Case Packaging Machinery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

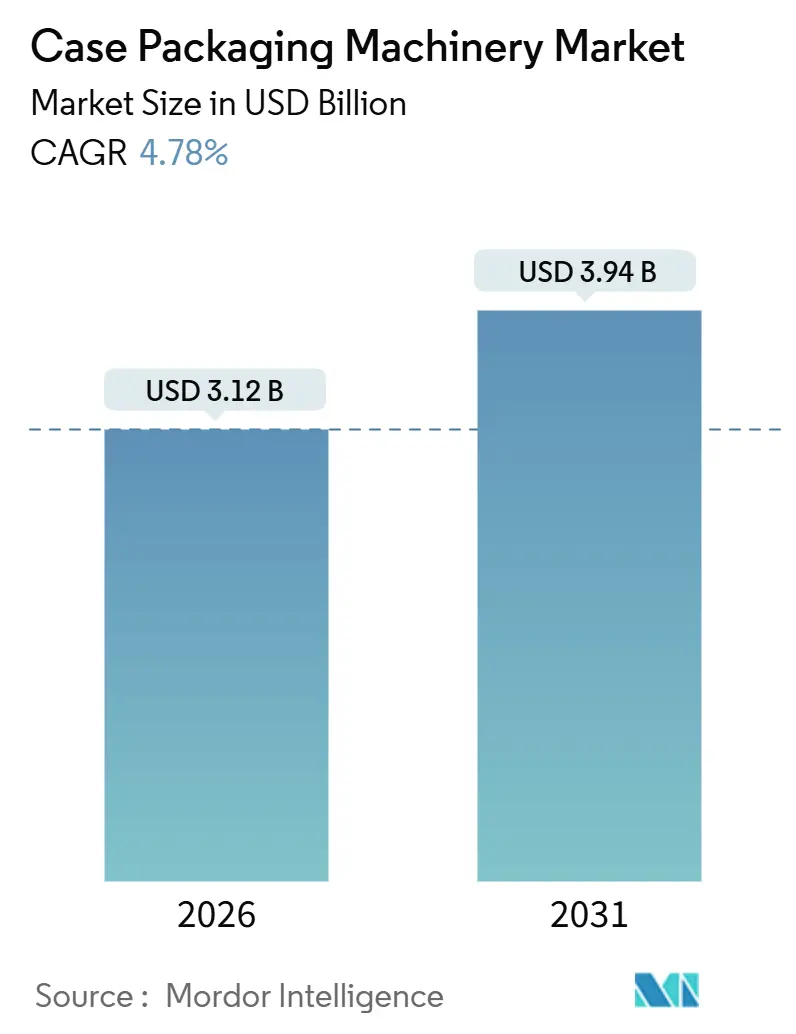

| Market Size (2026) | USD 3.12 Billion |

| Market Size (2031) | USD 3.94 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

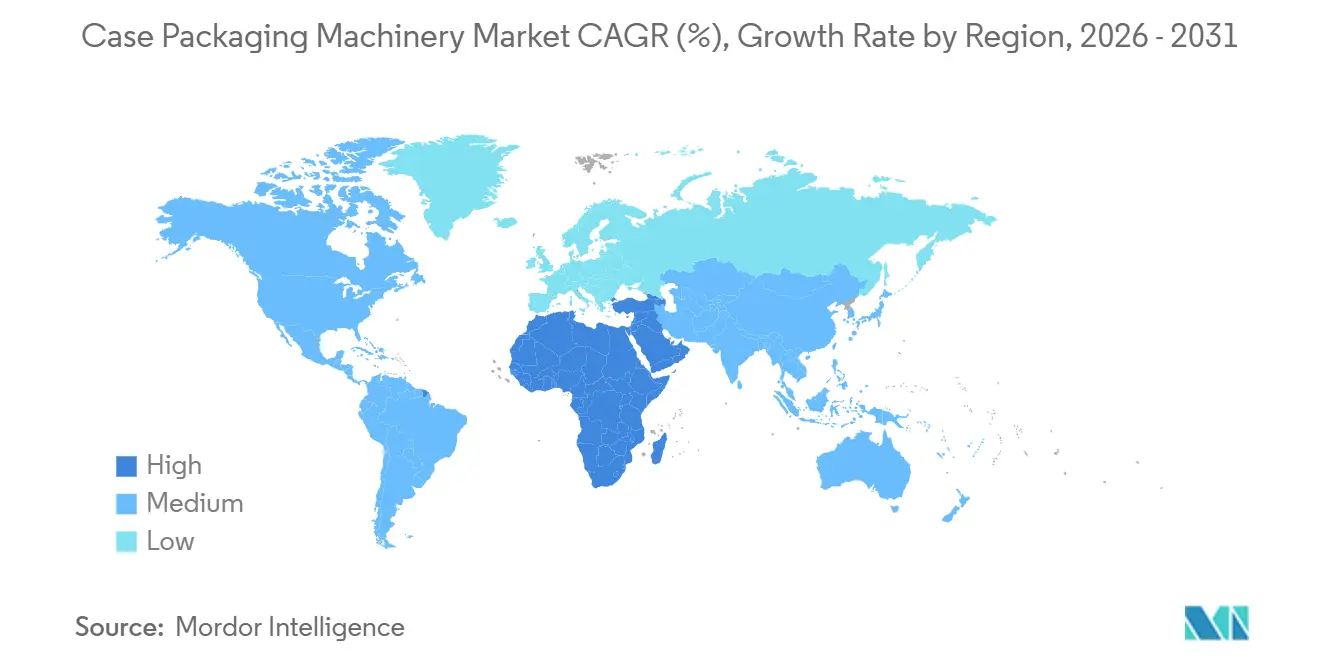

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

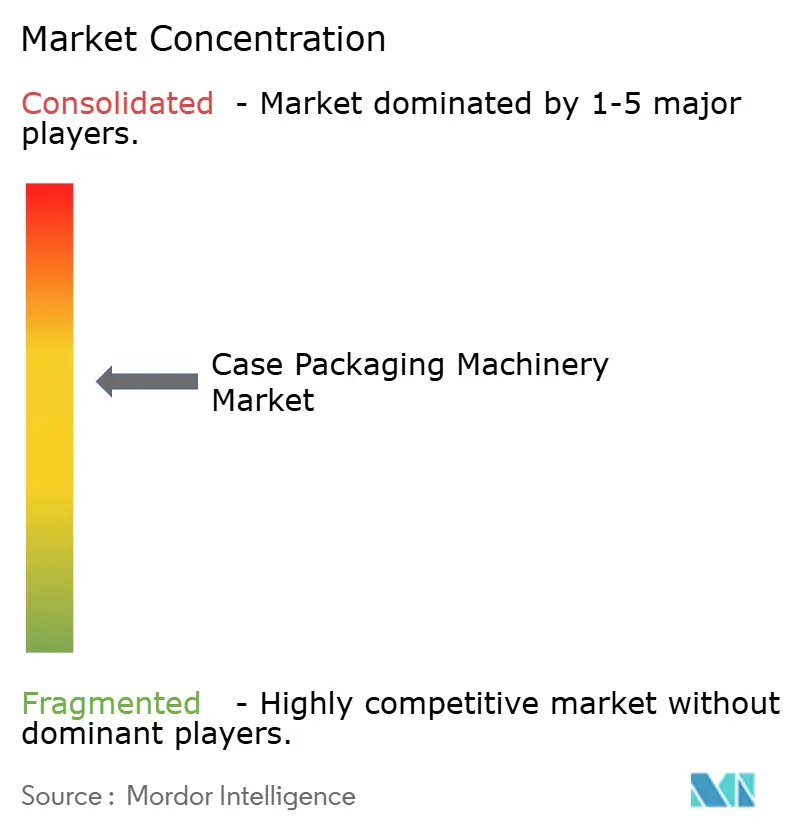

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Case Packaging Machinery Market Analysis by Mordor Intelligence

The case packaging machinery market size is currently USD 3.12 billion in 2026 and is projected to increase to USD 3.94 billion by 2031, reflecting a 4.78% CAGR throughout the forecast period. Escalating e-commerce order volumes, rising labor expenses in developed economies, and the need for hygienic equipment designs are reshaping demand patterns. End-users now favor robotic systems that manage more than 500 cases per minute, complete 15–20 SKU changeovers per shift, and compress payback periods to less than two years. Parallel sustainability mandates are steering buyers toward wraparound formats that cut corrugated usage by up to 18%, while predictive-maintenance software is gaining traction as manufacturers seek to curtail unplanned downtime by up to 40%.

Key Report Takeaways

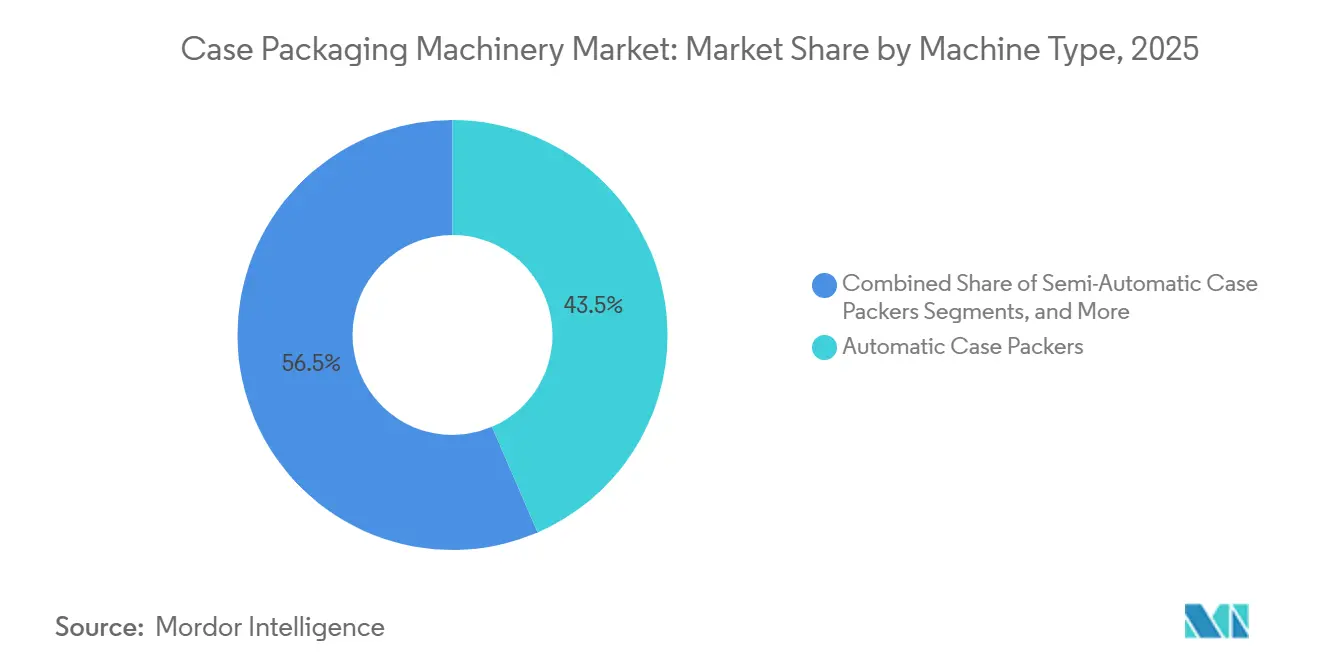

- By machine type, automatic case packers captured 43.52% of the case packaging machinery market share in 2025.

- By packaging speed, the case packaging machinery market size for machinery with more than 500 CPM is projected to grow at a 6.53% CAGR between 2026–2031.

- By product type, side-load configurations captured 38.39% of the case packaging machinery market share in 2025.

- By end-user industry, the case packaging machinery market size for personal care and cosmetics is projected to grow at a 6.84% CAGR from 2026 to 2031.

- By geography, the Asia-Pacific captured 39.81% of the case packaging machinery market share in 2025.

Global Case Packaging Machinery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding E-Commerce Requiring High-Throughput Secondary Packaging | +1.2% | Global, concentrated in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising Labor-Cost Inflation Propelling Demand for Automated Case Packers | +1.5% | North America, Western Europe, Japan, South Korea | Short term (≤ 2 years) |

| Stringent Food-Safety Regulations Boosting Adoption of Hygienic Machinery | +0.8% | Global, led by North America and the European Union | Long term (≥ 4 years) |

| Integration of Vision-Guided Robotics Reducing Change-Over Time | +0.9% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Sustainability Mandates Driving Corrugated Lightweight Case Formats | +0.6% | Europe and North America, and emerging Asia-Pacific | Medium term (2-4 years) |

| Surge in SKU Proliferation Pushing Need for Modular, Quick-Format Systems | +1.1% | Global, especially North America and Europe, CPG | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding E-Commerce Requiring High-Throughput Secondary Packaging

Global e-commerce shipments increased 23% year-over-year in 2024, prompting fulfillment centers to adopt case packers that can handle over 500 cases per minute to maintain same-day delivery promises. Amazon’s plan to add 50 automated fulfillment nodes across North America and Europe in 2025 alone will require roughly 900 high-speed packaging cells, underscoring the swelling installed base.[1]Amazon, “Amazon Announces Expansion of Fulfillment Network,” Press Release, aboutamazon.com Robotic systems equipped with 3D vision manage mixed-SKU orders without manual resets, which supports the ongoing decline in average cases per shipment from 24 in 2020 to 16 in 2024. Labor headcount per shift drops 30%–50% after automation, a critical offset against U.S. warehouse wage growth of 12% in 2024. These dynamics collectively fuel new orders, particularly for modular designs that fit into constrained urban facilities.

Rising Labor-Cost Inflation Propelling Demand for Automated Case Packers

Hourly operator wages rose USD 3.20 in the United States and EUR 2.40 (USD 2.70) in Germany during 2024, lifting cap-ex attractiveness for fully automated lines. Return-on-investment windows have tightened to 18–24 months, encouraging manufacturers to install lights-out robotic cells across second and third shifts. Nestlé documented a 35% per-case labor-cost reduction after deploying such cells at 14 European plants. Wage inflation is also significant in China and India, where annual increases of 8%–10% are eroding labor advantages and prompting multinational corporations to adopt global automation standards. Collaborative robots priced below USD 40,000 widen access for mid-sized contract packagers, further broadening the addressable market for case packaging machinery.

Stringent Food-Safety Regulations Boosting Adoption of Hygienic Machinery

The FDA’s 2026 traceability rule necessitates electronic lot records, driving preference for packers with in-line serialization and IP69K stainless-steel frames. Compliance adds roughly 15%–20% to purchase prices but is non-negotiable for dairy, meat, and ready-to-eat operators. The European Union’s Regulation 2073/2005 triggered widespread retrofits across 2,400 continental facilities, as processors replaced painted-steel frames that foster biofilms with EHEDG-certified hygienic designs. Pharmaceutical plants follow parallel GMP requirements, specifying ISO 14644 Class 7 compatibility. Together, these directives sustain long-run equipment upgrades, especially in mature regions where regulatory scrutiny is most stringent.

Integration of Vision-Guided Robotics Reducing Change-Over Time

Vision-guided packers integrate 3D cameras with AI algorithms to recognize product orientation, adjusting gripper trajectories in real-time. Omron’s platform cut changeovers from 45 minutes to 8 minutes on Japanese beverage lines in 2024, unlocking economical batches as small as 500 cases. Rockwell Automation achieved 99.7% pick accuracy on similarly equipped lines, resulting in a reduction of annual product damage by USD 120,000 in mid-volume operations. Unilever has already implemented the technology in 18 North American facilities to facilitate round-the-clock production. As software modules mature, buyers view rapid format agility and self-diagnosis as core investment criteria.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Nature of Fully Automated Lines | -0.9% | Global, especially South America, Africa, and smaller Asia-Pacific markets | Short term (≤ 2 years) |

| Volatility in Corrugated Board Prices Affects TCO Calculations | -0.6% | Global, heightened where pulp imports dominate | Medium term (2-4 years) |

| Scarcity of Skilled Maintenance Technicians | -0.5% | North America, Europe, and developed Asia-Pacific | Long term (≥ 4 years) |

| Cyber-Security Vulnerabilities in Connected Packaging Lines | -0.3% | Global, early concern in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Nature of Fully Automated Lines

Turnkey case-packing lines cost USD 500,000–1.5 million, exceeding the annual capital expenditure limits for many regional processors. Equipment-as-a-service offerings from financiers, such as Siemens Financial Services, provide 60-month leases at 4%–6% interest; yet, small enterprises remain cautious about long-term liabilities. Total cost of ownership also includes maintenance contracts at 8%–12% of the purchase price, as well as software fees of up to USD 25,000 per line each year. High interest rates in 2024 deferred several projects, with major builders reporting order declines of 12% to 18%. Semi-automatic alternatives priced between USD 80,000 and USD 150,000, therefore retain relevance among liquidity-constrained buyers in South America and Africa.

Volatility in Corrugated Board Prices Affects TCO Calculations

Corrugated board spiked 18% in early 2024 following pulp disruptions, then fell 10% by Q3 as capacity recovered. Since lightweight wraparound formats deliver 15%–18% savings only when board costs are stable, volatility complicates ROI forecasts. Engineers also need four to six weeks to recalibrate vacuum grippers and form modules for thinner grades, temporarily reducing line efficiency. Regions dependent on imported pulp, such as the Middle East and parts of Asia-Pacific, confront exchange-rate risk because invoices are denominated in USD or EUR. Lenders often insist on steady input-cost assumptions; swings greater than 15% in a year can invalidate projected cash flows, delaying new equipment financing.

Segment Analysis

By Machine Type: Robotic Flexibility Gains Favor

Automated case packers commanded 43.52% of the case packaging machinery market in 2025, reflecting their entrenched role in high-volume food and beverage operations. Robotic systems, advancing at a 6.12% CAGR, are quickly closing the gap by offering redeployable cells that can manage 80-120 SKUs without mechanical retooling. Semi-automatic units hold traction where batch sizes hover between 200 and 500 cases, as artisanal producers value manual intervention capabilities. Force-torque sensors paired with AI motion planning enable robots to handle fragile glass jars, resulting in a 22% reduction in breakage at a European cosmetics plant last year. Fixed-automation models still dominate beverage and canned-goods lines that run single formats at more than 400 cases per minute, yet hybrid configurations are blurring distinctions by combining servo-driven speed with cobot adaptability.

Demand is rising fastest in personal care and pharmaceuticals, where format diversity and frequent line changeovers outpace traditional tooling economics. Automatic systems retain an advantage in throughput stability, but new robotic entries priced roughly 60% lower than legacy six-axis units have lower adoption barriers. Regional dynamics echo these shifts: European and Japanese incumbents rely on engineering depth, while East Asian challengers leverage lower costs to tempt mid-tier buyers. Across all machine types, predictive-maintenance software is becoming a standard feature, as it aligns with buyer priorities to minimize downtime and support remote diagnostics in labor-constrained plants.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Speed: Ultra-High Throughput Pulls Ahead

The 201–500 CPM bracket captured 39.03% of installations in 2025, serving mid-tier lines across food processing, household care, and light industrial sectors. Systems topping 500 CPM, however, are projected to log a 6.53% CAGR through 2031 as fulfillment centers and mega-scale beverage plants seek 24-hour uptime. Equipment exceeding 500 CPM uses servo motors with sub-millisecond response times, vision devices that inspect 10 cases per second, and vibration-dampening frames that maintain 99.5% uptime. One North American beverage producer saved USD 0.08 per case, or USD 2.4 million annually, after upgrading from 350 CPM to 550 CPM machinery in 2024. At the low end, sub-50 CPM gear remains favored by craft producers who switch products multiple times per shift; here, quick-change tooling lets operators reset within 10 minutes.

Mid-speed lines between 51 and 200 CPM appeal to contract packagers that juggle diverse portfolios yet demand traceable, repeatable performance. ISO 11607 compliance requirements in pharmaceutical packaging often intersect with this speed range, reinforcing demand for high-reliability motion control. Throughout all brackets, the case packaging machinery market size for high-speed models continues to rise as e-commerce players scale their distribution hubs, whereas slower units retain relevance due to their lower capital expenditure and ease of operation.

By Product Type: Wraparound Systems Ride the Sustainability Wave

Side-load equipment represented 38.39% of 2025 deployments, which is favored for tall or unstable products that require lateral support. Wraparound systems are forecast to grow at a 7.18% CAGR as brands adopt corrugated designs that reduce material use by up to 18% and align with the 2030 European recycled-content targets. Top-load packers remain the workhorse for canned goods and boxed foods, offering the highest throughput at the lowest capital cost. Equipment purchasers now weigh the total cost of ownership rather than the acquisition price alone; in high-volume scenarios, wraparound machinery offsets its 15%-20% price premium within two years through board savings.

Innovation is accelerating across all three formats. Servo-driven flap-folding in modern side-load machines now covers case heights from 150 mm to 450 mm without physical change parts. Top-load units continue to excel in rapid SKU swaps, completing blank changes in under five minutes, a critical feature for specialty food processors. Pharmaceutical plants require side-load paths to maintain barcode integrity, demonstrating how regulatory compliance influences format selection. As environmental regulations tighten, the case packaging machinery market is likely to see wraparound solutions adopted beyond Europe into North America and, later, the Asia-Pacific region.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Personal Care Outpaces Traditional Segments

Food and beverages accounted for 47.72% of 2025 demand, driven by dairy, bakery, and beverage producers that require hygienic, high-throughput lines certified by EHEDG and 3-A standards. Personal care and cosmetics, which are expanding at a 6.84% CAGR, are the fastest-growing vertical, driven by direct-to-consumer models with batch sizes as small as 500 cases. Robotic cells that handle irregular containers reduce labor by up to 50% and boost on-time delivery, as evidenced by L’Oréal’s deployment of 22 units across Europe and North America. Pharmaceutical companies invest heavily in serialization-ready packaging; integrating track-and-trace modules can add USD 50,000–80,000 per line, but this remains mandatory under the U.S. Drug Supply Chain Security Act.

Household care and industrial packaging emphasize mechanical durability and ease of maintenance, given the abrasive contents that accelerate component wear. Across all verticals, the rising proliferation of SKUs and the influence of e-commerce are intensifying the need for rapid changeovers and smaller batch sizes. The packaging machinery market, therefore, continues to diversify, with suppliers tailoring feature sets to sector-specific regulatory and operational requirements.

Geography Analysis

North America and Europe together host a significant share of premium case-packer installations, reflecting high labor costs, strict regulatory frameworks, and well-developed automation ecosystems. U.S. food giants such as PepsiCo and Kraft Heinz earmarked USD 1.2 billion for packaging-line upgrades in 2024, focusing on robotic platforms that bolster FSMA traceability mandates. Germany, Italy, and France dominate European demand, exporting significant volumes and leveraging their engineering prowess in hygienic and servo-driven technologies. Post-Brexit regulatory divergence in the United Kingdom has added 10%–15% to compliance costs, as multinational firms must now validate equipment separately, extending project timelines.

The Asia-Pacific region represents the largest market for case packaging machinery, driven by India’s INR 109 billion (USD 1.3 billion) Production-Linked Incentive scheme for the food processing industry and China’s dual-circulation strategy, which encourages local machinery development.[2]Government of India, “Production-Linked Incentive Scheme for Food Processing Industry,” mofpi.gov.in Domestic suppliers price robotic systems 25%–35% lower than Western offerings, although some multinationals question their long-term reliability. Japan and South Korea present mature replacement markets; firms like Omron and Yaskawa are exporting vision-guided expertise to North America and Europe, reinforcing global competitive parity.

Middle East and Africa represents the fastest growing region, albeit from a smaller base, while South America contribute smaller volumes but offer strategic upside. Brazil invested USD 420 million in packaging automation in 2024, primarily in semi-automatic units that strike a balance between cost and throughput. The Middle East’s industrial diversification is channeling USD 2.8 billion into food security and pharmaceutical capacity, part of which funds new case-packing lines. African adoption remains restricted to South Africa and Nigeria, where consumer-goods multinationals localize plants to skirt tariffs, gradually expanding the installed base.

Competitive Landscape

The case packaging machinery industry exhibits moderate concentration, with the top ten suppliers accounting for roughly 55%–60% of the global revenue. Market leaders such as Tetra Pak, Syntegon, and IMA leverage vertically integrated mechanics, controls, and aftermarket services to embed customers inside proprietary ecosystems. Differentiation increasingly hinges on digital-twin simulations, predictive-maintenance analytics, and vision-guided QC that lower the total cost of ownership.

Tier-2 builders from China and South Korea are undercutting incumbents on price and rapidly improving their quality, thereby winning a share of the mid-tier market. Software-centric disruptors retrofit legacy lines with IoT sensors for predictive maintenance, extending asset life and delaying cap-ex. Omron’s 2024 patent on AI-adjusted gripper parameters exemplifies intelligence at the edge, reducing reliance on central PLCs and speeding up SKU switches.

Suppliers are also exploring vertical integration into the corrugated supply chain to combine equipment and consumables, echoing Tetra Pak’s liquid food model.[3]Tetra Pak, “Modular Packaging Systems Expansion,” tetrapak.com Equipment-as-a-service models, where vendors own machines and charge per-case fees, gained momentum after 2024 rate stabilization, shifting risk to equipment providers while easing investment hurdles for end-users.

Case Packaging Machinery Industry Leaders

-

Tetra Pak International S.A.

-

Syntegon Technology GmbH

-

IMA Industria Macchine Automatiche S.p.A.

-

Marchesini Group S.p.A.

-

Shibuya Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Tetra Pak announced a EUR 45 million (USD 49 million) expansion of its Modena, Italy, facility to boost robotic case-packing cell production for dairy and plant-based beverages.

- September 2025: Syntegon Technology acquired a 60% stake in a Chinese vision-systems integrator to shorten format-changeover times by 40% in its Asia-Pacific offerings.

- August 2025: IMA Group introduced the Ares HF hygienic robotic case packer, certified to EHEDG and ISO Class 7 standards for pharmaceutical serialization.

- July 2025: Shibuya Corporation partnered with a logistics firm to install 18 case-packing lines, each exceeding 600 CPM, in Japanese e-commerce hubs.

Global Case Packaging Machinery Market Report Scope

The study tracks the demand for case forming, packing, and filling machinery sales based on end-user trends and vendor activities. The study encompasses a portion of a broader offering on the packaging machinery sector, which covers several sub-types within the packaging industry.

The Case Packaging Machinery Market Report is Segmented by Machine Type (Robotic Case Packers, Automatic Case Packers, and Semi-Automatic Case Packers), Packaging Speed (Less than 50 CPM, 51-200 CPM, 201-500 CPM, and More than 500 CPM), Product Type (Top-Load, Side-Load, and Wraparound), End-user Industry (Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, Household Care, Industrial, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Robotic Case Packers |

| Automatic Case Packers |

| Semi-Automatic Case Packers |

| Less than 50 CPM |

| 51–200 CPM |

| 201–500 CPM |

| More than 500 CPM |

| Top-Load |

| Side-Load |

| Wraparound |

| Food and Beverages |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Household Care |

| Industrial |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Robotic Case Packers | ||

| Automatic Case Packers | |||

| Semi-Automatic Case Packers | |||

| By Packaging Speed | Less than 50 CPM | ||

| 51–200 CPM | |||

| 201–500 CPM | |||

| More than 500 CPM | |||

| By Product Type | Top-Load | ||

| Side-Load | |||

| Wraparound | |||

| By End-user Industry | Food and Beverages | ||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Household Care | |||

| Industrial | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the case packaging machinery market in 2026?

The global case packaging machinery market size is expected to reach USD 3.12 billion by 2026.

What CAGR is forecast for case packaging machinery to 2031?

The market is projected to register a 4.78% CAGR between 2026 and 2031.

Which end-user segment is growing fastest for case packaging machinery?

Personal care and cosmetics are projected to lead with a 6.84% CAGR through 2031.

Why are wraparound systems gaining popularity?

They cut corrugated material use by up to 18%, supporting corporate sustainability goals and quick payback.

Which geography is expanding fastest?

The Asia-Pacific region is the fastest-growing due to India’s incentives and China’s domestic machinery push.

How does automation lower labor costs in packaging?

Robotic case packers can reduce per-case labor expenses by 30%–50% and shorten ROI periods to under two years.

Page last updated on: