Cartilage Repair/Regeneration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

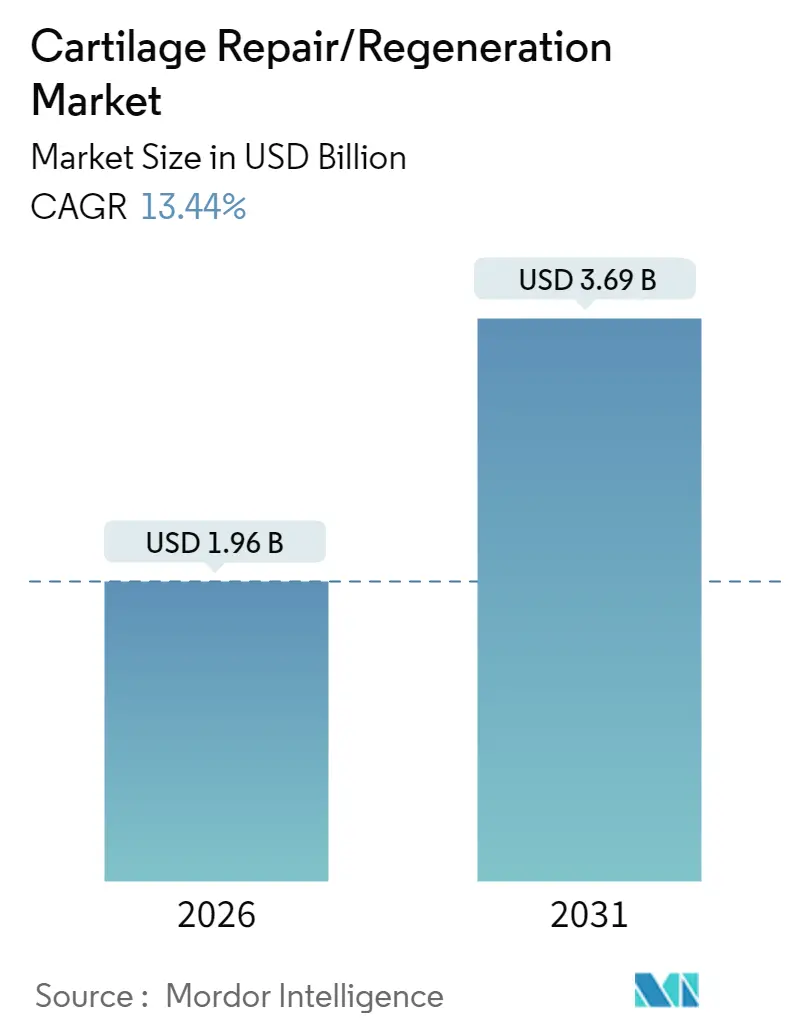

| Market Size (2026) | USD 1.96 Billion |

| Market Size (2031) | USD 3.69 Billion |

| Growth Rate (2026 - 2031) | 13.44% CAGR |

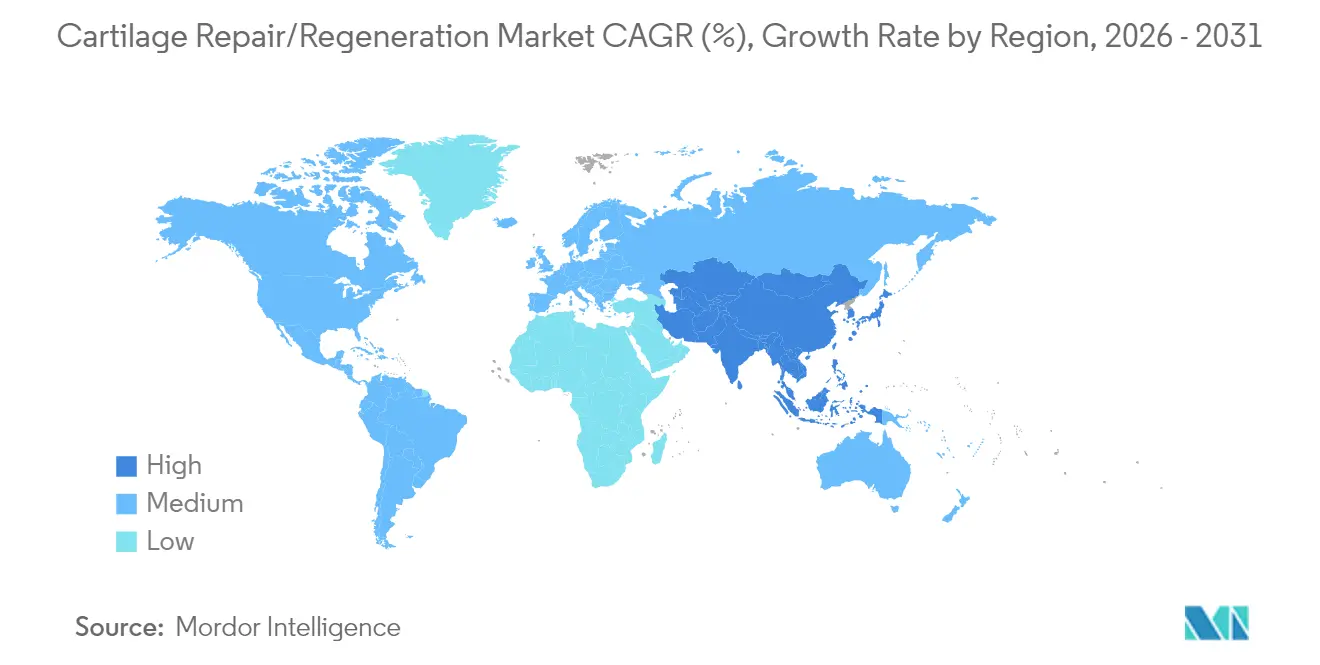

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cartilage Repair/Regeneration Market Analysis by Mordor Intelligence

Cartilage repair/regeneration market size in 2026 is estimated at $1.96 billion, growing from 2025 value of $1.73 billion with 2031 projections showing USD 3.69 billion, growing at 13.44% CAGR over 2026-2031. Demographic aging, rising obesity, and sports injury volumes expand the patient pool, while technological advances in cell-based implants and tissue-engineered scaffolds improve clinical outcomes. Outpatient arthroscopic procedures shorten recovery times and lower costs, reinforcing payer and provider adoption. North America leads revenue generation, but Asia-Pacific posts the fastest expansion as healthcare infrastructure and disposable incomes climb. Competitive activity is steady, with large device firms acquiring niche innovators to secure next-generation technologies.

Key Report Takeaways

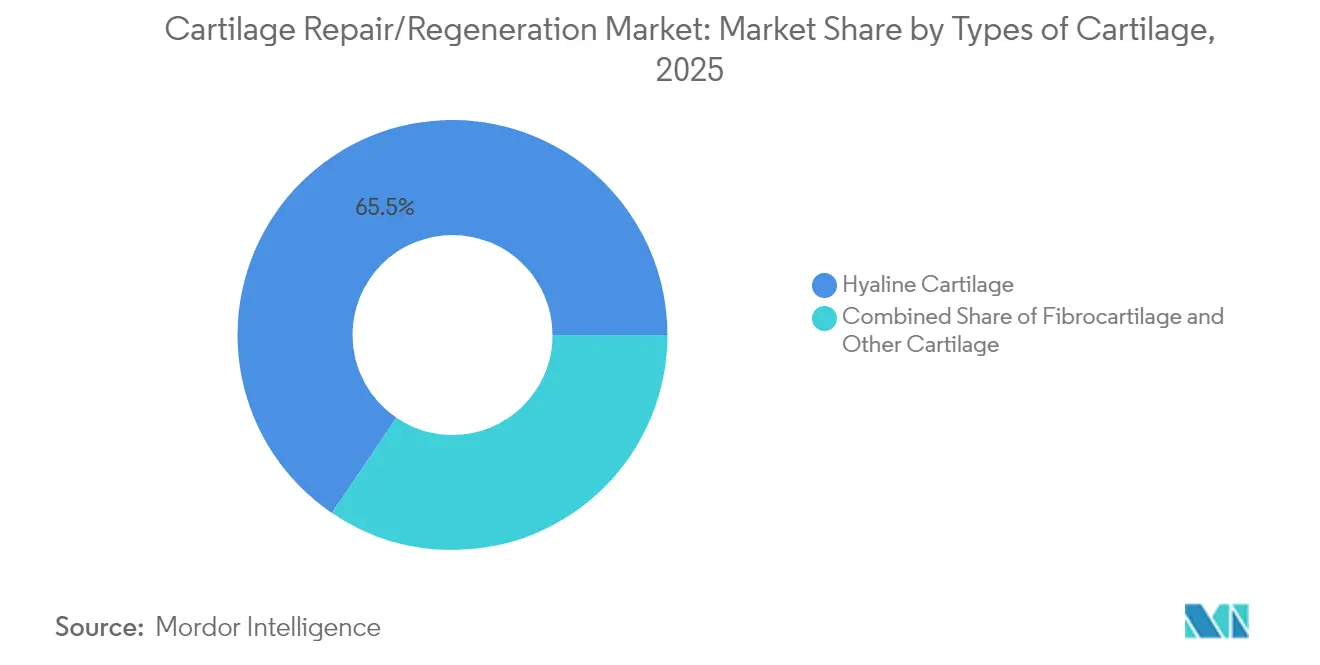

- By cartilage type, hyaline tissue dominated with 65.52% cartilage repair/regeneration market share in 2025, whereas fibrocartilage is projected to grow at a 14.02% CAGR through 2031.

- By treatment modality, cell-based approaches captured 61.72% of the cartilage repair/regeneration market size in 2025; non-cell-based options record the highest forecast growth at 14.21% CAGR.

- By treatment type, palliative procedures held 54.66% of revenue in 2025, while intrinsic repair stimulus methods are expected to accelerate at 13.98% CAGR.

- By surgical technique, chondroplasty and microfracture accounted for 27.74% of the cartilage repair/regeneration market size in 2025; matrix-induced ACI is set to lead growth at 14.55% CAGR.

- By application site, knee interventions commanded 49.62% of 2025 revenue, yet ankle repairs should advance fastest with 14.83% CAGR.

- By end user, hospitals and clinics controlled 61.85% of spending in 2025; ambulatory surgical centers are forecast to expand at 14.56% CAGR.

- By geography, North America contributed 44.72% of 2025 sales, while Asia-Pacific is projected to post a 15.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cartilage Repair/Regeneration Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden Of Heart Failure & Other Cardiac Disorders | +1.5% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rapidly Expanding Geriatric Population And Sedentary Lifestyles | +0.8% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) |

| Break-Through Product Innovations | +0.6% | North America & Europe first, then Asia-Pacific | Medium term (2-4 years) |

| Favourable Reimbursement & HF Disease-Management Mandates In OECD Nations | +0.4% | OECD countries, spillover to emerging markets | Medium term (2-4 years) |

| AI-Driven CRT Optimisation & Predictive Analytics Platforms | +0.3% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Commercialisation Of Leadless & Modular CRT Systems In Emerging Markets | +0.2% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Incidence of Osteoarthritis and Traumatic Cartilage Lesions

Surging osteoarthritis prevalence, which climbed 132.2% between 1990 and 2022, now affects 7.96% of the global population and drives sustained demand for restorative surgery. Adult cases aged 30-44 exceeded 32.97 million in 2022, underscoring a shift toward younger patients seeking durable repair solutions. Chondral defects afflict 36% of athletes’ knees, creating a sizable cohort that prefers definitive intervention over symptom management [1]Litchfield R et al., “Athlete Knee Chondral Defects,” journals.lww.com. The widening patient base ensures that the cartilage repair/regeneration market remains on an expanding trajectory through the decade.

Surge in Outpatient Minimally Invasive Orthopedic Procedures

Same-day discharge for joint surgeries in the United States rose from less than 1% in 2017 to 30.5% in 2023, demonstrating payer and provider confidence in ambulatory pathways. FDA clearance of MACI Arthro in August 2024 validated arthroscopic delivery of autologous chondrocyte implants, further normalizing outpatient treatment. Ambulatory surgical centers benefit most, displaying a 15.07% CAGR through 2030 as they combine cost savings with better patient convenience. This procedural migration underpins broader adoption across the cartilage repair/regeneration market.

Breakthroughs in Tissue-Engineered Scaffolds and Cell-Based Implants

Nanofiber “dancing molecule” technology from Northwestern University stimulates cartilage formation within hours, signaling future one-step biologic repairs. EU-funded ENCANTO is advancing nasal-septum chondrocyte constructs for knee defects, illustrating public investment in translational science. Clinical trials pairing allogeneic mesenchymal stromal cells with autologous chondrons show superior results to legacy techniques. These innovations collectively raise treatment efficacy and underpin premium pricing within the cartilage repair/regeneration market.

Increasing Participation in High-Impact and Recreational Sports

Soccer alone generated 843,063 lower-extremity injuries between 2014 and 2023, with 47% classified as strains or sprains that often involve cartilage damage. Track and field recorded 128,761 such injuries over the same period, with female athletes facing 58% higher risk. Rising female sports participation broadens demand for ligament and cartilage repair solutions. This youthful, active demographic values rapid return to play, boosting acceptance of advanced regenerative therapies across the cartilage repair/regeneration market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Multi-Region Regulatory Requirements And Lengthy Approval Cycles | -0.7% | Global, particularly impacting new market entries | Medium term (2-4 years) |

| High Procedure/Device Cost & Limited Implanter Skill Base | -0.5% | Emerging markets, rural areas in developed countries | Long term (≥ 4 years) |

| Supply-Chain Vulnerability For Rare-Earth Magnets And Semiconductor ICs | -0.4% | Global, with highest impact on Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Rising Clinical Scrutiny Of Non-Responder Rates Spurring CSP Substitutes | -0.3% | North America & Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure and Implant Costs Limiting Uptake

Stem-cell knee therapy costs range between USD 5,000 and USD 15,000 in South Korea, restricting adoption beyond affluent or insured patients. China’s volume-based procurement cut total hip arthroplasty prices by 50.1%, highlighting intense cost pressure that could spill over to cartilage technologies. Blue Cross payers in the United States mandate stringent criteria for autologous chondrocyte implantation, illustrating reimbursement hurdles. These economic constraints slow penetration in price-sensitive regions, tempering cartilage repair/regeneration market growth.

Lengthy and Complex Regulatory Approval Pathways

The European Medicines Agency requires extensive additional monitoring for 88% of cell and gene therapy products, extending time to market [2]European Medicines Agency, “Additional Monitoring for ATMPs,” ema.europa.eu . In the United States, combination products blending biologics and devices face dual-center review, prolonging timelines and increasing capital needs. Smaller innovators often lack resources for multipronged submissions, postponing commercialization and limiting competitive intensity in the cartilage repair industry.

Segment Analysis

By Types of Cartilage: Hyaline Dominance Reflects Weight-Bearing Demands

Hyaline tissue held 65.52% of revenue in 2025, confirming its central role in load-bearing joints most vulnerable to degeneration. Bilayer atelocollagen scaffolds now replicate hyaline morphology more reliably, improving long-term outlook for patients. Fibrocartilage, driven by meniscal repair needs, is projected to expand at 14.02% CAGR, supported by advances in collagen-based hydrogels that recruit endogenous stem cells.

The cartilage repair/regeneration market size for hyaline applications is projected to widen further as surgeons prioritize tissue-specific products that enhance integration. Meanwhile, niche elastic-cartilage reconstruction for ear and nasal defects creates incremental volume, diversifying revenue streams across smaller sub-segments.

Note: Segment shares of all individual segments available upon report purchase

By Treatment Modality: Cell-Based Therapies Lead Regenerative Revolution

Cell-based solutions captured 61.72% revenue in 2025 through clinical superiority in pain reduction and tissue restoration, as evidenced by meta-analysis reporting standardized mean differences of –1.27 in pain scores . However, cell-free implants should post 14.21% CAGR through 2031 on the strength of off-the-shelf availability and lower cost.

Premium products such as MACI generated USD 46.3 million in Q1 2025 sales, reflecting commercial traction in the United States. Conversely, CARTIHEAL Agili-C offers a cell-free scaffold that reduced total knee arthroplasty risk by 87% at four years. Healthy rivalry between personalized and ready-to-use solutions ensures a balanced growth outlook across the cartilage repair/regeneration market.

By Treatment Type: Palliative Procedures Dominate Current Practice

Palliative options—debridement, lavage, viscosupplementation—accounted for 54.66% of sales in 2025 because they impose minimal procedural complexity and allow rapid symptom relief. Yet intrinsic repair stimulus techniques such as microfracture, autologous chondrocyte implantation, and micro-fragmented adipose injections should climb at 13.98% CAGR.

Ten-year MACI outcomes show durable improvements in function and MRI morphology, spurring clinician confidence. This evidence nudges payers toward reimbursing curative approaches, progressively shifting revenue mix within the cartilage repair/regeneration market.

By Surgical Technique: Microfracture Leads Despite Limitations

Chondroplasty and microfracture retained 27.74% share in 2025 because they require no specialized infrastructure. Matrix-induced ACI, however, is forecast to expand 14.55% CAGR as larger lesion indications and arthroscopic delivery gain traction. FDA-cleared arthroscopic MACI simplifies operating-room workflow, aligning with outpatient migration.

Robotic assistance further refines precision; the global orthopedic robot pool is set to double by 2030. These enablers lay groundwork for scalability, broadening the cartilage repair/regeneration market size among complex cases previously judged inoperable.

By Application Site: Knee Dominance Drives Market Concentration

Knee interventions held 49.62% revenue in 2025, mirroring 364.58 million global knee-osteoarthritis cases. Ankle repairs, buoyed by talar autograft innovations, are poised for 14.83% CAGR as clinical outcomes improve.

The cartilage repair/regeneration market share of knee procedures may dilute slightly as ankle, hip, and shoulder indications mature, yet knees will remain the anchor of procedural volume. Site-specific instruments from Arthrex and others reinforce adoption across multiple joints.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospital Dominance Faces Outpatient Challenge

Hospitals and clinics controlled 61.85% of revenue in 2025 thanks to their capacity for complex, multiphase treatments. Ambulatory surgical centers should grow 14.56% CAGR as arthroscopic techniques shorten stay length.

The cartilage repair industry sees office-based biologic injections emerging as the next frontier, enabling physicians to capture more value and widening access in rural regions with limited surgical capacity.

Geography Analysis

North America produced 44.72% of 2025 revenue, underpinned by FDA clearances and consistent private‐payer reimbursement. Vericel, Arthrex, and Stryker dominate surgeon preference, while Johnson & Johnson’s VELYS unicompartmental knee robot received clearance in June 2024, spotlighting ongoing innovation. Growth remains steady as baby-boomer activity levels sustain procedure volumes.

Asia-Pacific is projected to deliver a 15.02% CAGR, buoyed by infrastructure investment and rising disposable incomes. China’s procurement reforms, which halved implant prices, improve affordability even as regulatory pathways tighten. Japan leverages universal coverage for advanced therapies, whereas South Korea attracts inbound medical tourists for stem-cell knee repairs priced at USD 5,000-15,000. India’s expanding middle class gradually lifts procedure counts despite reimbursement gaps.

Europe sustains innovation momentum through EMA’s advanced therapy framework and EUR 11.3 million ENCANTO funding. Middle East & Africa and South America remain nascent yet compelling as economic development enlarges insured populations, positioning them as long-range demand reservoirs for the cartilage repair/regeneration market.

Note: Segment shares of all individual segments available upon report purchase

Competitive Landscape

The cartilage repair/regeneration market is moderately fragmented. Arthrex, Stryker, and Zimmer Biomet command established portfolios in microfracture and fixation devices. Cell-therapy specialists such as Vericel hold proprietary manufacturing know-how, while CartiHeal brought a first-in-class osteochondral scaffold to market prior to its USD 180 million sale to Smith & Nephew in 2023.

Competition centers on technology and evidence generation. Vericel’s arthroscopic MACI launch creates a short-term edge, whereas Smith & Nephew integrates CartiHeal with its robotics suite for comprehensive knee solutions.

Robotic platforms from Johnson & Johnson and Stryker sharpen surgical precision, fostering hospital loyalty. Off-the-shelf peptides, exosome products, and bioprinted grafts from emerging biotech firms could reset cost structures, intensifying rivalry and quickening product cycles across the cartilage repair/regeneration market.

Cartilage Repair/Regeneration Industry Leaders

Zimmer Biomet

Stryker Corporation

Arthrex, Inc.

Smith & Nephew plc

Vericel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Zimmer Biomet agreed to acquire Paragon 28 for USD 1.1 billion, expanding its foot-and-ankle franchise.

- August 2024: Northwestern University unveiled an injectable hyaluronic-acid-peptide hydrogel that rapidly forms mature cartilage in preclinical knees.

- April 2024: Hyalex Orthopaedics initiated first-in-human trials of its HYALEX Knee Cartilage System in the United States and Europe.

- May 2024: Altach secured EUR 1.2 million to advance a type-II collagen scaffold that mimics native articular biomechanics.

- November 2023: Smith & Nephew completed the up-to-USD 330 million acquisition of CartiHeal, adding the FDA-approved Agili-C scaffold to its knee repair lineup.

Global Cartilage Repair/Regeneration Market Report Scope

As per the scope of the report, cartilage is a white polished material that helps cushion and cover the region where the bones meet joints. It acts as both a lubricating surface and a shock absorber. Cartilage damage can be a hole or crater on the smooth, superficial surface of the joint. The joint may become inflexible, swollen, and tender if left untreated. It can even develop to a stage that requires a total joint replacement with metal and plastic components. Cartilage repair or regeneration is a process that aims to restore injured cartilage by stimulating the body's cells to regrow or replace lost cartilage.

The cartilage repair/regeneration market is segmented by types of cartilage, treatment modality, treatment type, application, and geography. By type of cartilage, the market is segmented as fibrocartilage, hyaline cartilage, and others. By treatment modality, the market is bifurcated into cell-based and non-cell-based. By treatment type, the market is segmented as a palliative and intrinsic repair stimulus. By application, the market is segmented into knee, spine, ankle, hip, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers market sizes and forecasts for the cartilage repair/regeneration market in major countries across different regions. For each segment, the market size and forecasts are provided in terms of value (USD).

| Hyaline Cartilage |

| Fibrocartilage |

| Elastic / Other Cartilage |

| Cell-based Therapies |

| Non-cell-based / Cell-free Therapies |

| Palliative (Debridement, Viscosupplementation) |

| Intrinsic Repair Stimulus (ACI, MACI, Micro-fracture) |

| Chondroplasty & Micro-fracture |

| Autologous Chondrocyte Implantation (ACI) |

| Matrix-induced ACI (MACI) |

| Osteochondral Allograft / Juvenile Allograft |

| Knee |

| Hip |

| Ankle |

| Spine |

| Other Joints (Shoulder, Elbow, Wrist) |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Types of Cartilage | Hyaline Cartilage | |

| Fibrocartilage | ||

| Elastic / Other Cartilage | ||

| By Treatment Modality | Cell-based Therapies | |

| Non-cell-based / Cell-free Therapies | ||

| By Treatment Type | Palliative (Debridement, Viscosupplementation) | |

| Intrinsic Repair Stimulus (ACI, MACI, Micro-fracture) | ||

| By Surgical Technique | Chondroplasty & Micro-fracture | |

| Autologous Chondrocyte Implantation (ACI) | ||

| Matrix-induced ACI (MACI) | ||

| Osteochondral Allograft / Juvenile Allograft | ||

| By Application Site | Knee | |

| Hip | ||

| Ankle | ||

| Spine | ||

| Other Joints (Shoulder, Elbow, Wrist) | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the cartilage repair/regeneration market and how fast is it growing?

The cartilage repair/regeneration market is valued at USD 1.96 billion in 2026 and is projected to reach USD 3.69 billion by 2031.

Which region leads the cartilage repair/regeneration market?

North America accounts for 44.72% of 2025 revenue owing to early technology adoption and favorable reimbursement.

What segment holds the largest cartilage repair market share by treatment modality?

Cell-based therapies command 61.72% of global revenue due to their demonstrated regenerative benefits.

Why are ambulatory surgical centers growing faster than hospitals?

Outpatient arthroscopic techniques allow same-day discharge, lowering facility costs and driving a 14.56% CAGR for ASCs