| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 342.27 Million |

| Market Size (2030) | USD 643.26 Million |

| CAGR (2025 - 2030) | 13.45 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Chile Cold Chain Logistics Market Analysis

The Chile Cold Chain Logistics Market size is estimated at USD 342.27 million in 2025, and is expected to reach USD 643.26 million by 2030, at a CAGR of 13.45% during the forecast period (2025-2030).

Chile's cold chain logistics infrastructure has undergone significant transformation, driven by its position as a major global food exporter. The country's robust commercial network, supported by 29 trade agreements with 65 countries, has necessitated continuous advancement in cold chain capabilities. In a notable development, Emergent Cold Latin America announced the construction of a new temperature-controlled facility in Talcahuano in 2022, demonstrating the market's expansion to meet growing international demand. The pharmaceutical sector has emerged as another crucial driver, generating approximately USD 1.8 billion and contributing 0.73% to Chile's GDP, necessitating sophisticated temperature-controlled logistics solutions.

The market has witnessed innovative technological integration across its cold chain network. Maersk's launch of a refrigerated train service connecting the O'Higgins region to San Antonio represents a significant advancement in sustainable cold chain logistics transportation. This initiative has achieved approximately a 70% reduction in CO2 emissions compared to traditional ground transportation, while maintaining the capacity to transport 31 containers per trip. The development of specialized services like the Cherry Express, featuring integrated end-to-end logistics solutions, demonstrates the market's evolution toward tailored cold supply chain solutions for specific product categories.

The seafood sector has emerged as a significant contributor to cold chain demand, with Chile exporting USD 3.2 billion worth of Atlantic salmon and trout in the first half of 2022. This growth has spurred investment in specialized cold storage facilities and transportation solutions. In April 2022, the MSC Carole vessel set a new record by carrying 2,082 reefer containers from Valparaíso, equivalent to 4,164 TEUs, highlighting the expanding capacity of Chile's cold chain infrastructure to handle increasing export volumes.

The processed food segment has shown remarkable development, with Chile currently exporting 75% of its food products as fresh and semi-processed items, while the remaining 25% comprises processed food products. The OTC pharmaceuticals market, valued at USD 282.3 million in 2022, has further diversified the cold supply chain requirements, necessitating specialized temperature-controlled storage and transportation solutions. These developments have prompted cold chain operators to invest in multi-temperature facilities and advanced cold chain monitoring systems to ensure product integrity across various temperature ranges.

Chile Cold Chain Logistics Market Trends

The Booming Pharmaceutical Market is Driving Cold Chain Logistics

The pharmaceutical sector in Chile has emerged as a significant driver for pharmaceutical cold chain logistics, with the industry generating approximately USD 1.8 billion, representing 0.73% of the country's GDP. The sector's robust growth has created substantial opportunities for expansion, attracting foreign companies that recognize Chile's potential as a regional hub. The pharmaceutical business benefits multiple economic sectors, including manufacturing, trade, and transportation, creating a multiplier effect on pharmaceutical cold chain logistics demand. The industry's focus on treating chronic diseases and lifestyle-related illnesses has led to an expanding portfolio of temperature-sensitive medications requiring sophisticated cold chain management.

The pharmaceutical industry's infrastructure development and increasing domestic production capabilities have further amplified the need for specialized cold chain solutions. The sector has witnessed significant investments in research and development, with companies focusing on developing new pharmaceutical products that require precise temperature control during storage and transportation. The growing emphasis on maintaining product integrity throughout the supply chain has led to increased adoption of advanced cold chain technologies and monitoring systems. Additionally, the pharmaceutical industry's export potential has created new opportunities for cold chain logistics providers to establish international temperature-controlled supply chains.

Understand The Key Trends Shaping This Market

Download PDF

Growing Fish, Meat, and Seafood Industry Boosting Cold Chain Demand

Chile's position as the fourth-largest exporter of aquatic products globally has significantly influenced the cold chain logistics market's growth. With aquatic product exports reaching USD 5.9 billion, representing 3.9% of the global total, the industry demands sophisticated food cold chain infrastructure to maintain product quality. The country's strong position in salmonid production and mussel cultivation has created a robust demand for temperature-controlled storage and transportation solutions. The industry's commitment to maintaining product freshness and meeting international quality standards has led to increased investments in cold chain infrastructure and technology.

The meat and poultry sector has also emerged as a significant driver for cold chain logistics services. Chile's pork sector has shown remarkable development, with the country now exporting to more than 60 nations globally, accounting for 81% of its production. This extensive international reach has necessitated the development of advanced cold chain transportation solutions capable of maintaining product quality across long-distance transportation routes. The industry's focus on meeting diverse market requirements and maintaining product freshness has led to the adoption of sophisticated temperature monitoring systems and specialized transportation solutions, further driving the cold chain logistics market's growth.

Increasing Fruit Export Driving Cold Chain Infrastructure Development

Chile's fruit export sector has emerged as a major driver for cold chain logistics, with significant growth projected for 2023. According to recent USDA reports, Chilean citrus exports are expected to see substantial increases, with lemon exports anticipated to reach 100,000 metric tons and orange exports projected to hit 105,000 metric tons in 2023. This growth has necessitated substantial investments in cold chain distribution infrastructure to ensure product quality during transportation and storage. The industry's focus on maintaining fruit freshness and meeting international quality standards has led to the development of sophisticated temperature-controlled logistics solutions.

The expansion of Chile's fruit export market has been supported by the country's extensive network of free-trade agreements and strong relationships with international markets. The United States remains a primary destination for Chilean citrus exports, accounting for approximately 65% of total Chilean lemon exports. This international trade dynamic has driven the development of advanced cold chain transportation solutions capable of maintaining product quality during long-distance transportation. The industry's commitment to quality and the increasing demand for fresh Chilean fruits has led to continuous improvements in cold chain technology and infrastructure, including advanced temperature monitoring systems and specialized transportation solutions.

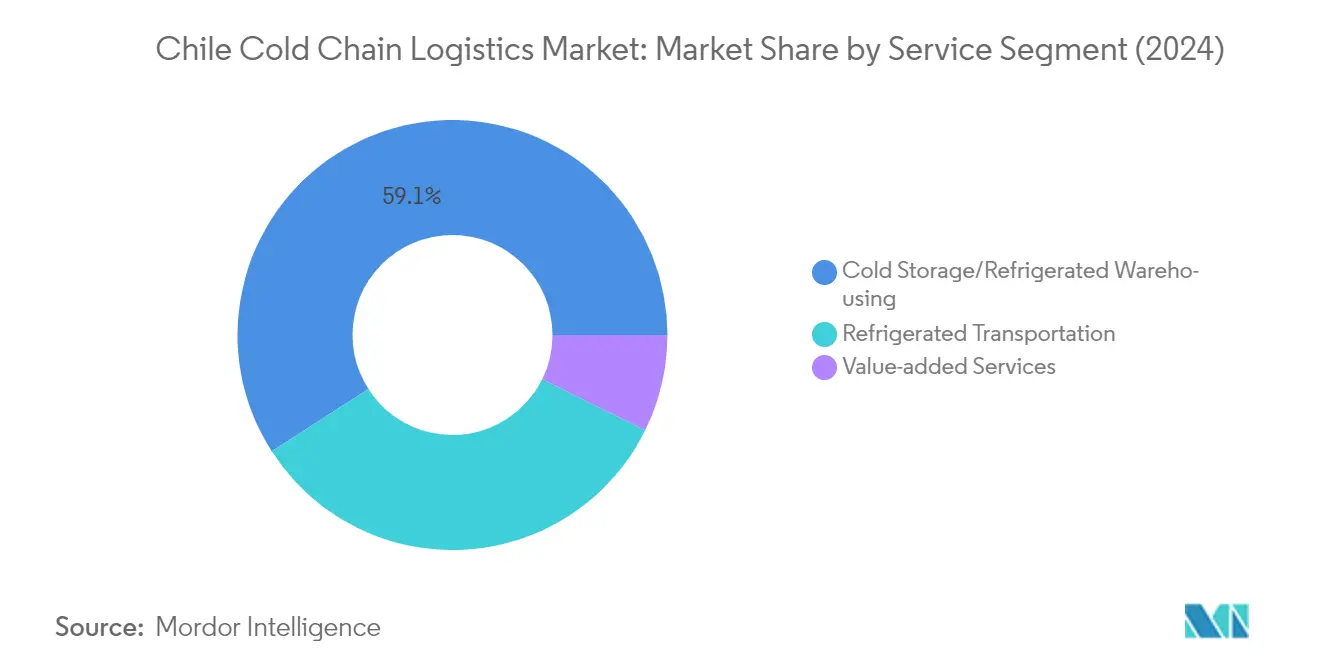

Segment Analysis: By Service

Cold Storage/Refrigerated Warehousing Segment in Chile Cold Chain Logistics Market

The cold storage and refrigerated warehousing segment continues to dominate the Chile cold chain logistics market, holding approximately 59% of the total market share in 2024. This segment's prominence is driven by Chile's position as a major global food exporter, particularly in fruits, seafood, and meat products. The strategic location of cold storage facilities near major ports like San Antonio and Valparaiso has strengthened this segment's market position. Companies like Emergent Cold LatAm are expanding their cold storage infrastructure, with new temperature-controlled facilities being constructed in key locations such as Talcahuano. These facilities are equipped with state-of-the-art technology for maintaining precise temperature controls and offer various storage options for different temperature-sensitive products, from fresh produce to frozen seafood.

Value-Added Services Segment in Chile Cold Chain Logistics Market

The value-added services segment is emerging as the fastest-growing segment in the Chile cold chain logistics market, with a projected growth rate of approximately 14% during 2024-2029. This rapid growth is being driven by increasing demand for specialized services such as order management, blast freezing, labeling, and inventory management. The segment's expansion is supported by the rising adoption of technology-driven solutions and the growing complexity of supply chain requirements. Companies are investing in advanced systems for real-time monitoring, quality control, and specialized packaging services. The growth is further fueled by the increasing need for customized solutions in the pharmaceutical and food industries, where precise handling and processing requirements are essential for maintaining product quality and compliance with regulatory standards.

Remaining Segments in Chile Cold Chain Logistics Market Service Segmentation

The refrigerated transportation segment plays a vital role in completing the cold chain logistics ecosystem in Chile. This segment encompasses both domestic and international transportation of temperature-sensitive goods through various modes including road, sea, and air. The segment is characterized by its extensive network of refrigerated trucks and containers that maintain product integrity throughout the transportation journey. The segment's significance is particularly evident in Chile's export-oriented economy, where efficient transportation of perishable goods to international markets is crucial. Recent developments in this segment include the adoption of advanced temperature monitoring systems, sustainable transportation solutions, and the integration of real-time tracking technologies to ensure product safety and quality during transit.

Segment Analysis: By Temperature

Chilled Segment in Chile Cold Chain Logistics Market

The chilled segment continues to dominate the Chile cold chain logistics market, commanding approximately 64% market share in 2024. This significant market position is primarily driven by Chile's status as the leading fruit exporter in the southern hemisphere and its position as the world's top exporter of table grapes, blueberries, plums, dried apples, and prunes. The segment's growth is further supported by the country's robust dairy industry and increasing demand for temperature-sensitive pharmaceutical products. The Far East remains the primary destination for Chilean chilled exports, while the United States maintains its position as the second-largest market. The segment's strength is reinforced by sophisticated cold chain infrastructure and strategic locations of cold storage facilities near major ports, enabling efficient handling and distribution of temperature-sensitive products.

Frozen Segment in Chile Cold Chain Logistics Market

The frozen segment is emerging as the fastest-growing category in Chile's cold chain logistics market, projected to grow at approximately 14% during 2024-2029. This growth is primarily driven by the expanding frozen food logistics industry and increasing exports of frozen seafood products. Chile's position as the world's second-largest producer of farmed salmon, contributing 32% of global production, has created substantial demand for frozen storage and transportation services. The segment's growth is further accelerated by increasing investments in frozen storage infrastructure, particularly in key ports like Talcahuano and Puerto Montt. The expansion of value-added frozen food processing facilities and rising domestic consumption of frozen products are also contributing to the segment's rapid growth trajectory.

Segment Analysis: By End User

Fish, Meat, and Seafood Segment in Chile Cold Chain Logistics Market

The fish, meat, and seafood segment dominates the Chile cold chain logistics market, holding approximately 36% of the market share in 2024. This segment's prominence is primarily driven by Chile's position as one of the world's largest exporters of frozen fish and seafood products, particularly salmon. The country's strategic location and extensive coastline have enabled it to become a major hub for seafood exports to key markets including the United States, Japan, Brazil, and various European nations. The segment's growth is further supported by the country's robust fishing industry infrastructure, advanced cold storage facilities near major ports, and stringent temperature-controlled logistics networks that ensure product quality throughout the supply chain.

Pharmaceutical Segment in Chile Cold Chain Logistics Market

The pharmaceutical segment is emerging as the fastest-growing segment in Chile's cold chain logistics market, with projections indicating strong growth through 2024-2029. This rapid expansion is driven by increasing domestic pharmaceutical production, growing healthcare infrastructure, and rising demand for temperature-sensitive medical products. The segment's growth is further accelerated by Chile's position as a regional pharmaceutical hub, with many international pharmaceutical companies establishing operations in the country. The implementation of stringent regulations for pharmaceutical storage and transportation, coupled with investments in specialized cold chain infrastructure and temperature-monitoring technologies, is strengthening this segment's growth trajectory.

Remaining Segments in Chile Cold Chain Logistics Market End User Segmentation

The other segments in Chile's cold chain logistics market include dairy products, vegetables, fruits, bakery and confectionery, processed food, and other applications. The dairy products segment maintains significant importance due to Chile's growing dairy industry and increasing export activities. The fruits and vegetables segments are driven by Chile's status as a major agricultural exporter, particularly of fresh produce to international markets. The bakery and confectionery segment is supported by growing domestic consumption and export opportunities, while the processed food segment continues to evolve with changing consumer preferences and increasing demand for convenience foods. Each of these segments contributes uniquely to the market's diversity and overall growth potential.

Chile Cold Chain Logistics Market Geography Segment Analysis

Chile Cold Chain Logistics Market in South Chile

South Chile dominates the country's cold chain logistics landscape, holding approximately 49% of the total market share in 2024. The region's prominence is largely attributed to its strategic location and robust infrastructure supporting the fishing and aquaculture industries. Major cities like Temuco, Valdivia, Puerto Montt, and Punta Arenas serve as key logistics hubs, facilitating efficient cold storage operations. The region's cold storage facilities and refrigerated transportation networks are particularly well-developed to handle the significant volumes of salmon, seafood, and agricultural products. The presence of important ports like Lirquen, Punta Arenas, and Talcahuano further strengthens the region's position in cold chain logistics, enabling seamless export operations to international markets.

Chile Cold Chain Logistics Market in Rest of Chile

The Rest of Chile region demonstrates the highest growth potential in the cold chain logistics market, with a projected CAGR of approximately 14% from 2024 to 2029. This remarkable growth is driven by increasing investments in cold storage infrastructure and the expansion of refrigerated logistics networks. The region's cold chain capabilities are being enhanced to support the growing pharmaceutical and processed food industries. The northern areas, including important cities like Arica and Iquique, are developing specialized cold chain solutions to cater to the unique requirements of mining-related logistics and pharmaceutical distribution. The modernization of ports and logistics facilities in these areas is attracting both domestic and international cold chain operators, fostering competitive service offerings and technological advancement.

Chile Cold Chain Logistics Market in Central Chile

Central Chile represents a crucial hub for temperature-controlled logistics operations, centered around the capital region of Santiago and neighboring areas. The region benefits from its dense population concentration and well-established transportation infrastructure. The presence of major ports like San Antonio and Valparaiso facilitates efficient handling of temperature-sensitive cargo. The area's cold chain network supports a diverse range of industries, including pharmaceuticals, fresh produce, and processed foods. The region's strategic location enables efficient distribution to both domestic and international markets, while its advanced cold chain warehouse facilities cater to the growing demands of e-commerce and retail sectors.

Chile Cold Chain Logistics Market in Other Regions

Beyond the primary regions, Chile's cold chain logistics market demonstrates varying degrees of development across different geographical areas. Each region presents unique opportunities and challenges based on local industry concentrations and infrastructure development levels. The market dynamics are influenced by factors such as proximity to agricultural production areas, port access, and population density. Emerging trends include the adoption of sustainable cold chain solutions, integration of IoT technologies for temperature monitoring, and development of specialized storage facilities for different product categories. The continued expansion of cold chain infrastructure across these regions is essential for supporting Chile's growing export-oriented economy and meeting increasing domestic demand for temperature-sensitive products.

Get Analysis on Important Geographic Markets

Download PDF

Chile Cold Chain Logistics Industry Overview

Top Companies in Chile Cold Chain Logistics Market

The cold chain logistics market in Chile is characterized by continuous innovation and strategic developments among key players like Megafrío Chile SA, Frio Romeral, and Empresas Taylor. Companies are increasingly investing in advanced cold chain monitoring technologies, including radio frequency identification in warehouses, cloud storage, the Internet of Things for real-time inventory management, and electronic data interchange to enhance information exchange with clients during transportation. The industry is witnessing a significant push toward greater visibility and transparency throughout the supply chain, particularly driven by pharmaceutical sector requirements. Market players are focusing on expanding their service portfolios through partnerships and acquisitions while simultaneously modernizing their infrastructure to meet evolving customer demands. The COVID-19 pandemic has accelerated digital transformation initiatives across the industry, with companies rapidly adopting new technologies to maintain operational continuity and improve service delivery.

Moderate Fragmentation with Strong Local Presence

The Chilean cold chain logistics market exhibits a moderately fragmented structure, with a mix of established local players and global logistics companies competing for market share. Local specialists like Megafrío Chile SA and Frio Romeral have built strong positions through their deep understanding of regional requirements and extensive client networks across sectors including retail, food service, and pharmaceuticals. The market has seen increasing consolidation activities as larger players seek to expand their capabilities and geographic reach through strategic acquisitions and partnerships.

The competitive dynamics are shaped by the presence of global logistics providers like CEVA Logistics and Agility Logistics, who bring international expertise and advanced technological capabilities to the market. These global players are actively expanding their presence in Chile through partnerships with local operators and investments in infrastructure. The industry is witnessing a trend toward vertical integration, with companies expanding their service offerings to provide end-to-end cold chain distribution solutions, from warehousing to last-mile delivery.

Innovation and Integration Drive Market Success

Success in the Chilean cold chain logistics market increasingly depends on companies' ability to integrate advanced technologies while maintaining cost efficiency. Market leaders are investing in automated warehouse management systems, robotics technology, and innovative packaging solutions to enhance operational efficiency and service quality. Companies that can offer comprehensive solutions, including value-added services like inventory management, blast freezing, and real-time monitoring, are better positioned to capture market share and maintain long-term client relationships.

The future competitive landscape will be shaped by companies' ability to address growing end-user demands for sustainability and transparency in controlled temperature logistics operations. Players must focus on developing environmentally friendly solutions while maintaining temperature integrity throughout the supply chain. The increasing regulatory focus on food safety and pharmaceutical storage requirements presents both challenges and opportunities for market participants. Success will depend on building strong relationships with key industry sectors, particularly in food and pharmaceuticals, while maintaining the flexibility to adapt to changing market conditions and customer requirements.

Chile Cold Chain Logistics Market Leaders

-

Megafrio Chile

-

Frio Romeral Limitada

-

Empresas Taylor

-

Transportes Nazar

-

Friofort SA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Chile Cold Chain Logistics Market News

June 2023: Emergent Cold Latin America announced the acquisition of Hook Chile, a prominent driver in the country’s salmon industry and food importer. Hook Chile operates two high-quality installations with fresh land for unborn expansions that could double the living capacity. First is a pallet storehouse in San Antonio, strategically located near the Port of San Antonio and the roadways connecting Chile’s main metropolitan areas.

February 2023: Emergent Cold Latin America, a growing refrigerated storehouse and logistics service provider, announced the acquisition of Multifrigo, a leading driver in Santiago – Chile’s capital and largest megacity. Emergent Cold LatAm also blazoned plans to expand Multifrigo’s central automated installation in El Olivo to 35,000 pallet positions or triple its current size, creating fresh capacity and service immolations.

Chile Cold Chain Logistics Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Current Market Scenario

-

4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Growing Fruit Exports

- 4.2.2 Restraints

- 4.2.2.1 Challenges of First Mile Distribution in Chile

- 4.2.3 Opportunities

- 4.2.3.1 Increasing Frozen Food Popularity

- 4.3 Technological Trends and Automation

- 4.4 Government Regulations and Initiatives

- 4.5 Industry Value Chain/Supply Chain Analysis

- 4.6 Spotlight on Ambient/Temperature-controlled Storage

-

4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Emission Standards and Regulations on the Cold Chain Industry

- 4.9 Impact of the COVID-19 Pandemic on the Market

5. MARKET SEGMENTATION

-

5.1 Service

- 5.1.1 Storage

- 5.1.2 Transportation

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

-

5.2 Temperature

- 5.2.1 Chilled

- 5.2.2 Frozen

- 5.2.3 Ambient

-

5.3 End User

- 5.3.1 Horticulture (Fresh Fruits and Vegetables)

- 5.3.2 Dairy Products (Milk, Ice Cream, Butter, etc.)

- 5.3.3 Meat, Fish, and Poultry

- 5.3.4 Processed Food Products

- 5.3.5 Pharma, Life Sciences, and Chemicals

- 5.3.6 Other End Users

6. COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

-

6.2 Company Profiles

- 6.2.1 Emergent Cold LatAm

- 6.2.2 Megafrio Chile SA

- 6.2.3 Empresas Taylor

- 6.2.4 Transportes Nazar

- 6.2.5 Friofort SA

- 6.2.6 Frigorifico Pravia

- 6.2.7 Frigorificos Puerto Montt

- 6.2.8 Tudefrigo SA

- 6.2.9 TIBA Chile

- 6.2.10 Ceva Logistics*

- *List Not Exhaustive

- 6.3 Other Companies

7. FUTURE OF THE MARKET

8. APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution by Activity, Contribution of the Transport and Storage Sector to the Economy)

- 8.2 Insights into Capital Flows (investments in the Transport and Storage Sector)

- 8.3 External Trade Statistics - Export and Import by Product and by Destination/Origin

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Chile Cold Chain Logistics Industry Segmentation

The technology and mechanism that allows for the secure delivery of temperature-sensitive goods and items along the supply chain are known as cold chain logistics. Any product that is perishable or is branded as such would almost certainly need cold chain management. A complete background analysis of Chile's cold chain logistics market, including the assessment of the economy and contribution of sectors in the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics and geographical trends, and COVID-19 impact, is covered in the report.

Chile's cold chain logistics market is segmented by service (storage, transportation, and value-added services), temperature type (chilled, frozen, and ambient), and end-user (horticulture ((fresh fruits and vegetables), dairy products (milk, ice cream, butter, etc.); meat, fish, and poultry; processed food products; pharma, life sciences, chemicals; and other end users). The report offers market size and forecasts for all the above segments in value (USD).

| Service | Storage |

| Transportation | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) | |

| Temperature | Chilled |

| Frozen | |

| Ambient | |

| End User | Horticulture (Fresh Fruits and Vegetables) |

| Dairy Products (Milk, Ice Cream, Butter, etc.) | |

| Meat, Fish, and Poultry | |

| Processed Food Products | |

| Pharma, Life Sciences, and Chemicals | |

| Other End Users |

Need A Different Region or Segment?

Customize Now

Chile Cold Chain Logistics Market Research FAQs

How big is the Chile Cold Chain Logistics Market?

The Chile Cold Chain Logistics Market size is expected to reach USD 342.27 million in 2025 and grow at a CAGR of 13.45% to reach USD 643.26 million by 2030.

What is the current Chile Cold Chain Logistics Market size?

In 2025, the Chile Cold Chain Logistics Market size is expected to reach USD 342.27 million.

Who are the key players in Chile Cold Chain Logistics Market?

Megafrio Chile, Frio Romeral Limitada, Empresas Taylor, Transportes Nazar and Friofort SA are the major companies operating in the Chile Cold Chain Logistics Market.

What years does this Chile Cold Chain Logistics Market cover, and what was the market size in 2024?

In 2024, the Chile Cold Chain Logistics Market size was estimated at USD 296.23 million. The report covers the Chile Cold Chain Logistics Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Chile Cold Chain Logistics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Chile Cold Chain Logistics Market Research

Mordor Intelligence offers a comprehensive analysis of the cold chain logistics sector in Chile. We leverage our extensive expertise in temperature controlled logistics and cold storage solutions. Our research thoroughly examines the evolving landscape of vaccine cold chain infrastructure, pharmaceutical cold chain developments, and food cold chain systems. The report provides detailed insights into cold chain transportation networks, cold supply chain dynamics, and the emerging cryogenic logistics technologies shaping the Chilean market.

Stakeholders gain valuable understanding of cold chain monitoring systems, cold chain warehouse operations, and refrigerated transportation solutions through our detailed analysis. This information is available as an easy-to-download report PDF. The study covers temperature sensitive logistics requirements for perishable goods logistics, while examining frozen food logistics and reefer logistics capabilities. Our research encompasses cold chain distribution strategies, cold chain shipping innovations, and advanced controlled temperature logistics solutions. It provides actionable insights for industry participants looking to optimize their operations in Chile's growing cold chain sector.