Celiac Disease Treatment Market Size

| Study Period | 2019 - 2029 |

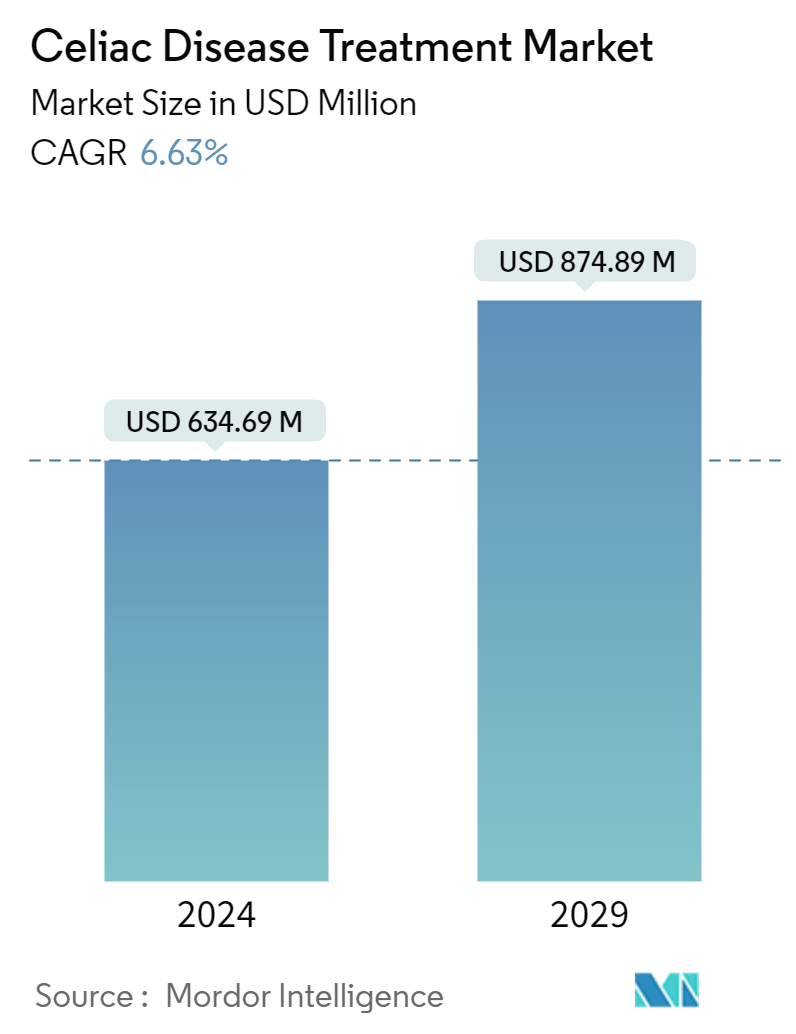

| Market Size (2024) | USD 634.69 Million |

| Market Size (2029) | USD 874.89 Million |

| CAGR (2024 - 2029) | 6.63 % |

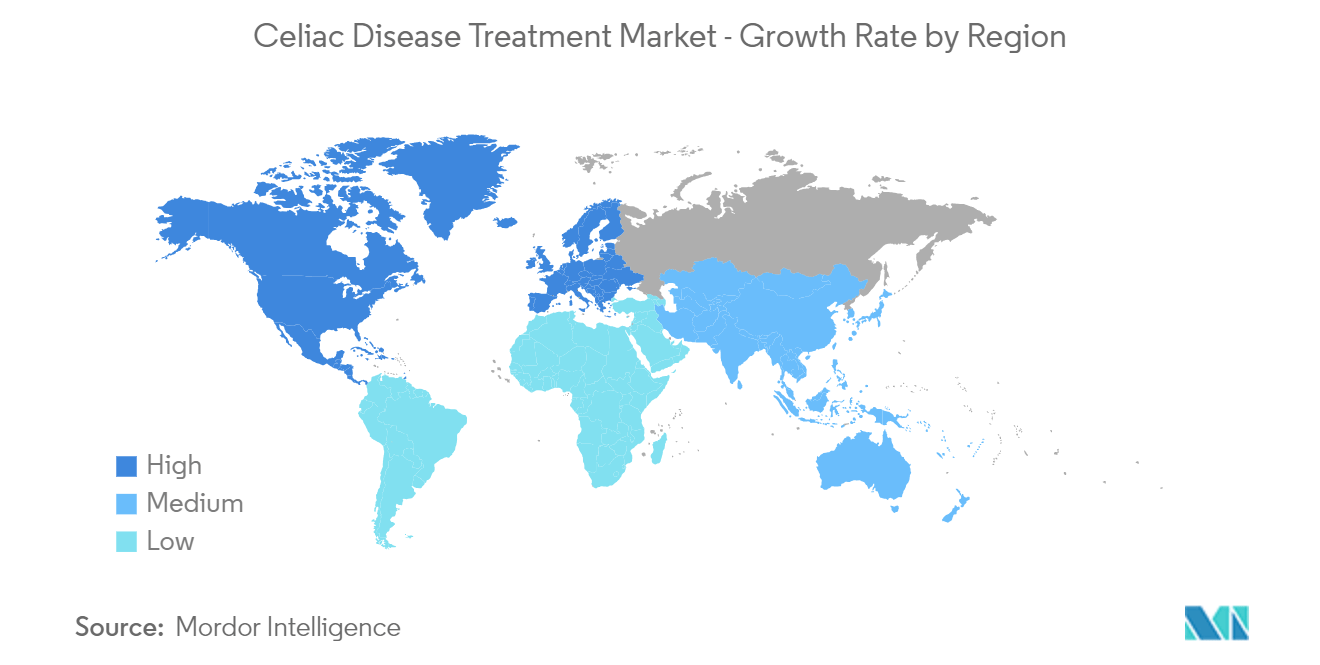

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Celiac Disease Treatment Market Analysis

The Celiac Disease Treatment Market size is estimated at USD 634.69 million in 2024, and is expected to reach USD 874.89 million by 2029, growing at a CAGR of 6.63% during the forecast period (2024-2029).

Celiac disease triggers an immune attack on the small intestine due to gluten commonly found in wheat, barley, and rye. This damages the gut lining and hinders nutrient absorption. The symptoms include bloating, diarrhea, and malnutrition. Hence, a strict gluten-free diet is the main treatment. Currently, there are no medications available to treat celiac disease, only symptomatic treatment. The key growth drivers include the rising prevalence of celiac disease, the development of novel therapies, and growing awareness of celiac disease.

The prevalence of celiac disease is increasing globally, which increases the need for treatment products. For instance, according to a study published in Gastroenterology in February 2024, celiac disease is a widespread lifelong disorder affecting 0.7% to 2.9% of the general population globally. Similarly, according to a study published in Gastroenterology in October 2023, the condition's incidence in Colorado, Washington, and Sweden was as high as 2.4%, 0.9%, and 3%, respectively, in 2022. In these regions, the number of people suffering from celiac disease is increasing. Thus, the increase in the incidence rates of celiac disease is expected to drive the market over the next five years.

The focus on an immune tolerance-based therapy signifies a potential shift in treatment goals. For instance, in May 2023, Topas Therapeutics commenced a Phase IIa clinical trial for TPM502 for the treatment of celiac disease. This trial investigates TPM502's ability to induce immune tolerance, potentially allowing patients to consume gluten without adverse effects. The introduction of TPM502 signifies a significant advancement in the immune tolerance-based clinical pipeline and reflects the commitment to offering innovative disease-modifying therapeutics to patients with limited pharmacological options. Thus, the constant research to develop the treatment for celiac disease is growing and is expected to drive the demand for celiac disease treatment over the next five years.

The market will likely continue to grow based on the increasing demand for improved treatment options and the growing prevalence of celiac disease. However, limited treatment options and challenges in accurately diagnosing celiac disease restrain market growth.

Celiac Disease Treatment Market Trends

The Segment for Refractory Celiac Disease is Expected to Witness Significant Growth Over the Forecast Period

The growing prevalence of refractory celiac disease (RCeD) is driving the segment. For instance, a study published in the Journal of Gastroenterology in April 2024 showed that refractory celiac disease (RCeD) affected 1-2% of patients in 2022 globally. These individuals experienced persistent symptoms and gut damage despite adhering to a gluten-free diet (GFD). This ineffectiveness underscores the need for new treatment options. It presents a significant unmet medical need for celiac disease (CeD) drug development, fueling the growth of the celiac disease treatment market.

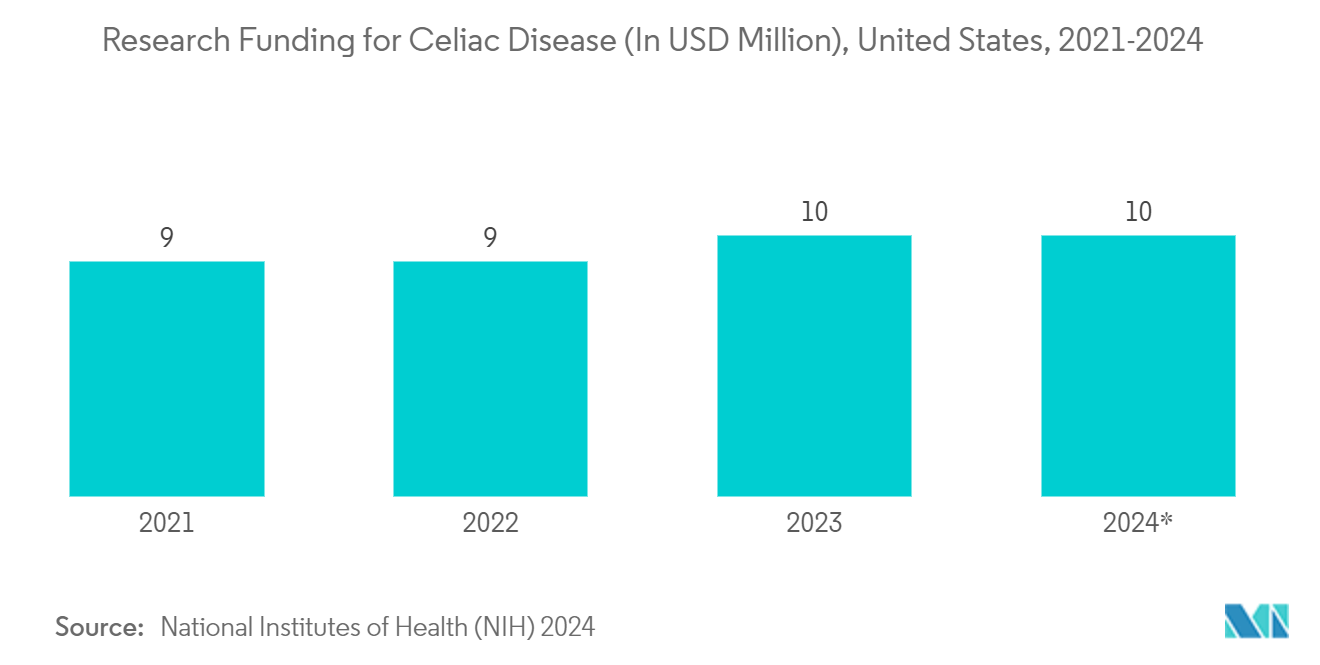

The funding from the National Institutes of Health (NIH) in May 2024 suggested a sustained interest in celiac disease research. This focus translates to more efforts to understand the disease, develop new treatments, and improve patient care. The consistent funding for celiac disease research was around USD 9 million annually from 2021 to 2022, with projections for USD 10 million in 2024 and 2025. This is expected to lead to an increase in investments in research and development, propelling the growth of the segment.

The growing adoption of various treatment options for refractory celiac disease is expected to drive segmental growth over the forecast period. For instance, according to data published in Clinical Gastroenterology and Hepatology in July 2024, for patients with refractory celiac disease type 2, particularly those unresponsive to treatments such as budesonide, Tofacitinib is a viable treatment option. This shows the new recommendation for refractory celiac disease treatment, which is expected to boost the usage of the drugs, thereby propelling the segment’s growth.

Hence, due to the rising incidence of refractory celiac disease, growing investments, and the growing demand for novel therapies, the overall market is expected to witness growth.

North America is Expected to Dominate the Celiac Disease Treatment Market

North America's leading position in the celiac disease treatment market is mostly due to the higher prevalence of celiac disease, increasing research and development, growing awareness of the condition, and rising advancements in diagnostic approaches.

The rising prevalence of celiac disease in the United States is expected to fuel the growth of the celiac disease treatment market in the region. For instance, according to a study published in the American Journal of Gastroenterology in February 2024, celiac disease (CD), a condition caused by the body's inability to tolerate gluten, impacted around 0.8% of the entire population in the United States in 2023. Therefore, the prevalence is expected to increase, impacting the market's growth over the forecast period.

In Canada, the awareness of celiac disease is rising, along with the need for improved treatments, and it is expected to drive the growth of the market. For instance, according to Health Canada, in May 2024, food allergies affect over 3 million people, while celiac disease impacts nearly 400,000 in Canada. Canada recognizes both food allergy awareness month and celiac awareness month, highlighting the challenges, anxieties, and uncertainties faced by those living with these conditions. Thus, awareness of celiac disease is rising, leading to earlier diagnosis and treatment; this is expected to drive the North American celiac disease treatment market over the next five years.

Also, the established key players in this region are focusing on the development of drug therapies to reduce the burden of celiac disease and improve health outcomes. Owing to these factors, North America is the leader in the celiac disease treatment market.

Celiac Disease Treatment Industry Overview

The celiac disease treatment market is semi-consolidated in nature due to the presence of companies operating globally and regionally. Key leading market players are investing heavily in clinical research and development to expand their product lines. The key strategies market participants adopt to expand their footprint are agreements, mergers, higher investments, and collaborations with other organizations. The major players in the market include General Mills Inc., Innovate Biopharmaceuticals, Takeda Pharmaceuticals, IMTherapeutics, and ImmunogenX.

Celiac Disease Treatment Market Leaders

-

General Mills, Inc.

-

Innovate Biopharmaceuticals

-

Takeda Pharmaceuticals

-

IMTherapeutics

-

ImmunogenX

*Disclaimer: Major Players sorted in no particular order

Celiac Disease Treatment Market News

- October 2023: Immunic Inc. presented positive data from a Phase 1b clinical trial of IMU-856, a potential new treatment for celiac disease. This orally administered medication represents a significant development in the field. IMU-856 targets SIRT6, a protein not previously explored in celiac disease treatment. This approach offered promise beyond existing therapies and was presented at the United European Gastroenterology Week (UEGW) 2023.

- June 2023: Takeda collaborated with Celiac Disease Foundation, actively recruiting participants for trials testing TAK-062 and TAK-101 promising therapies. This development signified a major step forward in celiac disease treatment research, offering hope for millions managing the condition.

Celiac Disease Treatment Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Increasing Awareness and Diagnosis of Celiac Disease

4.2.2 Rising Prevalence of Celiac Disease Globally

4.2.3 Increasing Research and Development for Celiac Disease Therapeutics

4.3 Market Restraints

4.3.1 Limited Availability of Treatment

4.4 Porter's Five Force Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

5.1 By Product Type

5.1.1 Vitamin and Minerals Supplements

5.1.2 Steroids and Immunosuppressive Drugs

5.2 By Type

5.2.1 Non-Responsive Celiac Disease

5.2.2 Refractory Celiac Disease

5.3 By Treatment Type

5.3.1 First Line

5.3.2 Second Line

5.4 By Distribution Channel

5.4.1 Hospital Pharmacy

5.4.2 Retail Pharmacy

5.4.3 Online Pharmacy

5.4.4 Others

5.5 Geography

5.5.1 North America

5.5.1.1 United States

5.5.1.2 Canada

5.5.1.3 Mexico

5.5.2 Europe

5.5.2.1 Germany

5.5.2.2 United Kingdom

5.5.2.3 France

5.5.2.4 Italy

5.5.2.5 Spain

5.5.2.6 Rest of Europe

5.5.3 Asia-Pacific

5.5.3.1 China

5.5.3.2 Japan

5.5.3.3 India

5.5.3.4 Australia

5.5.3.5 South Korea

5.5.3.6 Rest of Asia-Pacific

5.5.4 Middle East and Africa

5.5.4.1 GCC

5.5.4.2 South Africa

5.5.4.3 Rest of Middle East and Africa

5.5.5 South America

5.5.5.1 Brazil

5.5.5.2 Argentina

5.5.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 General Mills Inc.

6.1.2 Innovate Biopharmaceuticals

6.1.3 Precigen

6.1.4 Takeda Pharmaceuticals

6.1.5 Provention Bio

6.1.6 IMTherapeutics

6.1.7 ImmunogenX

6.1.8 Vetanda Group Limited

6.1.9 Allero Therapeutics

6.1.10 Enteralia Bioscience

6.1.11 AMYRA Biotech AG

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Celiac Disease Treatment Industry Segmentation

People with celiac disease have a variety of nutritional concerns. Gluten, a protein naturally found in certain grains like wheat, barley, rye, and some oats, triggers an autoimmune response that causes inflammation and damages the small intestine's lining. This damage can lead to abnormal digestion and reduced nutrient absorption. There are two types of celiac disease: Type I (RCeDI), which might be driven by an extreme sensitivity to gluten traces, and Type II (RCeDII), which is a severe form associated with a higher risk of cancer. The main treatment is to opt for a gluten-free diet and treatment plans.

The celiac disease treatment market is segmented by product type, type, treatment type, distribution channel, and geography. By product type, the market is segmented into vitamin and mineral supplements, steroids, and immunosuppressive drugs. By type, the market is segmented into non-responsive celiac disease and refractory celiac disease. By treatment, the market is segmented into first line and second line. By distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others, including home care settings and specialty clinics. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also offers the market sizes and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| By Product Type | |

| Vitamin and Minerals Supplements | |

| Steroids and Immunosuppressive Drugs |

| By Type | |

| Non-Responsive Celiac Disease | |

| Refractory Celiac Disease |

| By Treatment Type | |

| First Line | |

| Second Line |

| By Distribution Channel | |

| Hospital Pharmacy | |

| Retail Pharmacy | |

| Online Pharmacy | |

| Others |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Celiac Disease Treatment Market Research FAQs

How big is the Celiac Disease Treatment Market?

The Celiac Disease Treatment Market size is expected to reach USD 634.69 million in 2024 and grow at a CAGR of 6.63% to reach USD 874.89 million by 2029.

What is the current Celiac Disease Treatment Market size?

In 2024, the Celiac Disease Treatment Market size is expected to reach USD 634.69 million.

Who are the key players in Celiac Disease Treatment Market?

General Mills, Inc., Innovate Biopharmaceuticals, Takeda Pharmaceuticals, IMTherapeutics and ImmunogenX are the major companies operating in the Celiac Disease Treatment Market.

Which is the fastest growing region in Celiac Disease Treatment Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Celiac Disease Treatment Market?

In 2024, the North America accounts for the largest market share in Celiac Disease Treatment Market.

What years does this Celiac Disease Treatment Market cover, and what was the market size in 2023?

In 2023, the Celiac Disease Treatment Market size was estimated at USD 592.61 million. The report covers the Celiac Disease Treatment Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Celiac Disease Treatment Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Celiac Disease Treatment Industry Report

Statistics for the 2024 Celiac Disease Treatment market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Celiac Disease Treatment analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.