| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| CAGR | 6.20 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Chile In-vitro Diagnostic Market Analysis

The Chile In Vitro Diagnostics Market is expected to register a CAGR of 6.2% during the forecast period.

Chile's healthcare infrastructure is undergoing significant modernization, driven by increasing healthcare expenditure and technological advancements in diagnostic testing services. The country's aging demographic, with 13.1% of the population aged 65 and above in 2023 according to the United Nations Population Fund, has created a sustained demand for advanced medical diagnostics solutions. Healthcare providers are increasingly investing in automated diagnostics systems and digital pathology solutions to improve diagnostic accuracy and operational efficiency. This transformation is particularly evident in the expansion of laboratory diagnostics capabilities across both public and private healthcare facilities.

The clinical laboratory network in Chile continues to expand, with significant developments in both urban and rural areas to improve healthcare accessibility. This expansion is exemplified by RedSalud's growth in 2023, operating 30 ambulatory clinics, nine hospitals, and more than 40 dental clinics across the country. Healthcare facilities are increasingly adopting integrated laboratory information systems and automated workflows to handle growing test volumes efficiently. The modernization of laboratory infrastructure has also facilitated the implementation of quality management systems and standardized laboratory testing protocols across healthcare networks.

Technological innovation is reshaping the diagnostic landscape in Chile, with a growing emphasis on precision medicine and personalized diagnostics. In 2023, research scientists at the Technology Transfer Unit of the University of La Frontera developed innovative in vitro diagnostics tests for faster and less invasive detection of various conditions. Healthcare providers are increasingly adopting molecular diagnostic platforms and next-generation sequencing technologies, enabling more accurate and comprehensive diagnostic capabilities. This technological advancement has particularly benefited specialized testing areas such as oncology, where approximately 1,300 new cases of leukemia are diagnosed annually.

The market is witnessing significant consolidation through strategic partnerships and collaborations between local and international players. In October 2023, Cleveland Clinic and RedSalud formed a joint advisory council to enhance operational excellence and patient experience in diagnostic testing services. Healthcare providers are increasingly focusing on establishing centers of excellence and specialized diagnostic facilities. The trend toward public-private partnerships has accelerated, with government initiatives supporting the modernization of public hospital laboratories and improving access to advanced in vitro diagnostics services across different regions of Chile.

Chile In-vitro Diagnostic Market Trends

Rising Prevalence of Chronic and Infectious Diseases

The increasing burden of chronic and infectious diseases in Chile has become a significant driver for the diagnostic testing market. According to the Chilean health authorities in 2023, approximately 84,000 people were estimated to be living with HIV in the country, with 5,401 new HIV infections confirmed in 2022. The highest rates of infections were detected in the regions of Arica and Parinacota, Tarapacá, and Antofagasta. Additionally, according to the International Diabetes Federation (IDF) data from 2021, the population suffering from diabetes was 1,741.7 per 1,000 population, with projections indicating an increase to 1,965.2 per 1,000 people by 2030 and 2,215.7 per 1,000 people by 2045.

The burden of respiratory infections and non-communicable diseases further emphasizes the growing need for diagnostic testing solutions. According to a May 2023 update by MINSAL, respiratory infection cases increased by 100% compared to 2022, with 1,603 people currently hospitalized in Chile, of whom 738 tested positive for respiratory viruses. Furthermore, a study published in BMC Public Health in July 2023 estimated that approximately 669,000 cases of non-communicable chronic diseases, including coronary heart disease, stroke, hypertensive heart disease, type 2 diabetes, chronic kidney disease, cirrhosis, and various types of cancers, are expected to occur from 2020 to 2030 in Chile. This significant disease burden has created an urgent need for effective diagnostic testing solutions, driving the demand for in-vitro diagnostics in the country.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Use of Point-of-Care Diagnostics

The adoption of point-of-care diagnostics has seen substantial growth in Chile, driven by recent advances in biosensors, microfluidic technologies, bioanalytical platforms, assay formats, lab-on-a-chip technologies, and complementary technologies. According to an article published in the Virus Journal in January 2021, molecular diagnostics techniques have become widespread in large public and private medical centers in Chile. This expansion has led to increased demand for point-of-care diagnostics for quick and early detection of diseases. The advantages of early detection, coupled with supportive government legislation for testing, have facilitated the widespread adoption of rapid diagnostics across healthcare facilities.

The market has been further strengthened by strategic partnerships and distribution agreements among key industry players. In November 2022, Sense Biodetection entered into a strategic partnership with Biotecom for the non-exclusive distribution of Sense's Veros instrument-free, point-of-care molecular testing platform in Chile. The platform can provide results in 15 minutes using proprietary rapid molecular amplification technology, improving access to quick, highly accurate rapid diagnostics. Additionally, in October 2022, Nanomix Corporation signed a distribution agreement with Dialcinic SpA to distribute the Nanomix eLab system in Chile. This mobile, hand-held immunoassay and chemistry diagnostic device is designed for rapid point-of-care testing, demonstrating the industry's commitment to expanding access to quick and accurate diagnostic kit solutions throughout the country.

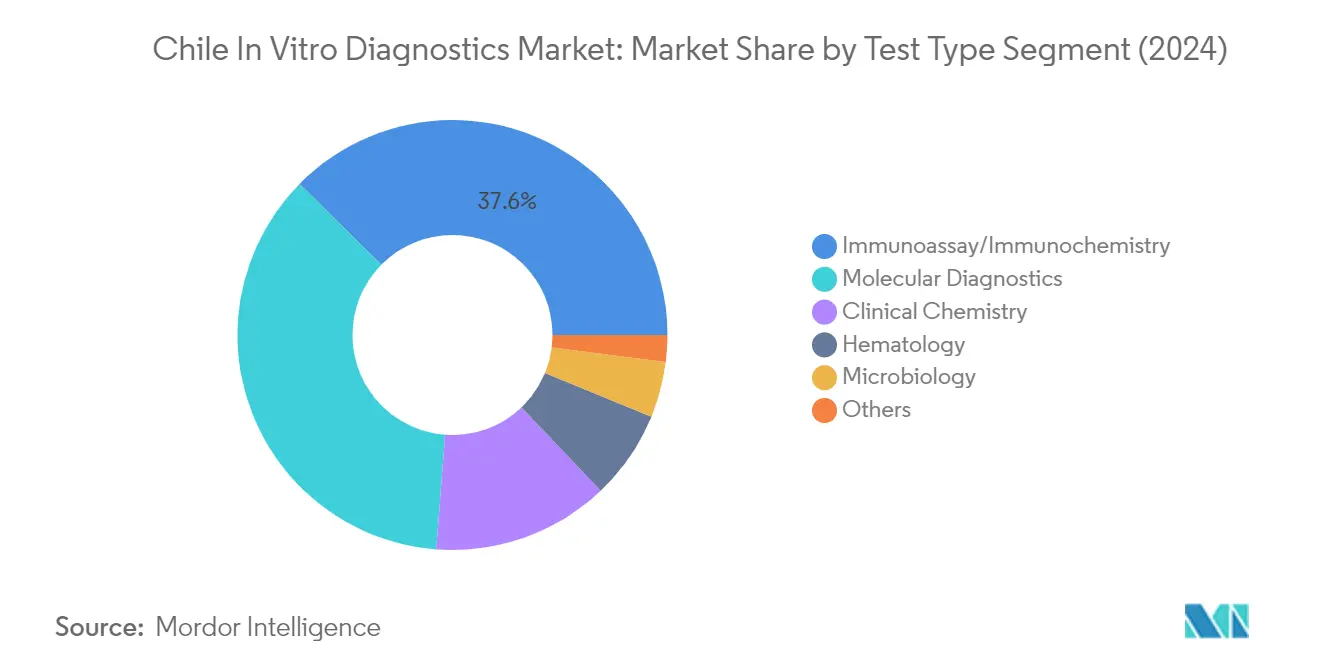

Segment Analysis: By Test Type

Immunoassay/Immunochemistry Segment in Chile In Vitro Diagnostics Market

The immunodiagnostics segment dominates the Chile In Vitro Diagnostics market, holding approximately 38% market share in 2024. This significant market position is driven by the increasing prevalence of chronic diseases like cancer and infectious diseases in Chile, which require accurate and reliable diagnostic solutions. The segment's leadership is further strengthened by the growing adoption of point-of-care immunodiagnostics across healthcare facilities and the continuous technological advancements in immunodiagnostic platforms. Strategic activities by key market players, such as Nanomix Inc.'s distribution agreement with Chilean medical distributor Diaclinic for their mobile immunoassay system, have also contributed to maintaining this segment's dominant position in the market.

Clinical Chemistry Segment in Chile In Vitro Diagnostics Market

The clinical chemistry segment is emerging as the fastest-growing segment in the Chile In Vitro Diagnostics market, projected to grow at approximately 8% during 2024-2029. This robust growth is primarily attributed to the increasing prevalence of diabetes and other chronic disorders requiring regular monitoring through clinical chemistry tests. The segment's growth is further fueled by the rising focus on preventive healthcare and a growing health-conscious population in Chile, driving the demand for regular check-ups and diagnostic tests. The expansion of healthcare infrastructure and increasing adoption of automated diagnostic analyzers across laboratories are also contributing factors to this segment's rapid growth trajectory.

Remaining Segments in Test Type Market Segmentation

The other segments in the Chile In Vitro Diagnostics market include molecular diagnostics, Hematology, Microbiology, Urinalysis, Histology, and Nucleic Acid Testing, each serving specific diagnostic needs. Molecular diagnostics maintains a strong presence due to its crucial role in infectious disease detection and genetic testing. The Hematology segment continues to be vital for blood disorder diagnostics, while Microbiology serves essential needs in infection detection and antibiotic resistance testing. Urinalysis, Histology, and Nucleic Acid Testing segments, though smaller in market share, play critical roles in specific diagnostic applications, contributing to the overall comprehensive diagnostic capabilities of the Chilean healthcare system.

Segment Analysis: By Product

Reagents Segment in Chile In Vitro Diagnostics Market

The diagnostic reagent segment dominates the Chile in vitro diagnostics market, commanding approximately 66% market share in 2024, driven by their essential role as common consumables in various diagnostic assays and confirmatory tests. These diagnostic reagents involve the supply of crucial chemical substances used in diagnostic tests and play a pivotal role in detecting and analyzing biological markers, facilitating accurate disease diagnosis and monitoring within the healthcare sector. The segment's prominence is further reinforced by the increasing prevalence of diseases in Chile, which drives the demand for diagnostic testing, as reagents are essential components for accurate and reliable in vitro diagnostics. The segment is also experiencing the highest growth rate of around 5% for the forecast period 2024-2029, attributed to growing awareness about the importance of early disease detection and the implementation of screening programs that contribute to an increased volume of diagnostic tests in the country.

Instruments Segment in Chile In Vitro Diagnostics Market

The diagnostic instrument segment represents a crucial component of the Chile in vitro diagnostics market, encompassing medical devices used to perform tests for detecting diseases and infections by examining specimens of bodily substances. These instruments deliver accurate, reliable screening and diagnostic testing, with the capability to run multiple assays simultaneously and perform various clinical research applications. The segment's growth is primarily driven by the rising incidence of diseases that necessitate enhanced diagnostic capabilities, leading to increased demand for advanced diagnostic instruments in Chile. The expansion of this segment is further supported by strategic initiatives taken by market players, such as partnerships and collaborations to increase the availability of advanced instruments in the country.

Remaining Segments in Product Segmentation

The other products segment in the Chile in vitro diagnostics market includes software and services associated with laboratory diagnostics. This segment plays a vital role in managing and integrating complex diagnostic data, supporting healthcare professionals in making informed decisions. The increasing volume of diagnostic data mandates robust software solutions for effective management and integration, while the rise in overall health expenditures often increases investments in healthcare infrastructure, including diagnostic facilities. The segment's growth is further driven by the adoption of advanced in-vitro diagnostics software to enhance the efficiency and accuracy of diagnostic processes.

Segment Analysis: By Usability

Reusable IVD Devices Segment in Chile In Vitro Diagnostics Market

The reusable IVD devices segment continues to dominate the Chile in vitro diagnostics market, holding approximately 70% market share in 2024. This significant market position can be attributed to the increasing advantages offered by reusable in vitro diagnostics compared to disposable IVDs, particularly in terms of cost-effectiveness and environmental sustainability. The segment's growth is driven by innovations like reusable glucose sensors that provide low-cost testing solutions for diagnosing and monitoring diabetes in clinics. Additionally, these devices undergo rigorous reprocessing procedures, including cleaning, disinfection, and sterilization, ensuring their safety and effectiveness for multiple uses. The segment is projected to maintain its leading position through 2024-2029, with an expected growth rate of around 5% during this period, supported by continuous technological advancements and increasing adoption across healthcare facilities. The expansion is further bolstered by the rising demand for automated analysis systems in laboratories and the growing preference for sustainable healthcare solutions.

Disposable IVD Devices Segment in Chile In Vitro Diagnostics Market

The disposable IVD devices segment plays a crucial role in the Chilean market, particularly in applications requiring single-use diagnostic tools to prevent cross-contamination and ensure accurate results. These devices are extensively used in diagnostic testing of infectious diseases, where disposing of the device after use significantly reduces the risk of infection transmission. The World Health Organization's (WHO) Essential Diagnostics List (EDL) continues to recognize the importance of disposable IVDs in advancing universal health coverage and addressing health emergencies. The segment's growth is supported by the increasing demand for diagnostic kits, assays, and single-use medical devices in oncology, with various products listed under the WHO's priority devices for cancer management. Furthermore, the segment benefits from infection prevention and control (IPC) guidelines, which emphasize the importance of disposable devices in maintaining sterility and safety during diagnostic procedures. The implementation of these guidelines particularly impacts healthcare delivery in Chile, where maintaining high hygiene standards is crucial for preventing secondary infections.

Segment Analysis: By Application

Infectious Disease Segment in Chile In Vitro Diagnostics Market

The infectious disease segment continues to dominate the Chile in vitro diagnostics market, holding approximately 66% of the market share in 2024. This substantial market share is primarily driven by the increasing burden of infectious diseases in Chile, particularly HIV, tuberculosis, and respiratory infections. According to recent health authority reports, around 84,000 people were estimated to be living with HIV in Chile in 2023, while tuberculosis cases reached 13 per 100,000 population. The segment's growth is further supported by the country's robust testing infrastructure and the increasing adoption of molecular diagnostic techniques in large public and private medical centers. Additionally, the Chilean government's emphasis on facilitating testing rates and implementing efforts to manage infectious diseases has significantly contributed to the segment's dominance in the market.

Cancer/Oncology Segment in Chile In Vitro Diagnostics Market

The cancer/oncology segment is projected to witness the highest growth rate of approximately 7% during the forecast period 2024-2029. This accelerated growth is attributed to the rising cancer incidence in Chile, with projections indicating 74,973 new cases by 2030, representing a 38.3% increase from 2020. The segment's growth is further bolstered by Chile's National Cancer Control Plan, which has set 15 objectives to promote primary prevention through cancer risk control and improve early detection. The increasing adoption of advanced diagnostic technologies, such as next-generation sequencing (NGS) and molecular testing, is also driving the segment's growth. Strategic collaborations between major market players, such as Veracyte Inc. and Illumina Inc., for developing and offering high-performing molecular tests are expected to further accelerate the segment's expansion in the coming years.

Remaining Segments in Application Market Segmentation

The other significant segments in the Chile in vitro diagnostics market include diabetes, cardiology, and autoimmune diseases. The diabetes segment plays a crucial role in monitoring and managing the country's growing diabetic population through various diagnostic tools such as glucose meters and glycohemoglobin test kits. The cardiology segment focuses on diagnostic solutions for cardiovascular diseases, particularly benefiting from the country's Garantías Explícitas en Salud program, which has improved access to cardiac diagnostic services. The autoimmune disease segment continues to evolve with the introduction of advanced diagnostic technologies and increased focus on early detection. These segments collectively contribute to the market's diversity and comprehensive diagnostic capabilities, addressing various healthcare needs across the Chilean population.

Segment Analysis: By End User

Hospitals and Clinics Segment in Chile In Vitro Diagnostics Market

The hospitals and clinics segment dominates the Chile in vitro diagnostics market, holding approximately 51% of the market share in 2024. This significant market position is attributed to the comprehensive medical care infrastructure and advanced diagnostic capabilities present in Chilean healthcare facilities. The segment's dominance is further strengthened by strategic partnerships and expansions, such as the collaboration between Cleveland Clinic and RedSalud, Chile's largest private healthcare network with 30 ambulatory clinics, nine hospitals, and more than 40 dental clinics. These facilities continue to drive the demand for in vitro diagnostic solutions by offering a wide range of diagnostic services, from routine check-ups to specialized testing. The segment's strong position is also supported by the increasing prevalence of infectious diseases and chronic conditions in Chile, necessitating robust diagnostic capabilities within hospital settings.

Diagnostic Laboratories Segment in Chile In Vitro Diagnostics Market

The diagnostic laboratories segment is emerging as the fastest-growing segment in the Chile in vitro diagnostics market, projected to grow at approximately 5.5% during 2024-2029. This growth is primarily driven by the increasing initiatives and government guidelines promoting laboratory diagnostics, including the World Health Organization's (WHO) essential diagnostics list (EDL) implementation. The segment's expansion is further supported by the rising volume of diagnostic tests performed in specialized laboratory facilities, particularly for infectious diseases and chronic conditions. The growth is also bolstered by partnerships between laboratories and international organizations, such as WHO's COVID-19 Technology Access Pool (C-TAP) collaboration with Universidad de Chile for diagnostic systems. Additionally, the increasing adoption of advanced diagnostic technologies and automation in laboratory settings is contributing to the segment's rapid growth trajectory.

Remaining Segments in End User Segmentation

The other end users segment, which includes in-home care, ambulatory care services, blood banks, schools, academic institutions, and research institutions, plays a vital role in the Chile in vitro diagnostics market. This segment is particularly significant in advancing research and development activities, with academic and research institutes conducting in-depth studies to uncover disease complexities using various diagnostic equipment and reagents. The home care segment within this category is gaining prominence due to the increasing inclination toward home healthcare and the rising demand for rapid tests among home care users. The segment is further strengthened by ongoing research initiatives and technological advancements, such as the development of innovative diagnostic tests by research institutions in Chile.

Chile In Vitro Diagnostics Market Geography Segment Analysis

In-Vitro Diagnostics Market in Chile

Chile represents approximately 5% of the Latin American in vitro diagnostics market, establishing itself as a significant player in the region. The country's market is characterized by a robust healthcare infrastructure and increasing adoption of advanced diagnostic testing technologies. The government's emphasis on improving healthcare accessibility has led to greater integration of in vitro diagnostic solutions across both public and private healthcare sectors. The market has seen particular strength in areas such as molecular diagnostics and immunoassays, driven by the growing prevalence of chronic and infectious diseases. The country's strategic position in Latin America, coupled with its stable regulatory environment, has attracted significant investments from major global diagnostic equipment companies, fostering innovation and market expansion.

In-Vitro Diagnostics Market in Brazil

Brazil has emerged as a pivotal market for in vitro diagnostics in Latin America, demonstrating robust growth potential through 2029. The country's large population base and expanding healthcare infrastructure have created substantial opportunities for market expansion. Brazilian healthcare facilities have shown increasing adoption of automated medical testing systems, particularly in major urban centers. The country's commitment to modernizing its healthcare system has led to significant investments in laboratory diagnostics infrastructure. Local manufacturing capabilities, combined with strong distribution networks, have enhanced market accessibility. The presence of both domestic and international players has created a competitive landscape that drives innovation and market development. Brazil's focus on preventive healthcare has further accelerated the adoption of advanced clinical testing solutions.

In-Vitro Diagnostics Market in Mexico

Mexico's in vitro diagnostics market has demonstrated remarkable resilience and growth potential, supported by ongoing healthcare reforms and increasing private sector participation. The country's strategic geographical location has facilitated strong trade relationships with North American diagnostic testing manufacturers, enabling easier access to advanced technologies. Mexican healthcare facilities have shown growing interest in point-of-care testing solutions, particularly in remote and underserved areas. The country's expanding middle class has driven increased demand for preventive healthcare services, including medical testing. Public-private partnerships have played a crucial role in expanding diagnostic capabilities across the country. The market has seen particular growth in areas such as diabetes monitoring and infectious disease testing.

In-Vitro Diagnostics Market in Argentina

Argentina has established itself as a key player in the Latin American in vitro diagnostics landscape, with a strong focus on technological advancement and healthcare accessibility. The country's well-developed healthcare system has facilitated the adoption of sophisticated clinical testing technologies across both public and private sectors. Argentine medical professionals have shown particular interest in molecular diagnostic solutions and automated testing platforms. The country's robust research and development infrastructure has supported local innovation in diagnostic technologies. Healthcare providers have increasingly emphasized preventive care, driving demand for routine diagnostic testing. The market has benefited from strong professional training programs and technical expertise in laboratory diagnostics.

In-Vitro Diagnostics Market in Other Countries

The in vitro diagnostics market across other Latin American countries, including Colombia, Peru, Ecuador, and Uruguay, shows varying degrees of development and potential. These markets are characterized by increasing healthcare awareness and growing demand for advanced diagnostic solutions. While smaller in scale, these countries have demonstrated commitment to improving their healthcare infrastructure and diagnostic capabilities. Regional cooperation and knowledge sharing have helped accelerate market development in these nations. The presence of international diagnostic companies has facilitated technology transfer and market expansion. These countries have shown particular interest in cost-effective diagnostic solutions that can serve their diverse population needs. Local healthcare policies and regulations continue to evolve to support market growth and ensure quality standards in diagnostic testing.

Get Analysis on Important Geographic Markets

Download PDF

Chile In-vitro Diagnostic Industry Overview

Top Companies in Chile In Vitro Diagnostics Market

The Chile in vitro diagnostics market features prominent global players like Abbott, Bio-Rad Laboratories, Roche, Siemens Healthcare, and bioMérieux leading the competitive landscape. These companies are driving market growth through continuous product innovation, particularly in molecular diagnostics and point-of-care testing solutions. Strategic partnerships with local distributors and healthcare providers have enhanced market penetration and service delivery capabilities. Companies are increasingly focusing on expanding their test menu offerings while improving automation and connectivity features of their diagnostic equipment platforms. The competitive dynamics are further shaped by investments in local infrastructure, technical support networks, and customer training programs. Market leaders are also emphasizing the development of integrated diagnostic device solutions that combine multiple testing capabilities on single platforms, while simultaneously working to optimize their supply chain operations for better market responsiveness.

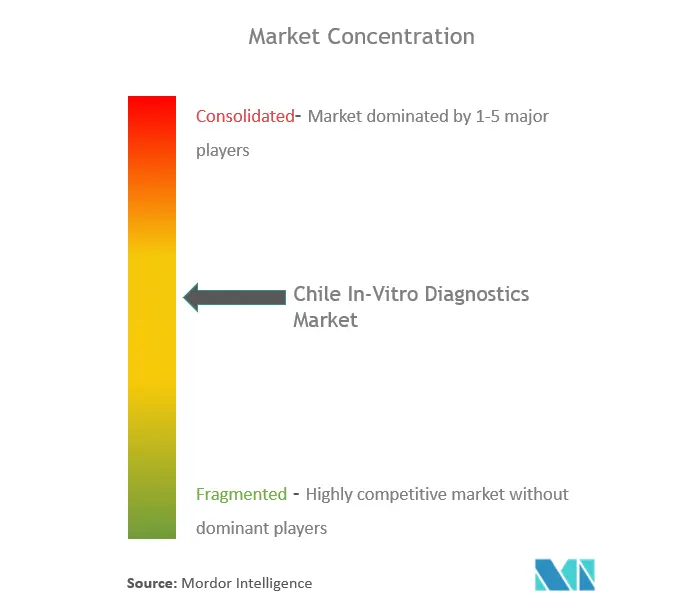

Consolidated Market with Strong Global Presence

The Chile in vitro diagnostics market demonstrates a moderately consolidated structure, dominated by multinational corporations with established global presence and comprehensive product portfolios. These major players leverage their extensive research and development capabilities, established distribution networks, and strong brand recognition to maintain their market positions. Local companies primarily operate as distributors and service providers, forming strategic alliances with global manufacturers to enhance their market presence. The market has witnessed several strategic collaborations and distribution agreements, particularly focusing on expanding access to advanced diagnostic technologies and improving healthcare infrastructure.

The competitive landscape is characterized by high entry barriers due to stringent regulatory requirements and significant capital investments needed for establishing operations. Market leaders have strengthened their positions through strategic acquisitions and partnerships, particularly in specialized diagnostic segments. The presence of well-established distribution channels and service networks creates additional challenges for new entrants, while existing players continue to invest in expanding their product portfolios and technological capabilities to maintain their competitive edge.

Innovation and Service Excellence Drive Success

Success in the Chile in vitro diagnostics market increasingly depends on companies' ability to offer comprehensive medical diagnostics solutions while maintaining high standards of service and support. Market leaders are focusing on developing user-friendly platforms with improved automation capabilities and reduced turnaround times. Companies are also investing in digital solutions and connectivity features to enhance laboratory efficiency and data management capabilities. The ability to provide localized technical support, training, and maintenance services has become crucial for maintaining customer relationships and market share. Additionally, companies are strengthening their supply chain resilience and inventory management to ensure consistent product availability.

Future market success will require companies to adapt to evolving healthcare needs while maintaining cost-effectiveness in their offerings. Players must focus on developing specialized testing solutions for emerging disease areas while ensuring compatibility with existing laboratory testing infrastructure. Building strong relationships with healthcare providers, laboratories, and regulatory authorities will be crucial for long-term success. Companies need to balance innovation with affordability, particularly as healthcare systems become more cost-conscious. The ability to provide comprehensive after-sales support, regular system updates, and flexible financing options will become increasingly important for maintaining competitive advantage in the market.

Chile In-vitro Diagnostic Market Leaders

-

Thermo Fischer Scientific Inc.

-

QIAGEN N.V.

-

Abbott Laboratories

-

Siemens Healthcare GmbH

-

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Chile In-vitro Diagnostic Market News

- January 2022: the Mexican platform announced the advancement of digital diagnostics in Latin America. Healthtech Eva has enabled remote test analysis and broadens access to healthcare by users outside large urban centers.

- November 2021: Todos Medical, Ltd. announced it has confirmed with its PCR test kit providers that the PCR test kits utilized at its Clinical Laboratory Improvement Amendments/Community-Acquired Pneumonia (CLIA/CAP) certified lab Provista Diagnostics based in the Atlanta, GA area can detect a SARS-CoV-2 infection caused by the Omicron variant, as well as all other variants of concern, based on in silico analysis.

Chile In-vitro Diagnostic Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Diseases

- 4.2.2 Increasing Use of Point-of-care (POC) Diagnostics

-

4.3 Market Restraints

- 4.3.1 Stringent Regulations

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Test Type

- 5.1.1 Clinical Chemistry

- 5.1.2 Molecular Diagnostics

- 5.1.3 Immuno Diagnostics

- 5.1.4 Hematology

- 5.1.5 Other Test Types

-

5.2 By Product

- 5.2.1 Instrument

- 5.2.2 Reagent

- 5.2.3 Other Products

-

5.3 By Usability

- 5.3.1 Disposable IVD Devices

- 5.3.2 Reusable IVD Devices

-

5.4 By Application

- 5.4.1 Infectious Disease

- 5.4.2 Diabetes

- 5.4.3 Cancer/Oncology

- 5.4.4 Cardiology

- 5.4.5 Autoimmune Disease

- 5.4.6 Other Applications

-

5.5 By End Users

- 5.5.1 Diagnostic Laboratories

- 5.5.2 Hospitals and Clinics

- 5.5.3 Other End Users

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Becton, Dickinson and Company

- 6.1.3 BioMérieux

- 6.1.4 Bio-Rad Laboratories Inc.

- 6.1.5 F. Hoffmann-La Roche AG

- 6.1.6 QIAGEN NV

- 6.1.7 Siemens Healthcare GmbH

- 6.1.8 Sysmex Corporation

- 6.1.9 Thermo Fischer Scientific Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Chile In-vitro Diagnostic Industry Segmentation

As per the scope of this report, in vitro diagnostics involves medical devices and consumables that are utilized to perform in vitro tests on various biological samples. The Chile in-vitro diagnostic market is segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, Immuno Diagnostics, Hematology, and Other Test Types) Product (Instrument, Reagent, Other Products), Usability (Disposable IVD Devices, Reusable IVD Devices), Application (Infectious Disease, Diabetes, Cancer/Oncology, Cardiology, Autoimmune Disease, and Other Applications), and End User (Diagnostic Laboratories, Hospitals and Clinics, and Other End-Users). The report offers the value (in USD million) for the above segments.

| By Test Type | Clinical Chemistry |

| Molecular Diagnostics | |

| Immuno Diagnostics | |

| Hematology | |

| Other Test Types | |

| By Product | Instrument |

| Reagent | |

| Other Products | |

| By Usability | Disposable IVD Devices |

| Reusable IVD Devices | |

| By Application | Infectious Disease |

| Diabetes | |

| Cancer/Oncology | |

| Cardiology | |

| Autoimmune Disease | |

| Other Applications | |

| By End Users | Diagnostic Laboratories |

| Hospitals and Clinics | |

| Other End Users |

Need A Different Region or Segment?

Customize Now

Chile In-vitro Diagnostic Market Research FAQs

What is the current Chile In Vitro Diagnostics Market size?

The Chile In Vitro Diagnostics Market is projected to register a CAGR of 6.20% during the forecast period (2025-2030)

Who are the key players in Chile In Vitro Diagnostics Market?

Thermo Fischer Scientific Inc., QIAGEN N.V., Abbott Laboratories, Siemens Healthcare GmbH and F. Hoffmann-La Roche AG are the major companies operating in the Chile In Vitro Diagnostics Market.

What years does this Chile In Vitro Diagnostics Market cover?

The report covers the Chile In Vitro Diagnostics Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Chile In Vitro Diagnostics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Chile In Vitro Diagnostics Market Research

Mordor Intelligence offers a comprehensive analysis of the in vitro diagnostics (IVD) sector in Chile. We leverage our extensive experience in clinical laboratory research and consulting to provide detailed insights. Our expert analysts delve into laboratory testing methodologies, clinical chemistry applications, and the advancement of molecular diagnostics technologies. The report thoroughly examines diagnostic testing trends, medical diagnostics developments, and emerging immunodiagnostics solutions. It is available as an easy-to-download report PDF.

The analysis covers crucial aspects of automated diagnostics systems, laboratory diagnostics procedures, and clinical diagnostics methodologies. Stakeholders gain valuable insights into diagnostic equipment innovations, point of care diagnostics advancements, and rapid diagnostics solutions. The report also examines diagnostic kit development, diagnostic reagent applications, and diagnostic instrument specifications. Additionally, it covers diagnostic device technologies, diagnostic biomarker research, diagnostic assay methodologies, and diagnostic analyzer systems. This comprehensive assessment enables healthcare providers, manufacturers, and investors to make informed decisions based on detailed medical testing data and industry trends.