| Study Period | 2024 - 2030 |

| Market Size (2025) | USD 6.53 Billion |

| Market Size (2030) | USD 9.26 Billion |

| CAGR (2025 - 2030) | 7.23 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players Slurry Market Major Players")

*Disclaimer: Major Players sorted in no particular order |

Slurry Market Size")

Chemical Mechanical Planarization (CMP) Slurry Market Analysis

The Chemical Mechanical Planarization Slurry Market size is estimated at USD 6.53 billion in 2025, and is expected to reach USD 9.26 billion by 2030, at a CAGR of 7.23% during the forecast period (2025-2030).

The semiconductor industry is undergoing significant transformation driven by massive investments and technological advancements. According to industry projections, the global semiconductor market is expected to double by 2030, reaching more than USD 1 trillion, with China contributing over 60% of that increase. This growth is evidenced by major investments such as the US Department of Commerce's April 2024 announcement to provide TSMC with USD 6.6 billion in direct funding for expanding its Arizona facilities. The increasing focus on domestic semiconductor manufacturing has led to various government initiatives worldwide, including the European Chips Act's approval of EUR 43 billion to develop more fabs and increase semiconductor fabrication in the region.

The rapid expansion of 5G technology and data center infrastructure is creating unprecedented demand for advanced semiconductor components. According to Ericsson's projections, 5G mobile subscriptions are anticipated to reach 5 billion by 2028, with 5G population coverage expected to reach 85% and networks carrying around 70% of mobile traffic. This growth is supported by the extensive development of data center infrastructure, with the United States alone hosting 5,381 data centers as of March 2024, the highest number globally. The increasing demand for high-performance computing and data processing capabilities is driving the need for more sophisticated semiconductor manufacturing processes.

The industry is witnessing a significant shift toward advanced manufacturing processes and materials innovation. Major manufacturers are investing in cutting-edge facilities and technologies to meet the growing demand for high-performance semiconductors. For instance, in January 2024, FUJIFILM Corporation announced the full-scale operation of its new CMP slurries production facility at its Kumamoto site, demonstrating the industry's commitment to expanding manufacturing capabilities. The focus on advanced nodes and complex architectures is driving the development of more sophisticated CMP solutions capable of handling increasingly intricate semiconductor designs, which are critical for advanced packaging.

Supply chain resilience has become a critical focus area, with major industry players implementing strategic initiatives to ensure stable production capabilities. In March 2024, Dongjin Semichem began supplying chemical mechanical polishing slurry to SK Hynix for high bandwidth memory production, representing a significant step toward supply chain diversification. The logic semiconductor market is showing strong growth potential, with revenues projected to reach USD 191.7 billion in 2024, marking a 9.6% increase from the previous year. This growth is driving investments in advanced semiconductor equipment and encouraging the development of more sophisticated CMP solutions to meet the increasing demands of logic device manufacturing.

Chemical Mechanical Planarization (CMP) Slurry Market Trends

Miniaturization of Electronic Products

The continuous push for smaller, thinner, and more powerful electronic devices is driving significant demand for electronic polishing and chemical mechanical planarization (CMP) slurry and pads. Portable electronic equipment such as smartphones, laptops, electric vehicles, tablets/notebooks, and wearable devices increasingly demand smaller, thinner semiconductor chips to save space and improve miniaturization. This trend is evidenced by the high smartphone penetration rates, with Ofcom reporting that the United Kingdom reached 94% smartphone penetration in 2023, with those between 24-34 and 35-54 years recording the highest rates. The miniaturization drive is not just about saving space; it's crucial in boosting speed and enhancing semiconductor devices, as smaller sizes lead to higher density and shorter distances, enabling faster frequencies and clock rates in electronic devices.

The automotive sector has emerged as a major driver for miniaturization, with vehicles incorporating increasingly sophisticated electronic systems requiring compact, high-performance semiconductors. According to Intel, global car sales are projected to reach 101.4 million units by 2030, with autonomous vehicles expected to account for approximately 12% of car registrations. This automotive evolution demands advanced driver-assistance systems (ADAS), infotainment systems, and sophisticated control units, all requiring miniaturized components that rely heavily on precise CMP processes. The trend toward miniaturization is further accelerated by the emergence of new materials like graphene, which facilitates the development of smaller, more efficient electronic components while typically consuming less power, paving the way for energy-efficient devices.

Understand The Key Trends Shaping This Market

Download PDF

The Growing Complexity of Integrated Circuits

The semiconductor industry's shift toward smaller nodes (7nm, 5nm, and beyond) has intensified the demand for precise wafer planarization processes, driving the need for advanced CMP slurry and pad solutions. The incorporation of novel materials such as low-k dielectrics and high-k metal gates in semiconductor devices necessitates the development of specialized CMP slurries and pads, particularly soft CMP pads for ensuring safe handling of these materials. This complexity is further amplified by the introduction of new metal alloys like copper and cobalt for interconnects, requiring customized CMP solutions to ensure defect-free surfaces. The explosion in data generation has fueled demand for improved memory and storage types, with data centers being a prime example of this trend. According to Cloudscene, in 2022, the United States led with 2,701 data centers, followed by Germany (487), the United Kingdom (456), and China (443), highlighting the massive infrastructure supporting these complex integrated circuits.

The advancement of 3D integrated circuits (3D ICs) and through-silicon vias (TSVs) has introduced additional complexity to the planarization landscape. These 3D structures not only aid in efficient heat dissipation but also address thermal challenges in densely packed electronics. The memory chip sector exemplifies this growing complexity, with WSTS reporting that revenue from memory component sales reached USD 134.41 billion in 2022. This growth is driven by expanding applications across server, mobile, data communication, automotive, and industrial segments. The rise of 5G technology is further revolutionizing applications across mobile, IoT, automotive, and other sectors, necessitating diverse design processes and more sophisticated IC architectures that require precise integrated circuit manufacturing and semiconductor polishing for optimal performance.

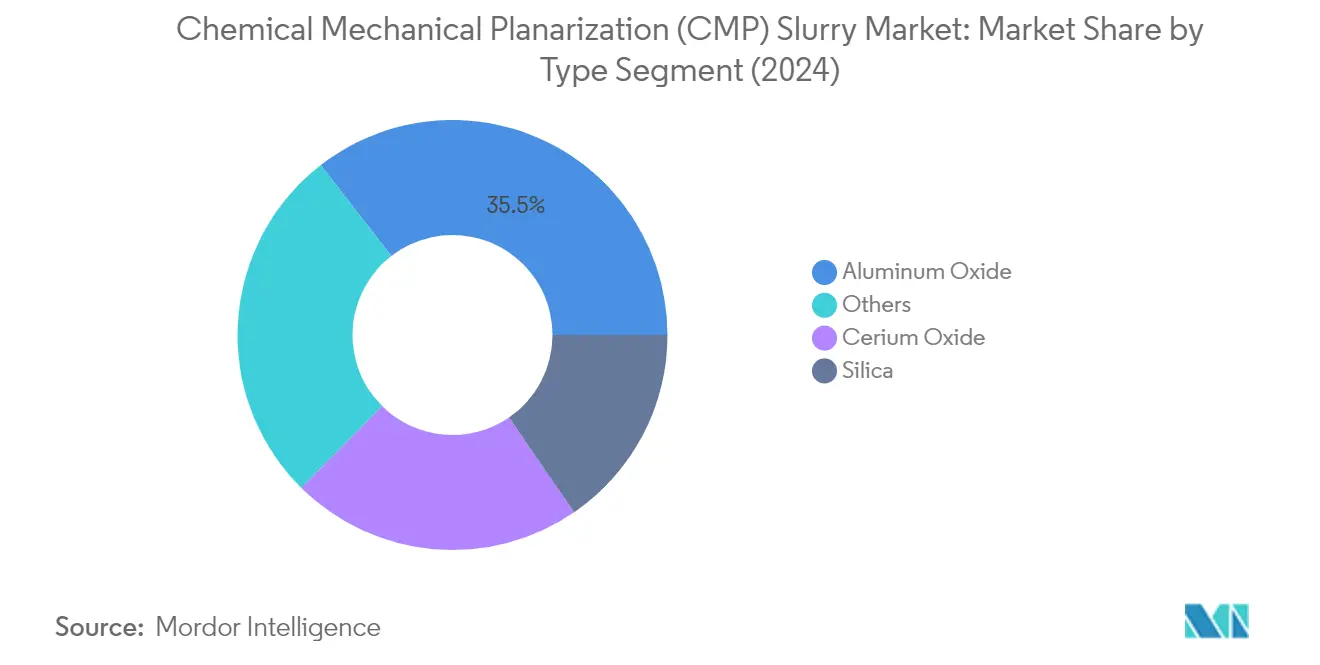

Segment Analysis: By Type - CMP Slurry

Aluminum Oxide Segment in Chemical Mechanical Planarization (CMP) Slurry Market

The aluminum oxide segment maintains its dominant position in the CMP slurry market, commanding approximately 35% market share in 2024. This leadership position is attributed to aluminum oxide's exceptional technical capabilities and widespread application in semiconductor manufacturing processes. The material's controlled particle size and exceptional hardness make it particularly effective in achieving precise wafer flatness and uniformity, crucial for optimal device performance. Aluminum oxide's versatility in CMP slurry applications, especially in tungsten CMP where precise uniformity and planarity are paramount, has solidified its market position. The segment's growth is further supported by its cost-effectiveness, ready availability, and proven track record in delivering consistent performance across various semiconductor manufacturing processes.

Cerium Oxide Segment in Chemical Mechanical Planarization (CMP) Slurry Market

The cerium oxide segment is projected to experience the highest growth rate of approximately 8% during the forecast period 2024-2029. This accelerated growth is driven by cerium oxide's superior performance in achieving high-precision finishes, particularly in applications such as shallow trench isolation (STI) and interlevel dielectrics (ILD). The material's unique chemical properties and interactions enable it to deliver superior finishes on glass and related substrates, often outperforming traditional alternatives. The segment's growth is further bolstered by increasing demand in LCD screen manufacturing, advanced packaging solutions, and emerging semiconductor applications where precision wafer polishing is critical.

Remaining Segments in CMP Slurry Market

The silica and other segments continue to play vital roles in the CMP slurry market, each offering unique advantages for specific applications. Silica-based slurries are particularly valued for their chemical stability and exceptional abrasive properties, making them ideal for polishing interlayer insulating films and various specialized applications. The other segment, comprising materials such as ceramics, silicon carbide, zirconia, and diamonds, addresses niche requirements in the semiconductor manufacturing process, providing solutions for specialized polishing needs and emerging technologies. These segments collectively contribute to the market's diversity and ability to meet evolving semiconductor manufacturing requirements.

Segment Analysis: By Type - CMP Pads

Hard Segment in Chemical Mechanical Planarization (CMP) Pads Market

The hard CMP pad segment continues to dominate the global CMP pad market, commanding approximately 60% of the market share in 2024. Hard CMP pads, primarily manufactured from rigid polyurethane materials, offer superior durability and resistance to wear during aggressive material removal processes in semiconductor manufacturing. These pads are particularly crucial for achieving precise control over material removal rates and meeting the stringent tolerances required in modern semiconductor fabrication. The segment's dominance is largely attributed to the increasing demand for 300mm wafers, where uniform material removal across larger surface areas is essential. Hard CMP pads excel in maintaining consistent performance throughout their lifecycle, making them indispensable for high-volume manufacturing operations. The segment's strength is further reinforced by continuous innovations in micro-texturing technologies that enhance slurry distribution and polishing uniformity, while regular conditioning with diamond-impregnated disks helps maintain optimal surface characteristics for extended periods.

Soft Segment in Chemical Mechanical Planarization (CMP) Pads Market

The soft CMP pad segment is experiencing the highest growth trajectory in the market, with a projected growth rate of approximately 9% during the forecast period 2024-2029. This accelerated growth is primarily driven by the increasing adoption of soft pads in delicate polishing applications, particularly in processes involving low-k dielectrics, copper, and other sensitive materials. The segment's expansion is further fueled by the growing demand for advanced semiconductor devices that require gentler polishing approaches to protect intricate features. Soft CMP pads offer superior defect control and reduced risk of scratching, making them ideal for final polishing stages and applications requiring high precision. The segment's growth is also supported by continuous innovations in pad materials and designs, including refined pad conditioning techniques and enhanced surface treatments. The development of hybrid pads that combine the advantages of both soft and hard materials is creating new opportunities for market expansion, particularly in advanced node semiconductor manufacturing processes.

Segment Analysis: By Device Type

Logic Segment in Chemical Mechanical Planarization (CMP) Slurry and Pad Market

The logic segment maintains its dominant position in the CMP slurry and CMP pad market, commanding approximately 36% market share in 2024. This leadership position is primarily driven by the increasing complexity of logic devices present in nearly all digital devices, ranging from smartphones to arithmetic logic units (ALUs). The segment's growth is substantially supported by the automotive and consumer electronics sectors, as both heavily rely on logic semiconductors. Logic devices play a crucial role in vehicle control and communication systems, finding applications in engine control units (ECUs), transmission control units (TCUs), antilock braking systems, infotainment systems, and airbag control modules. The advancement of digital processing in consumer electronics gadgets like smartphones, TVs, gaming consoles, and smart home devices has further strengthened the segment's position, as these devices heavily depend on digital logic ICs for processing and manipulating digital signals.

Memory Segment in Chemical Mechanical Planarization (CMP) Slurry and Pad Market

The memory segment is projected to exhibit the highest growth rate of approximately 9% during the forecast period 2024-2029. This remarkable growth is attributed to the increasing demand for high-performance memory devices across various applications. The segment's expansion is driven by the rising need for advanced memory solutions in data centers, artificial intelligence applications, and cloud computing infrastructure. The continuous evolution of memory technologies, particularly in DRAM and NAND flash applications, necessitates more sophisticated CMP equipment processes for achieving the required surface planarity and uniformity. The growing adoption of 3D NAND technology and the development of next-generation memory architectures are creating additional demands for specialized CMP solutions, further accelerating the segment's growth trajectory.

Remaining Segments in Device Type Market Segmentation

The analog and other device segments complete the market landscape, each serving distinct applications in the semiconductor industry. The analog segment is particularly significant in applications requiring continuous signal processing, such as automotive sensors, power management systems, and communication devices. These components are essential in various electronic devices where real-world signals need to be processed. The other device segment encompasses various applications including microprocessors, optoelectronic devices, and specialized semiconductor components. This segment plays a crucial role in emerging technologies such as Internet of Things (IoT) devices, advanced driver assistance systems, and industrial automation applications, contributing to the overall market dynamics of CMP slurry and pad solutions.

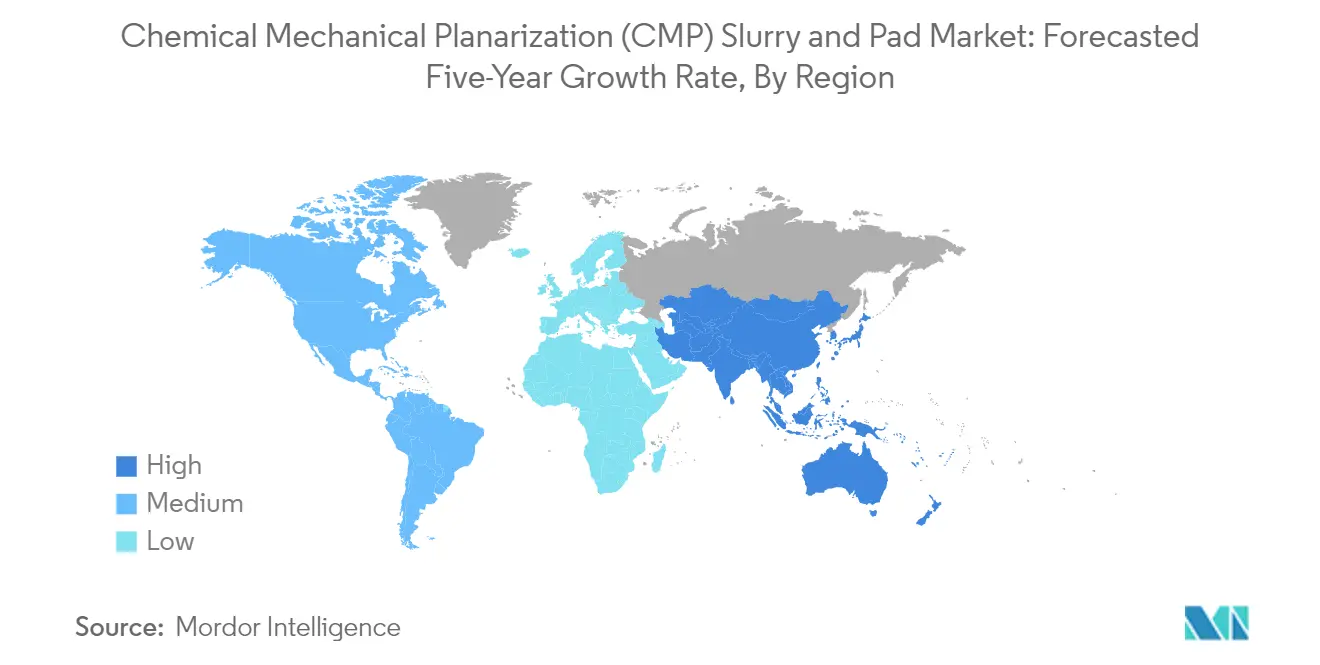

Chemical Mechanical Planarization (CMP) Slurry Market Geography Segment Analysis

Chemical Mechanical Planarization (CMP) Slurry and Pad Market in Taiwan

Taiwan, a semiconductor manufacturing powerhouse, dominates the global CMP market, commanding approximately 25% of the market share in 2024. The country's prominence in the semiconductor materials market is anchored by the presence of industry giants like Taiwan Semiconductor Manufacturing Limited (TSMC) and United Microelectronics Corporation. Taiwan's semiconductor industry contributes significantly to its GDP, with the country producing over 60% of global semiconductors. The continuous expansion of semiconductor fabrication facilities and the increasing complexity of chip manufacturing processes drive the demand for CMP slurry and pads. The region's focus on advanced nodes, particularly in 5nm and 3nm technology, necessitates sophisticated planarization processes, further boosting market growth. The presence of robust research and development facilities, coupled with strong industry-academia collaborations, enables continuous innovation in CMP technologies. Additionally, Taiwan's strategic position in the global semiconductor supply chain and its commitment to maintaining technological leadership contribute to its market dominance.

Chemical Mechanical Planarization (CMP) Slurry and Pad Market in China

China's CMP industry is experiencing remarkable growth, projected to expand at approximately 8% CAGR from 2024 to 2029. The country's aggressive push towards semiconductor self-sufficiency through initiatives like Made in China 2025 has catalyzed substantial investments in the semiconductor equipment market. The establishment of new fabrication facilities and the expansion of existing ones have created a robust demand for CMP consumables. China's focus on developing domestic semiconductor capabilities has attracted both local and international players to the market. The country's strategic emphasis on advanced technology development, particularly in areas such as artificial intelligence, 5G, and electric vehicles, has further accelerated the need for sophisticated semiconductor manufacturing processes. The government's supportive policies, including substantial funding and tax incentives, have created a favorable environment for market growth. Additionally, the increasing presence of domestic semiconductor manufacturers and the growing expertise in advanced manufacturing processes have strengthened China's position in the global CMP market.

Chemical Mechanical Planarization (CMP) Slurry and Pad Market in South Korea

South Korea's CMP market benefits from the country's strong semiconductor manufacturing ecosystem, led by industry giants like Samsung Electronics and SK Hynix. The country's semiconductor sector plays a crucial role in its economy, with continuous investments in research and development driving technological advancement. South Korea's emphasis on memory chip production, particularly in DRAM and NAND flash memory, creates substantial demand for CMP consumables. The country's focus on sustainable manufacturing practices has led to innovations in eco-friendly CMP solutions, exemplified by recent developments in pad recycling technologies. The presence of advanced manufacturing facilities and the continuous upgrade of existing infrastructure support market growth. Furthermore, South Korea's strategic partnerships with international technology providers and its commitment to maintaining its competitive edge in the global semiconductor equipment industry contribute to the market's robustness.

Chemical Mechanical Planarization (CMP) Slurry and Pad Market in Other Countries

The CMP industry extends beyond the major Asian manufacturing hubs to several other significant regions. The United States maintains a strong presence in the market through its advanced research capabilities and strategic investments in semiconductor manufacturing. Japan leverages its expertise in materials science and precision manufacturing to contribute significantly to the market. European countries, particularly Germany and France, are increasingly focusing on developing their semiconductor capabilities through initiatives like the European Chips Act. These regions bring unique strengths to the market, from technological innovation to specialized applications in emerging semiconductor technologies. The diverse geographical spread of the market ensures a robust supply chain and fosters healthy competition, driving continuous innovation and improvement in CMP technologies. The varying regulatory environments and manufacturing priorities across these regions also contribute to the development of specialized solutions tailored to local requirements.

Get Analysis on Important Geographic Markets

Download PDF

Chemical Mechanical Planarization (CMP) Slurry Industry Overview

Top Companies in Chemical Mechanical Planarization (CMP) Slurry Market

The chemical mechanical planarization companies and pad market is characterized by continuous innovation and strategic developments from key players like Entegris, Resonac, AGC, Fujifilm, Fujimi, DuPont, and Merck KGaA. Companies are heavily investing in research and development to enhance their product portfolios, particularly focusing on advanced node semiconductor manufacturing capabilities and specialized solutions for emerging technologies. The industry witnesses frequent capacity expansions and facility investments, especially in Asia-Pacific regions, to meet growing semiconductor demand. Strategic collaborations with semiconductor manufacturers and research institutes have become increasingly common, enabling companies to develop tailored solutions and maintain competitive advantages. Market leaders are emphasizing sustainability initiatives and digital transformation, incorporating advanced technologies like AI and machine learning in their manufacturing processes while simultaneously working on reducing environmental impact through innovative product formulations.

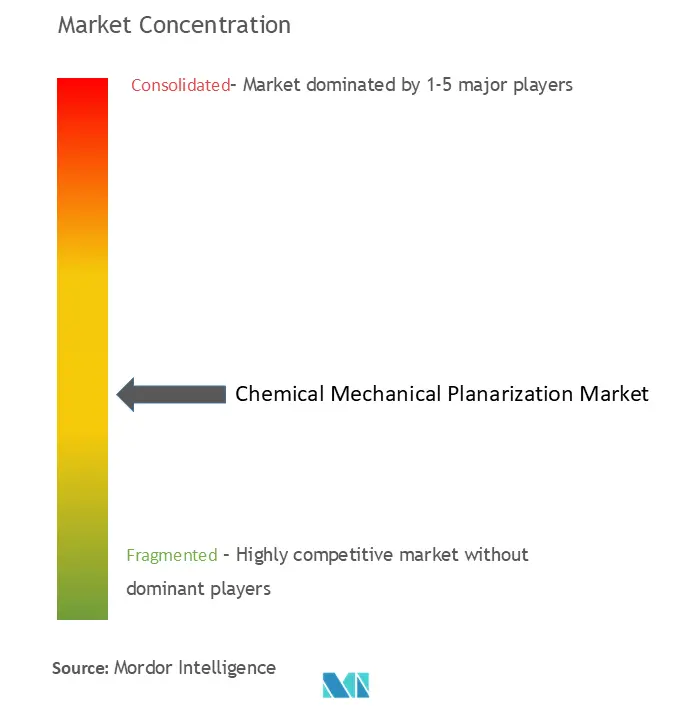

Market Dominated by Global Technology Conglomerates

The CMP slurry and pad market exhibits a moderately consolidated structure, with major global technology conglomerates holding significant CMP market share through their specialized divisions. These companies leverage their extensive research capabilities, global distribution networks, and long-standing relationships with semiconductor manufacturers to maintain their market positions. The market demonstrates a clear geographic concentration in Asia-Pacific, particularly in countries like South Korea, Taiwan, and Japan, where major semiconductor manufacturing facilities are located. This has led to strategic facility establishments and regional headquarters by global players to better serve these markets.

The industry has witnessed notable merger and acquisition activities, with larger companies acquiring specialized manufacturers to enhance their technological capabilities and market reach. Companies are increasingly focusing on vertical integration strategies, developing comprehensive solutions that include both slurries and pads, along with related services and support. Market entry barriers remain high due to the technical complexity of products, stringent quality requirements, and the need for substantial capital investments in research and manufacturing facilities. Regional players, particularly in China, are emerging as significant competitors, supported by government initiatives and increasing domestic semiconductor production capabilities.

Innovation and Customer Relations Drive Success

Success in the CMP slurry and pad market increasingly depends on companies' ability to develop innovative solutions that address the evolving needs of semiconductor manufacturers, particularly in advanced node technologies and emerging applications like 3D ICs. Market leaders are strengthening their positions through continuous investment in research and development, focusing on developing products with enhanced performance characteristics and lower environmental impact. Customer relationship management has become crucial, with successful companies establishing strong technical support networks and collaborative development programs with major semiconductor manufacturers.

For new entrants and smaller players, specialization in specific applications or regional markets offers opportunities for growth. Companies are focusing on developing proprietary technologies and unique value propositions to differentiate themselves in the market. The industry's regulatory environment, particularly regarding environmental standards and chemical safety, continues to influence product development and manufacturing processes. Success also depends on companies' ability to maintain stable supply chains and manage raw material costs effectively, while simultaneously investing in next-generation technologies and maintaining strong quality control systems. The concentration of end-users in the semiconductor industry makes strong customer relationships and technical support capabilities essential for long-term success.

Chemical Mechanical Planarization (CMP) Slurry Market Leaders

-

Applied Materials Inc.

-

Entegris Inc.

-

Ebara Corporation

-

Lapmaster Wolters Gmbh

-

Dupont De Nemours Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Chemical Mechanical Planarization (CMP) Slurry Market News

- April 2024: 3M announced that it was looking to increase its revenue from chemical mechanical polishing (CMP) pads by 300% within three years. The company has developed a micro-replicated CMP pad with asperities and pores, similar to the wafers before polishing, to expand its presence in the market. These pads are likely targeted at 10-nanometer or under processes requiring uniform CMP usage. Additionally, 3M asserts that its pads offer a 30% improvement in polishing efficiency and last 1.5 to 2 times longer than its competitors. Such vendor developments to drive the CMP capabilities are expected to enhance the market’s potential.

- March 2024: SK Hynix expanded its CMP slurry supply for HBM production by partnering with Dongjin Semichem. The new CMP slurry, introduced in January at Semicon Korea 2024, is designed to flatten the charged copper through silicon via (TSV) during HBM production. SK Hynix has shown a strong interest in the CMP slurry sample from Dongjin Semichem, deeming it superior to its competitors. These collaborative efforts between vendors are anticipated to stimulate market growth.

Chemical Mechanical Planarization (CMP) Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Need for Miniaturization of Semiconductors

- 5.1.2 Increasing use of Mems and Nems is Fueling the Growth of the CMP Market

-

5.2 Market Challenges

- 5.2.1 Complexity Regarding Manufacturing

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 CMP Equipment

- 6.1.2 CMP Consumable

- 6.1.2.1 Slurry

- 6.1.2.2 Pad

- 6.1.2.3 Pad Conditioner

- 6.1.2.4 Other Consumable Types

-

6.2 By Application

- 6.2.1 Compound Semiconductors

- 6.2.2 Integrated Circuits

- 6.2.3 Mems and Nems

- 6.2.4 Other Applications

-

6.3 By Geography***

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Applied Materials Inc.

- 7.1.2 Entegris Inc.

- 7.1.3 Ebara Corporation

- 7.1.4 Lapmaster Wolters Gmbh

- 7.1.5 Dupont De Nemours Inc.

- 7.1.6 Fujimi Incorporated

- 7.1.7 Revasum Inc.

- 7.1.8 Resonac Holdings Corporation (Showa Denko Materials)

- 7.1.9 Okamoto Corporation

- 7.1.10 Fujifilm Corporation (Fujifilm Holdings Corporation)

- 7.1.11 Tokyo Seimitsu Co. Ltd (Accretech Create Corp.)

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Chemical Mechanical Planarization (CMP) Slurry Industry Segmentation

The market is defined by the revenue accrued from the sales of chemical mechanical polishing solutions worldwide. The study focuses on various chemical and mechanical polishing equipment and consumables. It also analyzes different trends and dynamics related to protective chemical and mechanical polishing solutions across multiple application areas and geographical regions.

The chemical mechanical planarization market is segmented by type (CMP equipment, CMP consumable [slurry, pad, pad conditioner, other consumable types]), by application (compound semiconductors, integrated circuits, MEMS and NEMS, and other applications), by geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| By Type | CMP Equipment | ||

| CMP Consumable | Slurry | ||

| Pad | |||

| Pad Conditioner | |||

| Other Consumable Types | |||

| By Application | Compound Semiconductors | ||

| Integrated Circuits | |||

| Mems and Nems | |||

| Other Applications | |||

| By Geography*** | North America | ||

| Europe | |||

| Asia | |||

| Australia and New Zealand | |||

| Latin America | |||

| Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Chemical Mechanical Planarization (CMP) Market Research FAQs

How big is the Chemical Mechanical Planarization Slurry Market?

The Chemical Mechanical Planarization Slurry Market size is expected to reach USD 6.53 billion in 2025 and grow at a CAGR of 7.23% to reach USD 9.26 billion by 2030.

What is the current Chemical Mechanical Planarization Slurry Market size?

In 2025, the Chemical Mechanical Planarization Slurry Market size is expected to reach USD 6.53 billion.

Who are the key players in Chemical Mechanical Planarization Slurry Market?

Applied Materials Inc., Entegris Inc., Ebara Corporation, Lapmaster Wolters Gmbh and Dupont De Nemours Inc. are the major companies operating in the Chemical Mechanical Planarization Slurry Market.

Which is the fastest growing region in Chemical Mechanical Planarization Slurry Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Chemical Mechanical Planarization Slurry Market?

In 2025, the Asia Pacific accounts for the largest market share in Chemical Mechanical Planarization Slurry Market.

What years does this Chemical Mechanical Planarization Slurry Market cover, and what was the market size in 2024?

In 2024, the Chemical Mechanical Planarization Slurry Market size was estimated at USD 6.06 billion. The report covers the Chemical Mechanical Planarization Slurry Market historical market size for years: 2024. The report also forecasts the Chemical Mechanical Planarization Slurry Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Chemical Mechanical Planarization (CMP) Slurry Market Research

Mordor Intelligence delivers a comprehensive analysis of the chemical mechanical planarization industry. We leverage our extensive expertise in semiconductor materials and semiconductor equipment research. Our detailed report examines the complete ecosystem of CMP slurry and CMP pad technologies, which are essential components in semiconductor fabrication and wafer manufacturing processes. The analysis encompasses crucial aspects of electronic polishing and semiconductor processing. We focus particularly on advanced packaging applications and integrated circuit manufacturing methodologies. Our research team provides detailed insights into microelectronics processing and wafer planarization techniques. This information is available in an easy-to-download report PDF format.

This authoritative market analysis benefits stakeholders across the semiconductor equipment industry. It delivers actionable insights into CMP equipment trends and semiconductor consumables dynamics. The report examines key aspects of wafer polishing and semiconductor polishing technologies. It also provides a detailed analysis of the CMP pad market and semiconductor materials market. Our comprehensive coverage includes emerging trends in advanced packaging market developments and CMP slurry market innovations. This is supported by extensive data on semiconductor equipment market dynamics. The report offers valuable insights for companies involved in chemical mechanical planarization technologies, enabling informed decision-making in this rapidly evolving sector.