Carbon Composites Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Volume (2025) | 238.48 kilotons |

| Market Volume (2030) | 343.33 kilotons |

| Growth Rate (2025 - 2030) | 7.56% CAGR |

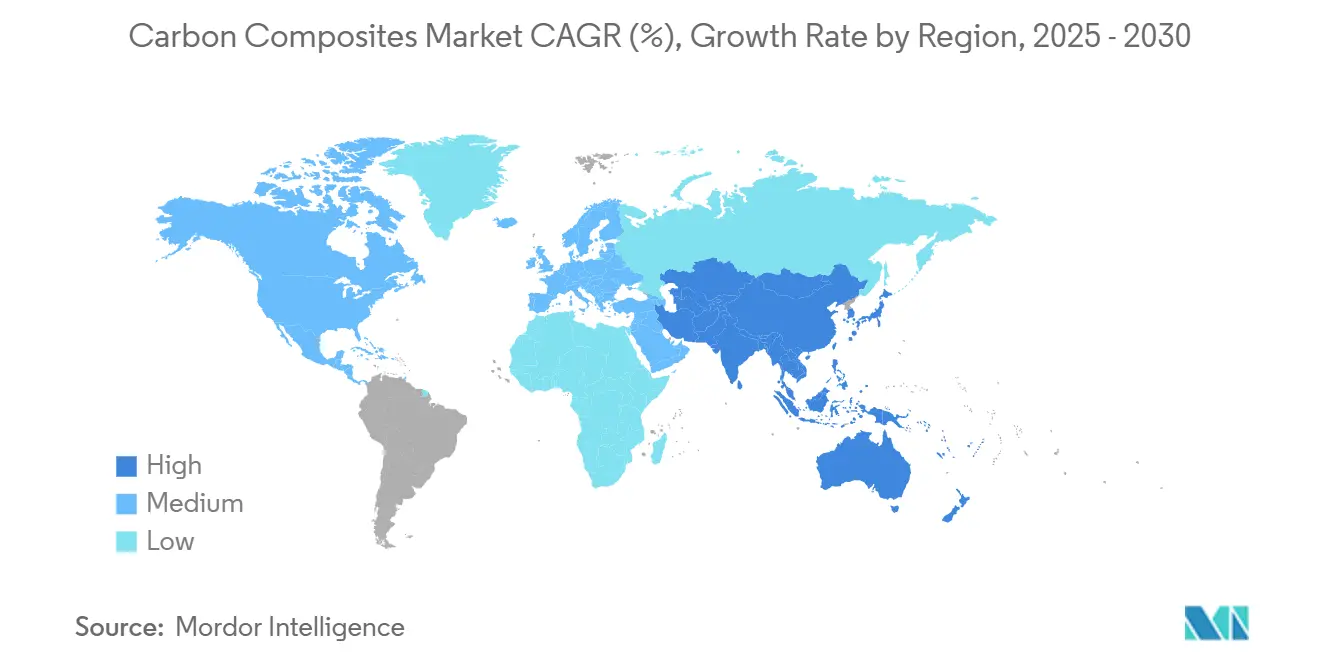

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Carbon Composites Market Analysis by Mordor Intelligence

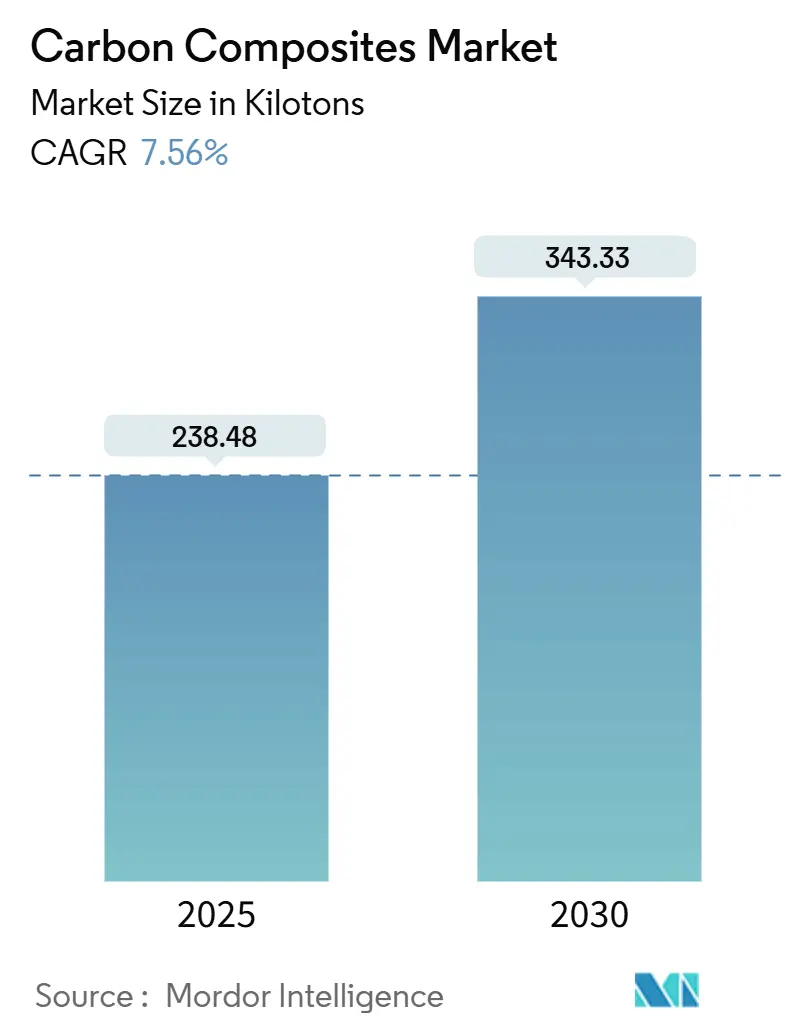

The Carbon Composites Market size is estimated at 238.48 kilotons in 2025, and is expected to reach 343.33 kilotons by 2030, at a CAGR of 7.56% during the forecast period (2025-2030). Manufacturers are accelerating the substitution of metals with lightweight carbon composites to meet fuel-economy and emissions goals, helped by a decline in large-tow fiber pricing below USD 20 per kilogram, which opens the door to higher-volume automotive and wind-turbine parts. Aerospace demand stays robust, yet wind-energy blade upsizing and electric-vehicle (EV) range-extension targets have emerged as faster-growing catalysts. On the supply side, Chinese producers have lifted global capacity by almost 30% since 2024, tilting the cost curve and prompting Western incumbents to defend high-margin aerospace niches through certification advantages. Process innovation, notably high-pressure resin transfer molding (HP-RTM), now delivers sub-five-minute cycles that move composites into annual runs beyond 200,000 parts, a decisive threshold for mainstream automotive adoption.

Key Report Takeaways

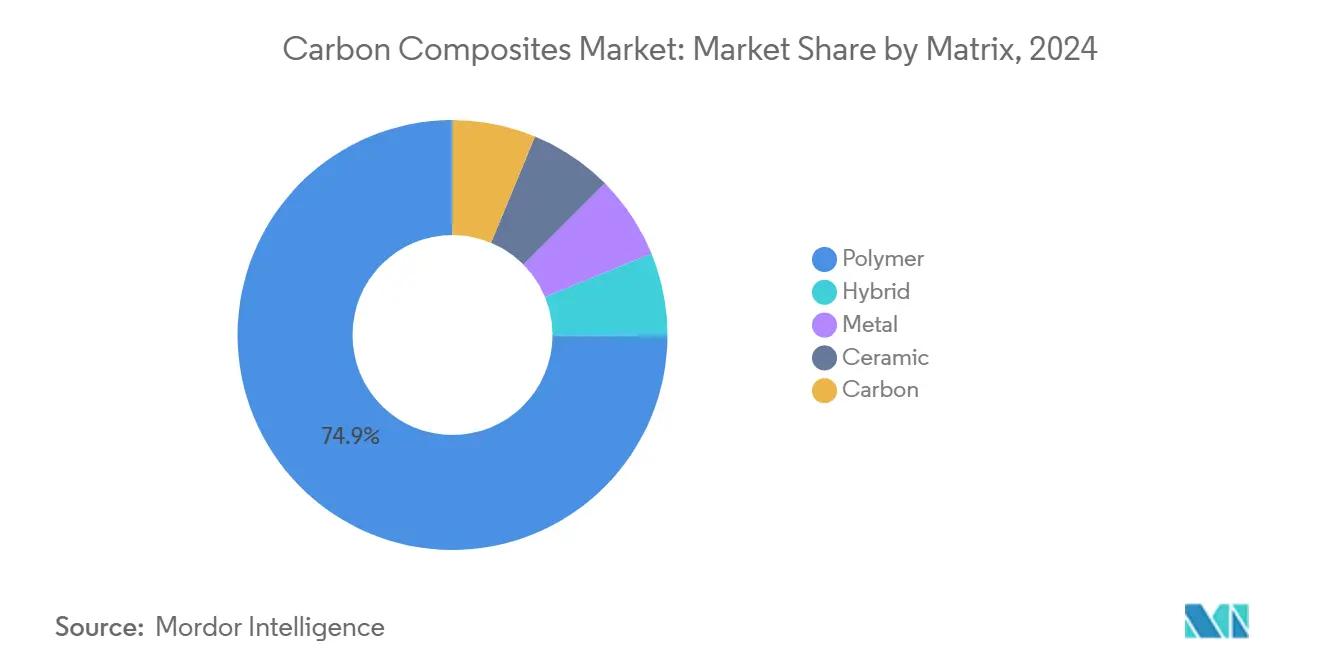

- By matrix, polymer had the largest market share of 74.92% in 2024. Polymer's market share is also expected to increase at a CAGR of 8.67% during the forecast period (2025-2030).

- By process, press and injection processes had the largest share of 33.15% in 2024, and this is expected to grow at a CAGR of 8.12% during the forecast period (2025-2030).

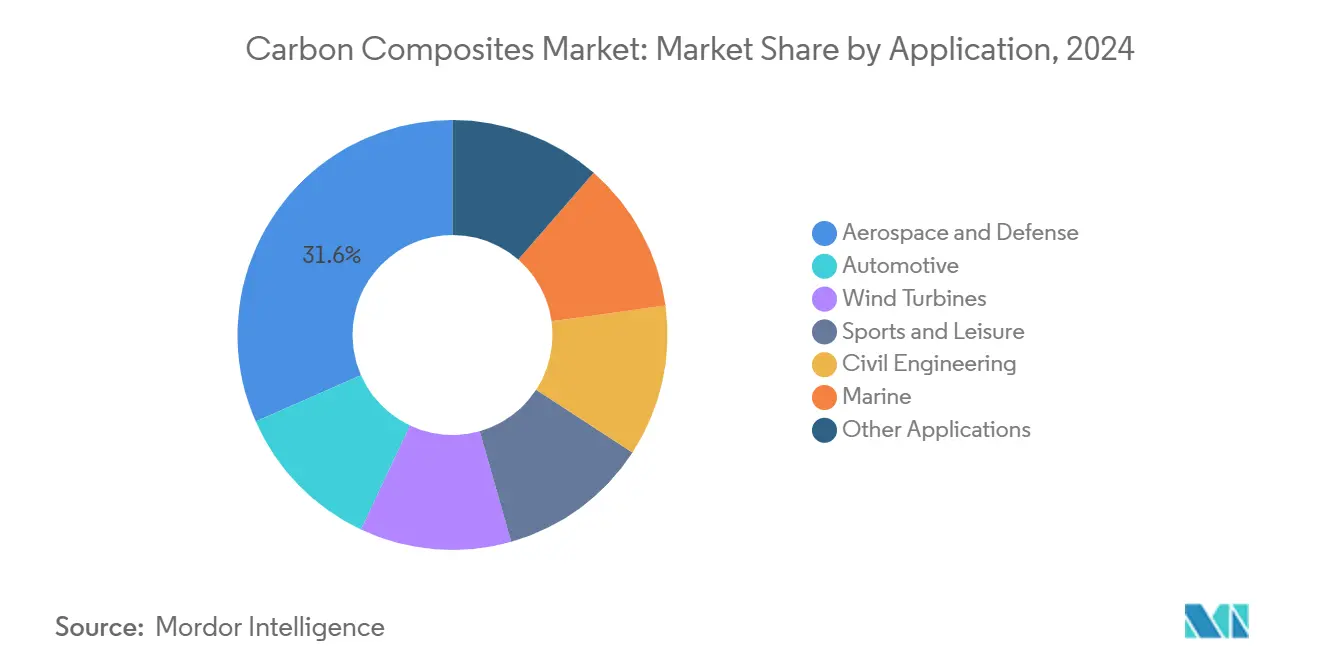

- By application, aerospace and defense had the largest share of 31.59% in 2024, while the share of wind turbines is expected to grow with a CAGR of 8.27% during the forecast period (2025-2030).

- By geography, the Asia Pacific had the largest market share of 38.64% in 2024, and this is expected to increase at a CAGR of 8.48% during the forecast period (2025-2030).

Global Carbon Composites Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerospace lightweighting boom | +1.8% | North America and Europe | Long term (≥ 4 years) |

| EV range-extension requirements | +1.5% | Asia-Pacific core; spill-over to North America and Europe | Medium term (2–4 years) |

| Wind-turbine blade length upsizing | +1.4% | Europe and Asia-Pacific coastal markets; emerging Middle East | Long term (≥ 4 years) |

| Chinese large-tow capacity expansion | +1.2% | Global supply impact, strongest in Asia-Pacific | Short term (≤ 2 years) |

| Carbon-composite H₂ pressure vessels | +0.9% | Europe, Japan, South Korea, California | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Aerospace Lightweighting Boom

Composite content on Boeing 787 and Airbus A350 exceeds 50% by weight, trimming airframe mass by 20% and lowering fuel burn 15%, a benchmark that next-generation single-aisle jets aim to replicate. Thermoplastic fuselage demonstrators reduce production time by 40% and enable field repairs with simple heat sources, driving demand for higher-throughput automated fiber placement (AFP) lines. Regulatory acceptance has broadened as the FAA now recognizes AFP for primary aerostructures, easing adoption barriers. With wide-body output plateauing, narrow-body successors that specify 30–35% composites still drive the carbon composites market upward. The driver’s influence is strongest in North America and Europe, where certification infrastructure is mature.

EV Range-Extension Requirements

Every 100 kg shaved from an EV boosts driving range by roughly 10 km, placing lightweighting on par with battery chemistry advances[1]Chalmers University, “Structural Battery Breakthrough,” chalmers.se. Carbon-fiber battery enclosures and body panels, therefore, rank high on automaker bills of material. Chinese brands integrate thermoplastic carbon composites into seat frames and door interiors, while U.S. and European OEMs focus on prepreg for stiffness-critical underbody shields. HP-RTM consistently delivers part costs within 20% of those for steel stampings at volumes exceeding 50,000 units, validating composites for mid-segment vehicles. Pending 2025 fleet CO₂ targets in Europe cement the demand outlook. The Asia-Pacific region remains the epicenter, yet the spill-over is accelerating in North America and Europe.

Wind-Turbine Blade Length Upsizing

Offshore turbines now ship with blades beyond 115 m, and prototypes stretch to 143 m, scales that mandate carbon-fiber spar caps to limit tip deflection under extreme gusts[2]Vestas, “V236 Technical Datasheet,” vestas.com. Hybrid carbon-glass layups increase the carbon content per blade from 3% in 2020 to 8% in 2024, adding approximately 1.2 tons of fiber per unit. Europe’s REPowerEU initiative aims to achieve 480 GW of installed wind capacity by 2030, further reinforcing the demand surge. Thermoplastic roots and trailing edges simplify welding and enable end-of-life recycling, aligning with circular-economy directives. These dynamics position wind as the fastest-growing application in the carbon composites market through 2030.

Rapid Expansion of Chinese Large-Tow CF Capacity

Sinopec’s 2024 commissioning of a 30,000 t line dropped 50K to spot prices 45% to USD 18 kg, swinging cost advantages decisively toward composites in price-sensitive sectors. Domestic demand accounts for only 60% of China’s output, prompting aggressive export campaigns that depress global pricing. Western and Japanese suppliers defend aerospace grades via AS9100 credentials, yet large-tow commodity grades are now effectively a Chinese export. The supply shock is expected to reverberate worldwide, particularly in Asia and emerging markets, over the next two years.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High comparative manufacturing cost | -1.1% | Global; acute in automotive and civil engineering | Medium term (2–4 years) |

| Aluminum-lithium and advanced steel substitutes | -0.7% | Aerospace and automotive in North America and Europe | Long term (≥ 4 years) |

| Autoclave bottlenecks for wide-body aircraft | -0.5% | North America and Europe aerospace supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Comparative Manufacturing Cost

Aerospace-grade prepreg sells at USD 40–60 kg, which is 2–3 times the cost of aluminum-lithium, while autoclave processing adds USD 200–300 m², curbing uptake outside weight-critical parts. Automotive economics improve only when HP-RTM cycle times drop below five minutes and annual volumes exceed 50,000 units. Labor still accounts for up to 45% of hand-layup cost, making automation the decisive lever. Out-of-autoclave and thermoplastic press-forming reduce energy and cycle times; however, certification delays slow the aerospace transition. Civil engineering uses lag because composite rebar costs quadruple steel. Until material prices fall below USD 15 kg, cost pressure will moderate market growth.

Aluminum-Lithium and Advanced Steel Substitutes

Airbus’s 2099 Al-Li alloy delivers a 10% weight reduction at one-third the cost of composite material, enabling riveted assembly that fits existing lines. Automotive OEMs deploy press-hardened steels with a tensile strength of 1,500 MPa at USD 2–3 kg, eroding the value proposition of composites in crash-critical zones. Weight-optimized metals now capture secondary structures that once eyed carbon fiber. Continuous alloy advances—density cuts and strength gains—could further narrow the cost-to-benefit gap through 2030, especially in Europe and North America, where fabrication expertise is well-established.

Segment Analysis

By Matrix: Thermoplastic Variants Reshape Automotive Economics

Thermoplastic polymer matrices represented 74.92% of 2024 shipments and are forecast to outpace the broader carbon composites market at an 8.67% CAGR through 2030, reflecting a decisive pivot away from slow-curing epoxies. Early adopters, such as BMW, leveraged PEEK and PPS to press-form passenger-cell structures in under three minutes, keeping part costs within 25% of those of steel and validating composites for 50,000-unit annual programs. Thermoset epoxy retains its primacy in aerospace and wind applications, where thick sections are required and high glass-transition temperatures are mandatory. Ceramic and metal matrices stay niche at <2% volume because material costs exceed USD 300 kg. Hybrid resin systems that combine the workability of thermosets with the toughness of thermoplastics are now being used in A350 wing ribs, adding 20% compression-after-impact strength without requiring retooling. Thermoplastic penetration, however, hinges on scaling PEEK supply and tooling rated to 400°C. Recycling economics favor thermoplastics, recovering up to 85% of material value, a critical advantage as EU circular-economy rules tighten from 2028.

Material price gaps persist. PEEK runs USD 80–100 kg, quadruple epoxy, and demands heated metal tools costing USD 3–5 million per line. Yet as Chinese resin suppliers expand, PEEK prices are expected to fall toward USD 60 kg by 2027, accelerating thermoplastic adoption in battery enclosures and H₂ tanks. Syensqo’s 60% bio-based epoxy launched in 2024 provides an alternative pathway by lowering Scope 3 emissions for aerospace customers without changing cure infrastructure. The interplay of cost, cycle time, and recyclability will dictate matrix selection and steer growth across automotive, hydrogen, and consumer end uses, keeping the carbon composites market dynamic through the decade.

Note: Segment shares of all individual segments available upon report purchase

By Process: Press Molding Scales Automotive Volumes

Press and injection technologies controlled 33.15% of the carbon composites market size in 2024 and are poised to expand at an 8.12% CAGR, underpinned by HP-RTM’s ability to combine 55–60% fiber volume fraction with cycle times under five minutes. HP-RTM injects resin at pressures of up to 150 bar into closed molds, achieving tolerances of ±0.2 mm that match those of aerospace prepreg, yet at one-third the material cost. Compression-molded sheet molding compound serves semi-structural parts, such as seat frames, where chopped fiber is sufficient. Prepreg lay-up remains indispensable for primary aerostructures; however, its 8- to 12-hour autoclave cure time limits volume scalability. Pultrusion and filament winding deliver the lowest cost per kilogram for constant-section profiles and pressure vessels, and they are poised to ride the hydrogen storage wave at a 6.8% CAGR. Automated fiber placement and tape laying occupy just 12% of the volume yet command strategic focus; Boeing’s 777X wing skin shows a 70% reduction in lay-up time after AFP adoption. Equipment costs of USD 10–15 million per cell restrain diffusion, but falling unit prices and higher labor-saving offsets will widen adoption after 2027.

Other advanced processes, such as additive manufacturing and in-situ consolidation, could disrupt further. Continuous-fiber 3D printing now achieves 60% fiber fraction and near-net-shape parts, although build rates remain comparatively slow. As tool-less methods mature, small-lot aerospace spares and complex EV brackets will shift away from prepreg, supporting a diversified processing landscape and sustaining the carbon composites market share of automated routes.

By Application: Wind Turbines Outpace Aerospace Growth

Aerospace and defense consumed 31.59% of the carbon composites market volume in 2024, but wind turbines are set to eclipse all segments with an 8.27% CAGR, spurred by offshore installations that demand carbon-fiber spar caps for 115–150 m blades. Each 15 MW blade now uses approximately 1.2 tons of carbon fiber, a fourfold increase since 2020, driving annual demand growth above 25,000 tons worldwide. Boeing and Airbus account for roughly 6,500 t combined today, rising modestly as single-aisle successors debut in the late decade. Defense programs—including the F-35 and Next-Generation Air Dominance aircraft—add 3,000 tons annually and grow at a rate of 6.5%, driven by the need for stealth and high-temperature capabilities. Automotive ranks third in growth, with a 7.9% CAGR, as EVs pursue weight offsets; yet, penetration remains concentrated in premium models due to options costing USD 5,000 or more. Sports gear, marine craft, and civil infrastructure collectively provide steady mid-single-digit growth, ensuring diversified demand and guarding against the cyclicality of the aerospace sector.

Wind’s rapid ascent reshapes raw-material and process priorities. Large-tow fiber dominates spar-cap supply because modulus targets can be met without expensive small-tow grades. Hybrid carbon-glass shells optimize cost while meeting stiffness metrics, and thermoplastic trailing edges promise 30% assembly-time cuts. Regional blade plants in China, Europe, and the United States localize production to bypass logistics constraints on 100-plus-meter components. Together these trends accelerate carbon composites market penetration into renewable-energy hardware and dilute over-reliance on aerospace cycles.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The Asia-Pacific region accounted for 38.64% of the 2024 carbon composites market volume and is projected to log an 8.48% CAGR, driven by the expansion of the wind, EV, and hydrogen sectors. Japan remains the technology leader, with Toray supplying 60% of aerospace-qualified prepreg. South Korea’s Hyosung targets cost parity with Chinese fibers by 2026, while India grows at the fastest rate of 9.2% driven by wind-energy and defense offsets. ASEAN nations are emerging as fabrication hubs, importing prepreg from Japan and South Korea and exporting parts at a 30% lower landed cost to Western buyers.

North America held a significant portion of global shipments in 2024, underpinned by the combined pull of Boeing, Spirit AeroSystems, and Lockheed Martin, which accounted for approximately 8,500 tons annually. Hexcel and Solvay control 70% of aerospace prepreg capacity across Utah, Kansas, and Alabama. Automotive uptake lags behind Europe due to lower fuel prices, yet Tesla’s Cybertruck and structural battery packs could potentially pivot volumes if fiber prices fall below USD 15 kg. Canada’s wind build and Mexico’s aerospace assemblies add incremental demand but remain reliant on U.S. and Japanese fiber imports.

Europe’s market volume in 2024, fueled by CAFE targets of 95 g CO₂ km fleet average and REPowerEU’s 480 GW wind capacity goal. Germany’s premium automakers pull 3,500 t annually for battery trays and driveline tubes, while SGL Carbon’s 9,000 t plant focuses on large-tow fiber for automotive and wind. Brexit-driven trade friction has nudged some U.K. aerospace work to Poland. Spain’s blade plants double carbon-fiber consumption by 2028 on 15 MW turbine rollouts. Eastern Europe rises as a cost-competitive fabrication base, reflecting the region’s balanced growth trajectory.

Competitive Landscape

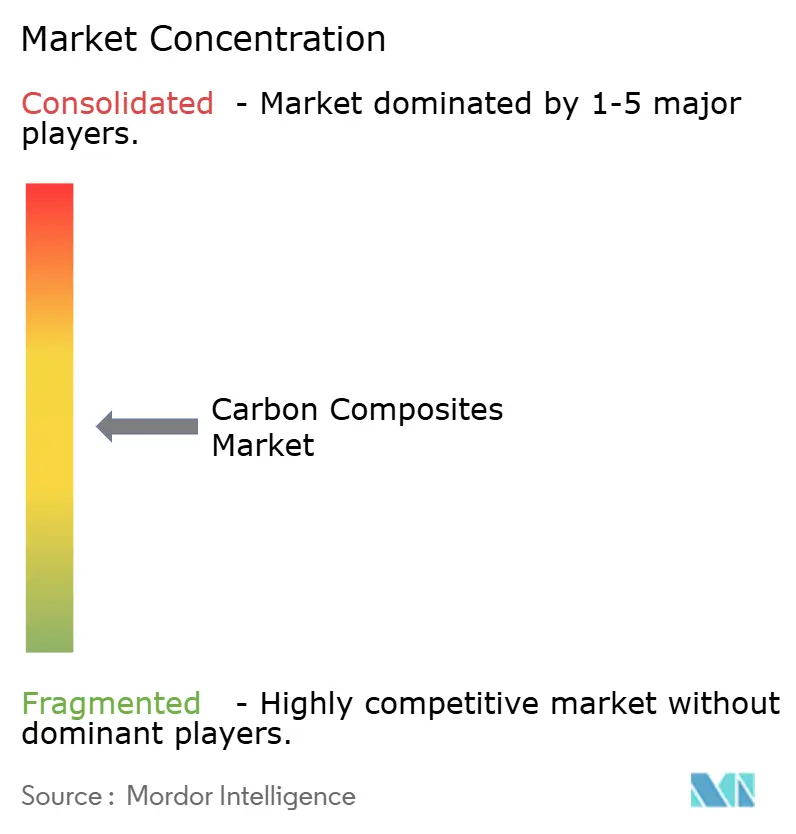

The Carbon Composites Market is moderately consolidated. Incumbents rely on AS9100 and NADCAP qualifications that wall off 70% of aerospace revenue from low-cost rivals. Strategy bifurcates: Western and Japanese firms invest in high-modulus, small-tow lines and downstream AFP integrations, whereas Chinese entrants flood the market with commodity, large-tow fiber across Asia, India, and the Middle East. The technology race is pointing toward bio-based resins and thermoplastic matrices that meet EU circular economy mandates without sacrificing mechanical properties. Electroimpact and Arkema exemplify disruptive automation and material substitution, respectively, compressing lay-up labor by 50% and enabling room-temperature infusion.

Carbon Composites Industry Leaders

-

TORAY INDUSTRIES, INC.

-

Hexcel Corporation

-

Mitsubishi Chemical Group Corporation

-

SGL Carbon

-

Teijin Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Toray Advanced Composites has acquired assets, technology, and intellectual property from Gordon Plastics. This strategic acquisition enhances TAC's capabilities in the development, testing, and production of continuous fiber-reinforced thermoplastic composite unidirectional (UD) tapes and higher-melting-temperature polymer systems.

- February 2024: Syensqo partnered with Trillium to deliver sustainable solutions that enable customers to achieve their environmental objectives. Through this collaboration, Syensqo emphasizes the creation of sustainable raw materials tailored for carbon fiber applications. Syensqo and Trillium expect to further advance towards fully bio-based carbon fiber composites.

- February 2024: Schiebel, a manufacturer of unmanned air systems, partnered with Syensqo as its advanced material supplier. Syensqo's carbon fiber composite materials, integrated with titanium on the fuselage of Schiebel's CAMCOPTER S-100 UAS, enable diverse payload and endurance configurations. The CAMCOPTER S-100 UAS is actively utilized in both defense and civil sectors.

Global Carbon Composites Market Report Scope

Carbon composites are composite materials with carbon fiber reinforcements. Carbon composites usually comprise 80%–90% carbon and graphite. The unique blend of natural and synthetic graphite particles, carbon fibers, and amorphous carbon particles is proprietary and tailored for specific desired properties.

The carbon composites market is segmented by matrix, process, application, and geography. By matrix, the market is segmented into hybrid, metal, ceramic, carbon, and polymer. By process, the market is segmented into prepreg layup process, pultrusion, wet lamination and infusion process, press and injection processes, and others (3D printing). By application, the market is segmented into aerospace and defense, automotive, wind turbines, sport and leisure, civil engineering, marine applications, and other applications (electronics, medical applications, protective clothing, and pressure vessels). The report also covers the market size and forecasts for carbon composites in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kilotons).

| Hybrid | |

| Metal | |

| Ceramic | |

| Carbon | |

| Polymer | Thermosetting |

| Thermoplastic |

| Prepreg Lay-up |

| Pultrusion and Winding |

| Wet Lamination and Infusion |

| Press and Injection Processes |

| Other Processes |

| Aerospace and Defense |

| Automotive |

| Wind Turbines |

| Sports and Leisure |

| Civil Engineering |

| Marine |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Matrix | Hybrid | |

| Metal | ||

| Ceramic | ||

| Carbon | ||

| Polymer | Thermosetting | |

| Thermoplastic | ||

| By Process | Prepreg Lay-up | |

| Pultrusion and Winding | ||

| Wet Lamination and Infusion | ||

| Press and Injection Processes | ||

| Other Processes | ||

| By Application | Aerospace and Defense | |

| Automotive | ||

| Wind Turbines | ||

| Sports and Leisure | ||

| Civil Engineering | ||

| Marine | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What volume will global carbon composites demand reach by 2030?

The market size is expected to climb from 238.48 kilotons in 2025 to 343.33 kilotons by 2030 on a 7.56% CAGR led by wind-energy and EV demand.

Which end-use will add the most new demand through 2030?

Wind-turbine blades are set to expand at an 8.27% CAGR as blade lengths exceed 115 m and carbon spar caps become mandatory.

Why are thermoplastic matrices gaining share in automotive parts?

They allow sub-five-minute press-forming cycles, enable welded assembly, and improve recyclability, which together cut lifecycle cost despite higher resin prices.

How are Chinese producers disrupting global supply?

Large-tow capacity additions have pushed 50K tow prices down to USD 18 kg, giving Chinese exporters a 30–40% cost edge in wind and automotive grades.

Which process is scaling fastest for high-volume parts?

HP-RTM combines 55–60% fiber content with sub-five-minute cycles and is on track to grow 8.12% CAGR, making it the preferred route for 200,000-unit automotive runs.

Page last updated on: