Market Trends of Cattle Feed Industry

Cereals Segment Leads the Market

Cereal grains have long been essential in livestock nutrition, particularly for cattle feed. These grains are used both as whole plant forage and as feed grains. Their high energy content makes them crucial, especially in systems aimed at maximizing growth rates or milk production. Corn is a primary choice due to its high starch content, providing readily available energy. Additionally, barley and oats offer a more balanced energy profile and are often combined with other feeds to optimize nutritional intake.

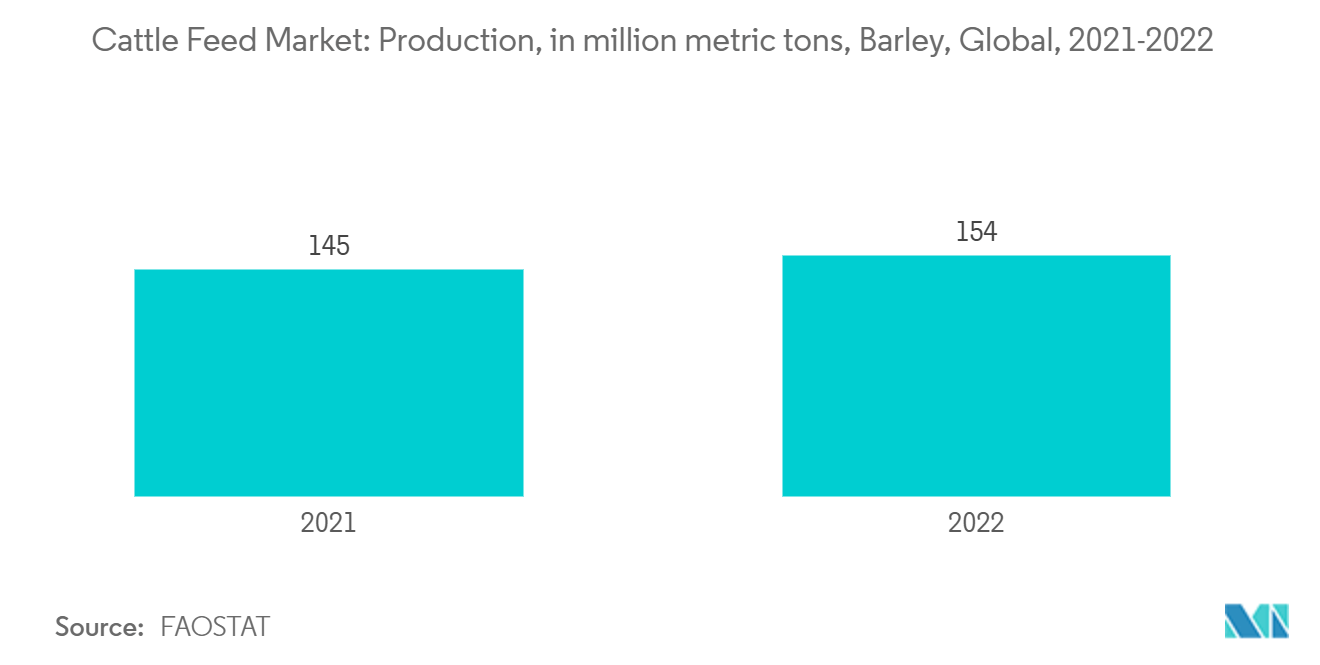

Along with this, corn, barley, wheat, oats, and rye, are majorly used in cattle feeds as they provide essential nutrients that support growth, reproduction, and overall health in cattle, aiding segment growth. The growing area under these crops fuels the market growth. As per FAOSTAT, the production of barley in the world grew from 145 million metric tons to 154 million metric tons from 2021 to 2022. Similarly, Cereal grains serve as concentrated energy sources in the cattle feeding sector, especially in finishing rations, where they can constitute up to 90% of the nation's dry matter. This significant dependence on cereals for energy stems largely from their cost-effectiveness as they usually offer a lower cost per unit of dietary energy compared to other readily available feed sources.

Furthermore, the rise of cereal-based feed mills serving cattle is driving the market's growth. For example, in 2023, a new feed mill commenced operations in Kidapawan City, located on Mindanao's southern main island in the Philippines. This facility processes corn and rice, creating diets for various livestock, including cattle. Additionally, the European Union (EU) contributed USD 119 thousand towards the feed mill's construction. Therefore, the high nutritional value, competitive pricing and the expansions of the cereal grains feeding mills make cereals attractive feed sources for cattle.

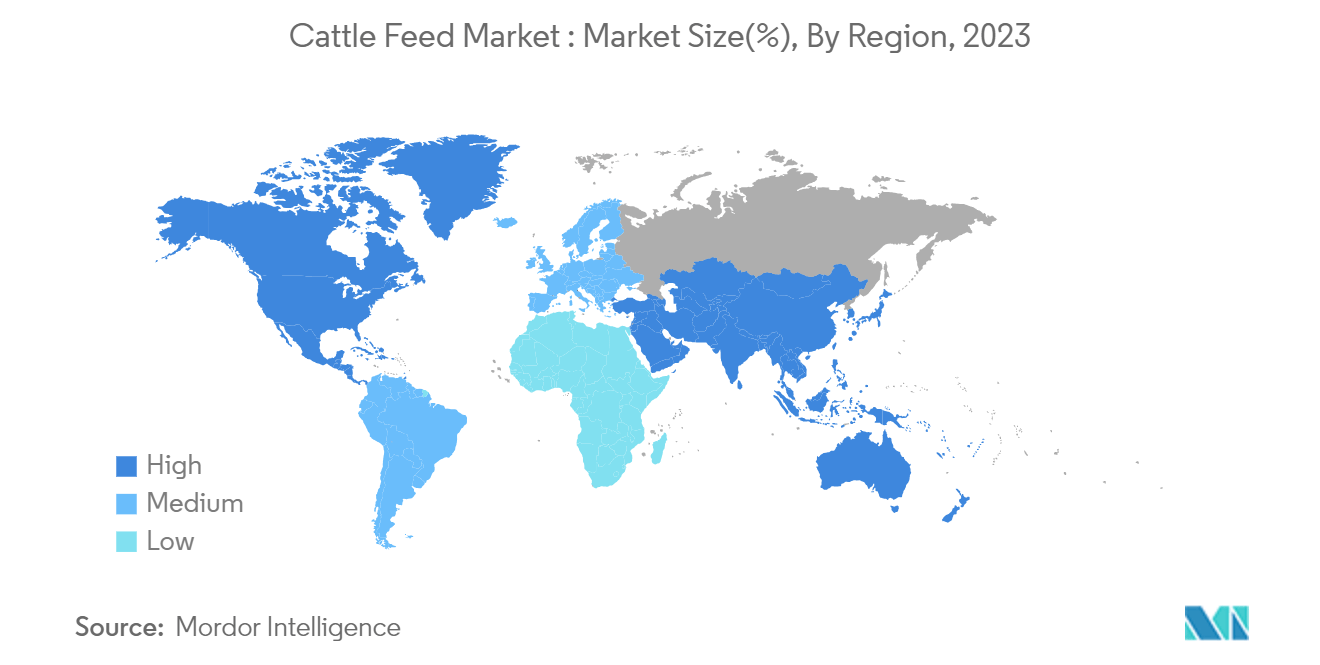

North America Dominates the Market

The cattle feed market in North America, including the United States and Canada, is substantial due to high cattle inventories and advanced farming practices. The market has shown steady growth driven by increasing demand for beef and dairy products in the countries. The per capita consumption of beef in Canada is observed to be growing from 26.2 kgs to 26.8 kgs from 2021 to 2022, according to Statistics Canada. Despite the growing consumption, the production of beef is reducing in the country. As per Statistics Canada, beef production dropped from 1.38 million metric tons to 1.29 million metric tons in 2022. This shortfall amplifies the need for imports and underscores the urgency to boost local production, subsequently bolstering the cattle feed market.

The United States cattle feed market is vast, driven by extensive beef and dairy cattle farming, technological advancements in feed production, and a heightened emphasis on sustainable, eco-friendly feeding practices. For example, data from the United States Department of Agriculture indicates that the United States milk cow population increased from 9.33 million in 2019 to 9.38 million in 2023. This growing dairy cattle population underscores the demand for high-quality feed, essential for boosting milk production and, consequently, propelling market growth.

Moreover, companies in the animal nutrition sector are strategizing to broaden their reach and ensure high-quality feed for animals, including cattle. For example, in 2022, the Buhler Group formed a joint venture with IMDHER S.A. de C.V., a prominent player in Mexico's animal nutrition market. This move focuses on enhancing process efficiency, quality, and sustainability in the feed industry, particularly for cattle. Consequently, the surging demand for cattle-based products, combined with escalating farming activities and proactive measures by key industry players, is propelling the market's growth during the forecast period.