in sedans and compacts, but their growth is slower. Spoiler types stay niche among sports models. Webasto’s Jiaxing plant manufactures external-sliding solutions tailored for local SUVs. It exports them to Southeast Asia, indicating that Chinese engineering can influence the global design language in the Chinese automotive sunroof market.

By Operation Type: Electric Systems Reflect Electrification Leadership

Electric drives accounted for 82.95% of units shipped in 2025, reflecting consumer expectations for push-button convenience. It is also projected to grow at a robust CAGR of 9.94% by 2031, driven by integrated voice control, smartphone apps, and sensor-based auto-close functions.

Manual operation maintains relevance in low-cost models and aftermarket retrofits, favored by fleet buyers aiming to minimize repair complexity. Safety upgrades—such as pinch protection, rain detection, and emergency override—solidify regulatory compliance and underscore why electric systems will remain dominant despite marginal price premiums.

By Vehicle Type: Sports Utility Vehicles Drive Market Expansion

Sports utility vehicles contributed a 45.12% share in 2025 and are projected to grow at a 9.91% CAGR, resulting in an additional multiple roofs by 2031. Elevated seating and headroom enhance the experiential value of panoramic roofs, making them a staple option for family buyers. Rail-to-rail glazing enhances rear-seat daylight, a selling point emphasized in the marketing for the BYD Song L and Geely Boyue L.

Sedans and hatchbacks account for nearly one-third of demand, but they suffer from spatial constraints that limit the length of their glass. MPVs rely on luxury shuttle use cases and remain stable. Sports coupes and convertibles maintain limited volumes yet showcase cutting-edge integrations, such as electrochromic spoilers, reinforcing brand halo effects within the Chinese automotive sunroof market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Propulsion: Battery Electric Vehicles Emerge as Growth Engine

Internal combustion engine platforms still occupy 60.74% of 2025 installations. However, BEVs represent the fastest-moving cohort with a 9.95% CAGR, adding numerous incremental roofs by 2031. Government mandates targeting two-fifths NEV penetration encourage OEMs to bundle premium features, including full-length glass, to differentiate electric trims.

Solar cell-infused glass facilitates auxiliary charging and heat mitigation, thereby extending the perceived driving range. Hybrid and plug-in hybrid vehicles serve as transitional vehicles, with a moderate annual growth rate of less than one-fifth. As BEV prices fall, their share of the Chinese automotive market will broaden from premium to mass segments, accelerating the trickle-down of technology.

Geography Analysis

Eastern coastal provinces lead in both production and consumption. In Jiangsu, Zhejiang, and Guangdong, companies like Webasto and Fuyao, along with several Tier-2 suppliers, offer OEMs advantages in logistics and reduced freight costs. These provinces boast high sunroof penetration rates in premium vehicles, positioning them as trendsetters in automotive design.

In Tier-1 metros—Beijing, Shanghai, Guangzhou, and Shenzhen—a significant proportion of premium vehicles feature sunroofs, with a growing preference for electrochromic panels. Rising disposable incomes and traffic regulations favoring new energy vehicles (NEVs) pave the way for the swift adoption of solar roofs. Surveys indicate consumers in these cities are willing to pay a premium for electrochromic upgrades, which is notably higher than the national average.

While Tier-2 urban centers like Chengdu, Hangzhou, and Wuhan have comparatively lower sunroof penetration, they're rapidly catching up, bolstered by credit-friendly financing and promotions for NEVs. Although western provinces lag, ongoing infrastructure projects and factory expansions in Chongqing and Xi’an are streamlining supply chains, signaling potential growth for China's automotive sunroof market.

Competitive Landscape

The field shows moderate concentration. Webasto leads, relying on its Jiaxing megaplant and localized R&D to tailor modules for Chinese SUVs. Inalfa, now under BAIC Hainachuan, holds a solid share through JV synergies [3]“Jiaxing Plant Fact Sheet,” Webasto Group, webasto-group.com . In recent times, domestic challenger Yutian Guanjia secured a significant market share, capitalizing on its vertically integrated strengths in stamping, glazing, and electronics to drive down system costs.

Local entrants benefit from cost leadership and rapid iteration cycles. Suppliers like Ambilight and Wicue, specializing in electrochromic and PDLC films, enhance the feature offerings for OEMs. In an effort to counter domestic competition and capitalize on foreign exchange revenues, a majority of leading Chinese roof manufacturers are investing in European sites, underscoring their global ambitions.

Webasto is set to debut cross-strut-free panoramic roofs at Auto Shanghai in the near future, a move that champions full-glass visibility for BEVs. Meanwhile, Fuyao's large-scale capacity expansion not only secures upstream float glass and coatings but also ensures locked-in profit margins. XPeng's patent filings on smart window controls and ADAS sensor mounts underscore the rising significance of software integration in the competitive landscape of China's automotive sunroof sector.

China Automotive Sunroof Industry Leaders

AISIN SEIKI Co. Ltd

Inalfa Roof Systems Group B.V.

Yachiyo Industry Co. Ltd

Inteva Products LLC

Webasto Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Webasto introduced an openable BEV roof module at Auto Shanghai that removes traditional cross struts to maximize transparency and headroom.

- March 2025: Argotec and Miru presented a record-size electrochromic roof module using thermoplastic polyurethane interlayers to prove industrial scalability for large innovative glass applications.

China Automotive Sunroof Market Report Scope

By Material Type

| Glass |

| Fabric |

| Others |

By Sunroof System Type

| Built-in |

| Tilt-n-Slide |

| Panoramic |

| Pop-Up / Spoiler |

By Operation Type

| Electric |

| Manual |

By Vehicle Type

| Hatchback |

| Sedan |

| Sports Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) / Others |

By Vehicle Propulsion

| Internal Combustion Engines (ICEs) |

| Battery Electric Vehicles (BEVs) |

| Hybrid Electric Vehicles (HEVs) |

| Plug-in Hybrid Electric Vehicles (PHEVs) |

| By Material Type | Glass |

| Fabric | |

| Others | |

| By Sunroof System Type | Built-in |

| Tilt-n-Slide | |

| Panoramic | |

| Pop-Up / Spoiler | |

| By Operation Type | Electric |

| Manual | |

| By Vehicle Type | Hatchback |

| Sedan | |

| Sports Utility Vehicles (SUVs) | |

| Multi-Purpose Vehicles (MPVs) / Others | |

| By Vehicle Propulsion | Internal Combustion Engines (ICEs) |

| Battery Electric Vehicles (BEVs) | |

| Hybrid Electric Vehicles (HEVs) | |

| Plug-in Hybrid Electric Vehicles (PHEVs) |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Chinese automotive sunroof market?

The market is valued at USD 4.87 billion in 2026 and is on track to reach USD 7.78 billion by 2031.

How fast is demand for panoramic sunroofs growing?

Panoramic systems are expanding at a 9.89% CAGR through 2031, well above the overall market pace.

Which vehicle category installs sunroofs most frequently?

SUVs lead with a 45.12% share in 2025 and remain the fastest-growing body style at a 9.91% CAGR.

Why are electric sunroof mechanisms so dominant?

Electric drives hold an 82.95% share because Chinese buyers expect automated one-touch operation, and OEMs integrate voice or app control to add value.

How do quality recalls affect market growth?

Recalls tied to glass detachment and leakage can shave up to 1.8 percentage points off forecast CAGR by damaging consumer trust and prompting stricter regulation.

Which companies are gaining share in China’s sunroof space?

Webasto retains leadership, but domestic supplier Yutian Guanjia rose a significant share in 2025 by combining vertical integration with competitive pricing.