| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 2.76 Billion |

| Market Size (2030) | USD 5.37 Billion |

| CAGR (2025 - 2030) | 14.21 % |

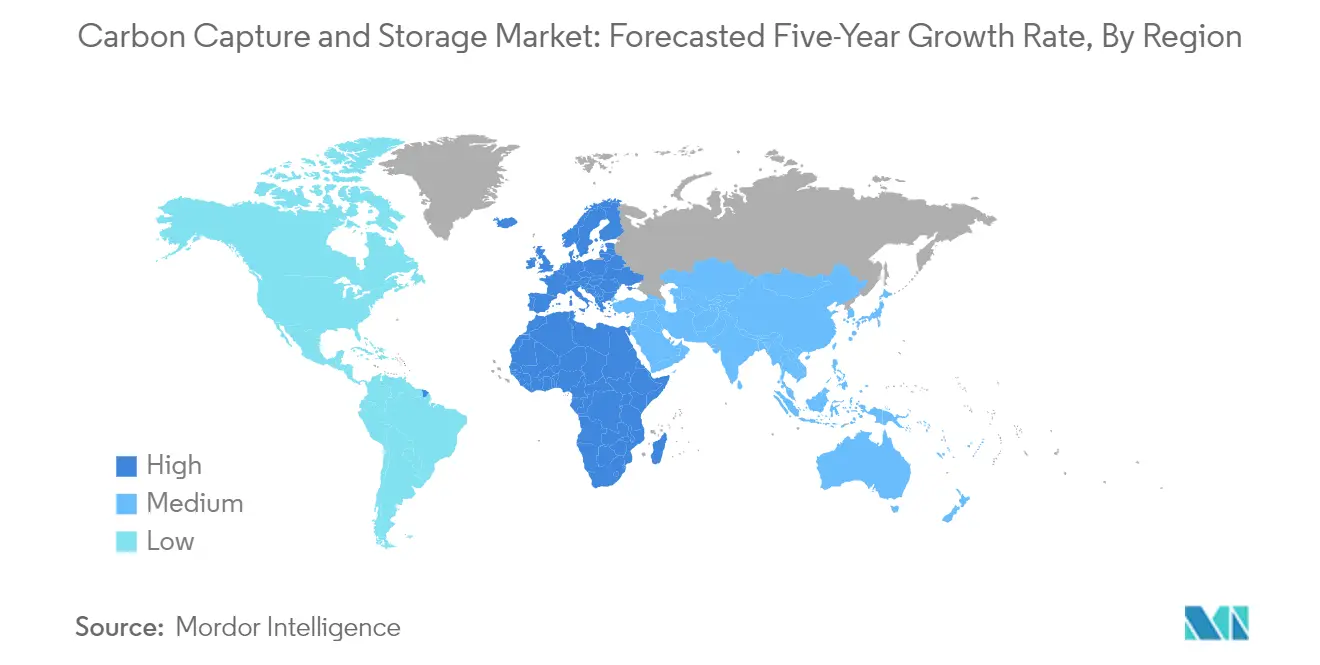

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Carbon Capture And Storage Market Analysis

The Carbon Capture And Storage Market size is estimated at USD 2.76 billion in 2025, and is expected to reach USD 5.37 billion by 2030, at a CAGR of 14.21% during the forecast period (2025-2030).

The carbon capture and storage industry is experiencing rapid technological advancement and infrastructure development as organizations worldwide intensify their decarbonization efforts. According to the International Energy Agency (IEA), global energy-related CO2 emissions grew by 0.9% in 2022, reaching a new high of 36.8 gigatons, highlighting the urgent need for carbon capture solutions. The industry is witnessing increased collaboration between technology providers, energy companies, and industrial manufacturers to develop and implement more efficient capture technologies. Major energy companies are particularly focused on developing integrated CCS networks that can serve multiple industrial clusters, optimizing infrastructure utilization and reducing overall implementation costs.

The market landscape is characterized by significant project pipeline expansion and growing commercial deployment of CCS technologies across various industrial sectors. As of 2023, there are 41 commercial-scale CCS facilities in operation globally, with 26 facilities under construction and 325 in various stages of development. This substantial project pipeline demonstrates the increasing commercial viability and industry confidence in CCS technology. The industry is also witnessing innovation in capture technologies, with companies developing more energy-efficient and cost-effective solutions for both new installations and retrofit applications.

The integration of CCS with renewable energy projects is emerging as a significant trend, particularly in the power generation sector. Companies are increasingly exploring hybrid solutions that combine CCS with biomass power generation, solar, and wind energy to achieve negative emissions. This integration is driving innovation in capture technologies and storage solutions, with particular emphasis on developing more efficient and scalable systems. The industry is also seeing growing interest in direct air capture technologies, with several commercial-scale projects being planned or implemented globally.

The market is experiencing a shift toward larger-scale projects and the development of industrial CCS hubs. The world's largest operating CCS facility, the Petrobras Santos Basin Pre-Salt Oil Field CCS facility, demonstrates the scalability of these technologies with its capture capacity of 10.6 Mtpa of CO2. Industrial clusters are increasingly being developed to share infrastructure and reduce costs, particularly in regions with suitable geological storage capacity. These hubs are enabling smaller industrial facilities to access CCS infrastructure that would otherwise be economically unfeasible, while also optimizing transportation and storage solutions through shared infrastructure and economies of scale.

Carbon Capture And Storage Market Trends

Emerging Demand for CO2 Injection Technique for Enhanced Oil Recovery (EOR)

The oil and gas industry has witnessed a significant surge in the adoption of CO2 injection techniques for Enhanced Oil Recovery (EOR), driven by both environmental and economic benefits. When carbon dioxide is injected into an oilfield, it creates a dual advantage—it can mix with crude oil, causing it to swell and reduce viscosity while also maintaining or increasing reservoir pressure, ultimately enabling more efficient oil extraction from mature fields. This technique has proven particularly successful in regions like Texas, United States, where EOR operations account for over 20% of total oil production, with some fields achieving remarkable recovery rates of nearly 70%, demonstrating the technique's effectiveness in maximizing oil recovery from existing reserves.

The industry's commitment to CO2-EOR is evidenced by several major projects launched in 2023. For instance, in September 2023, ADNOC finalized a deal to build a carbon capture and storage project in the UAE's Habshan oil and gas field, extending the company's existing CCS operations at a steel plant. Similarly, in November 2023, Shell entered into a partnership with CNOOC to develop a CO2 EOR project in China, aiming to capture and store 10 million tons of CO2. These developments highlight the growing recognition of CO2-EOR as a viable solution for both enhanced oil recovery and environmental sustainability in the oil and gas sector.

Understand The Key Trends Shaping This Market

Download PDF

Strict Government Norms Towards GHG Emissions

Governments worldwide have intensified their regulatory frameworks and emission reduction targets, compelling industries to adopt carbon capture and storage technologies. According to the International Energy Agency (IEA), global energy-related CO2 emissions grew by 0.9% or 321 million tons in 2022, reaching a new high of 36.8 gigatons (Gt), highlighting the urgent need for stringent emission control measures. In response, governments have introduced various support mechanisms, such as Canada's establishment of a CAD 2.6 billion (approximately USD 1.9 billion) tax credit for carbon capture and storage projects in 2022, while Saskatchewan extended its 20% tax credit under the province's Oil Infrastructure Investment Program to pipelines carrying CO2.

The commitment to emission reduction is further demonstrated by significant policy developments in 2023. For instance, the US government allocated USD 12.1 billion for carbon management technologies through the Infrastructure Investments and Jobs Act, with USD 2.54 billion specifically designated for carbon capture and storage demonstration projects from 2022 to 2025. Similarly, Japan adopted the Green Transformation (GX) Basic Policy in February 2023, emphasizing the development of carbon capture and storage technologies, along with ammonia and hydrogen co-firing in the power sector. The European Union has also set ambitious legally binding targets to cut carbon emissions by at least 55% by 2030 compared to 1990 levels, with the European Parliament advocating for an even higher reduction target of 60%.

Segment Analysis: Technology

Pre-combustion Capture Segment in Carbon Capture and Storage Market

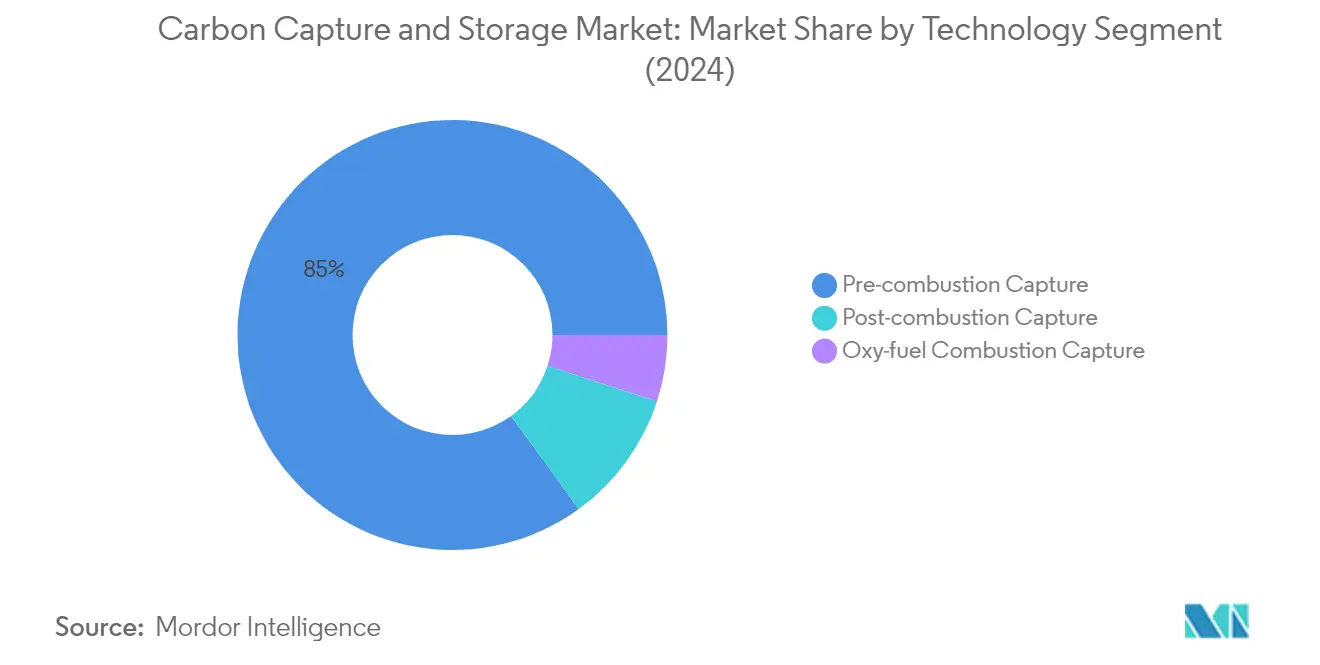

Pre-combustion capture technology dominates the global carbon capture and storage market, accounting for approximately 85% of the market share in 2024. This technology's dominance stems from its higher capture efficiencies and ability to produce high-purity hydrogen as a clean energy carrier. Pre-combustion capture separates carbon dioxide capture from gasification and reforming processes, yielding a mixture primarily consisting of hydrogen and carbon dioxide. The technology is particularly prevalent in integrated gasification combined cycle (IGCC) power plants, where carbon-based fuels are reacted with steam and oxygen under pressure to form syngas. The captured carbon dioxide can be utilized for enhanced oil recovery or stored permanently in geological formations, making it an attractive option for both environmental and economic benefits. The technology's widespread adoption is further supported by its established presence in refineries and chemical plants worldwide, where it is used not only for carbon capture but also for hydrogen production.

Post-combustion Capture Segment in Carbon Capture and Storage Market

The post-combustion capture segment is experiencing rapid growth in the carbon capture and storage market, driven by its versatility and applicability across various industries. This technology is particularly valuable as it can be retrofitted to existing facilities without requiring significant modifications to the original process, making it an attractive option for power plants and industrial facilities looking to reduce their carbon footprint. Post-combustion systems utilize liquid solvents to capture carbon dioxide from flue gases, typically capturing 3-15% by volume from nitrogen-rich streams. The technology's growth is further accelerated by continuous improvements in solvent technology and process optimization, leading to enhanced capture efficiency and reduced operational costs. The segment's expansion is also supported by increasing adoption in natural gas combined cycle plants and pulverized coal power plants, where monoethanolamine (MEA) and other advanced solvents are being deployed for carbon capture technology.

Remaining Segments in Technology

The oxy-fuel combustion capture segment represents a significant technological approach in the carbon capture and storage market, offering unique advantages in certain applications. This technology involves burning fossil fuels in an oxygen-rich environment, producing flue gases primarily composed of water vapor and carbon dioxide, which simplifies the separation process. The technology is particularly effective in boiler designs, where it can be configured in either low-temperature or high-temperature configurations to match specific operational requirements. Oxy-fuel combustion has found notable applications in welding and cutting of metals, especially steel, where it enables higher flame temperatures than traditional air-fuel flames. The technology continues to evolve with advanced designs and improved efficiency, contributing to the overall growth of the carbon capture and storage market.

Segment Analysis: End-user Industry

Oil and Gas Segment in Carbon Capture and Storage Market

The oil and gas sector dominates the global carbon capture and storage market, accounting for approximately 70% of the total market share in 2024. This significant market position is primarily driven by the extensive application of CO2 injection techniques for enhanced oil recovery (EOR) operations. The sector's leadership is further strengthened by the presence of major operational facilities like the Shute Creek gas processing plant in the United States and various projects in the Middle East. The implementation of carbon capture technology in this sector has been particularly notable in regions like the United States, Canada, and the Middle East, where large-scale projects have demonstrated successful integration of CCS technologies with existing oil and gas operations.

Chemical Segment in Carbon Capture and Storage Market

The chemical segment is projected to experience the most rapid growth in the carbon capture and storage market, with an expected growth rate of approximately 26% during the forecast period 2024-2029. This exceptional growth trajectory is driven by increasing environmental regulations and the chemical industry's commitment to reducing its carbon footprint. The segment's growth is particularly evident in regions like North America, where the chemical industry accounts for a significant portion of CCS operations. The expansion is further supported by technological advancements in carbon sequestration technology and the development of new chemical solvent technologies that enhance capture efficiency.

Remaining Segments in End-User Industry

The carbon capture and storage market encompasses several other significant segments, including coal and biomass power plants, iron and steel, and cement industries. The coal and biomass power plant sector is particularly noteworthy due to its potential for achieving negative emissions through BECCS (Bioenergy with Carbon Capture and Storage) technology. The iron and steel industry represents a crucial application area, especially in regions with significant steel production capabilities, while the cement sector is emerging as a promising segment due to its high CO2 emissions and increasing focus on sustainability measures. Each of these segments contributes uniquely to the market's dynamics, driven by sector-specific regulations and decarbonization goals.

Carbon Capture And Storage Market Geography Segment Analysis

Carbon Capture and Storage Market in Asia-Pacific

The Asia-Pacific region represents a dynamic carbon capture and storage market, with significant developments across China, India, Japan, and Australia. The region's growth is driven by ambitious climate goals, increasing industrial activities, and supportive government policies. China leads the regional market with substantial investments in CCS projects, particularly in the chemical and power generation sectors. India is rapidly developing its CCS capabilities through various public sector initiatives, while Japan continues to advance its technological expertise in carbon capture solutions. Australia has positioned itself as a key player with several large-scale CCS projects under development.

Carbon Capture and Storage Market in China

China dominates the Asia-Pacific CCS market with approximately 15% of the region's total CCS projects in 2024. The country has established itself as a leader in CCS technology implementation, particularly in the chemical industry and power stations. China's commitment to reaching carbon neutrality by 2060 has driven significant investments in CCS infrastructure. The nation has developed a comprehensive network of CCS facilities, with multiple projects in various stages of development, construction, and operation. The country's focus spans multiple sectors, including chemical production, power generation, and industrial applications, with particular emphasis on integrating CCS technologies into existing industrial facilities.

Carbon Capture and Storage Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 20% from 2024 to 2029. The country's carbon capture and storage industry is experiencing rapid transformation through various public sector initiatives and government support. India's geological storage potential for carbon dioxide, ranging from 500 to 1,000 gigatons, presents significant opportunities for market expansion. The country has established National Centres of Excellence in Carbon Capture and Utilization, demonstrating its commitment to advancing CCS technologies. Major public sector oil and gas companies are actively adopting emission reduction strategies, including CCS technologies, to align with the country's net-zero targets.

Carbon Capture and Storage Market in North America

North America stands as the global leader in carbon capture and storage technology implementation, with extensive developments across the United States, Canada, and Mexico. The region benefits from well-established infrastructure, strong government support, and significant private sector investments. The market is characterized by large-scale projects across various industries, including oil and gas, power generation, and chemical production. The region's leadership is reinforced by comprehensive regulatory frameworks, tax incentives, and extensive research and development activities in CCS technologies.

Carbon Capture and Storage Market in United States

The United States maintains its position as the dominant force in North America's carbon capture and storage market, commanding approximately 51% of the regional market share in 2024. The country's leadership is demonstrated through its extensive network of operational CCS facilities and numerous projects under development. The nation has implemented significant policy support, including the Infrastructure Investments and Jobs Act and various tax incentives, to promote CCS adoption. The US market is characterized by diverse applications across natural gas processing, power generation, and industrial sectors, with particular strength in enhanced oil recovery applications.

Carbon Capture and Storage Market in Canada

Canada represents the fastest-growing market in North America, with a projected growth rate of approximately 13% from 2024 to 2029. The country's carbon capture and storage industry is driven by strong government support and ambitious climate goals. Canada's strategic advantage lies in its proximity to suitable geological storage sites, particularly in the Western Canadian Sedimentary Basin. The nation has demonstrated leadership in implementing large-scale CCS projects, with significant developments in the fuel transformation and power generation sectors. Canadian authorities continue to introduce supportive policies and funding mechanisms to accelerate CCS adoption across various industries.

Carbon Capture and Storage Market in Europe

Europe demonstrates strong commitment to carbon capture and storage technology adoption, with significant developments across Germany, the United Kingdom, France, Norway, and the Netherlands. The region's market is characterized by innovative projects and strong policy support for decarbonization initiatives. Each country contributes unique strengths to the market, with the UK leading in project development, Germany focusing on industrial applications, France advancing in technological innovation, Norway pioneering in storage solutions, and the Netherlands developing integrated CCS infrastructure.

Carbon Capture and Storage Market in United Kingdom

The United Kingdom stands as the largest CCS market in Europe, with extensive project development across various industrial sectors. The country's leadership is demonstrated through its comprehensive CCS strategy, particularly in developing industrial clusters and offshore storage capabilities. The UK has established itself as a pioneer in implementing large-scale CCS projects, supported by strong government backing and private sector participation. The nation's focus on developing CCS infrastructure in industrial hubs has created a robust framework for future market expansion.

Carbon Capture and Storage Market in France

France emerges as the fastest-growing market in Europe's CCUS market, driven by its ambitious carbon neutrality goals and comprehensive Carbon Capture, Storage, and Utilization Strategy. The country has identified key industrial zones for CCS deployment, including Dunkerque, Fos-sur-Mer, and Le Havre. France's approach combines technological innovation with strategic industrial planning, focusing on developing integrated solutions for various sectors. The nation's commitment to CCS is demonstrated through multiple collaborative projects and partnerships across the industrial spectrum.

Carbon Capture and Storage Market in Rest of the World

The Rest of the World region encompasses significant CCS developments across various countries, particularly in the Middle East and Brazil. This market segment demonstrates strong potential for growth, driven by increasing environmental regulations and the need for sustainable industrial practices. Brazil leads the carbon capture and storage market size in this region, particularly through its established CCS projects in the oil and gas sector, while Saudi Arabia shows the fastest growth potential due to its ambitious industrial decarbonization initiatives. The region benefits from extensive natural resources and geological storage capabilities, particularly in the Middle East, where countries are increasingly investing in CCS technologies to support their economic diversification goals while addressing environmental concerns.

Get Analysis on Important Geographic Markets

Download PDF

Carbon Capture And Storage Industry Overview

Top Companies in Carbon Capture and Storage Market

The carbon capture and storage companies market features prominent players like ExxonMobil, Shell, Occidental Petroleum, SLB, and Baker Hughes leading technological innovation and project development. These carbon capture and storage companies are increasingly focusing on developing proprietary carbon capture technologies and expanding their project portfolios through strategic partnerships and acquisitions. The industry is witnessing significant investment in research and development to improve capture efficiency and reduce implementation costs. Market leaders are demonstrating operational agility by integrating carbon capture solutions across various industrial sectors, from oil and gas to cement and power generation. Strategic moves include forming dedicated low-carbon divisions, establishing cross-border collaborations, and developing end-to-end CCUS value chains. Companies are also expanding their geographical presence through joint ventures and technology licensing agreements while investing in direct air capture facilities and large-scale storage projects.

Dynamic Market Structure Drives Industry Evolution

The carbon capture and storage market exhibits a complex competitive structure characterized by both global energy conglomerates and specialized technology providers. Major oil and gas companies leverage their existing infrastructure and expertise in subsurface operations to dominate large-scale projects, while specialized engineering firms focus on developing innovative capture technologies and project-specific solutions. The market shows moderate consolidation with increasing vertical integration as companies seek to control multiple aspects of the CCUS industry value chain. The industry is experiencing a wave of strategic partnerships and acquisitions, particularly evident in the collaboration between technology providers and industrial end-users.

The competitive landscape is further shaped by regional dynamics, with different markets showing varying levels of maturity and competitive intensity. North American and European markets feature established players with extensive project experience, while emerging markets see increasing participation from local companies through technology partnerships with global leaders. The industry demonstrates strong collaboration trends, with companies forming consortiums to share project risks and leverage complementary capabilities. Market participants are increasingly focusing on developing specialized expertise in specific aspects of the CCS industry value chain while maintaining flexibility through strategic alliances.

Innovation and Integration Drive Market Success

Success in the carbon capture and storage market increasingly depends on companies' ability to develop cost-effective, scalable solutions while maintaining technological leadership. Incumbent players are strengthening their market position by expanding their intellectual property portfolios, developing modular and adaptable capture technologies, and creating comprehensive service offerings that span the entire CCS value chain. Companies are also focusing on building strong relationships with industrial customers, particularly in hard-to-abate sectors, while investing in digital capabilities to optimize project performance and reduce operational costs. The ability to navigate complex regulatory environments and secure government support remains crucial for project development.

Market contenders are gaining ground by focusing on specialized technological solutions and targeting specific industry segments or geographical regions. Success factors include developing strategic partnerships with established players, demonstrating operational excellence in pilot projects, and maintaining flexibility in business models to adapt to evolving market needs. Companies must also address the growing importance of environmental, social, and governance (ESG) considerations while managing the risk of alternative decarbonization technologies. The regulatory landscape continues to evolve, with increasing support for CCS projects through carbon pricing mechanisms and investment incentives, creating opportunities for both established players and new entrants to expand their market presence. Additionally, carbon capture and sequestration companies are focusing on enhancing carbon capture and storage systems to meet regulatory standards and market demands.

Carbon Capture And Storage Market Leaders

-

Occidental Petroleum Corporation

-

Exxon Mobil Corporation

-

Dakota Gasification Company

-

Air Liquide

-

Shell PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Carbon Capture And Storage Market News

- March 2024: JX Nippon Oil & Gas Exploration Corporation and Chevron New Energies, a division of Chevron U.S.A. Inc., entered into a memorandum of understanding aimed at assessing the potential export of carbon dioxide from Japan to carbon capture and storage (CCS) initiatives situated in Australia and other nations across Asia-Pacific. This agreement enhances the company's market footprint.

- March 2024: Shell and ONGC collaborated on a storage study and enhanced oil recovery (EOR) screening assessment in India, including depleted oil and gas fields and saline aquifers. This collaboration aims to develop carbon capture, utilization, and storage, or CCUS/carbon capture and storage (CCS), as an emissions mitigation tool for combating climate change and injecting carbon dioxide for geological storage and enhanced oil production from mature fields of ONGC.

- February 2024: Fluor Corporation and Chevron New Energies signed a license agreement with Fluor to use its proprietary Econamine FG PlusSM carbon capture technology to reduce carbon dioxide emissions at Chevron’s Eastridge Cogeneration facility in Kern County, California.

Carbon Capture and Storage Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Emerging Demand for CO2 Injection Technique for Enhanced Oil Recovery (EOR)

- 4.1.2 Strict Government Norms Toward GHG Emissions

-

4.2 Market Restraints

- 4.2.1 Huge CCS Technology Implementation Costs

- 4.2.2 Growth in Shale Investments

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 By Technology

- 5.1.1 Pre-combustion Capture

- 5.1.2 Oxy-fuel Combustion Capture

- 5.1.3 Post-combustion Capture

-

5.2 By End-user Industry

- 5.2.1 Oil and Gas

- 5.2.2 Coal and Biomass Power Plant

- 5.2.3 Iron and Steel

- 5.2.4 Chemical

- 5.2.5 Cement

-

5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 Australia

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Norway

- 5.3.3.5 Netherlands

- 5.3.3.6 Rest of Europe

- 5.3.4 Rest of the World

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Air Liquide

- 6.4.2 Aker Solutions

- 6.4.3 Baker Hughes Company

- 6.4.4 Dakota Gasification Company

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Fluor Corporation

- 6.4.7 General Electric

- 6.4.8 Halliburton

- 6.4.9 Honeywell International Inc.

- 6.4.10 Japan CCS Co. Ltd

- 6.4.11 JX Nippon Oil & Gas Exploration Corporation

- 6.4.12 Linde PLC

- 6.4.13 Mitsubishi Heavy Industries Ltd

- 6.4.14 Occidental Petroleum Corporation

- 6.4.15 Shell PLC

- 6.4.16 Siemens Energy

- 6.4.17 SLB

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Augmenting Prominence for Bioenergy Carbon Capture and Storage (BECCS)

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Carbon Capture And Storage Industry Segmentation

Carbon capture and storage (CCS) is a technology that can capture up to 90% of the carbon dioxide emissions produced from various sources that use fossil fuels in electricity generation and industrial processes, preventing carbon dioxide from entering the atmosphere. The first stage in the CCS process is capturing carbon dioxide released while burning fossil fuels or as a result of industrial processes, such as making cement and steel or in the chemical industry.

The carbon capture and storage market is segmented by technology, end-user industry, and geography. By technology, the market is segmented into pre-combustion capture, oxy-fuel combustion capture, and post-combustion capture. The market is segmented by end-user industries into oil and gas, coal and biomass power plants, iron and steel, chemical, and cement. The report also covers the market size and forecasts for 12 countries across major regions. For each segment, the market sizing and forecasts are provided based on revenue (USD).

| By Technology | Pre-combustion Capture | ||

| Oxy-fuel Combustion Capture | |||

| Post-combustion Capture | |||

| By End-user Industry | Oil and Gas | ||

| Coal and Biomass Power Plant | |||

| Iron and Steel | |||

| Chemical | |||

| Cement | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Norway | |||

| Netherlands | |||

| Rest of Europe | |||

| Rest of the World | |||

Need A Different Region or Segment?

Customize Now

Carbon Capture and Storage Market Research FAQs

How big is the Carbon Capture And Storage Market?

The Carbon Capture And Storage Market size is expected to reach USD 2.76 billion in 2025 and grow at a CAGR of 14.21% to reach USD 5.37 billion by 2030.

What is the current Carbon Capture And Storage Market size?

In 2025, the Carbon Capture And Storage Market size is expected to reach USD 2.76 billion.

Who are the key players in Carbon Capture And Storage Market?

Occidental Petroleum Corporation, Exxon Mobil Corporation, Dakota Gasification Company, Air Liquide and Shell PLC are the major companies operating in the Carbon Capture And Storage Market.

Which is the fastest growing region in Carbon Capture And Storage Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Carbon Capture And Storage Market?

In 2025, the North America accounts for the largest market share in Carbon Capture And Storage Market.

What years does this Carbon Capture And Storage Market cover, and what was the market size in 2024?

In 2024, the Carbon Capture And Storage Market size was estimated at USD 2.37 billion. The report covers the Carbon Capture And Storage Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Carbon Capture And Storage Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Carbon Capture And Storage Market Research

Mordor Intelligence delivers a comprehensive analysis of the carbon capture and storage industry. We leverage our extensive expertise in carbon management and emissions reduction technology. Our detailed research covers the complete spectrum of carbon capture utilization and storage (CCUS) and carbon capture and storage (CCS) technologies. This includes direct air capture, CO2 capture, and carbon dioxide removal systems. The report PDF, available for download, provides in-depth coverage of carbon storage technology, carbon transportation infrastructure, and geological carbon storage solutions. It offers stakeholders a thorough understanding of this rapidly evolving sector.

Our analysis benefits industry participants by delivering crucial insights into carbon capture equipment developments and industrial carbon capture implementations. It also highlights emerging clean carbon technology trends. The report examines carbon storage solutions and greenhouse gas capture methodologies. Additionally, it provides detailed carbon capture and storage market size projections and growth indicators. Stakeholders gain access to comprehensive carbon sequestration technology assessments and decarbonization technology advancements. The report also offers strategic insights into CCUS market dynamics, enabling informed decision-making in this critical industry sector.