Cement Board Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

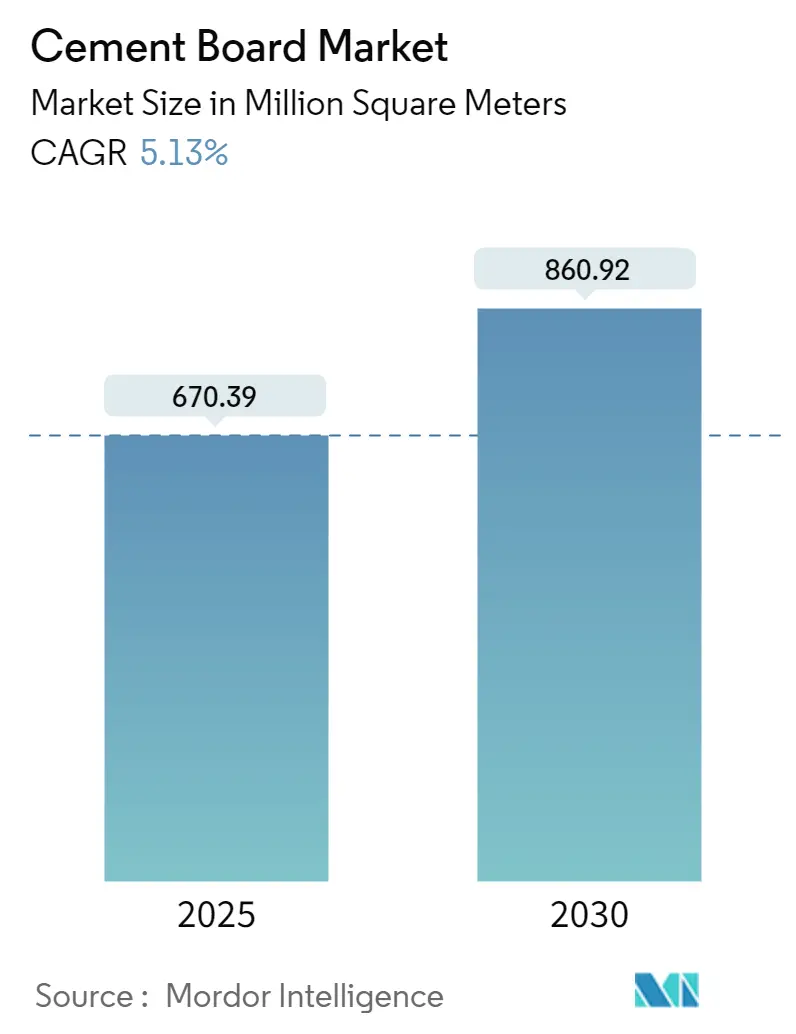

| Market Volume (2025) | 670.39 Million square meters |

| Market Volume (2030) | 860.92 Million square meters |

| Growth Rate (2025 - 2030) | 5.13% CAGR |

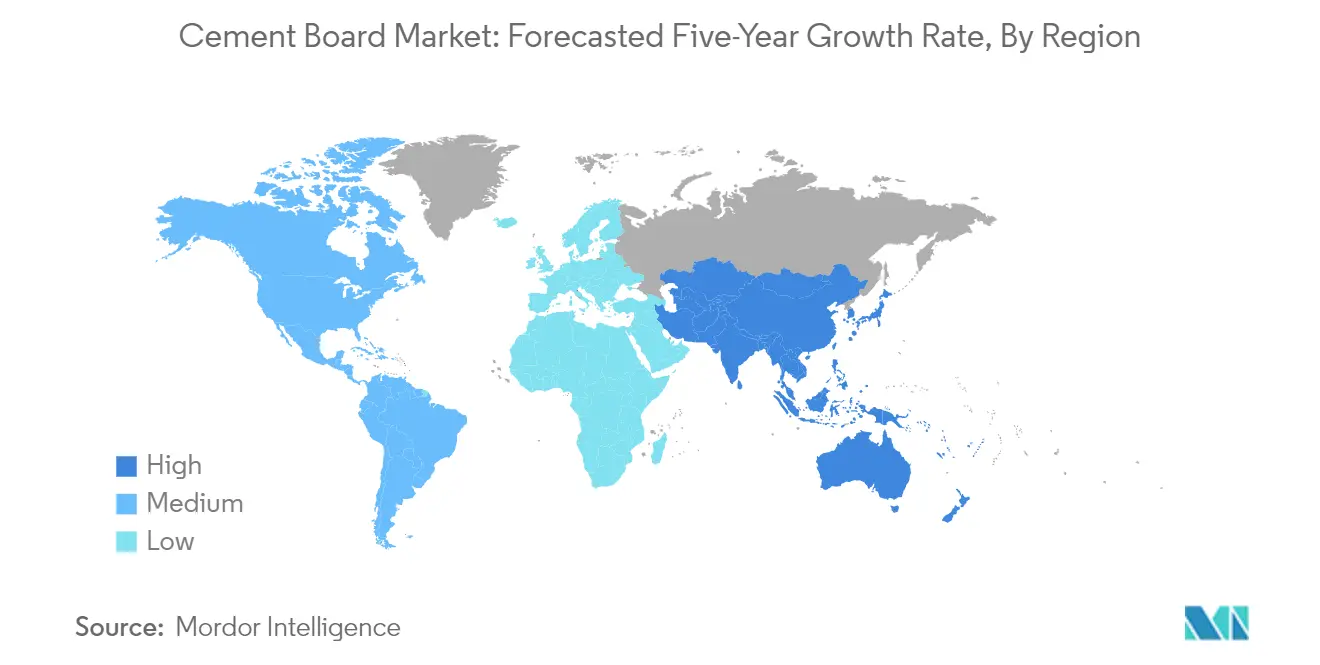

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

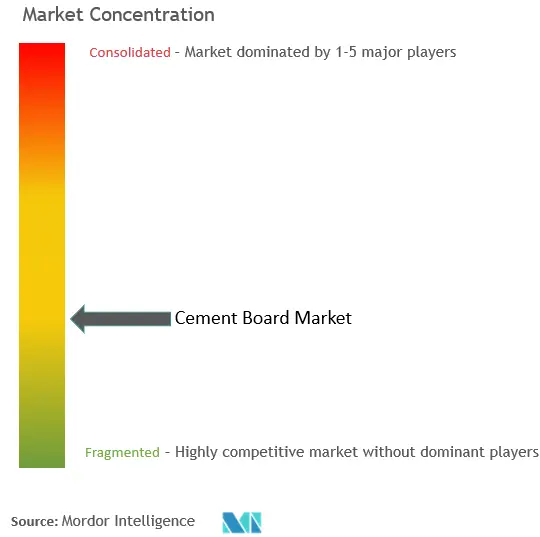

| Market Concentration | Low |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cement Board Market Analysis by Mordor Intelligence

The Cement Board Market size is estimated at 670.39 million square meters in 2025, and is expected to reach 860.92 million square meters by 2030, at a CAGR of 5.13% during the forecast period (2025-2030).

The global construction industry is experiencing significant transformation driven by technological advancements and changing market dynamics. The construction sector has shown remarkable resilience, with the United States witnessing a notable increase in construction businesses to 3,787,470 in 2023, representing a 2.5% growth from the previous year. Advanced manufacturing techniques and automation are revolutionizing construction practices, leading to improved efficiency and reduced waste in cement board production and installation. The integration of digital technologies, including Building Information Modeling (BIM) and automated quality control systems, is reshaping how cement boards are designed, manufactured, and implemented in construction projects.

The industry is witnessing a strong shift towards sustainable and environmentally conscious construction practices. Construction output in the European Union maintained stability throughout 2022, with building permits increasing in nine EU countries, including significant rises in Malta (+29%), Spain (+28%), and Croatia (+21%). This trend is accompanied by a growing emphasis on green building certifications and environmental compliance, pushing manufacturers to develop eco-friendly cement board variants. The focus on sustainability has led to innovations in raw material sourcing and manufacturing processes, with companies increasingly incorporating recycled materials and implementing energy-efficient production methods.

Infrastructure development continues to drive market dynamics, particularly in emerging economies. Saudi Arabia's construction sector recorded its highest growth of 8.8% in 2022, demonstrating robust development in the Middle East region. The surge in infrastructure projects, particularly in urban development and transportation, has created substantial opportunities for cement board applications. Major construction firms are forming strategic partnerships and joint ventures to strengthen their market presence and enhance their technological capabilities, leading to improved product offerings and expanded distribution networks.

The market is experiencing significant evolution in product development and application techniques. In France, building permits reached 44,600 in June 2023, reflecting the growing construction activity in developed markets. Manufacturers are investing in research and development to enhance product characteristics such as durability, fire resistance, and acoustic properties. The industry is witnessing increased customization in product offerings, with manufacturers developing specialized fiber cement board for specific applications such as moisture-resistant variants for bathrooms and impact-resistant versions for high-traffic areas. This specialization trend is accompanied by improvements in installation techniques and the development of complementary products, creating comprehensive building solution systems.

Global Cement Board Market Trends and Insights

Increasing Demand from Residential Construction Sector

The global cement board market is experiencing substantial growth driven by increasing residential construction activities worldwide, particularly in developing economies. The rising urbanization rates, exemplified by China's ambitious target of achieving 70% urbanization by 2030, are creating significant demand for housing and residential infrastructure. This demographic shift, coupled with the growing middle-class population's desire to improve living conditions, has led governments worldwide to implement various housing development initiatives. For instance, India's 'Housing for All' initiative successfully delivered over 20 million affordable homes for urban residents in 2022, demonstrating the massive scale of residential construction activities in developing nations.

The residential construction sector's robust growth is further evidenced by numerous ongoing and planned development projects across major economies. In the United States, the commercial construction sector demonstrated remarkable growth, with construction value reaching USD 115 billion in 2022, marking a significant 21.4% increase from the previous year. The Asia-Pacific region has emerged as a particularly dynamic market, with extensive development plans including 444 planned hotels with 111,798 rooms in 2022, followed by 179 properties with 43,735 rooms in 2023, and 515 hotels with 127,104 rooms confirmed for 2024. These developments, combined with China's ambitious plans to expand from 4,000 shopping centers to add 7,000 more by 2025, highlight the substantial growth in construction activities that directly drive demand for cement boards.

Desirable Properties of Impact Resistance and Durability

Cement boards have gained significant market traction due to their superior physical properties, particularly their exceptional impact resistance and durability compared to traditional building materials. These boards are engineered to withstand severe weather conditions, making them ideal for both interior and exterior cladding applications in construction projects. The material's inherent strength and durability make it particularly valuable in high-traffic areas and regions prone to extreme weather conditions, while its fire-resistant properties enhance building safety standards. Additionally, cement boards offer excellent moisture resistance, making them ideal for wet areas and exterior applications, which significantly expands their utility in various construction scenarios.

The versatility of cement boards is further enhanced by their ability to maintain structural integrity under varying environmental conditions. Their resistance to warping, rotting, and pest infestation makes them a superior alternative to traditional wood-based materials, particularly in long-term applications. The material's durability translates to reduced maintenance requirements and longer service life, making it increasingly attractive to builders and developers focused on sustainable construction practices. Furthermore, cement boards' ability to withstand high-pressure water exposure and resist mold and mildew growth makes them particularly valuable in bathroom and kitchen installations, as well as in exterior cladding applications where weather resistance is crucial. These desirable properties have made cement boards an increasingly popular choice in both residential and commercial construction projects, driving market growth across various applications.

Segment Analysis: Product Type

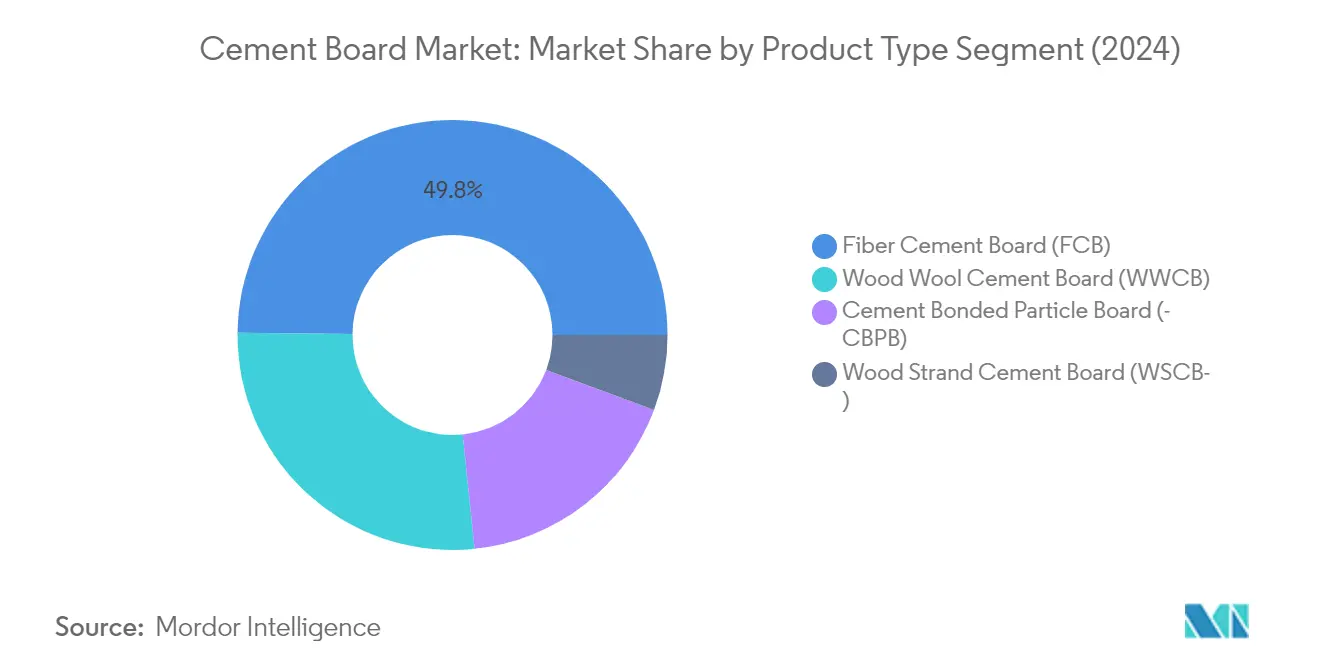

Fiber Cement Board Segment in Cement Board Market

The fiber cement board (FCB) segment dominates the global cement board market, holding approximately 50% market share in 2024. FCB's market leadership is driven by its superior characteristics, including high durability, impact resistance, and versatility in both residential and commercial applications. The segment's growth is particularly strong in exterior applications like cladding and roofing, where its weather resistance and low maintenance requirements make it an ideal choice. FCB's popularity is further enhanced by its fire-resistant properties and excellent performance in wet conditions, making it particularly suitable for bathroom and kitchen applications. The segment is also experiencing the highest growth rate of around 6% for the forecast period 2024-2029, driven by increasing adoption in modern construction projects and growing awareness of its environmental benefits compared to traditional building materials.

Remaining Segments in Product Type Segmentation

The Wood Wool Cement Board (WWCB) segment represents the second-largest share in the market, valued for its excellent acoustic properties and thermal insulation capabilities, making it particularly popular in commercial and institutional buildings. The cement bonded particle board (CBPB) segment maintains a significant presence in the market, particularly in applications requiring high dimensional stability and moisture resistance. The Wood Strand Cement Board (WSCB) segment, while smaller, serves specialized applications where higher structural strength is required, particularly in load-bearing applications and high-performance construction projects. Each of these segments contributes uniquely to the market, serving specific construction needs and applications, from sound insulation to structural support.

Segment Analysis: Application

Exterior and Partition Walls Segment in Cement Board Market

The exterior wall board and partition walls segment dominates the global cement board market, accounting for approximately 33% of the total market share in 2024. This significant market position is driven by the segment's versatility and essential role in both residential and commercial construction. Cement boards are increasingly preferred for wall partitions due to their superior properties, including fire resistance, moisture resistance, and durability compared to traditional brick-and-mortar construction. The segment's dominance is further strengthened by the growing trend toward prefabricated and modular construction methods, where cement boards offer significant advantages in terms of installation speed and cost-effectiveness. Additionally, the rising demand for energy-efficient building solutions has boosted the adoption of cement boards in exterior wall applications, as they provide excellent insulation properties and contribute to sustainable building practices.

Exterior and Partition Walls Segment in Cement Board Market - Growth Analysis

The exterior and partition walls segment is projected to maintain its position as the fastest-growing segment in the cement board market, with an expected growth rate of approximately 6% during 2024-2029. This robust growth is primarily driven by the increasing adoption of modern construction techniques and the growing emphasis on sustainable building materials. The segment's growth is further supported by the rising demand for quick and efficient construction solutions in both residential and commercial sectors. Technological advancements in cement board manufacturing have led to improved product characteristics, making them more attractive for exterior and partition wall applications. The segment is also benefiting from the global trend toward urbanization and the subsequent need for rapid construction solutions that offer both durability and aesthetic appeal.

Remaining Segments in Application Segmentation

The cement board market encompasses several other significant application segments, including facades, weatherboard, and cladding, which represents the second-largest application area, followed by columns and beams, acoustic and thermal insulation, flooring, and roofing applications. Each of these segments serves specific construction needs and contributes uniquely to the market's diversity. The facades segment particularly stands out for its architectural applications and aesthetic versatility, while the columns and beams segment is crucial for structural applications. The acoustic and thermal insulation segment is gaining importance due to increasing focus on building energy efficiency, while flooring applications benefit from cement boards' durability and moisture resistance. The roofing segment, though smaller, remains essential for specific construction requirements, particularly in regions with extreme weather conditions.

Segment Analysis: End-User Industry

Commercial Segment in Cement Board Market

The commercial segment has emerged as the dominant force in the global cement board market, commanding approximately 51% of the total market share in 2024. This segment's prominence is driven by increasing investments in office spaces, retail establishments, hotels, and other commercial buildings worldwide. The segment is experiencing robust growth due to several major commercial construction projects, particularly in the Asia-Pacific region, where rapid urbanization and economic development are fueling demand. For instance, China has nearly 4,000 shopping centers, with an estimated 7,000 more planned to open by 2025. The commercial segment is also witnessing significant expansion in North America, where, according to the American Hotel & Lodging Association, hotel construction and renovation activities have increased substantially to meet growing tourism and business needs. Additionally, various European countries are investing heavily in commercial infrastructure development, with multiple office projects and retail spaces under construction, further solidifying the segment's market leadership.

Growth Trajectory of Commercial Segment

The commercial segment is projected to maintain its growth momentum during the forecast period 2024-2029, with an expected growth rate of approximately 6%. This accelerated growth is attributed to the increasing number of commercial construction projects globally, particularly in emerging economies. The segment's expansion is supported by various factors, including the rise in corporate office spaces, shopping malls, and hospitality sector developments. In the United States alone, construction firms have reported a 2.5% increase in commercial construction businesses in 2023, indicating a strong growth trajectory. The segment is further bolstered by significant investments in retail infrastructure, with major developments occurring in countries like India, where projects such as the Commerz III Commercial Office Complex worth USD 900 million are underway. The trend towards sustainable and energy-efficient commercial buildings is also driving the adoption of cement composite board in this segment, as they offer superior durability and environmental benefits.

Remaining Segments in End-User Industry

The residential and industrial & institutional segments complete the cement board market's end-user industry landscape, each serving distinct market needs. The residential segment maintains a significant presence in the market, driven by increasing housing construction activities and government initiatives for affordable housing across various regions. This segment particularly benefits from the growing trend of using cement boards in modern residential construction for both interior and exterior applications. The industrial & institutional segment, while smaller in market share, plays a crucial role in serving specialized construction needs for factories, educational institutions, healthcare facilities, and other institutional buildings. This segment is characterized by large-scale projects requiring high-performance construction materials, particularly in developing economies where industrial and institutional infrastructure development is gaining momentum.

Cement Board Market Geography Segment Analysis

Cement Board Market in Asia-Pacific

The Asia-Pacific region represents the largest cement board market globally, driven by rapid urbanization and extensive construction activities across residential, commercial, and industrial sectors. China leads the regional market, followed by significant contributions from India, Japan, and South Korea. The region's growth is supported by increasing investments in infrastructure development, rising disposable incomes, and government initiatives promoting sustainable construction practices. Countries like Indonesia, Thailand, and Singapore are also witnessing increased adoption of fiber cement board in various applications, including facades, partitions, and flooring systems.

Cement Board Market in China

China dominates the Asia-Pacific cement board market with approximately 37% market share in 2024. The country's construction sector has maintained robust growth through various initiatives, including the development of smart cities and sustainable urban planning. The housing authorities of Hong Kong have implemented measures to accelerate low-cost housing construction, aiming to provide 301,000 public housing units by 2030. China's commitment to modern construction techniques and materials has led to increased adoption of cement board in both residential and commercial applications, particularly in regions experiencing rapid urbanization and infrastructure development.

Growth Dynamics in Chinese Cement Board Market

China is projected to maintain its position as the fastest-growing market in the Asia-Pacific region, with an expected growth rate of approximately 6% during 2024-2029. The country's growth is driven by massive construction plans, including provisions for the movement of rural populations to new megacities. The expansion of shopping centers, with plans for 7,000 new facilities by 2025, further supports market growth. Additionally, the government's focus on sustainable building practices and energy-efficient construction has increased the demand for fiber cement board in various applications, particularly in exterior walls and facade systems.

Cement Board Market in North America

The North American cement board market is characterized by strong demand from both residential and commercial construction sectors, with significant contributions from the United States, Canada, and Mexico. The region's market is driven by increasing renovation activities, growing awareness about sustainable building materials, and stringent building safety regulations. The construction industry's adoption of modern building materials and techniques has further accelerated the use of cement board across various applications, particularly in moisture-prone areas and exterior cladding systems.

Cement Board Market in United States

The United States maintains its position as the largest cement board market in North America, holding approximately 67% of the regional market share in 2024. The country's construction sector has shown remarkable resilience, supported by various infrastructure development initiatives and housing projects. The US government's allocation of over USD 110 billion for modernizing airports, ports, and rebuilding roads and bridges has created substantial opportunities for cement board applications. The residential construction sector remains particularly strong, with significant ongoing projects in major metropolitan areas.

Growth Dynamics in United States Cement Board Market

The United States is expected to maintain the highest growth rate in North America, with an anticipated growth of approximately 6% during 2024-2029. This growth is supported by increasing investments in commercial and residential construction projects, including significant developments in healthcare facilities and educational institutions. The country's focus on sustainable construction practices and energy-efficient building materials has further boosted the demand for cement board. The expansion of commercial spaces and ongoing urban development projects continue to drive market growth across various applications.

Cement Board Market in Europe

The European cement board market demonstrates a mature and sophisticated landscape, with significant contributions from Germany, France, the United Kingdom, and Italy. The region's focus on sustainable construction practices and energy-efficient building materials has driven the adoption of cement board across various applications. The market benefits from stringent building regulations and increasing renovation activities across both residential and commercial sectors.

Cement Board Market in Germany

Germany maintains its position as the largest cement board market in Europe, driven by its robust construction industry and strong emphasis on quality building materials. The country's construction sector has shown resilience despite economic challenges, particularly in the commercial and industrial segments. The government's initiatives towards sustainable construction and energy-efficient buildings have further strengthened the market for cement board in various applications.

Growth Dynamics in German Cement Board Market

Germany leads the European market in terms of growth potential, supported by ongoing infrastructure development projects and increasing renovation activities. The country's focus on modern construction techniques and sustainable building materials has created substantial opportunities for cement board applications. The commercial construction sector, particularly in office spaces and industrial facilities, continues to drive market growth, while residential construction maintains steady demand for cement board in various applications.

Cement Board Market in South America

The South American cement board market is experiencing steady growth, driven by increasing construction activities across residential and commercial sectors. Brazil, Argentina, and other countries in the region are witnessing growing adoption of fiber cement board in various applications. Brazil emerges as both the largest and fastest-growing market in the region, supported by government initiatives and increasing investments in construction projects. The region's focus on modern construction techniques and sustainable building materials continues to drive market growth.

Cement Board Market in Middle East and Africa

The Middle East and Africa cement board market is witnessing significant growth potential, driven by extensive construction activities across residential, commercial, and infrastructure sectors. Saudi Arabia and South Africa are key contributors to the regional market, with Saudi Arabia emerging as both the largest and fastest-growing market. The region's ambitious infrastructure development plans, including smart city projects and sustainable building initiatives, continue to drive the demand for cement board across various applications.

Competitive Landscape

Top Companies in Cement Board Market

The global cement board market is led by major players including James Hardie Industries PLC, Etex Group, Knauf Gips KG, Swisspearl Group AG, and Saint-Gobain, who are driving innovation through advanced manufacturing technologies and sustainable product development. These companies are focusing on expanding their production capacities and geographical footprint through strategic acquisitions and greenfield investments, particularly in high-growth regions like Asia-Pacific. Product innovation efforts are centered around developing lightweight, durable, and environmentally friendly cement board solutions with enhanced performance characteristics. Companies are strengthening their distribution networks and forming strategic partnerships to improve market penetration and customer reach. Operational excellence initiatives include implementing advanced manufacturing processes, optimizing supply chains, and investing in research and development to maintain competitive advantages.

Fragmented Market with Strong Regional Players

The cement board market exhibits a partially fragmented structure with a mix of global conglomerates and specialized manufacturers competing across different regions. The top players command significant market share through their established brands, extensive distribution networks, and technological capabilities, while numerous regional players maintain strong positions in their local markets through deep customer relationships and customized offerings. Market consolidation is primarily driven by larger companies acquiring regional players to expand their geographical presence and product portfolio, as evidenced by recent acquisitions like Saint-Gobain's purchase of Hume Cemboard Industries and Swisspearl Group's acquisition of Cembrit Group.

The competitive dynamics are characterized by vertical integration across the value chain, with many leading players manufacturing both raw materials and finished products to maintain cost advantages and ensure quality control. Companies are increasingly focusing on sustainability initiatives and green building certifications to differentiate their offerings and capture the growing environmental consciousness among customers. The market also sees significant investment in manufacturing facilities and technology upgrades to improve operational efficiency and meet evolving customer requirements.

Innovation and Sustainability Drive Future Success

Success in the fiber cement board market increasingly depends on companies' ability to develop innovative, sustainable products while maintaining cost competitiveness. Incumbent players are strengthening their market positions through investments in research and development, focusing on product improvements in areas such as durability, fire resistance, and environmental performance. Companies are also expanding their service offerings to include technical support, installation guidance, and customization options to create stronger value propositions for customers. The ability to navigate raw material price fluctuations and maintain efficient supply chains has become crucial for maintaining competitive advantages.

For new entrants and smaller players, success strategies include focusing on specific market niches, developing specialized products for particular applications, and building strong relationships with local construction companies and distributors. The increasing emphasis on green building standards and sustainable construction practices presents opportunities for companies to differentiate themselves through eco-friendly products and manufacturing processes. Regulatory requirements related to building safety and environmental protection are becoming more stringent, making compliance capabilities and certification achievements important competitive factors. The market's growth potential is further influenced by the increasing adoption of modern construction techniques and the rising demand for high-performance building materials, including fiber-reinforced cement and cement sheathing solutions.

Cement Board Industry Leaders

-

James Hardie Industries Plc.

-

Etex Group

-

Saint-Gobain

-

Johns Manville

-

NICHIHA Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2023: Saint-Gobain signed an agreement to acquire cement board producer Hume Cemboard Industries. Through this acquisition, the company strengthened its lightweight product offering in Malaysia.

- February 2023: Everest Industries Limited intends to invest USD 22.5 million to establish a manufacturing unit on a 20-acre site in the Badanaguppe Kellambali KIADB layout of Chamarajanagar, Karnataka, India. The new facility aims to produce 72,000 metric tons (MT) of fiber cement board and 19,000 MT of Rapicon wall panels. This state-of-the-art, highly automated plant is projected to generate approximately 127 job opportunities.

Global Cement Board Market Report Scope

Cement boards serve as versatile building materials, finding applications in construction, renovation, and decoration. Composed of a blend of cement, water, and aggregates (like sand or silica), these boards are molded into sheets. Unlike traditional wood-based materials, cement boards exhibit reduced shrinkage and expansion, making them particularly suited for regions experiencing significant temperature and humidity variations.

The cement board market is segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into fiber cement board, wood wool cement board, wood strand cement board, and cement bonded particle board. By application, the market is segmented into flooring, exterior and partition walls, roofing, columns and beams, facades, weatherboard, and cladding, acoustic and thermal insulation, and other applications (prefabricated houses, permanent shuttering, fire-resistant construction, etc.). By end-user industry, the market is segmented into residential, commercial, and industrial and institutional. The report also covers the sizes and forecasts for the cement board market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (square meters).

| Fiber Cement Board (FCB) |

| Wood Wool Cement Board (WWCB) |

| Wood Strand Cement Board (WSCB) |

| Cement Bonded Particle Board (CBPB) |

| Flooring |

| Exterior and Partition Walls |

| Roofing |

| Columns and Beams |

| Facades, Weatherboard, and Cladding |

| Acoustic and Thermal Insulation |

| Other Applications (Prefabricated Houses, Permanent Shuttering, Fire-resistant Construction, etc.) |

| Residential |

| Commercial |

| Industrial and Institutional |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Fiber Cement Board (FCB) | |

| Wood Wool Cement Board (WWCB) | ||

| Wood Strand Cement Board (WSCB) | ||

| Cement Bonded Particle Board (CBPB) | ||

| By Application | Flooring | |

| Exterior and Partition Walls | ||

| Roofing | ||

| Columns and Beams | ||

| Facades, Weatherboard, and Cladding | ||

| Acoustic and Thermal Insulation | ||

| Other Applications (Prefabricated Houses, Permanent Shuttering, Fire-resistant Construction, etc.) | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial and Institutional | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Cement Board Market?

The Cement Board Market size is expected to reach 670.39 million square meters in 2025 and grow at a CAGR of 5.13% to reach 860.92 million square meters by 2030.

What is the current Cement Board Market size?

In 2025, the Cement Board Market size is expected to reach 670.39 million square meters.

Who are the key players in Cement Board Market?

James Hardie Industries Plc., Etex Group, Saint-Gobain, Johns Manville and NICHIHA Co. Ltd are the major companies operating in the Cement Board Market.

Which is the fastest growing region in Cement Board Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Cement Board Market?

In 2025, the Asia-Pacific accounts for the largest market share in Cement Board Market.

What years does this Cement Board Market cover, and what was the market size in 2024?

In 2024, the Cement Board Market size was estimated at 636.00 million square meters. The report covers the Cement Board Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Cement Board Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: