| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 3.78 Billion |

| Market Size (2030) | USD 5.20 Billion |

| CAGR (2025 - 2030) | 6.58 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

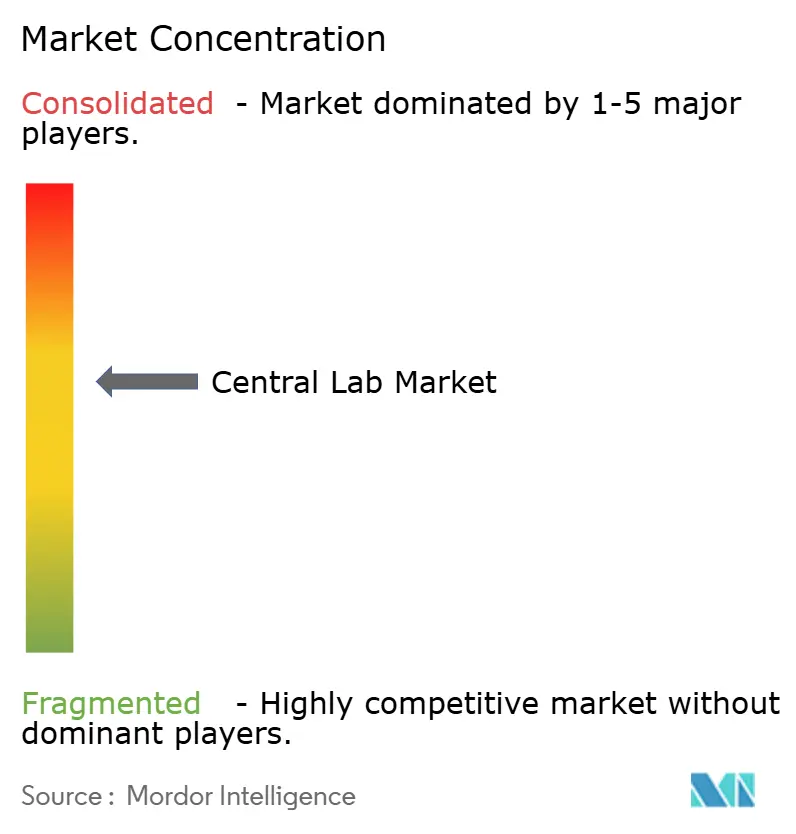

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Central Lab Market Analysis

The Central Lab Market size is estimated at USD 3.78 billion in 2025, and is expected to reach USD 5.20 billion by 2030, at a CAGR of 6.58% during the forecast period (2025-2030).

Central Lab Market Overview

The central laboratory services industry is undergoing a significant transformation, driven by consolidation and strategic partnerships. In 2023, the sector experienced substantial capital inflows. LabCentral reported that its resident and alumni companies collectively secured USD 1.7 billion in funding during the year. This accounted for 28.3% of all early-stage (seed and Series A) bio-pharma financing in Massachusetts and 16.3% of such financing nationwide. Additionally, LabCentral's portfolio companies raised a total of USD 6.05 billion in funding. These companies initiated 132 clinical trials, including 16 launched in 2023. This influx of investment has supported the global expansion of laboratory infrastructure and capabilities. Key industry players are increasingly leveraging strategic alliances and acquisitions to enhance their service offerings and expand their geographical footprint. For instance, Cerba Research entered into a joint venture with Teddy Clinical Research Laboratory in early February 2023 to strengthen its presence in mainland China.

Laboratory automation and digital transformation are reshaping central laboratory operations, with a strong focus on improving efficiency and accuracy. For example, in April 2023 China Association of Clinical Laboratory Practice Expo (CACLP) brought together over 30,000 industry professionals, showcasing advanced automation solutions and digital platforms. The integration of artificial intelligence (AI) and machine learning (ML) into laboratory processes has significantly reduced turnaround times and improved data accuracy. Leading laboratories are implementing advanced Laboratory Information Management Systems (LIMS) and automated sample processing systems to streamline workflows and maintain consistent quality across multiple locations.

The industry is witnessing a growing trend toward outsourcing, with an increasing volume of central laboratory work being assigned to specialized service providers. This shift reflects the rising complexity of clinical trials and the need for specialized expertise to manage diverse testing requirements. Contract research organizations (CROs) are expanding their capabilities to provide comprehensive central laboratory services, including biomarker testing, genomics, and specialized chemistry services. The focus on quality and standardization has driven the development of robust quality management systems (QMS) and standardized operating procedures (SOPs) across global laboratory networks.

Global expansion and cross-border collaborations are transforming the competitive landscape, with laboratories forming strategic partnerships to support multinational clinical trials. In May 2023, LabConnect established a strategic alliance with Labor Dr. Wisplinghoff to enhance central laboratory services in Europe, highlighting the industry's emphasis on building global capabilities. Laboratories are investing in harmonized systems and processes to ensure consistent quality across different regions. Additionally, the industry has seen increased adoption of virtual reporting solutions and cloud-based platforms, enabling real-time data sharing and analysis among global research teams.

Central Lab Market Trends

Increasing Prevalence of Chronic and Infectious Diseases

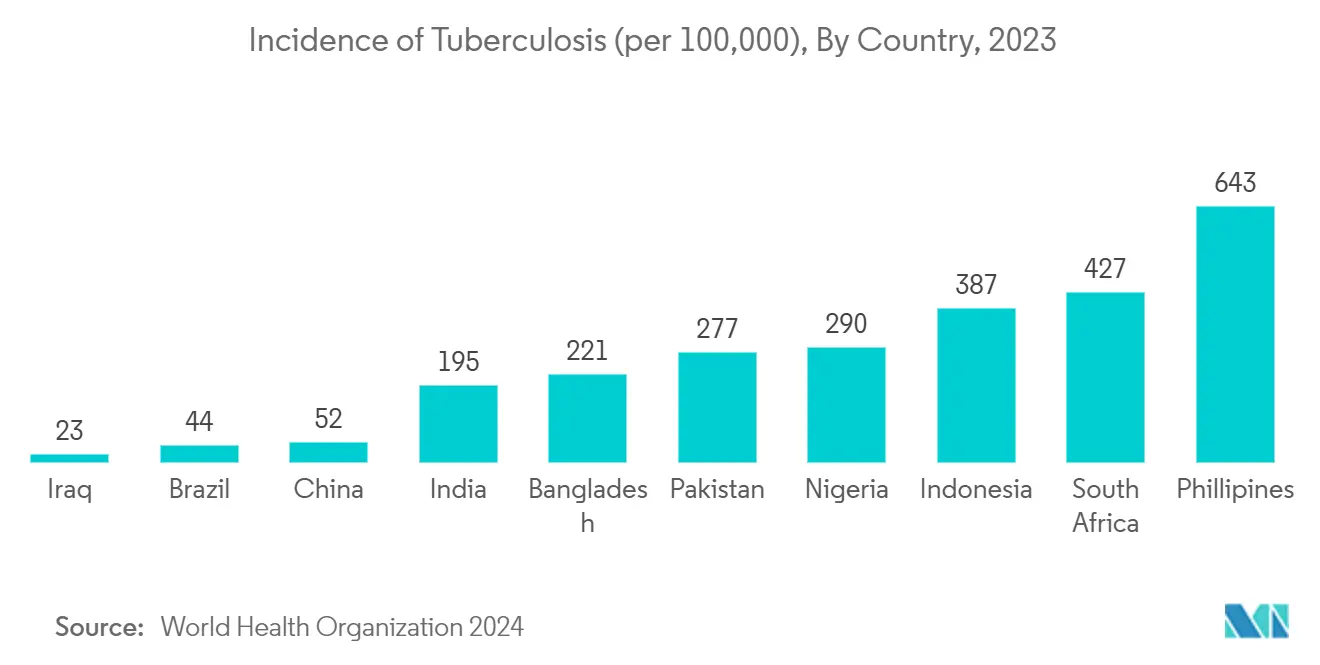

The global rise in chronic and infectious diseases is a key factor propelling the growth of the central laboratory market, as these conditions demand continuous monitoring and specialized diagnostic services. As per the World Health Organization (WHO) fact sheet released in April 2023, approximately 10.6 million individuals were diagnosed with tuberculosis worldwide, including 6 million men, 3.6 million women, and 1.3 million children. This highlights the ongoing challenges in managing infectious diseases, driving the need for advanced diagnostic and monitoring solutions. Similarly, the May 2024 Alzheimer's Association report estimates that the number of Americans aged 65 and older living with Alzheimer's disease will grow from 6.9 million in 2024 to 13.8 million by 2060. This increasing disease burden has prompted central laboratories to diversify their test portfolios and invest in advanced technologies to address complex chronic conditions such as cancer, cardiovascular diseases, and diabetes, which require consistent monitoring and precise diagnostic data to guide critical treatment decisions.

The complexities of chronic disease management have driven central laboratories to design comprehensive testing panels that can simultaneously monitor multiple biomarkers, facilitating improved disease management and treatment optimization. These advanced testing capabilities are crucial for healthcare providers to track disease progression, refine treatment plans, and assess therapeutic effectiveness. Furthermore, the adoption of molecular diagnostics and genetic testing has enhanced the role of central laboratories in chronic disease management, enabling more accurate diagnoses and personalized treatment strategies tailored to individual patient profiles and disease-specific markers.

Technological Advancements

The central lab market is experiencing a transformative phase driven by rapid technological innovations that enhance testing accuracy, efficiency, and throughput capabilities. The integration of artificial intelligence and machine learning algorithms has revolutionized data analysis and interpretation, enabling faster and more accurate test results while reducing human error. Advanced automation systems have significantly improved workflow efficiency, allowing laboratories to handle larger sample volumes while maintaining high-quality standards and reducing turnaround times for critical test results.

The emergence of next-generation sequencing technologies and advanced molecular diagnostic platforms has expanded the capabilities of central laboratories, enabling them to offer more sophisticated testing services. These technological advancements have also facilitated the development of novel biomarker detection methods and improved the sensitivity and specificity of existing tests. The adoption of laboratory information management systems (LIMS) and digital pathology solutions has enhanced data management and sharing capabilities, enabling better collaboration between healthcare providers and improving the overall quality of patient care. Additionally, the integration of cloud-based solutions has improved data storage and accessibility, allowing for better resource management and enhanced operational efficiency.

Growing Demand for Personalized Medicine and Biomarker Research

The growing emphasis on personalized medicine is driving significant growth in the central lab market, as healthcare providers increasingly adopt customized therapeutic approaches tailored to individual patient profiles. This shift has fueled demand for advanced testing services capable of identifying genetic markers, analyzing molecular data, and evaluating drug responses on a personalized level. In response, central laboratories have expanded their capabilities in genetic testing, pharmacogenomics, and biomarker analysis, enabling healthcare providers to make data-driven decisions for optimized patient care.

The progression of precision medicine has compelled central laboratories to enhance their testing methodologies and analytical capabilities. These labs now play a critical role in detecting genetic variations that influence drug metabolism, predicting treatment outcomes, and monitoring therapeutic efficacy. The FDA's forecast of approving 10-20 cell and gene therapy products annually by 2025 highlights the increasing reliance on personalized medicine and the essential role of central laboratories in supporting these innovative therapeutic approaches. This trend has also spurred investments in specialized technologies and expertise to facilitate the development and implementation of personalized treatment protocols.

Rising Clinical Trials, R&D Investment, and Outsourcing By Pharma and Biotech Companies

The growing volume of clinical trial activities worldwide has significantly boosted the demand for central laboratory services. Leading research hubs are conducting thousands of studies annually. Data from ClinicalTrials.Gov indicates that, as of January 2025, the United States accounted for 155,622 clinical trials, while 298,488 trials were conducted outside the U.S. This heightened research activity has compelled central laboratories to enhance their capabilities, catering to requirements such as patient screening, safety monitoring, and efficacy evaluation.

The increasing complexity of clinical trials, particularly in areas such as oncology and rare diseases, has driven the need for more sophisticated laboratory services and specialized testing capabilities. Surge in R&D funding has led to increased demand for sophisticated laboratory services, specialized testing capabilities, and advanced analytical tools necessary for drug development and clinical research activities.

The expansion of R&D activities has prompted central laboratories to enhance their technological capabilities and expand their service offerings to support complex research projects. This includes investments in advanced equipment, development of novel testing methodologies, and expansion of expertise in specialized areas such as biomarker development and validation. The growing focus on developing innovative therapeutics has also led to increased collaboration between central laboratories and pharmaceutical companies, creating new opportunities for service expansion and technological advancement in the laboratory sector.

Central Lab Market Services Segment Analysis

Biomarker Services Segment in Central Lab Market

The biomarker services segment is projected to exhibit the highest growth rate in the central lab market, with an estimated CAGR of 7.26% from 2025 to 2030. This exceptional growth trajectory is primarily fueled by the increasing adoption of personalized medicine approaches and precision diagnostics. The segment's expansion is further accelerated by technological advancements in biomarker discovery and validation techniques. Rising investments in companion diagnostic development and the growing importance of biomarker-driven clinical trials are creating substantial growth opportunities. The integration of novel technologies such as digital biomarkers and multi-omics approaches is revolutionizing disease diagnosis and treatment monitoring capabilities. Furthermore, the increasing application of biomarkers in immunotherapy development and patient stratification is driving segment growth. The emergence of new therapeutic modalities and the focus on targeted therapies have created additional demand for biomarker services. The segment also benefits from increasing regulatory acceptance of biomarker-based endpoints in clinical trials.

Remaining Segments in Central Lab Market

The remaining segments, including Genetic Services, Microbiology Services, and Special Chemistry Services, continue to play vital roles in the central lab market's ecosystem. Genetic services has gained significant traction due to advances in genomic technologies and increasing applications in rare disease diagnostics. Microbiology services maintains steady growth driven by infectious disease testing requirements and antimicrobial resistance studies. Special chemistry services demonstrates consistent performance through specialized testing capabilities and custom analytical solutions. These segments collectively respond to evolving healthcare needs and regulatory requirements, contributing to the market's overall dynamics. The integration of automation and digital solutions across these services has enhanced their operational efficiency and market relevance. Additionally, the increasing focus on quality standards and accreditation requirements has strengthened their market positions. The segments also benefit from growing applications in drug development and safety testing, maintaining their strategic importance in the central lab landscape.

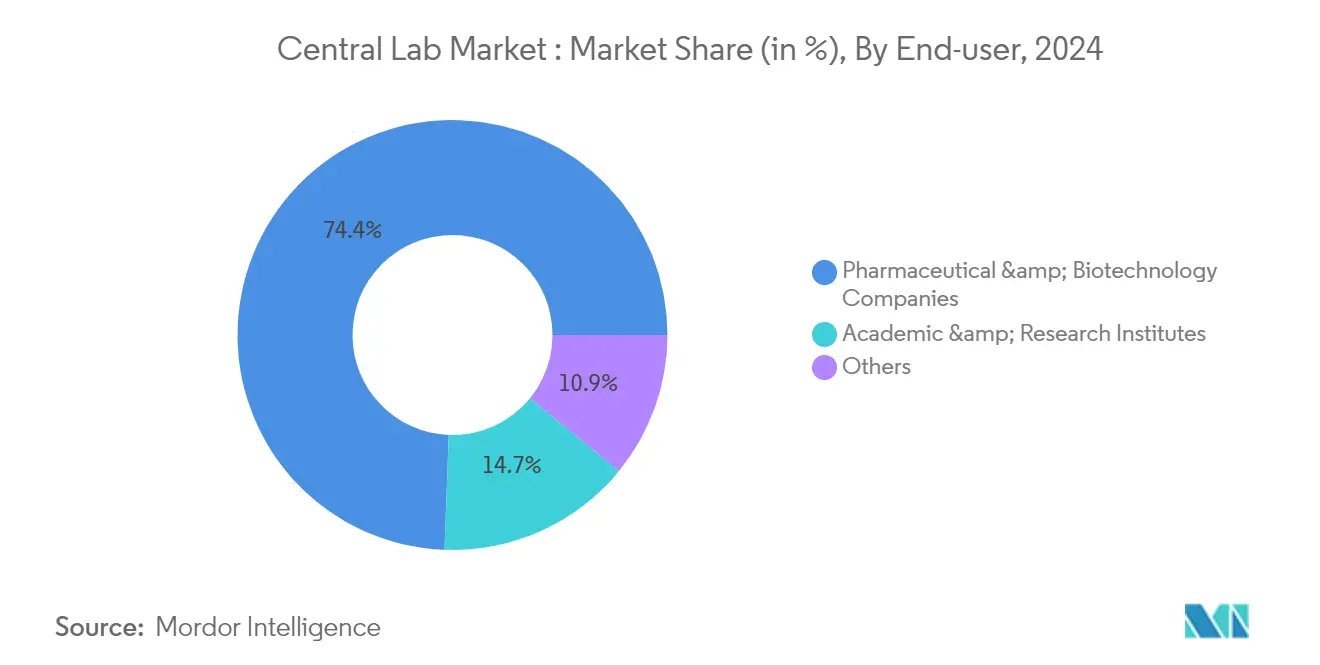

Central Lab Market End-user Segment Analysis

Pharmaceutical and Biotechnology Companies Segment in Central Lab Market

Pharmaceutical and biotechnology companies increasingly depend on central laboratory services, leveraging these specialized facilities for drug development, clinical trials, and meeting regulatory compliance requirements. Across the various phases of clinical trials, these companies require a centralized and standardized testing framework to ensure consistent and accurate data collection across global study sites. Central laboratories perform critical functions such as biomarker analyses, pharmacokinetic and pharmacodynamic studies, genetic testing, immunogenicity assessments, and safety monitoring to evaluate drug efficacy and patient responses.

Furthermore, these companies must comply with stringent regulatory standards set by agencies such as the U.S. Food and Drug Administration (FDA), European Medicines Agency (EMA), and International Council for Harmonisation (ICH). Central laboratories support compliance by adhering to Good Laboratory Practices (GLP) and Good Clinical Practices (GCP), ensuring trial data is reliable and reproducible.

As the pharmaceutical and biotechnology sectors increasingly focus on personalized medicine and biologics, the demand for advanced genomic testing, next-generation sequencing (NGS), and biomarker-driven studies continues to grow. Central laboratories provide specialized expertise in these areas, enabling companies to optimize drug formulations, predict patient responses, and accelerate the regulatory approval process. Additionally, outsourcing laboratory services to central laboratories allows pharmaceutical companies to concentrate on their core competencies, reduce infrastructure expenses, and streamline research and development (R&D) operations.

With the globalization of clinical trials, pharmaceutical and biotechnology companies require centralized, high-quality laboratory testing services that deliver uniform methodologies across different regions. This ensures standardized and reliable data, enhancing the efficiency of drug development and solidifying the role of central laboratory services as a critical component of modern pharmaceutical research.

Central Lab Market Services Segment Analysis

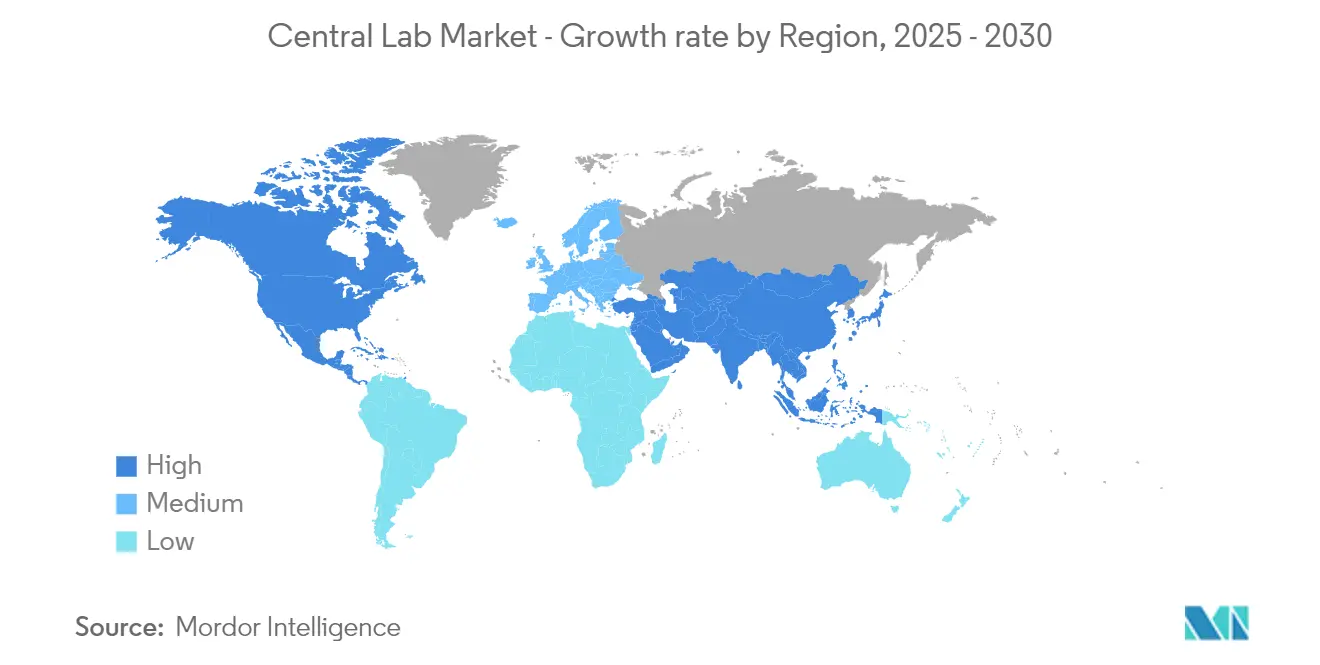

Central Lab Market in North America

North America maintains its dominant position in the global central lab market, commanding approximately 40% of the market share in 2024. The region's leadership is underpinned by its robust healthcare infrastructure, extensive network of research institutions, and presence of major pharmaceutical and biotechnology companies. The United States, in particular, serves as a hub for clinical trials and innovative research activities, supported by favorable regulatory frameworks and substantial healthcare investments. The region's market is characterized by early adoption of advanced diagnostic technologies, strong focus on precision medicine, and increasing demand for specialized testing services. Additionally, the presence of well-established central laboratory service providers, coupled with high healthcare expenditure and sophisticated reimbursement systems, continues to drive market growth. The region also benefits from strong collaboration between academic institutions, research organizations, and industry players, fostering innovation and development of new testing methodologies.

Central Lab Market in Europe

Europe represents a sophisticated and mature market in the global central lab landscape, projected to grow at significant CAGR from 2025 to 2030. The region's market is characterized by its strong emphasis on research and development, particularly in countries like Germany, France, and the United Kingdom. European central labs benefit from advanced healthcare systems, stringent quality standards, and robust regulatory frameworks that ensure high-quality testing services. The market is witnessing significant developments in specialized testing capabilities, particularly in areas such as biomarker testing and genetic analysis. The presence of leading pharmaceutical companies and research institutions continues to drive demand for central lab services. The region's focus on innovative healthcare solutions and personalized medicine approaches is creating new opportunities for market expansion. Additionally, increasing collaboration between academic institutions and industry players is fostering innovation in testing methodologies and service delivery models. The market also benefits from strong intellectual property protection and established networks of clinical research organizations.

Central Lab Market in Asia Pacific

The Asia Pacific region has emerged as a dynamic growth center in the global central lab market, demonstrating remarkable expansion with approximately 8% growth rate from 2025 to 2030. The region's evolution is driven by rapid healthcare infrastructure development, increasing research and development activities, and growing investment in clinical trials. Countries like China, Japan, and India are becoming preferred destinations for clinical research, supported by large patient populations and cost-effective research environments. The market is witnessing significant transformation through the adoption of advanced diagnostic technologies and increasing focus on personalized medicine approaches. Local governments' supportive policies and initiatives to promote healthcare research and development are creating favorable conditions for market expansion. The region's growing biotechnology and pharmaceutical sectors, combined with increasing healthcare awareness and expenditure, are creating substantial opportunities for central lab service providers. Furthermore, the emergence of specialized testing facilities and increasing collaboration with global research organizations are enhancing the region's capabilities in clinical testing services.

Central Lab Market in Middle East and Africa

The Middle East and Africa region presents unique opportunities in the central lab market, characterized by rapid development of healthcare infrastructure and increasing focus on research capabilities. The market is witnessing transformation through significant investments in healthcare facilities, particularly in Gulf Cooperation Council (GCC) countries. Growing awareness about the importance of clinical research and quality diagnostic services is driving market development. The region is increasingly participating in global clinical trials, supported by improving regulatory frameworks and growing healthcare expenditure. Local governments are implementing initiatives to attract international healthcare investments and develop domestic research capabilities. The market is also benefiting from increasing collaboration with international research organizations and growing emphasis on developing specialized testing capabilities. Furthermore, the region's unique genetic diversity and disease patterns make it an important destination for specific types of clinical research. The development of medical cities and healthcare clusters, particularly in GCC countries like Saudi Arabia and the UAE, is creating new opportunities for central laboratory services.

Central Lab Market in South America

South America is emerging as a promising market for central laboratory services, driven by increasing investment in healthcare infrastructure and growing clinical research activities. The region is witnessing significant developments in its healthcare ecosystem, particularly in countries like Brazil and Argentina, where there is growing emphasis on improving research capabilities and diagnostic services. The market is characterized by increasing adoption of international quality standards and growing participation in global clinical trials. Local governments are implementing supportive policies to attract international research organizations and promote domestic research capabilities. The region's large and diverse patient population makes it an attractive destination for clinical trials, particularly in therapeutic areas relevant to the local population. Furthermore, increasing collaboration with global pharmaceutical companies and research organizations is helping to enhance the technical capabilities and service offerings of local central laboratories. The market is also benefiting from growing awareness about the importance of quality diagnostic services and increasing healthcare expenditure.

Central Lab Industry Overview

Top Companies in Central Lab Market

The central lab market is led by key players including ACM Global Laboratories, CIRION BioPharma Research, Eurofins Scientific, ICON plc, Intermountain Health, IQVIA, LabConnect, Labcorp, Medpace, Reprocell, SGS S.A., and Thermo Fisher Scientific. These companies demonstrate consistent focus on expanding their technological capabilities and service portfolios through strategic initiatives. The industry witnesses regular product innovations particularly in areas of biomarker testing, genetic analysis, and specialized testing services. Operational agility is demonstrated through the adoption of automated systems, digital pathology solutions, and advanced data management platforms. Companies are actively pursuing geographic expansion through both organic growth and strategic partnerships, with particular focus on emerging markets in Asia Pacific and South America. The market also sees continuous investment in research and development to enhance testing capabilities and develop novel assay methods.

Market Structure Shows Strategic Consolidation Patterns

The central lab market exhibits a moderately consolidated structure with a mix of global conglomerates and specialized regional players. Global players leverage their extensive networks, comprehensive service portfolios, and strong financial capabilities to maintain market leadership, while regional specialists thrive by offering customized solutions and maintaining strong local relationships. The market demonstrates active merger and acquisition activity, with larger players acquiring specialized laboratories to expand their service offerings and geographic presence. Strategic partnerships between central labs and pharmaceutical companies are increasingly common, creating integrated service models that support complex clinical trials and research programs.

The competitive dynamics are characterized by a balance between established multinational corporations and emerging specialized providers. Market consolidation is driven by the need to achieve economies of scale, expand service capabilities, and enhance geographic reach. Recent years have witnessed increased collaboration between central labs and technology providers to incorporate advanced analytical capabilities and digital solutions. The industry also sees growing partnerships between central labs and academic institutions, fostering innovation and expanding research capabilities.

Innovation and Adaptability Drive Future Success

Success in the central lab market increasingly depends on the ability to offer comprehensive, technologically advanced services while maintaining operational efficiency. Incumbents must focus on continuous innovation in testing methodologies, investment in advanced technologies, and development of specialized expertise in emerging therapeutic areas. Market leaders need to balance geographic expansion with service quality standardization, while developing strong relationships with pharmaceutical and biotechnology companies. The ability to handle complex trial designs, manage large data volumes, and provide rapid, accurate results will become increasingly critical for maintaining competitive advantage.

For emerging players and contenders, success lies in identifying and serving niche markets, developing specialized expertise, and leveraging technological innovations to improve service delivery. Companies must focus on building robust quality management systems, establishing strong data management capabilities, and developing flexible operational models to adapt to changing market demands.

Central Lab Market Leaders

-

ACM Global Laboratories

-

Eurofins Scientific

-

ICON plc

-

Labcorp

-

Thermo Fisher Scientific

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Central Lab Market News

- February 2025: LabConnect, a global frontrunner in central laboratory services, has opted for Sapio LIMS (Laboratory Information Management System) from Sapio Sciences. This move aims to digitally revolutionize intricate research workflows, simplify sample tracking, and bolster data management.

- June 2024: Thermo Fisher Scientific, Inc. announced the expansion of its central laboratory operations in Kentucky with an investment of USD 47.8 million to accelerate the delivery of safe and effective medicines to patients. The new 65,000-square-foot space will help expand sample management and biorepository operations.

- May 2024: Intermountain Health expanded its Central Lab facility, bringing state-of-the-art testing and advanced diagnostic technologies to enhance lab services and reduce testing costs.

- July 2023: Versiti announced the acquisition of Quantigen, an Indiana-based company, to expand its clinical trial and service offerings in the central lab space.

Central Lab Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic and Infectious Diseases

- 4.2.2 Technological Advancements

- 4.2.3 Growing Demand for Personalized Medicine and Biomarker Research

- 4.2.4 Rising Clinical Trials, R&D Investment, and Outsourcing By Pharma and Biotech Companies

-

4.3 Market Restraints

- 4.3.1 High Operational Costs and Complex Regulatory Requirements

- 4.3.2 Clinical Trial and Logistical Challenges

-

4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

-

5.1 By Services

- 5.1.1 Biomarker Services

- 5.1.2 Genetic Services

- 5.1.3 Microbiology Services

- 5.1.4 Special Chemistry Services

- 5.1.5 Anatomic Pathology/Histology

- 5.1.6 Specimen Management & Storage

- 5.1.7 Other Services

-

5.2 End-user

- 5.2.1 Pharmaceutical and Biotechnology Companies

- 5.2.2 Academic & Research Institutes

- 5.2.3 Others

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 ACM Global Laboratories

- 6.1.2 CIRION BioPharma Research

- 6.1.3 Eurofins Scientific

- 6.1.4 ICON plc

- 6.1.5 Intermountain Health

- 6.1.6 IQVIA

- 6.1.7 LabConnect

- 6.1.8 Labcorp

- 6.1.9 Medpace

- 6.1.10 Reprocell

- 6.1.11 SGS S.A.

- 6.1.12 Thermo Fisher Scientific

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape Covers - Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Central Lab Industry Segmentation

As per the scope of the report, central lab is a specialized laboratory facility that provides standardized testing, sample analysis, and data management services for clinical trials, pharmaceutical research, and diagnostics. These labs ensure consistent, high-quality, and regulatory-compliant testing across multiple study sites, enabling pharmaceutical and biotech companies, contract research organizations (CROs), and healthcare providers to obtain reliable results.

The central lab market is segmented as services, end-user, and geography. By services, the market is segmented as biomarker services, genetic services, microbiology services, special chemistry services, anatomic pathology/histology, specimen management & storage, and other services. By End-user, the market is segmented as pharmaceutical & biotechnology companies, academic & research institutes and Others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions, globally. The report offers the value (in USD) for the above-mentioned segments.

| By Services | Biomarker Services | ||

| Genetic Services | |||

| Microbiology Services | |||

| Special Chemistry Services | |||

| Anatomic Pathology/Histology | |||

| Specimen Management & Storage | |||

| Other Services | |||

| End-user | Pharmaceutical and Biotechnology Companies | ||

| Academic & Research Institutes | |||

| Others | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Central Lab Market Research Faqs

How big is the Central Lab Market?

The Central Lab Market size is expected to reach USD 3.78 billion in 2025 and grow at a CAGR of 6.58% to reach USD 5.20 billion by 2030.

What is the current Central Lab Market size?

In 2025, the Central Lab Market size is expected to reach USD 3.78 billion.

Which is the fastest growing region in Central Lab Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Central Lab Market?

In 2025, the North America accounts for the largest market share in Central Lab Market.

What years does this Central Lab Market cover, and what was the market size in 2024?

In 2024, the Central Lab Market size was estimated at USD 3.53 billion. The report covers the Central Lab Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Central Lab Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Central Lab Industry Report

Statistics for the 2025 Central Lab market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Central Lab analysis includes a market forecast outlook for 2025 to 2030 and historical overview. Get a sample of this industry analysis as a free report PDF download.