Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

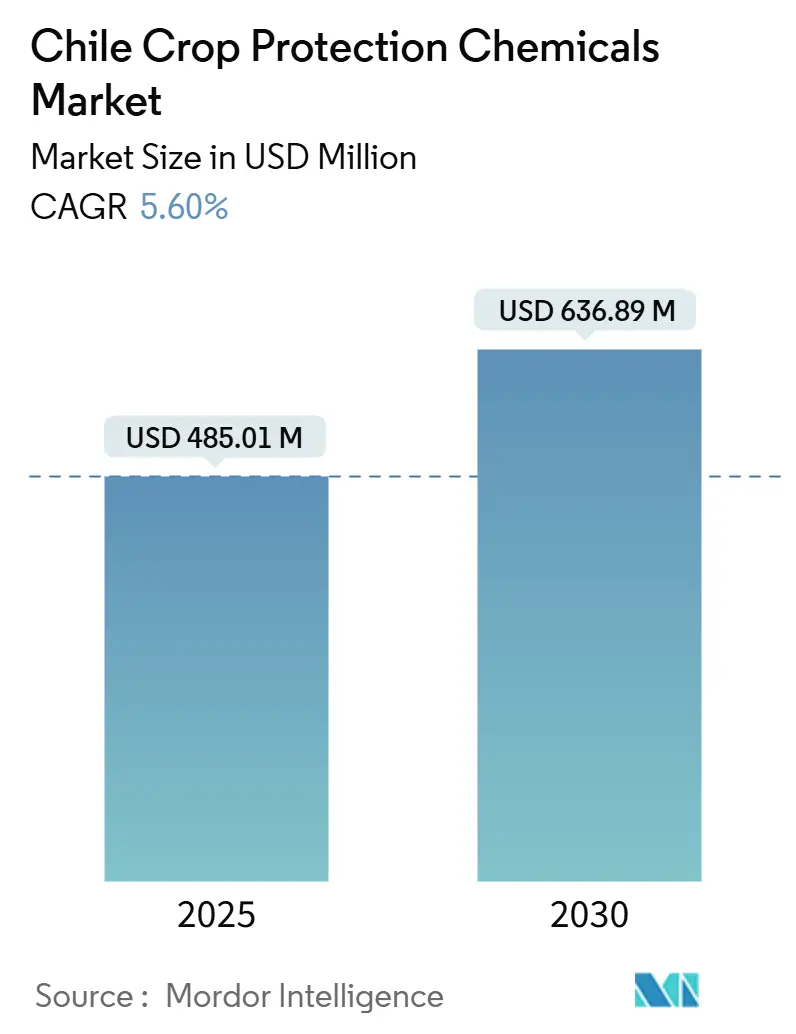

| Market Size (2025) | USD 485.01 Million |

| Market Size (2030) | USD 636.89 Million |

| Growth Rate (2025 - 2030) | 5.60% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chile Crop Protection Chemicals Market Analysis by Mordor Intelligence

The Chile crop protection chemicals market size stands at USD 485.01 million in 2025 and is projected to reach USD 636.89 million in 2030, advancing at a 5.6% CAGR over 2025-2030. Sustained export demand for premium fruit and vegetable crops, rising climate-driven pest pressures, and continued government credit programs for smallholders underpin near-term volume growth. Multinationals are accelerating portfolio renewal to address tightening maximum residue limits, while local innovators leverage biological formulations to capture zero-residue niches. The market's expansion is underpinned by Chile's export-oriented agricultural sector, which contributes approximately 4.7% to the country's GDP. Wider deployment of drone-based precision spraying is lifting application efficiency and mitigating labor shortages in the central valleys. Long-term growth opportunities center on chemigation systems that conserve scarce irrigation water and on commercial crop expansion into avocados and nuts.

Key Report Takeaways

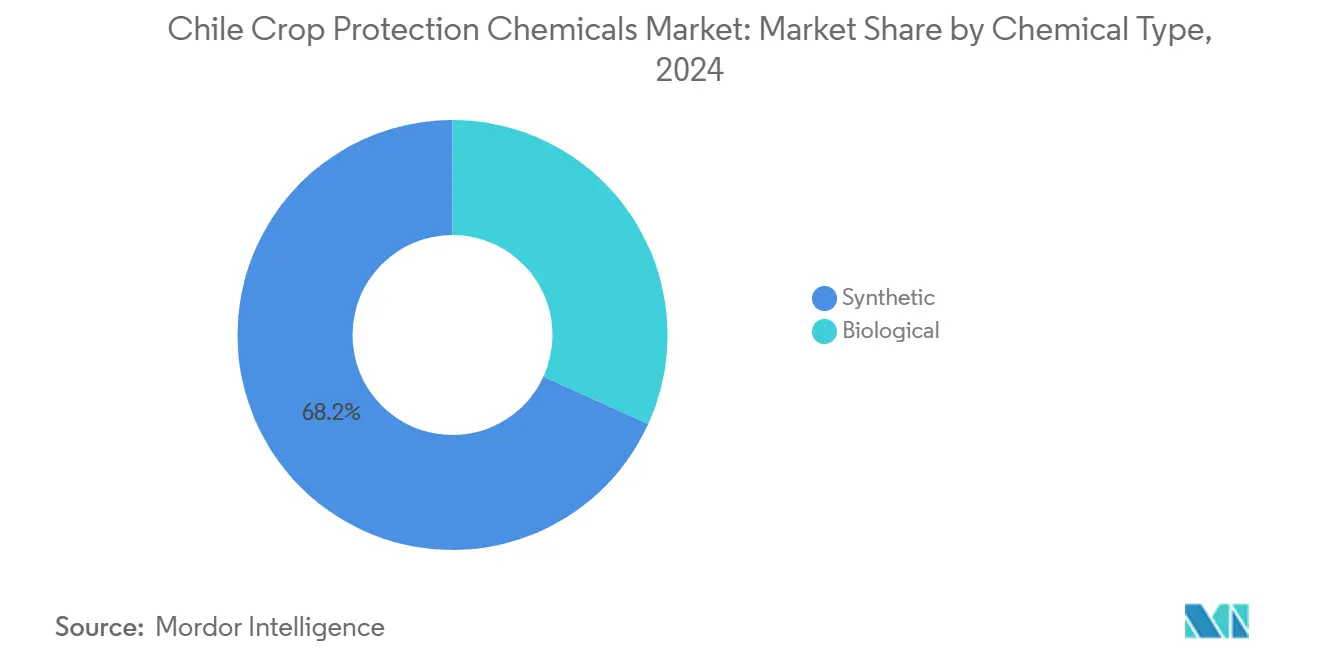

- By chemical type, synthetic led with 68.2% of the Chile crop protection chemicals market share in 2024, while biologicals are advancing at a 9.2% CAGR through 2030.

- By product type, fungicides led with 39.7% revenue share in 2024. Insecticides are forecast to grow at a 9.8% CAGR through 2030.

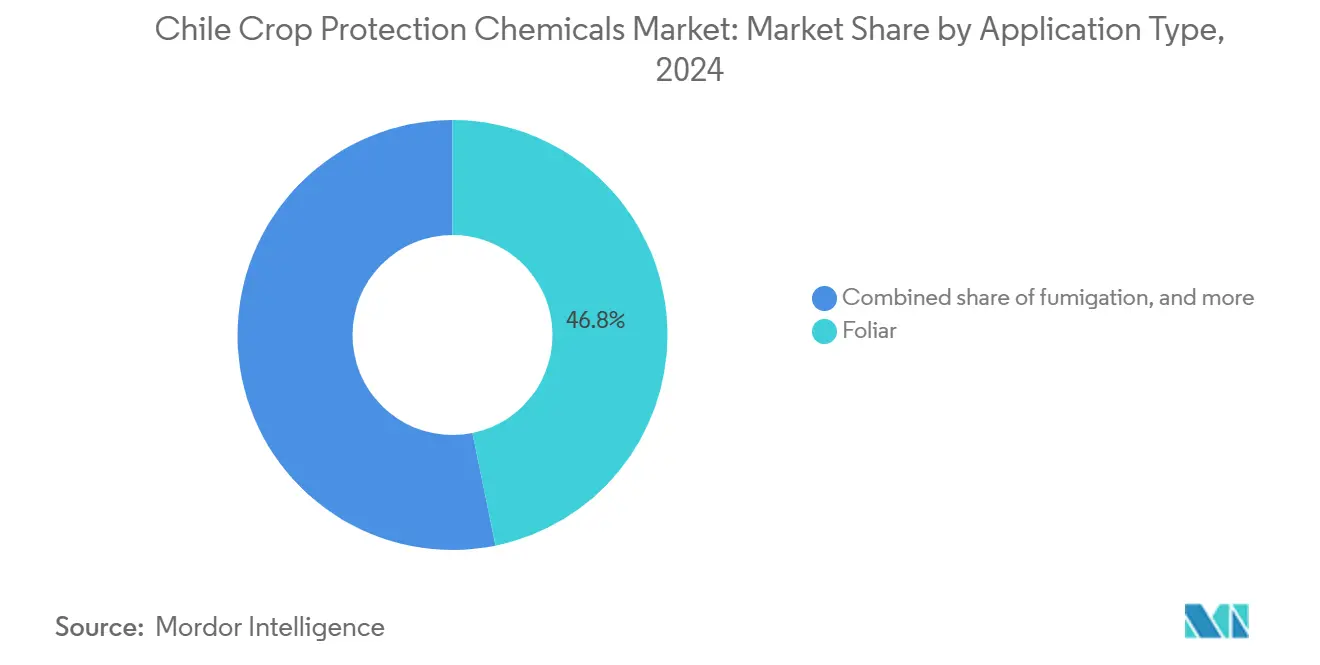

- By application method, foliar spraying accounted for 46.8% of the market share in 2024, while chemigation is projected to expand at a 7.5% CAGR between 2025 and 2030.

- By crop type, fruits and vegetables accounted for a 34.3% share of the Chile crop protection chemicals market size in 2024, and commercial crops are growing at an 8.8% CAGR through 2030.

Chile Crop Protection Chemicals Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-change–driven expansion of desert locust corridors | +0.8% | Northern agricultural regions, expanding southward | Medium term (2-4 years) |

| Escalating fungicide resistance in the table-grape export supply chain | +1.2% | Central valleys, O'Higgins and Maule regions | Short term (≤ 2 years) |

| Government emergency-credit lines for smallholder input purchases | +0.6% | National, concentrated in smallholder regions | Short term (≤ 2 years) |

| Growing adoption of drone-based spot spraying in fruit orchards | +0.9% | Fruit-growing regions, Santiago Metropolitan, and Valparaíso | Medium term (2-4 years) |

| Rapid shift toward zero-residue labels by Chilean retailers | +1.1% | Export-oriented production areas nationwide | Long term (≥ 4 years) |

| Re-registration of paraquat alternatives approved by SAG | +0.7% | National, particularly in grain and commercial crop areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climate-Change–Driven Expansion of Desert Locust Corridors

Warming temperatures and altered rainfall are enabling South American locust species (Schistocerca cancellata) to colonize previously inhospitable zones, forcing growers to invest in broad-spectrum insecticides and real-time monitoring tools[1]Source: Food and Agriculture Organization, “Pesticide Database,” FAO.org. New incursions threaten high-value crops in the Atacama rim, where historically low pesticide use leaves plants vulnerable. Research institutes are piloting integrated control programs that blend entomopathogenic fungi with low-dose synthetics to maintain export compliance. Suppliers able to provide dual-mode products are well positioned as the Chile crop protection chemicals market pivots toward rapid-response solutions. Extension services emphasize early warning and coordinated spraying to reduce migration into the central valleys.

Escalating Fungicide Resistance in Table-Grape Export Supply Chain

Gray mold populations in table grapes are displaying growing resistance to single-site fungicides, jeopardizing shipments that must withstand long, cold-chain journeys to Asia and North America. Exporters now rotate multi-mode chemistries with biological additives to preserve efficacy and meet stricter residue caps. The strategy raises per-hectare spend, supporting value growth for premium formulations in the Chile crop protection chemicals market. Syngenta group and BASF SE have introduced new Succinate Dehydrogenase Inhibitors (SDHI)-based mixtures targeting Botrytis, while Bio Insumos Nativa supplies Trichoderma blends that cut residue loads without compromising shelf life. Continued surveillance of resistance genes informs the development of tailored spray programs every season.

Government Emergency Credit Lines for Smallholder Input Purchases

Inter-American Institute for Agricultural Cooperation (INDAP) and BancoEstado (Bank of the State of Chile) expanded short-term credit to cover seed, fertilizer, and pesticide bills, thereby increasing the adoption of higher-cost biologicals among small orchards. Immediate liquidity eases the cash-flow squeeze at flowering, when timely sprays prevent downgrades that erode export premiums. Suppliers bundle agronomic advice with financing, widening their rural footprint. As more smallholders access modern inputs, volume penetration rises even though consolidation trims the absolute farm count, keeping the Chile crop protection chemicals market on a steady upward path.

Growing Adoption of Drone-Based Spot Spraying in Fruit Orchards

XAG P100 PRO units treat 19 hectares per hour while cutting water use by 96%, a critical gain in drought-exposed central valleys. Orchards with complex canopies benefit from uniform coverage and reduced drift, aligning with new Screen Actors Guild (SAG) buffer rules. Service contractors offering per-acre drone spraying alleviate labor shortages and open a platform for digital prescription maps. This precision trend supports premium price points for low-volume adjuvanted formulations within the Chile crop protection chemicals market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of regenerative agriculture acreage | -0.9% | Coquimbo, Maule, and organic transition zones | Long term (≥ 4 years) |

| Tightening MRLs on export blueberries | -0.6% | Southern regions, blueberry production areas | Medium term (2-4 years) |

| Labor-shortage–induced under-application of field pesticides | -0.8% | National, particularly seasonal crop areas | Short term (≤ 2 years) |

| Capital-intensive drift-mitigation equipment requirements | -0.4% | High-density production areas near sensitive crops | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise of Regenerative Agriculture Acreage

INDAP’s Temporary Activities Sponsor (TAS) program sponsors compost-based fertility and sheep grazing to suppress weeds, trimming synthetic demand on 2,000 hectares in Coquimbo. Premium farmgate prices offset yield dips, yet total chemical volumes contract on transitioning farms. Suppliers counter by promoting biostimulants and microbial pesticides aligned with soil-health goals, cushioning revenue erosion in the Chile crop protection chemicals market. The trend is supported by premium pricing for regeneratively produced crops and increasing consumer demand for environmentally sustainable production methods. While currently concentrated in niche markets, the market represents a structural headwi nd for synthetic chemical demand as adoption scales across Chile's diverse agricultural systems.

Tightening MRLs on Export Blueberries

International market access requirements are constraining chemical options for Chile's expanding blueberry industry, limiting growth in certain product categories. EU and Asian buyers lowered the export for key insecticides, prompting costly switch-outs to compliant actives and biologicals[2]Source: United States Department of Agriculture Foreign Agricultural Service, “Chile: Exporter Guide Annual,” USDA.gov. Extended harvest windows increase the risk of residue buildup, forcing growers to space sprays and accept lower intervention intensity. Although unit prices rise, aggregate insecticide use per hectare falls, mitigating the value upside for certain chemistries. The tightening of Maximum Residue Limits (MRLs) is creating opportunities for biological alternatives while constraining sales of conventional chemistry in one of Chile's fastest-growing export crops.

Segment Analysis

By Chemical Type: Synthetic Leadership Meets Rapid Biological Uptake

Synthetic products held 68.2% of the Chile crop protection chemicals market share in 2024 as their fast knock-down and broad spectrum remain indispensable for export quality. The segment benefits from multi-site innovations that manage resistance while satisfying low-residue mandates. However, biologicals are expanding at a 9.2% CAGR, fueled by retailer zero-residue pledges and SAG’s streamlined bio-pesticide registration. The Chile crop protection chemicals market size captured by biologicals is on track to surpass its 2024 base by 2030, doubling its current value.

Local player Bio Insumos Nativa commands roughly 30% of the national biocontrol sales market and leverages Sumitomo’s capital to scale its fermentation capacity. National Association for Agriculture and Health's (ANASAC) Xilema division distributes Bacillus and Trichoderma lines, while Bayer partners with Koppert for predatory mites. Growers now integrate microbial sprays at bloom and pre-harvest windows, reducing the frequency of synthetic applications yet increasing total spend per hectare due to higher unit prices. The combined approach underpins balanced growth across both chemistry classes in the Chile crop protection chemicals market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Fungicides Dominate but Insecticides Accelerate

Fungicides generated 39.7% of 2024 revenue, anchored in disease-prone grapes, cherries, and blueberries. Complex export logistics mean that a single Botrytis outbreak can erase margin gains, sustaining high per-acre fungicide bills. Conversely, insecticides post the fastest 9.8% CAGR as climate shifts introduce Australian leaf miner, spotted-wing drosophila, and new aphid biotypes. The market size for insecticides is set to climb.

Novel diamide and spinosyn classes gain traction where resistance troubles older pyrethroids. BASF’s Inscalis formulation, launched in 2024, shows quick adoption in citrus against woolly whitefly. Herbicide demand remains steady after paraquat’s exit, with diquat and PPO inhibitors priced at 12-15% premiums over legacy products. Niche lines such as nematicides grow slowly, constrained to high-value berry and grape nurseries.

By Application Method: Chemigation Makes Inroads in Water-Stressed Zones

Foliar spraying still accounts for 46.8% of all treated hectares, yet chemigation grows 7.5% each year as drip systems dominate new orchard plantings. The market size linked to chemigation already exceeds and benefits from metered dosing that lowers runoff. Drone-assisted spot spraying complements chemigation during peak pest waves, synergizing input optimization. The technology is particularly valuable in cherry and avocado orchards, where terrain challenges and tree architecture make ground-based application inefficient.

Fumigation and seed treatment remain specialty niches. Soil treatment gains modest traction in new hazelnut orchards where nematode suppression is critical for early vigor. Suppliers bundle moisture sensors with fertigated pesticide cartridges, positioning themselves as water-savvy partners in Chile’s drought landscape. Labor shortage pressures are accelerating the mechanization and automated application systems that reduce manual workforce requirements while maintaining application quality standards.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop Type: Commercial Crops Outpace Traditional Fruit Mainstays

Fruits and vegetables retained a 34.3% revenue lead in 2024, sustained by cherries whose export receipts hit in season 2023-24. Yet commercial crops, chiefly avocados, citrus, and almonds, expand at an 8.8% CAGR as investors allocate fresh capital into long-life orchards. The market size generated by commercial crops is projected to reach a high in 2030, narrowing the gap with the fruit segments.

Grains and oilseeds require reliable herbicides to offset labor constraints, but limited acreage caps absolute value. Emerging turf and ornamental demand clusters around Santiago’s urban expansion, providing stable, though modest, outlets for selective herbicides and fungicides. This shift toward perennial crops is creating demand for specialized pest management programs designed for long-term orchard and vineyard production systems that require different chemical application strategies than annual crop rotations.

Geography Analysis

Chile’s central valleys, O’Higgins, Maule, Metropolitan Santiago, and Valparaíso command a combined 78.3% of the national fruit area and thus anchor the Chile crop protection chemicals market. The Mediterranean climate aligns with export-grade production yet fosters pathogen proliferation, driving intensive fungicide programs. Easy truck access to San Antonio and Valparaíso ports streamlines input logistics and technical service coverage.

Northern Atacama parcels now receive locust and leaf-miner incursions as warming temperatures redraw pest maps. Growers who once sprayed twice a year now budget for up to six interventions, boosting market value in regions traditionally regarded as marginal. Southern Los Ríos and Los Lagos blueberry belts grapple with stricter European residue caps, pivoting toward biological insecticides and protective nets rather than high-volume sprays.

Regional policy also shapes demand. Coquimbo pioneers regenerative pilots that phase out synthetics, trimming local market size but unlocking sales for biostimulants. Conversely, Biobío intensifies pyrethroid use to combat rising aphid pressure in grains. Nationally consistent SAG rules on drift mitigation standardize equipment upgrades, but adoption speed varies, with wealthier central orchards transitioning first.

Competitive Landscape

The Chile crop protection chemicals market is consolidated, with global multinational corporations maintaining dominant positions alongside emerging regional specialists and biological innovators. Global companies such as Syngenta Group, Bayer AG, BASF SE, UPL Ltd., and Corteva Agriscience collectively account for a significant share of revenue, supplying integrated portfolios that marry chemistry with digital agronomy platforms. Syngenta’s Cropwise suite logs over 120,000 monitored hectares, feeding prescription maps into drone fleets for variable-rate sprays[3]Source: Syngenta Group, “Product Portfolio,” Syngenta.com. BASF’s Revylution fungicide family secures early-season bookings among table grape exporters chasing residue margins.

Regional challenger ANASAC leverages its 600-agent network to penetrate remote zones, while UPL Ltd. bundles post-patent actives with stewardship workshops for smallholders. Biological specialist Bio Insumos Nativa controls 30% of the domestic biocontrol niche following Sumitomo’s investment, which injected scale capital. Med-X’s Nature-Cide tie-up with ANASAC widens retail shelf space for essential-oil formulations.

Competitive intensity centers on proving residue compliance and water-saving credentials rather than sheer product breadth. Firms investing in registration dossiers for paraquat replacements and bee-safe adjuvants gain first-mover rents. Concentration remains high, the top five vendors approach major share, yet dozens of niche importers thrive in specialty segments, preserving choice for growers.

Chile Crop Protection Chemicals Industry Leaders

-

Bayer AG

-

BASF SE

-

Syngenta Group

-

UPL Ltd.

-

Corteva Agriscience

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Med-X formed partnership with ANASAC for Nature-Cide biological product distribution across Chile, expanding biological control options for fruit and vegetable producers seeking zero-residue solutions.

- December 2024: Astarte Capital and Toesca have unveiled a USD 350 million fund dedicated to permanent crops. This move underscores a growing investor interest in orchards, which, in turn, is propelling the expansion of the chemical market, especially those requiring long-term pest management programs.

- October 2024: Sumitomo Corporation completed strategic investment in Bio Insumos Nativa (BIN), Chile's largest biocontrol company with approximately 30% market share and USD 5.6 million annual sales, expanding biological crop protection capabilities in the Chilean market.

Chile Crop Protection Chemicals Market Report Scope

Crop protection chemicals have been defined for this report as commercially manufactured agrochemicals used to prevent crop destruction by pests, diseases, and weeds, thereby improving crop yield and quality. Agrochemicals used by farmers and large commercial growers in crops and non-crop agricultural practices are included in the market studied. Chile Crop Protection Chemicals market is segmented by Chemical Type (Synthetic, Biological), Product Type (Herbicides, Insecticides, Fungicides, Molluscicides, and Nematicides), Application (Chemigation, Foliar, Fumigation, Seed Treatment, and Soil Treatment), and Crop Type (Grains and Cereals, Oilseeds and Pulses, Fruits and Vegetables, Commercial Crops, and Turf and Ornamental Grass). The report offers market size and forecasts in value (USD) and volume (metric tons) for all the above segments.

By Chemical Type

| Synthetic |

| Biological |

By Product Type

| Herbicides |

| Insecticides |

| Fungicides |

| Molluscicides |

| Nematicides |

By Application

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

By Crop Type

| Grains and Cereals |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Commercial Crops |

| Turf and Ornamental Grass |

| By Chemical Type | Synthetic |

| Biological | |

| By Product Type | Herbicides |

| Insecticides | |

| Fungicides | |

| Molluscicides | |

| Nematicides | |

| By Application | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| By Crop Type | Grains and Cereals |

| Oilseeds and Pulses | |

| Fruits and Vegetables | |

| Commercial Crops | |

| Turf and Ornamental Grass |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Chile crop protection chemicals market in 2025?

The market is valued at USD 485.01 million in 2025 and is forecast to grow steadily through 2030.

Which product category dominates grower spending?

Fungicides remain the leading category, generating 39.7% of 2024 revenue due to intensive disease control in fruit crops.

What is driving faster uptake of biological crop protection in Chile?

Export buyers zero-residue standards and SAG's streamlined registration process are pushing biologicals to a 9.2% CAGR through 2030.

Which regions account for most pesticide demand?

The central valley's O'Higgins, Maule, Metropolitan Santiago, and Valparaíso collectively host over 78% of fruit hectares and thus lead national chemical consumption.

Page last updated on: