China Architectural Coatings Market Analysis

The China Architectural Coatings Market size is estimated at USD 27.12 billion in 2024, and is expected to reach USD 32.68 billion by 2028, growing at a CAGR of 4.77% during the forecast period (2024-2028).

The Chinese architectural coating industry is experiencing a significant transformation driven by stringent environmental regulations and changing consumer preferences. The implementation of strict VOC regulations by the Chinese government in 2020 has fundamentally reshaped the industry landscape, pushing manufacturers to reformulate their products and adopt cleaner technologies. This regulatory framework has accelerated the transition towards eco-friendly paint and coating solutions, particularly in urban development projects. The shift has prompted major industry players to invest heavily in research and development, focusing on innovative low-VOC and zero-VOC formulations that maintain high performance standards while meeting environmental compliance requirements.

The residential construction sector continues to be the primary growth engine for architectural coatings in China, supported by ongoing urbanization initiatives and housing development projects. The sector's dominance is particularly evident in tier-2 and tier-3 cities, where rapid urban expansion and renovation projects drive building coating demand. The growing middle-class population and increasing disposable income levels have led to higher consumer expectations regarding coating quality and performance. This trend has resulted in manufacturers developing premium product lines with enhanced durability, aesthetic appeal, and functional properties such as antibacterial and self-cleaning capabilities.

Waterborne coatings have emerged as the dominant technology segment, reflecting both regulatory compliance and market preference for sustainable solutions. The transition from solventborne to waterborne systems has been particularly pronounced in interior applications, where health and environmental concerns are paramount. Major coating manufacturers have expanded their waterborne product portfolios, introducing advanced formulations that offer improved application properties and durability. The industry has also witnessed significant investments in production capacity for waterborne coatings, with several manufacturers establishing dedicated facilities to meet growing demand.

The resin technology landscape is experiencing notable evolution, with acrylic resins maintaining their position as the preferred choice for waterborne architectural coatings. The superior weather resistance, durability, and versatility of acrylic-based coatings have made them particularly suitable for China's diverse climate conditions. Manufacturers are increasingly focusing on developing hybrid resin systems that combine the benefits of different resin types to achieve optimal performance characteristics. The industry has also seen growing interest in bio-based and renewable resin technologies, although these remain in early stages of commercial adoption. This technological advancement has been accompanied by improvements in application methods and curing technologies, contributing to enhanced coating performance and reduced environmental impact.

China Architectural Coatings Market Trends

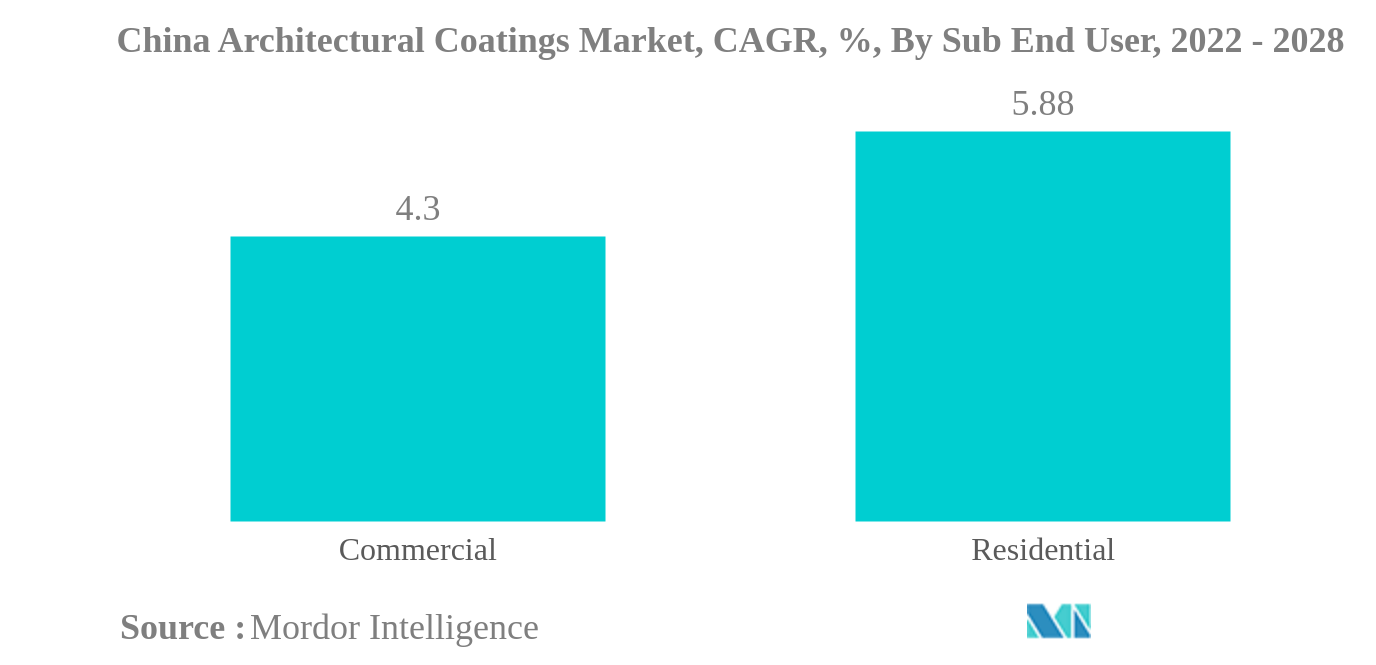

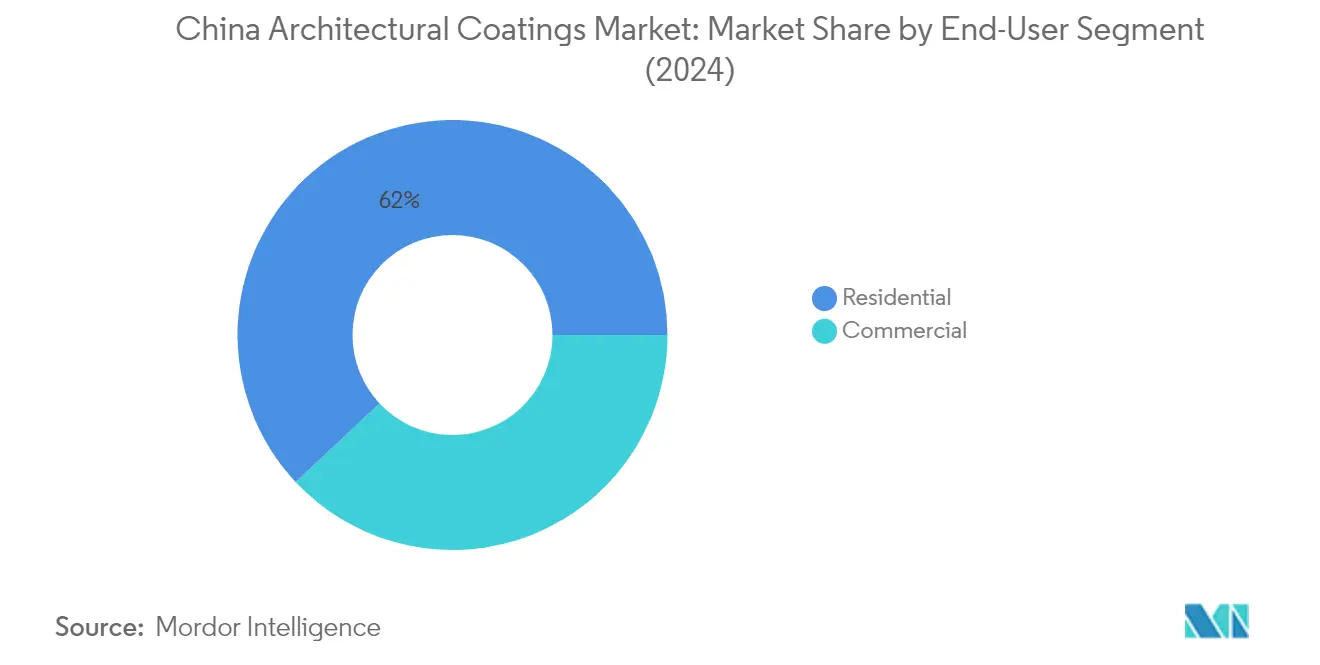

Residential is the largest segment by Sub End User.

- The architectural coating consumption in China peaked in 2017 with an increment of 7.80% from the previous year’s total architectural coating consumption, due to the long-time recovery since 2015, and increase in investment in the residential building by 9.4% y-o-y in 2017. Furthermore, rise in sales of total floor space was also observed in 2017, for instance, floor space of commercial buildings sold was up by 7.7% y-o-y in 2017, while the floor space of residential buildings sold went up by 5.3%.

- The normal new housing starts growth was observed in 2018 and 2019, however from 2018 the downturn was observed due to the over rise in housing prices and declining country’s GDP.The slow growth in the architectural coating consumption in 2020 due to lower new constructions in both residential cand commercial sector owing to the spread of covid-19 in the country was recovered in 2021 due to stronger completion and the rise in Do-it-yourself segment which got popularity in 2020.

- The increase in consumption and sales is expected to grow in forecasted period due to the government initiatives such as revoking filing and mandatory testing requirements of imported paint and coatings in the country from march, 2022 grows the confidence of coating companies in the positive future of architectural coating in the country.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: Sub End User

Residential Segment in China Architectural Coatings Market

The residential segment dominated the China architectural coatings market, holding approximately 62% of the market share in 2024. This dominance is primarily driven by China's massive housing sector and ongoing urbanization initiatives. The segment's strength is reinforced by the government's focus on affordable housing projects and the renovation of existing residential buildings across major cities. The growing middle-class population and increasing disposable income have led to higher investments in home improvement and decoration projects, including house paint and wall paint. Additionally, the trend toward sustainable and eco-friendly homes has boosted the demand for low-VOC and environmentally friendly coating solutions in the residential sector. The segment has also benefited from the rising number of smart cities and modern residential complexes being developed across various provinces in China.

Commercial Segment in China Architectural Coatings Market

The commercial segment is projected to witness significant growth in the China architectural coatings market during the forecast period 2024-2029. This growth is primarily attributed to the rapid expansion of commercial infrastructure, including office buildings, shopping malls, hotels, and institutional facilities. The segment's growth is further supported by China's continued investment in commercial real estate development and the modernization of existing commercial spaces. The increasing adoption of advanced commercial coating technologies in commercial buildings, particularly those focusing on energy efficiency and sustainability, has become a major growth driver. Additionally, stringent building codes and regulations regarding fire safety and environmental protection have led to increased demand for specialized commercial architectural coating solutions.

Segment Analysis: Technology

Waterborne Segment in China Architectural Coatings Market

Waterborne coatings have emerged as the dominant technology segment in China's architectural coatings market, holding approximately 65% of the market share in 2024. This dominance is primarily driven by China's stringent environmental regulations limiting VOC emissions and the government's push toward sustainable coating technologies. The segment's growth is further supported by increasing awareness among consumers about environmental and health impacts, leading to higher adoption in both residential and commercial applications. The superior performance characteristics of waterborne coatings, including better durability, lower odor, and faster drying times, have made them particularly attractive for interior applications, such as wall paint and masonry coating. Additionally, major manufacturers have significantly invested in R&D to improve the performance and application properties of waterborne coatings, making them more competitive with traditional solventborne alternatives.

Solventborne Segment in China Architectural Coatings Market

The solventborne coatings segment continues to maintain its presence in specific applications where high performance and durability are critical requirements. These coatings are particularly valued in exterior applications and harsh environmental conditions where their superior weather resistance and durability properties provide advantages. Despite facing regulatory pressures, solventborne coatings remain essential in certain specialized architectural applications where waterborne alternatives may not yet provide equivalent performance characteristics. Manufacturers are focusing on developing low-VOC solventborne formulations to comply with environmental regulations while maintaining the performance benefits that make these coatings valuable in specific market niches, such as facade coating.

Segment Analysis: Resin

Acrylic Segment in China Architectural Coatings Market

Acrylic resins have established themselves as the dominant segment in China's architectural coatings market, holding approximately 40% market share in 2024. This commanding position can be attributed to acrylic resins' superior weatherability, excellent adhesion properties, and versatile application characteristics. The segment's strength is particularly evident in exterior architectural applications, where durability and UV resistance are crucial. The increasing focus on sustainable building practices in China has further boosted the demand for water-based acrylic coatings, as they align well with stricter environmental regulations. Major coating manufacturers have expanded their acrylic resin-based product portfolios to meet the growing demand from both residential and commercial construction sectors, particularly in tier-1 and tier-2 cities where premium house paint solutions are preferred.

Epoxy Segment in China Architectural Coatings Market

The epoxy resin segment is emerging as the fastest-growing category in China's architectural coatings market, projected to expand significantly during the forecast period 2024-2029. This growth is primarily driven by the increasing adoption of epoxy-based coatings in commercial and industrial flooring applications, where durability and chemical resistance are paramount. The segment's expansion is further supported by the rising demand for high-performance protective coatings in infrastructure projects, including bridges, airports, and commercial complexes. Technological advancements in epoxy formulations, particularly in developing low-VOC and water-based alternatives, have opened new application opportunities and contributed to the segment's rapid growth trajectory. The segment has also benefited from China's ongoing urbanization and infrastructure development initiatives, which require robust construction coating solutions for long-term protection.

Remaining Segments in Resin

The other resin segments, including alkyd, polyester, polyurethane, and various specialty resins, continue to play important roles in China's architectural coatings market. Alkyd resins maintain their significance in traditional architectural applications, particularly in interior wood coatings and metal finishes, though their market share has been impacted by the shift toward water-based technologies. Polyurethane resins are gaining traction in premium architectural applications where superior scratch resistance and flexibility are required. Polyester resins find their niche in specialty architectural applications, particularly in powder coatings for metal substrates. These segments collectively contribute to the market's diversity, offering specific performance characteristics for various architectural coating applications and ensuring manufacturers can meet diverse customer requirements across different price points and performance specifications.

China Architectural Coatings Industry Overview

Top Companies in China Architectural Coatings Market

The Chinese architectural coatings market is characterized by intense competition among both domestic and international players, with companies focusing heavily on product innovation and sustainable solutions. Major market participants have been investing substantially in research and development to develop eco-friendly architectural paint solutions that comply with China's stringent environmental regulations. Companies are expanding their distribution networks, particularly in tier-2 and tier-3 cities, to capture emerging opportunities. Strategic partnerships with real estate developers and construction companies have become increasingly common to secure long-term contracts. Digital transformation initiatives, including e-commerce platforms and digital color matching services, are being implemented to enhance customer experience and operational efficiency. Additionally, manufacturers are investing in automated production facilities and smart manufacturing technologies to improve productivity and maintain quality consistency.

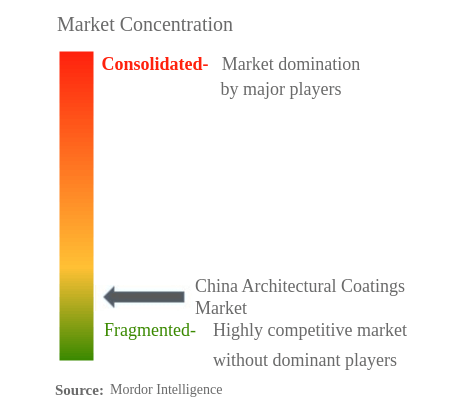

Market Structure Shows Dynamic Competitive Environment

The Chinese architectural coatings market exhibits a moderately consolidated structure, with a mix of large multinational corporations and strong domestic players competing for market share. Local manufacturers have gained significant ground by leveraging their understanding of regional preferences and establishing robust distribution networks in lower-tier cities. The market has witnessed increased consolidation through mergers and acquisitions, as larger players seek to expand their geographical presence and product portfolio.

Recent years have seen a notable shift in competitive dynamics, with domestic players increasingly challenging international brands through improved product quality and competitive pricing strategies. Joint ventures and strategic alliances between local and international companies have become more prevalent, combining global technological expertise with local market knowledge. The market also features numerous regional players who maintain strong positions in specific geographical areas through specialized product offerings and established customer relationships.

Innovation and Sustainability Drive Future Success

Success in the Chinese architectural coatings market increasingly depends on companies' ability to develop innovative, environmentally friendly products while maintaining cost competitiveness. Manufacturers are focusing on developing advanced formulations that offer superior performance characteristics such as better durability, weather resistance, and reduced environmental impact. Building strong relationships with key stakeholders, including property developers, architects, and contractors, has become crucial for maintaining market position. Companies are also investing in technical support services and customer education programs to differentiate themselves in the market.

The future competitive landscape will be shaped by companies' ability to adapt to evolving regulatory requirements, particularly regarding VOC emissions and environmental protection. Investment in digital technologies, including AI-driven color matching systems and online consultation services, will become increasingly important for market success. Companies must also focus on supply chain optimization and raw material sourcing strategies to maintain price competitiveness while ensuring product quality. The ability to offer customized solutions for specific application needs and regional preferences will be a key differentiator in the market. The integration of decorative paint and professional paint solutions will further enhance market offerings, catering to diverse consumer demands.

China Architectural Coatings Market Leaders

-

3TREESGROUP

-

AkzoNobel N.V.

-

CARPOLY

-

Nippon Paint Holdings Co., Ltd.

-

PPG Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

China Architectural Coatings Market News

- April 2022: Nippon Paint Holdings Co., Ltd. has formed a strategic partnership with the Sichuan Academy of Construction Sciences, cooperating in multiple fields to promote the high-quality development of the coating industry.

- January 2022: Nippon Paint Holdings Co., Ltd. proposes new solutions for focusing on dual carbon goals and reducing building energy consumption.

- October 2021: PPG completed the acquisition of Tikkurila a Nordic paint company in June 2021. This acquisition will help PPG grow its Architectural coatings business in EMEA and China in the Nordic region.

China Architectural Coatings Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3. KEY INDUSTRY TRENDS

- 3.1 Floor Area Trends

- 3.2 Regulatory Framework

- 3.3 Value Chain & Distribution Channel Analysis

4. MARKET SEGMENTATION

-

4.1 Sub End User

- 4.1.1 Commercial

- 4.1.2 Residential

-

4.2 Technology

- 4.2.1 Solventborne

- 4.2.2 Waterborne

-

4.3 Resin

- 4.3.1 Acrylic

- 4.3.2 Alkyd

- 4.3.3 Epoxy

- 4.3.4 Polyester

- 4.3.5 Polyurethane

- 4.3.6 Other Resin Types

5. COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

-

5.4 Company Profiles

- 5.4.1 3TREESGROUP

- 5.4.2 AkzoNobel N.V.

- 5.4.3 Axalta Coating Systems

- 5.4.4 CARPOLY

- 5.4.5 DAI NIPPON TORYO CO.,LTD.

- 5.4.6 Flügger group A/S

- 5.4.7 Foshan Caboli Painting Material Co.,Ltd.

- 5.4.8 Guangdong Maydos building materials limited company

- 5.4.9 Hempel A/S

- 5.4.10 Jotun

- 5.4.11 Kansai Paint Co.,Ltd.

- 5.4.12 Nippon Paint Holdings Co., Ltd.

- 5.4.13 PPG Industries, Inc.

- 5.4.14 SKK(S) Pte. Ltd

- 5.4.15 The China Paint Mfg. Co. (1932) Ltd.

- *List Not Exhaustive

6. KEY STRATEGIC QUESTIONS FOR ARCHITECTURAL COATINGS CEOS

7. APPENDIX

-

7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- CHINA MARKET, UNDEFINED YOY GROWTH RATE, 2016 - 2028

- Figure 2:

- CHINA ARCHITECTURAL COATINGS MARKET, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 3:

- CHINA ARCHITECTURAL COATINGS MARKET, VALUE, USD, 2016 - 2028

- Figure 4:

- CHINA ARCHITECTURAL COATINGS MARKET, BY SUB END USER, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 5:

- CHINA ARCHITECTURAL COATINGS MARKET, BY SUB END USER, VALUE, USD, 2016 - 2028

- Figure 6:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY SUB END USER, 2016 - 2028

- Figure 7:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY SUB END USER, 2016 - 2028

- Figure 8:

- CHINA ARCHITECTURAL COATINGS MARKET, BY SUB END USER, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 9:

- CHINA ARCHITECTURAL COATINGS MARKET, BY SUB END USER, VALUE, USD, 2016 - 2028

- Figure 10:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY TECHNOLOGY, 2021 - 2028

- Figure 11:

- CHINA ARCHITECTURAL COATINGS MARKET, BY SUB END USER, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 12:

- CHINA ARCHITECTURAL COATINGS MARKET, BY SUB END USER, VALUE, USD, 2016 - 2028

- Figure 13:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY TECHNOLOGY, 2021 - 2028

- Figure 14:

- CHINA ARCHITECTURAL COATINGS MARKET, BY TECHNOLOGY, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 15:

- CHINA ARCHITECTURAL COATINGS MARKET, BY TECHNOLOGY, VALUE, USD, 2016 - 2028

- Figure 16:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY TECHNOLOGY, 2016 - 2028

- Figure 17:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY TECHNOLOGY, 2016 - 2028

- Figure 18:

- CHINA ARCHITECTURAL COATINGS MARKET, BY TECHNOLOGY, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 19:

- CHINA ARCHITECTURAL COATINGS MARKET, BY TECHNOLOGY, VALUE, USD, 2016 - 2028

- Figure 20:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY SUB END USER, 2021 - 2028

- Figure 21:

- CHINA ARCHITECTURAL COATINGS MARKET, BY TECHNOLOGY, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 22:

- CHINA ARCHITECTURAL COATINGS MARKET, BY TECHNOLOGY, VALUE, USD, 2016 - 2028

- Figure 23:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY SUB END USER, 2021 - 2028

- Figure 24:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 25:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VALUE, USD, 2016 - 2028

- Figure 26:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY RESIN, 2016 - 2028

- Figure 27:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY RESIN, 2016 - 2028

- Figure 28:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 29:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VALUE, USD, 2016 - 2028

- Figure 30:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY SUB END USER, 2021 - 2028

- Figure 31:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 32:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VALUE, USD, 2016 - 2028

- Figure 33:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY SUB END USER, 2021 - 2028

- Figure 34:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 35:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VALUE, USD, 2016 - 2028

- Figure 36:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY SUB END USER, 2021 - 2028

- Figure 37:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 38:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VALUE, USD, 2016 - 2028

- Figure 39:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY SUB END USER, 2021 - 2028

- Figure 40:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 41:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VALUE, USD, 2016 - 2028

- Figure 42:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY SUB END USER, 2021 - 2028

- Figure 43:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VOLUME, KILOGRAMS, 2016 - 2028

- Figure 44:

- CHINA ARCHITECTURAL COATINGS MARKET, BY RESIN, VALUE, USD, 2016 - 2028

- Figure 45:

- CHINA ARCHITECTURAL COATINGS MARKET MARKET, SHARE(%), BY SUB END USER, 2021 - 2028

- Figure 46:

- CHINA ARCHITECTURAL COATINGS MARKET, MOST ACTIVE COMPANIES, BY NUMBER OF STRATEGIC MOVES, 2018 - 2021

- Figure 47:

- CHINA ARCHITECTURAL COATINGS MARKET, MOST ADOPTED STRATEGIES, 2018 - 2021

- Figure 48:

- CHINA ARCHITECTURAL COATINGS MARKET SHARE(%), BY MAJOR PLAYERS, 2021

China Architectural Coatings Industry Segmentation

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.| Sub End User | Commercial |

| Residential | |

| Technology | Solventborne |

| Waterborne | |

| Resin | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types |

Need A Different Region or Segment?

Customize Now

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF