Market Overview

| Study Period | 2019 - 2030 |

|---|---|

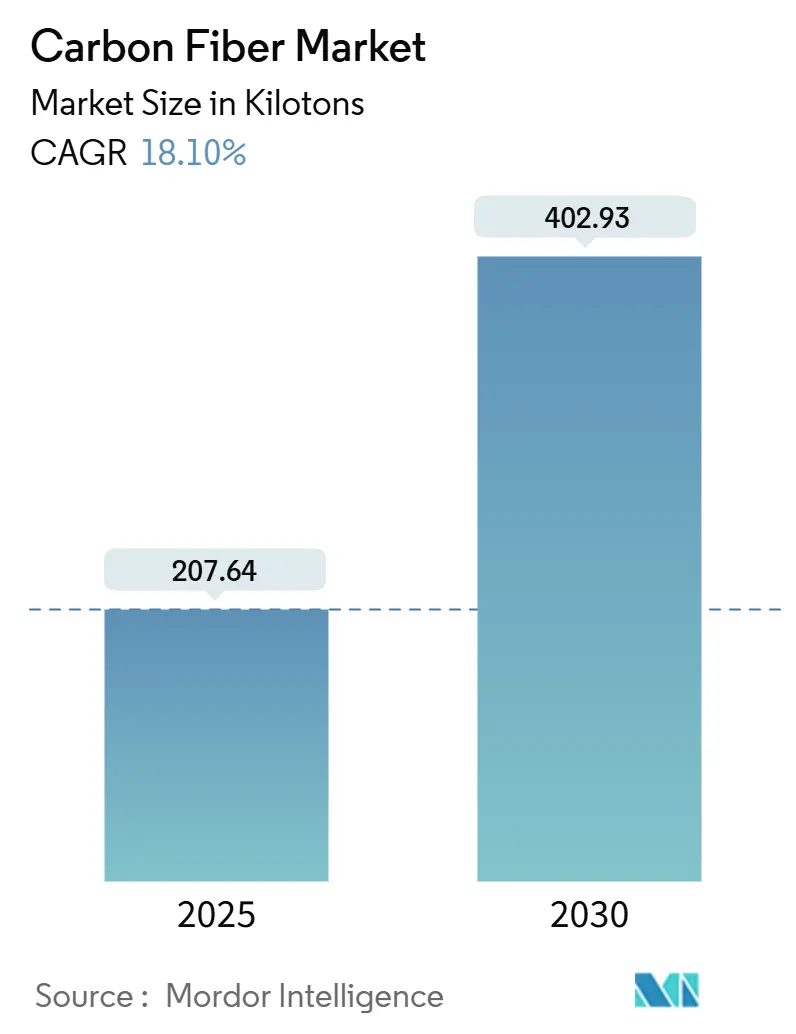

| Market Volume (2025) | 207.64 kilotons |

| Market Volume (2030) | 402.93 kilotons |

| Growth Rate (2025 - 2030) | 18.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Carbon Fiber Market Analysis by Mordor Intelligence

The carbon fiber market stands at 207.64 kilotons in 2025 and is forecast to reach 402.93 kilotons by 2030, expanding at an 18.10% CAGR for 2025-2030. Demand is scaling rapidly as multiple industries replace metals with lightweight composites to cut fuel use, shrink emissions, and unlock design flexibility. Major growth catalysts include fast-evolving aerospace programs, accelerating wind-turbine installations, rising adoption of high-pressure hydrogen vessels, and the spread of electric-vehicle (EV) lightweighting initiatives. Innovations such as microwave-assisted carbonization that trim manufacturing energy by as much as 70% are beginning to improve cost dynamics and could widen the total addressable carbon fiber market.

Key Report Takeaways

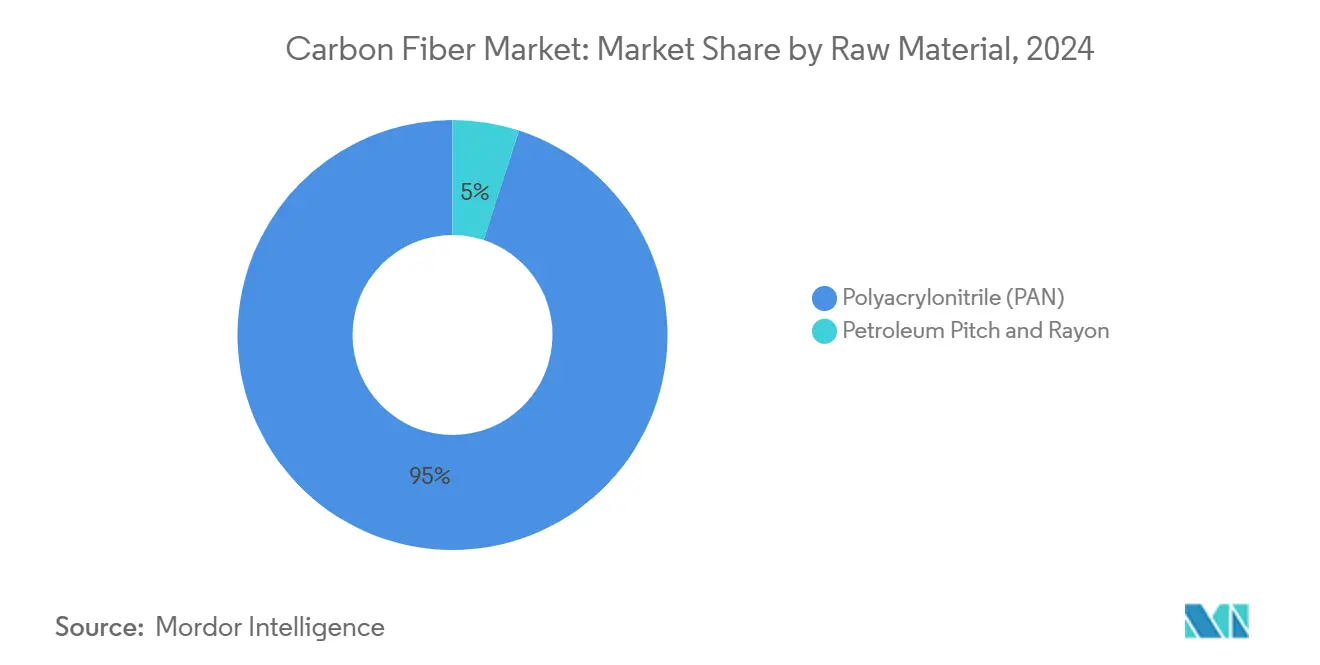

- By raw material, PAN retained 95% share of the carbon fiber market in 2024, and is expected to post the fastest 18.3% CAGR through 2030.

- By fiber type, virgin grades held 63% of the carbon fiber market share in 2024, while recycled grades are set to grow at a 19.5% CAGR to 2030.

- By application, composite materials captured 87% of the carbon fiber market size in 2024; micro-electrodes are expected to register the highest 25.0% CAGR between 2025-2030.

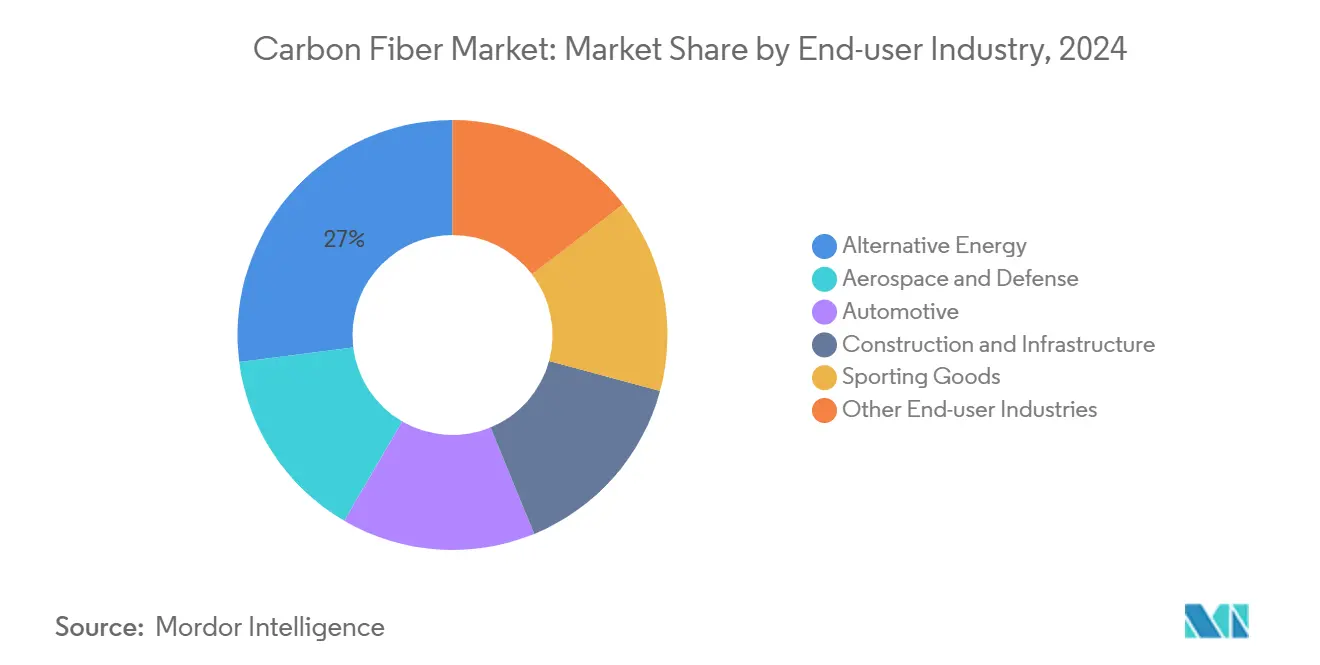

- By end-user industry, alternative energy led with 27% revenue share in 2024; the “others” cluster of emerging uses is forecast to advance at a 25% CAGR to 2030.

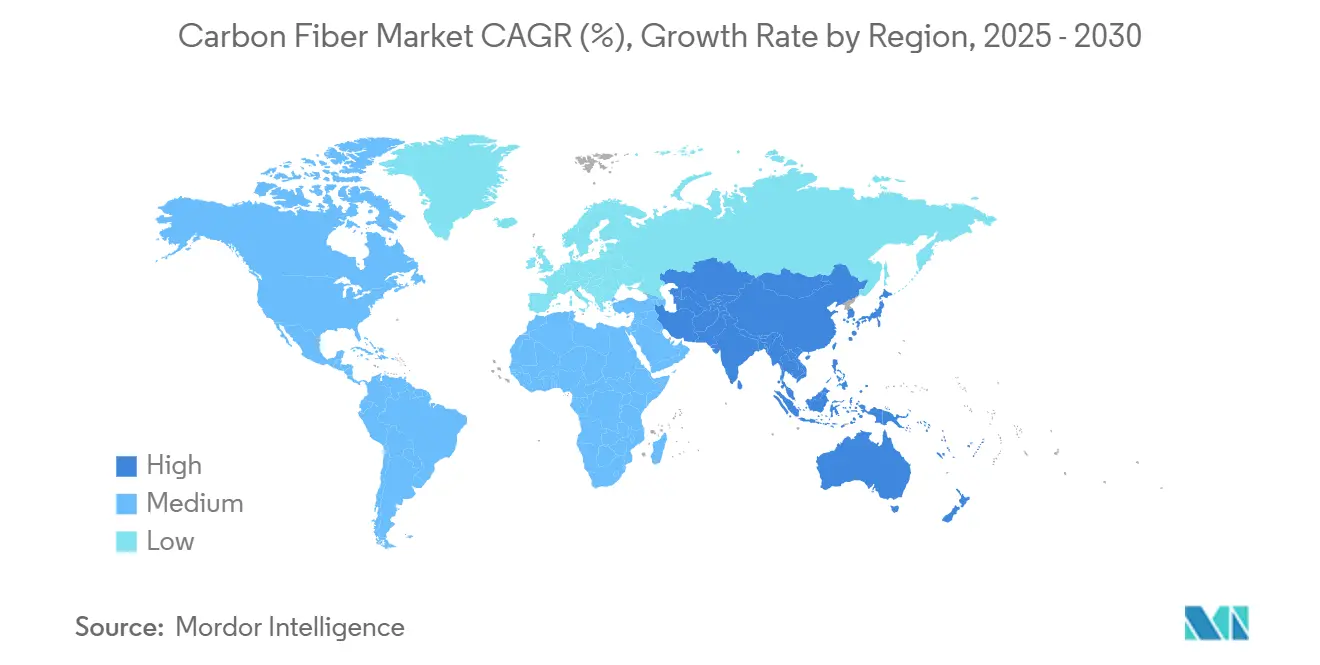

- By geography, Asia-Pacific commanded 44.3% of the carbon fiber market in 2024 and is projected to log a 20.6% CAGR through 2030.

Global Carbon Fiber Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerospace and defense advancements | +4.2% | North America, Europe | Medium term (2-4 years) |

| Wind-energy blade expansion | +3.8% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Hydrogen and CNG pressure vessels | +2.5% | Europe, Asia-Pacific, Global OEM roll-out | Long term (≥4 years) |

| EV battery enclosures and BIW lightweighting | +3.9% | Asia-Pacific, Europe | Medium term (2-4 years) |

| Carbon-fiber rebars in seismic construction | +1.8% | China, Japan, India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Recent Advancements in Aerospace and Defense

Boeing 787, Airbus A350, and new space platforms depend heavily on carbon composites, which have pushed major suppliers to ramp up capacity. Hexcel posted 17.2% growth in its commercial-aerospace revenue in 2024 as lightweight parts replaced aluminum skins. Complementing established prepregs, Massachusetts Institute of Technology researchers introduced “nanostitching,” embedding carbon nanotubes between laminate layers to boost toughness by 62% and curb delamination, which can lengthen service life while lowering lifecycle cost. Ceramic-matrix composites capable of 1,500 °C, bio-derived fibers that cut aviation CO₂, and rapid-cure thermosets are widening performance envelopes, underscoring how aerospace design upgrades raise the carbon fiber market ceiling.

Increasing Applications in Wind Energy

Longer blades enable higher-capacity turbines. Carbon spar caps deliver the stiffness needed for 100-meter rotors while holding weight down. In September 2024, Kineco Exel Composites India landed a contract to supply pultruded planks to Vestas, underscoring how blade makers lean on regional supply to support offshore growth. Europe’s build-out, China’s auctions, and United States tax credits favor carbon fiber structural parts, reinforcing the material’s role in the carbon fiber market.

Hydrogen and CNG High-Pressure Vessels in Commercial Vehicles

Toray projects carbon fiber demand for Type IV tanks to climb 42% a year and approach 40,000 tons by 2025 as truck OEMs pilot fuel-cell drivelines. Cryomotive’s cryo-compressed hydrogen tanks cut fiber use while raising storage density, which can temper raw-material bottlenecks yet still spur overall volume growth.

EV Battery-Pack Enclosures and BIW Lightweighting

Carbon fiber-reinforced plastic (CFRP) battery cases weigh up to 40% less than aluminum equivalents, lowering energy consumption by 4% for each 100 kg trimmed. Fraunhofer researchers built a multi-material housing 60% lighter than legacy steel, reducing embedded manufacturing emissions by 15%. Structural batteries that integrate storage and load paths promise up to 70% range gains in future EV platforms.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-intensive oxidation and carbonization | −2.7% | Global | Short term (≤2 years) |

| Supply-chain gaps for recycled carbon fiber | −1.9% | North America, Europe | Medium term (2-4 years) |

| High-performance thermoplastic substitution in sporting goods | −0.8% | North America, Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Energy-Intensive Oxidation and Carbonization

Conventional lines run above 1,000 °C for long dwell times, consuming vast power and locking in more than 40% of operating cost. Energy price swings squeeze margins and deter capacity adds. Microwave-assisted furnaces and alternative precursors could eventually resolve the bottleneck, yet large-scale retrofits remain capital-heavy.

Supply-Chain Security for Recycled Carbon Fiber

Less than 100,000 tons of annual recycling capacity stand against growing composite waste, exposing OEMs to landfill rules and supply risk. The U.S. Department of Homeland Security flagged advanced-materials dependence as a national vulnerability[1]Department of Homeland Security, “Threat of Limited U.S. Access to Critical Raw Materials,” dhs.gov . Toray’s capture of off-cuts from Boeing 787 wings into Lenovo laptops shows how closed-loop models can ease pressure, yet scale remains limited.

Segment Analysis

By Raw Material: PAN’s Scale Keeps Costs in Check

PAN-based grades held 95% of the carbon fiber market volume in 2024, backed by refined supply chains and known mechanical properties. They are projected to keep an 18.3% CAGR to 2030, even as producers test pitch and lignin options. Adding 0.075 wt% graphene lifted PAN tensile strength 225% and Young’s modulus 184% in lab trials, pointing to scope for incremental gains[2]Graphene Council, “Graphene Reinforced Carbon Fibers,” thegraphenecouncil.org. Pitch fibers claim the remaining share and are securing niches in satellites and high-rigidity shafts thanks to modulus advantages, which could widen automotive reach.

Sustained investment in precursor research and development points to a gradual shift where multiple feedstocks coexist. Yet PAN’s entrenched infrastructure, proven quality control, and broad certification base will safeguard its position through the decade. Cost relief from energy-efficient oxidation could allow producers to pass savings and defend their share against alternative high-performance plastics.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Fiber Type: Recycled Grades Narrow the Gap

Virgin material commanded 63% of the carbon fiber market volume in 2024. Performance consistency, aerospace qualification, and availability favor virgin output in safety-critical parts. However, advanced solvolysis now recovers up to 90% fiber strength at lower energy load, handing recycled grades a 19.5% CAGR, runway. Automotive, consumer electronics, and sporting goods are testing recycled fiber to lower embedded emissions and cut costs, and Toray’s Lenovo program illustrates mainstream appeal.

The carbon fiber market share advantage of virgin fibers will erode incrementally as OEMs integrate sustainability targets into sourcing. Scaling infrastructure, harmonizing waste regulations, and ensuring stable supply quality remain prerequisites for broader adoption. Specialized fibers with nano-pores, metal-like thermal conductivities, or other functional properties sit on the sidelines for now, yet can emerge as profit pools once volumes justify dedicated lines.

By Application: Composites Dominate; Micro-Electrodes Race Ahead

Composite materials accounted for 87% of the carbon fiber market demand in 2024. Aerospace panels, wind blades, pressure vessels, and EV battery shells anchor consistent pull. Automated fiber placement, 3D printing, and rapid-cure epoxy systems raise deposition speed and material yield, sustaining the carbon fiber market size for composites despite cost headwinds.

Micro-electrodes, although a comparatively small pool, are forecast to grow 25.02% annually to 2030. High surface area, conductivity, and corrosion resistance make carbon fibers attractive in sensors, medical devices, and supercapacitors. Structural batteries that embed anode-cathode layers directly into load paths exemplify how micro-scale electrode tech can feed back into macro-scale vehicle platforms. Textiles and catalytic substrates remain niche but steady, benefiting from continual process refinements.

By End-User Industry: Alternative Energy Holds the Lead

Alternative energy kept a 27% share in 2024. Offshore-class blades drove volume while hydrogen storage moved from pilot to early adoption. The carbon fiber market size tied to wind equipment is poised for sustained growth as longer rotors unlock a lower levelized cost of electricity.

Automotive trails but climbs steadily, fueled by EV lightweighting mandates. Construction applications such as CFRP rebars in seismic zones carve a slow but strategic beachhead. The diverse “others” bucket, including consumer electronics and industrial filtration, is on track for the fastest 25% CAGR, reflecting carbon fiber’s reputation as a problem-solving material where strength, weight, and corrosion resistance intersect.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific controlled 44.3% of the carbon fiber market in 2024 and should keep the fastest trajectory with a 20.6% CAGR to 2030. Japanese incumbents Toray and Mitsubishi Chemical sustain global leadership through captive PAN lines and steady innovation. Chinese producers are scaling aggressively and benefit from national energy transition programs.

North America retains a strong aviation hub and is expanding hydrogen-truck trials. Hexcel’s aerospace backlog and emerging Department of Energy support for clean materials consolidate the region’s position. Europe benefits from offshore wind, luxury autos, and regulatory pushes that reward low-carbon production; Brussels’ debate over composite waste could, however, add compliance hurdles for imported parts.

South America and the Middle East, and Africa account for modest volumes yet offer upside. Brazil leverages wind resources and infrastructure buildouts.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The top five suppliers held a major share of the installed capacity in 2024, indicating high concentration. Cost-innovation race continues. SGL unveiled a climate-friendly fiber line that can emit 50% less CO₂, catering to automotive and wind OEMs seeking low-carbon inputs. University-industry collaborations on bitumen, lignin, and recycled feedstocks aim to disrupt cost curves. Partnerships between resins, sizing specialists, and fiber makers underscore vertical cooperation as producers chase specialized growth pockets.

Carbon Fiber Industry Leaders

-

Hexcel Corporation

-

Mitsubishi Chemical Group Corporation

-

SGL Carbon

-

Teijin Limited

-

TORAY INDUSTRIES, INC.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Bodo Möller Chemie partnered with DowAksa to distribute carbon fiber products, expanding the chemical distributor’s high-performance composite portfolio.

- October 2023: TORAY INDUSTRIES, INC., announced plans to expand French subsidiary Toray Carbon Fibers Europe S.A.’s production facilities for regular tow medium- and high-modulus carbon fibers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global carbon fiber market as the sale of continuous, semi-continuous, and chopped fibers produced from polyacrylonitrile, pitch, or rayon precursors that possess a minimum tensile strength of 3 GPa and are delivered in raw fiber form to converters or captive composite lines. Outputs are tracked in kilotons at factory gate and tied to equivalent invoice revenues where available.

Scope Exclusions: Finished composite parts (e.g., bicycle frames, pressure vessels) and activated-carbon cloth are kept outside this baseline.

Segmentation Overview

- By Raw Material

- Polyacrylonitrile (PAN)

- Petroleum Pitch and Rayon

- By Fiber Type

- Virgin Carbon Fiber (VCF)

- Recycled Carbon Fiber (RCF)

- Others

- By Application

- Composite Materials

- Textiles

- Micro-Electrodes

- Catalysis

- By End-User Industry

- Aerospace and Defense

- Alternative Energy

- Automotive

- Construction and Infrastructure

- Sporting Goods

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview fiber producers, converters, and wind-blade OEMs in North America, Europe, China, and the Gulf, followed by structured surveys of composite distributors and pressure-vessel winders. These conversations validate real operating rates, precursor transfer prices, and region-specific demand pivots that seldom surface in filings.

Desk Research

We begin with public-domain production and trade statistics issued by UN Comtrade, Eurostat Comext, and Korea Customs, which let us map precursor flows and export-grade tow. Industry bodies such as JEC Group, the Japan Carbon Fiber Manufacturers Association, and the American Composites Manufacturers Association supply capacity expansions and utilization alerts. Cost drivers are benchmarked through quarterly energy indices from the U.S. EIA and China National Bureau of Statistics, while patent trends are scraped from Questel to flag new low-cost stabilization methods. Company 10-Ks and investor decks then help our team link stated nameplate tonnage to realized shipments. Select paywalled inputs, Dow Jones Factiva for deal flow and D&B Hoovers for plant-level revenue splits, round out the desk effort. This list is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down build starts from observed precursor consumption and trade, back-calculating finished fiber output after yield factors, which is then reconciled with demand-pool estimates drawn from aircraft deliveries, MW of installed wind capacity, and BEV production. Select bottom-up checks, supplier roll-ups at large tow lines and sampled ASP x volume invoices, tighten the bands. Key variables tracked include: - PAN spot price spread to acrylonitrile - Wind-turbine blade average length additions per year - Narrow-body aircraft build-rate guidance - Regional hydrogen storage tank orders - Scrap-generation ratios feeding recycled fiber uptake

A multivariate regression with ARIMA residual correction projects each driver toward 2030, and scenario analysis adjusts for precursor energy shocks. Gaps in bottom-up estimates (e.g., new Chinese lines ramping mid-year) are bridged by weighted moving averages of adjacent quarters.

Data Validation & Update Cycle

Outputs pass a four-level review: automated anomaly flags, peer cross-check, senior analyst sign-off, and an external expert callback when +/-5% variances emerge. The model refreshes annually; material events, like a force-majeure shutdown, trigger interim revisions before client delivery.

Why Our Carbon Fiber Baseline Commands Reliability

Published figures often diverge because some firms bundle downstream composites, convert at assumed ASPs, or lock forecasts to single-region growth spurts.

By anchoring on physically measured fiber tonnage and reconciling it with verified precursor flows, Mordor Intelligence avoids double counting and currency-conversion skews that inflate USD values when resin inflation spikes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 207.64 kilotons (2025) | Mordor Intelligence | |

| USD 4.82 bn (2025) | Global Consultancy A | Bundles prepregs & compounds; excludes recycled fiber streams |

| USD 6.37 bn (2025) | Trade Journal B | Merges carbon fiber with CFRP part revenues, lifting totals |

| USD 3.12 bn (2025) | Industry Tracker C | Covers only PAN small-tow and omits Latin America, understating size |

These contrasts show that, while others either broaden or narrow scope, our volume-first, dual-check process offers decision-makers a balanced, transparent baseline they can trace back to clear variables and repeat with confidence.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the carbon fiber market and its growth outlook?

The carbon fiber market measures 207.64 kilotons in 2024 and is projected to reach 402.93 kilotons by 2030, reflecting an 18.10% CAGR.

Which region leads the carbon fiber market?

Asia-Pacific holds 44.3% share and is also the fastest-growing region with a 20.6% CAGR through 2030.

Why is PAN still the dominant precursor?

PAN offers mature supply chains, consistent mechanical properties, and certification pedigree, giving it 95% volume share even as pitch and bio-based routes evolve.

How is recycled carbon fiber adoption progressing?

Recycled grades retain up to 90% original strength and are growing at a 19.5% CAGR, driven by sustainability targets and cost advantages.

Which applications are growing fastest?

Micro-electrodes and structural batteries are expanding the quickest at a forecast 25% CAGR due to demand in energy storage and advanced sensors.

Page last updated on: