Cell Culture Media Bags Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

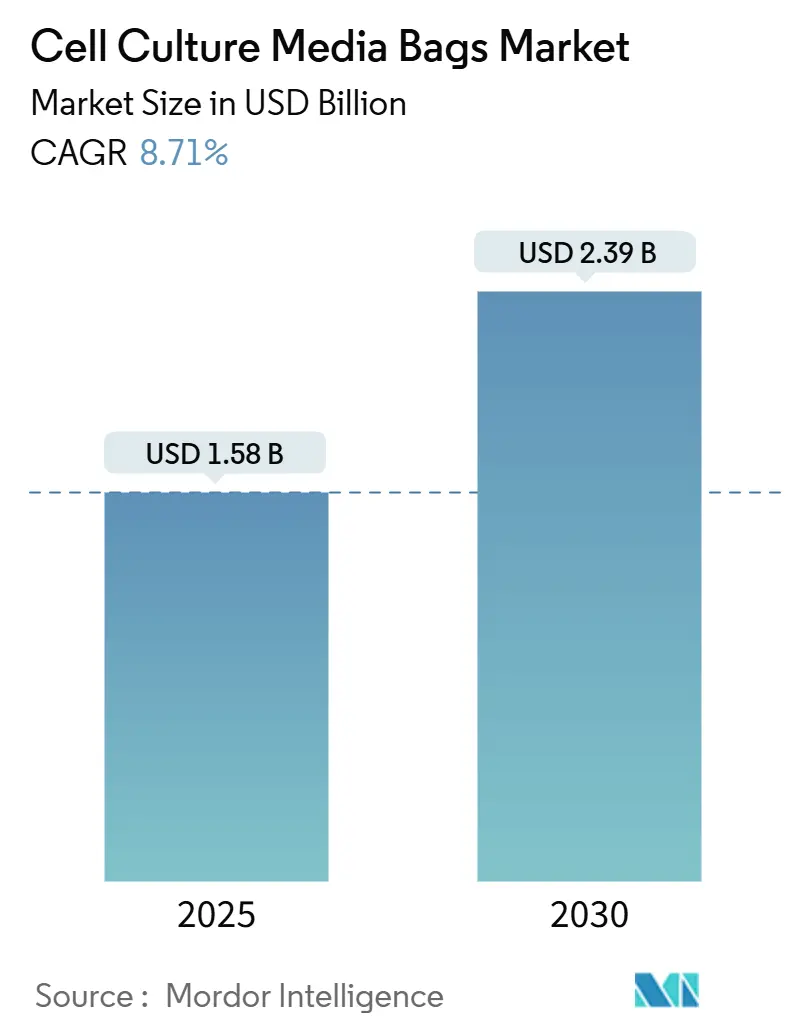

| Market Size (2025) | USD 1.58 Billion |

| Market Size (2030) | USD 2.39 Billion |

| Growth Rate (2025 - 2030) | 8.71% CAGR |

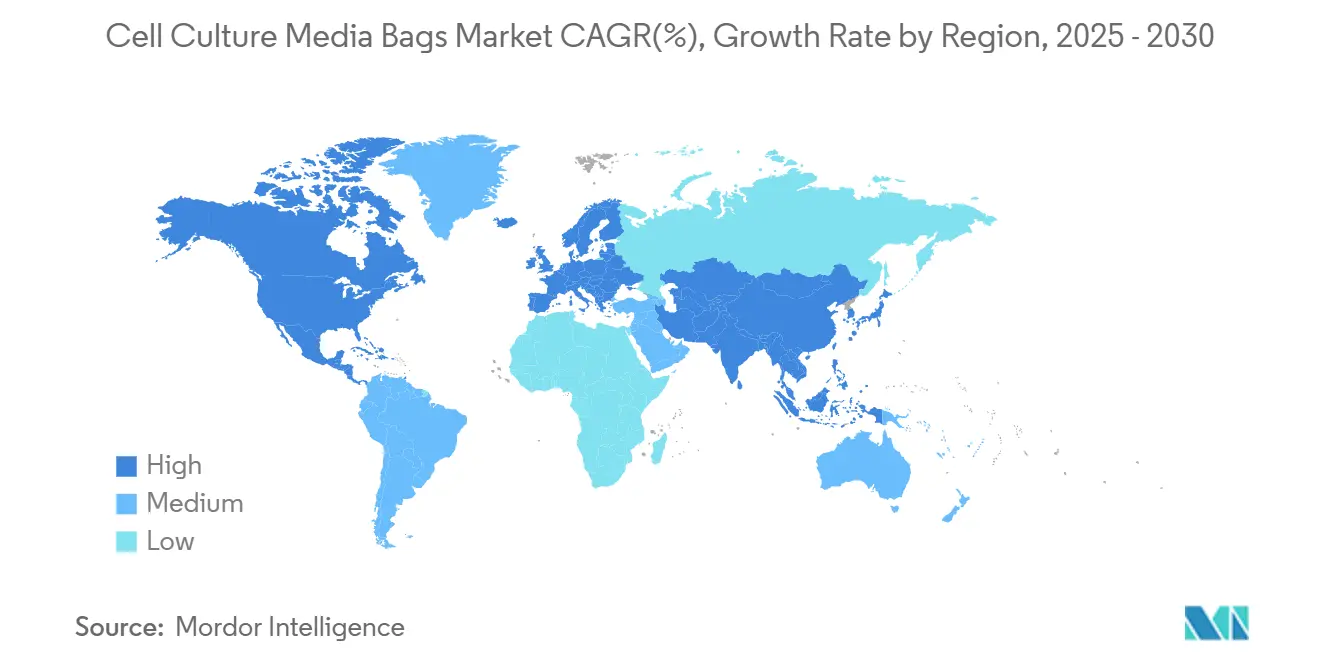

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cell Culture Media Bags Market Analysis by Mordor Intelligence

The cell culture media bags market stands at USD 1.58 billion in 2025 and is on track to reach USD 2.39 billion by 2030, advancing at an 8.71% CAGR. Robust demand is tied to accelerating single-use bioprocessing adoption, expanding monoclonal antibody (mAB) pipelines, and renewed capacity investment by vaccine CDMOs. Intensifying focus on contamination-free operations, shorter changeovers, and sustainability credentials positions single-use media bags as a preferred alternative to stainless-steel vessels. Fluoropolymer innovations that lower leachable risk, coupled with vertical integration moves by major suppliers, create added momentum. At the same time, supply-chain vulnerability in premium-grade polymers and stricter regulatory oversight on extractables present countervailing pressures.

Key Report Takeaways

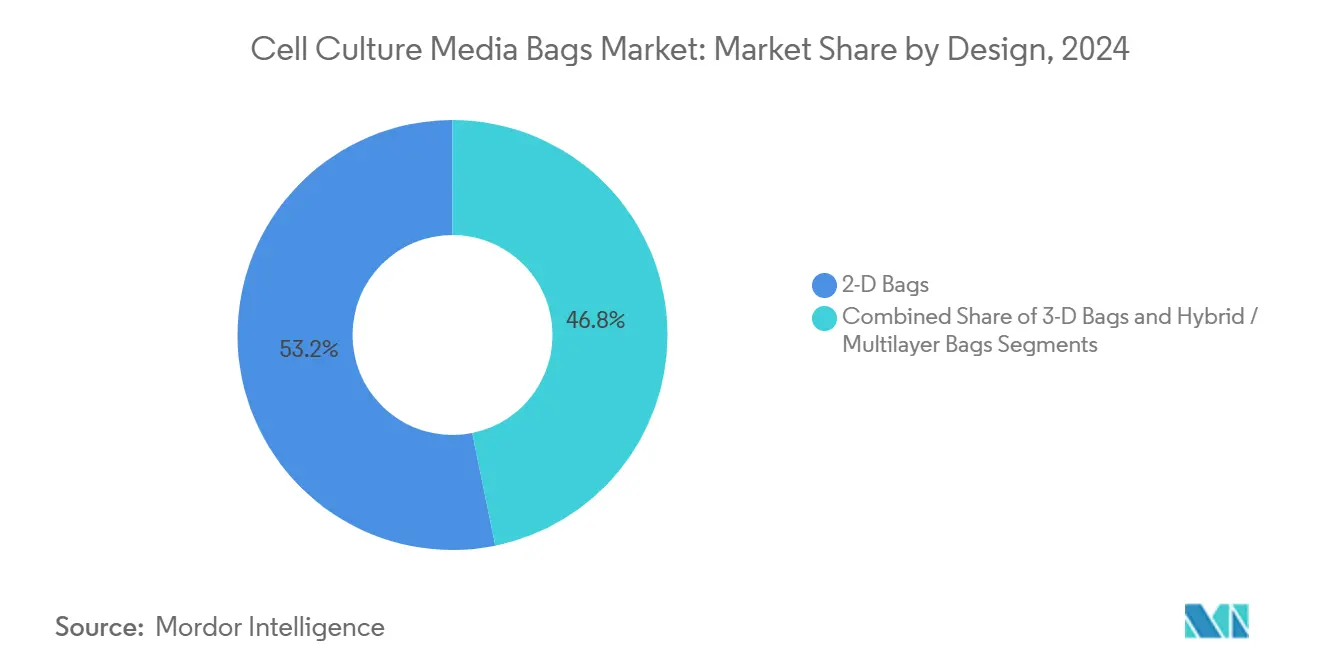

- By design, 2-D bags led with 53.18% of the cell culture media bags market share in 2024, while 3-D bags are forecast to expand at a 10.36% CAGR to 2030.

- By material, EVA captured 35.46% revenue share in 2024; fluorinated polymers such as PVDF are projected to grow at a 10.73% CAGR through 2030.

- By capacity volume, the 50–500 L segment accounted for 39.45% of the cell culture media bags market size in 2024; volumes above 500 L are set to rise at an 11.36% CAGR.

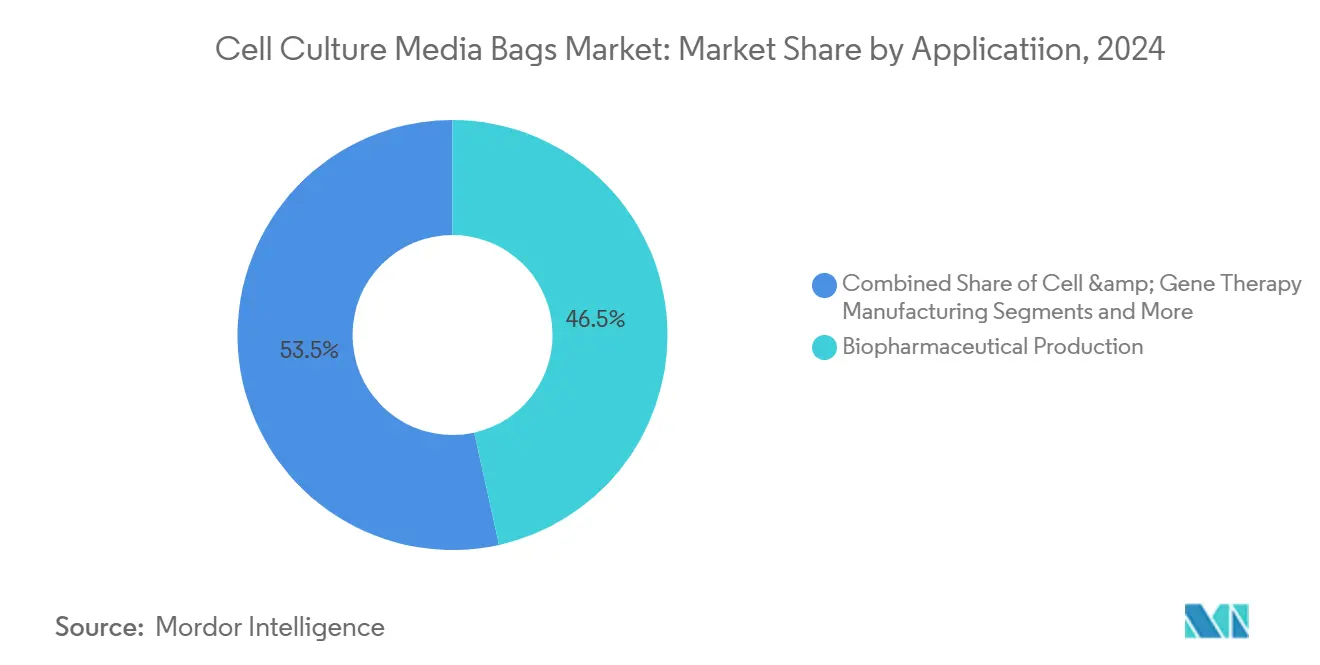

- By application, biopharmaceutical production held a 46.53% share of the cell culture media bags market size in 2024, whereas cell and gene therapy manufacturing is advancing at a 12.45% CAGR.

- By end user, pharmaceutical and biotechnology firms commanded 54.71% share in 2024; CDMOs/CROs exhibit the fastest growth at a 10.04% CAGR.

- By geography, North America controlled 39.18% of 2024 revenues, while Asia-Pacific is the quickest riser with an 11.83% CAGR toward 2030.

Global Cell Culture Media Bags Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Biopharma and mAB Production Pipelines | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Rapid Adoption of Single-Use Bioprocessing Systems | +2.1% | Global, led by North America, expanding in APAC | Short term (≤ 2 years) |

| Rising Stem-Cell & Regenerative-Medicine Clinical Trials | +1.2% | North America & EU core, emerging in APAC | Long term (≥ 4 years) |

| Capacity Build-Out of Vaccine CDMOs Post-COVID-19 | +0.9% | Global, with focus on APAC and emerging markets | Medium term (2-4 years) |

| Shift Toward High-Density Perfusion Micro-Bioreactors | +1.4% | North America & EU, technology transfer to APAC | Medium term (2-4 years) |

| Scope-3 Decarbonisation Mandates Favouring Lightweight Polymer Bags | +0.7% | EU-led, expanding to North America and multinational corporations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Biopharma and mAB Production Pipelines

Monoclonal antibody capacity additions such as Fujifilm Diosynth’s USD 1.6 billion Denmark expansion underscore the scale of demand for large-volume cell culture media bags market solutions. Higher-titer processes lengthen culture duration and increase protein concentration, requiring durable bag films that resist extractable buildup. Antibody-drug conjugate manufacturing further elevates contamination control needs, reinforcing the shift to pre-sterilised single-use assemblies. Geographic diversification of clinical trials into China and India is creating regional sourcing opportunities that still comply with FDA and EMA expectations.

Rapid Adoption of Single-Use Bioprocessing Systems

Changeover times that drop from weeks to 48 hours and lower cleaning requirements make single-use systems highly attractive for multiproduct CDMOs.[1]Boyd Biomedical, “Single-Use Systems Cut Changeover to 48 Hours,” BioProcess International, bioprocessintl.com Life-cycle assessments reveal smaller overall environmental footprints compared with stainless steel, dispelling myths about disposables. Cell and gene therapy producers regard single use as mandatory to mitigate cross-contamination between autologous batches, lifting demand for bespoke bag geometries compatible with perfusion and intensified processes.

Rising Stem-Cell & Regenerative-Medicine Clinical Trials

Clinical programs such as Mass General Brigham’s Parkinson’s trial rely on ultra-low-leachable fluoropolymer bags to preserve sensitive stem-cell phenotypes.[2]Mass General Brigham, “Clinical trial tests novel stem-cell treatment for Parkinson's disease,” Science Daily, sciencedaily.com As research settings scale toward commercial volumes, suppliers offering consistent bag performance from <5 L to 50 L gain an advantage. Stringent biocompatibility standards in regenerative medicine reward manufacturers capable of USP <87> and USP <665> compliance.

Capacity Build-Out of Vaccine CDMOs Post-COVID-19

Investments like Resilience’s USD 225 million fill-finish upgrade are expanding viral-vector and mRNA production footprints. These modalities demand bag films that tolerate low pH and solvent contact. Regional localisation in Asia-Pacific tightens lead times and reduces freight-related emissions, further propelling the cell culture media bags market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Contamination & Leachable Risk Versus Rigid Vessels | -1.3% | Global, with heightened scrutiny in North America & EU | Short term (≤ 2 years) |

| Bio-Hazardous Waste-Disposal Cost Escalation | -0.8% | Developed markets, spreading to emerging economies | Medium term (2-4 years) |

| Volatility in Premium-Grade EVA & PE Resin Prices | -0.6% | Global, with regional variations in supply access | Short term (≤ 2 years) |

| Geopolitical Polymer-Supply Concentration | -0.4% | Global, with particular impact on Western manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Contamination & Leachable Risk Versus Rigid Vessels

Discovery of cytotoxic compounds such as bDtBPP has placed fresh emphasis on rigorous extractables testing, prompting FDA guidance that redefines acceptable risk thresholds. Transition from USP <88> to USP <87>/<665> raises qualification costs, encouraging suppliers to develop fluoropolymer-lined bags despite higher price points.

Bio-Hazardous Waste-Disposal Cost Escalation

Incineration remains the dominant end-of-life route, yet escalating fees and tightening landfill regulations add operating expenses. Early-stage recycling and pyrolysis pilots offer promise but require capital outlays and regulatory clarity before mainstream adoption.

Segment Analysis

By Design: 3-D innovation drives premium adoption

2-D films retained 53.18% of the cell culture media bags market in 2024, reflecting legacy dominance in seed-train and buffer-prep tasks. However, 3-D formats are expanding at a 10.36% CAGR, powered by strong uptake in intensified perfusion and commercial-scale viral-vector suites. The flexible cube geometry improves mixing and mass-transfer rates while conserving floor space, attributes validated through computational fluid dynamics studies.[3]Ian Ransome, “Implementation of Single-Use Miniature Bioreactors,” BioProcess International, bioprocessintl.com Hybrid multilayer versions that combine EVA core layers with fluoropolymer contact surfaces target high-potency biologics and cell therapy batches, commanding price premiums that elevate revenue growth.

Demand for 3-D bags also rides on integration with automated pallet tanks that simplify logistics between upstream and downstream steps. As mAB facilities standardize on 2,000 L single-use bioreactors, suppliers are aligning 3-D bag designs with g-force limitations of modern rocking platforms. The cell culture media bags market size for 3-D configurations is projected to reach USD 0.92 billion by 2030, underpinning expanded capital investment by extrusion firms. Innovations such as laser-etched port reinforcements and pre-installed sensors reduce operator touches and help CDMOs accelerate turnaround times.

Note: Segment shares of all individual segments available upon report purchase

By Material: Fluorinated polymers lead innovation

EVA captured 35.46% revenue in 2024 because of its balance of clarity, weldability, and cost. Even so, fluorinated polymers such as PVDF are registering a 10.73% CAGR, outpacing the cell culture media bags industry average as stem-cell and gene therapy operators insist on ultra-clean contact layers. Regulatory flags over PFAS substance classes create future uncertainty, but interim demand remains high given limited non-fluorinated substitutes with comparable inertness.

Multi-layer structures that sandwich a thin PVDF surface between EVA support webs help manage cost while delivering leachable performance. Supplier R&D is also targeting bio-based tie layers that maintain gas-barrier traits yet improve end-of-life recyclability. The cell culture media bags market size for fluorinated films is set to surpass USD 0.55 billion by 2030 as mature facilities retrofit older suites to meet updated extractables limits. Conversely, PVC usage is tapering because of phthalate migration concerns, accelerating material mix shift toward high-performance alternatives.

By Capacity Volume: Large-scale drives growth

The 50–500 L range accounted for 39.45% of 2024 sales given its central role in clinical supply and pilot runs. Nevertheless, volumes above 500 L are rising at an 11.36% CAGR due to surge investments such as Lonza’s 330,000 L Vacaville site. High-volume demand benefits suppliers offering reinforced handle loops and wider-bore ports capable of rapid media transfer.

Process intensification lets manufacturers achieve >100 × 10^6 cells/mL viable density, which extends bag service life and raises scrutiny of film fatigue performance. The cell culture media bags market share held by >500 L formats is expected to climb to 18% by 2030 as scale-out strategies complement traditional scale-up. Suppliers are ensuring consistent mixing performance across bag sizes by preserving aspect ratios and sparger configurations, easing validation burdens for GMP operators.

By Application: Cell & gene therapy accelerates

Biopharmaceutical protein production remained the backbone with 46.53% share in 2024, reflecting entrenched antibody and recombinant protein programmes. The cell & gene therapy segment, however, is growing at 12.45% CAGR on the back of multiple FDA gene-therapy approvals in 2024. Autologous workflows demand small, closed, single-use systems that protect patient-specific batches from cross-talk.

Advanced therapy vectors often involve low pH or solvent steps that challenge conventional bag films, stimulating upgrades to fluoropolymer contact layers. The cell culture media bags market size tied to cell & gene therapy could top USD 0.48 billion by 2030, propelled by more than 1,200 ongoing trials worldwide. Vaccine manufacturing also contributes incremental volume, especially for mRNA platforms that require nuclease-free process contact.

Note: Segment shares of all individual segments available upon report purchase

By End User: CDMOs drive market expansion

In-house operations at pharma and biotech companies commanded 54.71% of 2024 demand; yet CDMOs and CROs are surging at 10.04% CAGR as innovators outsource to gain capacity agility. Outsourcers favour turnkey packages that bundle bags, connectors, and pre-validated sterilisation certificates to streamline regulatory filings.

Strategic alliances between bag suppliers and service providers integrate supply security with process-development expertise. The cell culture media bags market size linked to CDMOs is projected to exceed USD 0.84 billion by 2030. Academic labs and diagnostic firms offer steady but smaller growth, benefitting from miniature bag variants that reduce media consumption in high-throughput formats.

Geography Analysis

North America secured 39.18% of global revenue in 2024 thanks to deep clinical pipelines, mature GMP infrastructure, and FDA regulatory leadership. Investments such as Pfizer’s USD 200 million Massachusetts site and Fujifilm’s USD 1.2 billion North Carolina plant reinforce regional scale advantages. Canada and Mexico augment regional supply through niche production and cost-efficient fill-finish capacity. High uptake of cell and gene therapy platforms further boosts sophisticated single-use bag demand, particularly those lined with fluoropolymer contact layers for ultra-low extractables.

Asia-Pacific is the fastest-growing region, advancing at an 11.83% CAGR to 2030 on the back of Chinese and Indian policy support for domestic biologics. China’s regulatory harmonisation with ICH standards favours Western-compliant local media bag production. India’s cost-competitive manufacturing model attracts contract work from global sponsors, while South Korea leverages government incentives to build advanced therapy clusters. Japan transitions legacy stainless-steel suites toward flexible single-use platforms, although validation practices remain conservative. The cell culture media bags market size attributable to Asia-Pacific is projected to overtake Europe by 2028.

Europe maintains solid growth fuelled by German, UK, and French biologics hubs plus EU sustainability mandates that reward low-carbon materials. Circular-economy policies are catalysing R&D into recyclable films and closed-loop take-back schemes. Brexit reshapes supply logistics, but EMA adoption of FDA-aligned extractables guidance simplifies technology transfer. Italy and Spain add capacity for niche vaccines, whereas Eastern Europe remains a smaller yet rising player. Collectively, Europe emphasises carbon footprint disclosure in procurement, spurring adoption of life-cycle-assessed bag portfolios.

Competitive Landscape

The cell culture media bags market demonstrates moderate consolidation, with leading five suppliers accounting for an estimated 55% of 2024 revenue. Danaher’s USD 7.5 billion merger of Cytiva and Pall forms an expansive single-use platform covering media preparation through chromatography. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification unit extends its reach into downstream filtration, reinforcing a vertically integrated offering. Sartorius and Merck KGaA remain strong through differentiated film chemistries and regional manufacturing nodes that shorten lead times.

Technology rivalry centres on reducing leachable profiles without compromising weldability. Patent filings highlight multilayer fluoropolymer-EVA constructions and port designs that maintain integrity during gamma irradiation. Saint-Gobain leverages aerospace-grade polymer know-how to craft high-clarity, high-strength films for perfusion bioreactors. Smaller players such as Single Use Support carve niches in cold-chain bulk drug storage, aided by Novo Holdings’ 2024 majority stake purchase.

Geographic expansion remains a strategic priority. Major suppliers are commissioning extrusion lines in Singapore, Wuxi, and Wuppertal to mitigate freight and tariff risks. Sustainability offerings—including take-back programs and recycled resin blends—are becoming table stakes in EU tenders. Regulatory tightening around PFAS may reorder material hierarchies, giving an edge to companies with alternative high-performance polymers already in pipeline.

Cell Culture Media Bags Industry Leaders

-

ThermoFisher Scientific

-

Sartorius AG

-

Corning Incorporated

-

Danaher

-

Saint- Gobain Performance Plastics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cytiva announced a USD 1.6 billion program to boost resin, filtration, single-use bag, and media output across Europe, Asia-Pacific, and North America.

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s purification and filtration business for USD 4.1 billion, expanding its bioprocessing footprint.

- May 2024: Novo Holdings secured a 60% stake in Single Use Support to enhance global fluid-management solutions for advanced therapies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cell culture media bags market as all sterile, single-use or limited-reuse polymer bags (2-D and 3-D formats) that hold prepared growth media during upstream and downstream bioprocess steps for mammalian, insect, or microbial cells.

Scope exclusion: support accessories such as tubing manifolds, bag holders, and rigid seed-train vessels are excluded.

Segmentation Overview

-

By Design

- 2-D Bags

- 3-D Bags

- Hybrid / Multilayer Bags

-

By Material

- EVA

- LDPE

- PVC

- Polypropylene

- Fluorinated Polymers (e.g., PVDF)

- Others

-

By Capacity Volume

- <5 L

- 5 – 50 L

- 50 – 500 L

- >500 L

-

By Application

- Biopharmaceutical Production

- Cell & Gene Therapy Manufacturing

- Vaccine Manufacturing

- Stem-Cell & Academic Research

- Others

-

By End User

- Pharmaceutical & Biotechnology Companies

- CDMOs / CROs

- Academic & Research Institutes

- Diagnostic Laboratories

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed procurement heads at biopharma manufacturers, process-development scientists at CDMOs, and quality managers in academic GMP suites across North America, Europe, and Asia-Pacific. These conversations validated average selling prices, shipment lead times, and adoption barriers, bridging gaps left by secondary data.

Desk Research

We began by mapping publicly available data from authoritative sources, such as the US FDA's Device Registration database, European Medicines Agency filings, United States Patent & Trademark Office records, and trade statistics from UN Comtrade that list HS codes for plastic bioprocess containers. Annual reports and 10-Ks from leading bioproduction suppliers, plus investor presentations that disclose single-use penetration rates, further grounded base-year volume and pricing assumptions.

To refine regional splits, analysts reviewed import duties published by the European Plastics Converters Association, capacity announcements logged in BioProcess International, and facility counts maintained by BioPhorum. Select insights from paid platforms, D&B Hoovers for company revenues and Dow Jones Factiva for transaction news, rounded out the desk work. This list is illustrative; many other open and subscription sources informed cross-checks and clarifications.

Market-Sizing & Forecasting

A top-down construct starts with global biologics production volumes, which are then paired with media-to-product conversion factors to derive total media demand; unit penetration of single-use bags translates this pool into bag volumes. Bottom-up checks, supplier revenue roll-ups and sampled ASP × units from purchasing managers, calibrate the totals. Key drivers inside the model include single-use adoption rates, median bag capacity used per batch, biopharmaceutical CAPEX outlays, active cell and gene therapy trial count, regional GMP facility expansion, and polymer price trends. Multivariate regression projects each driver through the forecast period, producing the final CAGR that, according to Mordor Intelligence, underpins the market value. Gap areas in granular supplier data are bridged with conservative interpolation based on nearest known benchmarks.

Data Validation & Update Cycle

Outputs undergo three-level analyst review, anomaly checks against external production indices, and back-testing versus prior editions. We refresh every twelve months, with interim updates triggered by material events such as large-scale bioreactor capacity additions.

Why Our Cell Culture Media Bags Baseline Earns Trust

Published figures often diverge because firms adopt differing product scopes, apply aggressive versus conservative ASP progressions, or refresh numbers on uneven schedules.

Key gap drivers include whether reusable bags are counted, how aggressively future clinical-trial growth is baked in, and the frequency of currency-conversion updates; areas where Mordor's disciplined refresh cadence and clearly documented scope deliver steadier outputs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.58 billion | Mordor Intelligence | |

| USD 2.35 billion | Global Consultancy A | Includes wider "media storage containers" and applies forward ASP escalation without bottom-up calibration |

| USD 1.34 billion | Industry Data Publisher B | Excludes 3-D bags and uses 2024 trade data rolled forward without primary validation |

| USD 1.69 billion | Technology Market Advisor C | Forecasts built on linear biologics pipeline growth and triennial refresh cycle |

These contrasts show that Mordor's scope discipline, dual-track modeling, and annual updates yield a balanced, transparent baseline that decision-makers can reliably trace to clear variables and repeatable steps.

Key Questions Answered in the Report

1. What is the current size of the cell culture media bags market?

The market is valued at USD 1.58 billion in 2025.

2. How fast is the cell culture media bags market expected to grow?

It is forecast to expand at an 8.71% CAGR, reaching USD 2.39 billion by 2030.

3. Which region is growing the fastest?

Asia-Pacific is the fastest-growing region with an 11.83% CAGR through 2030.

4. Why are 3-D bag designs gaining traction?

They offer improved mixing, smaller footprints, and better compatibility with high-density perfusion cultures.

5. What material trends dominate the market?

EVA remains most common, while fluorinated polymers such as PVDF are gaining due to lower leachables.

6. How are sustainability goals influencing procurement?

Scope 3 emission targets push buyers toward lightweight single-use bags and encourage development of recycling programs.

Page last updated on: