Caravan And Motor Home Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

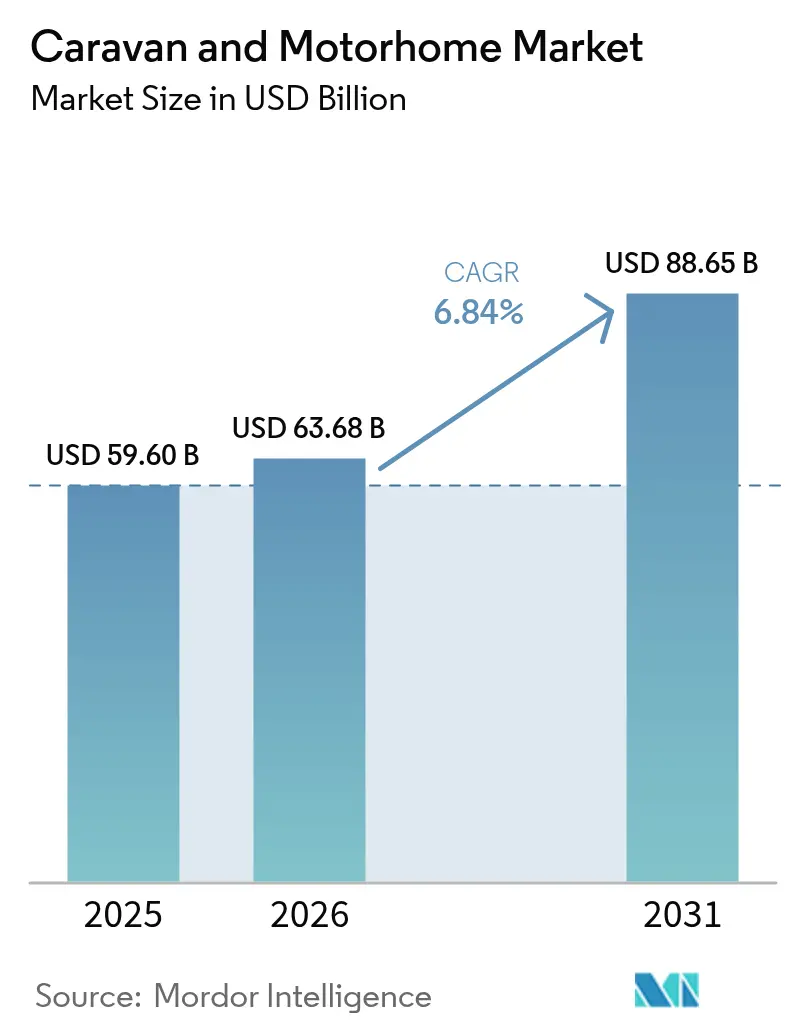

| Market Size (2026) | USD 63.68 Billion |

| Market Size (2031) | USD 88.65 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

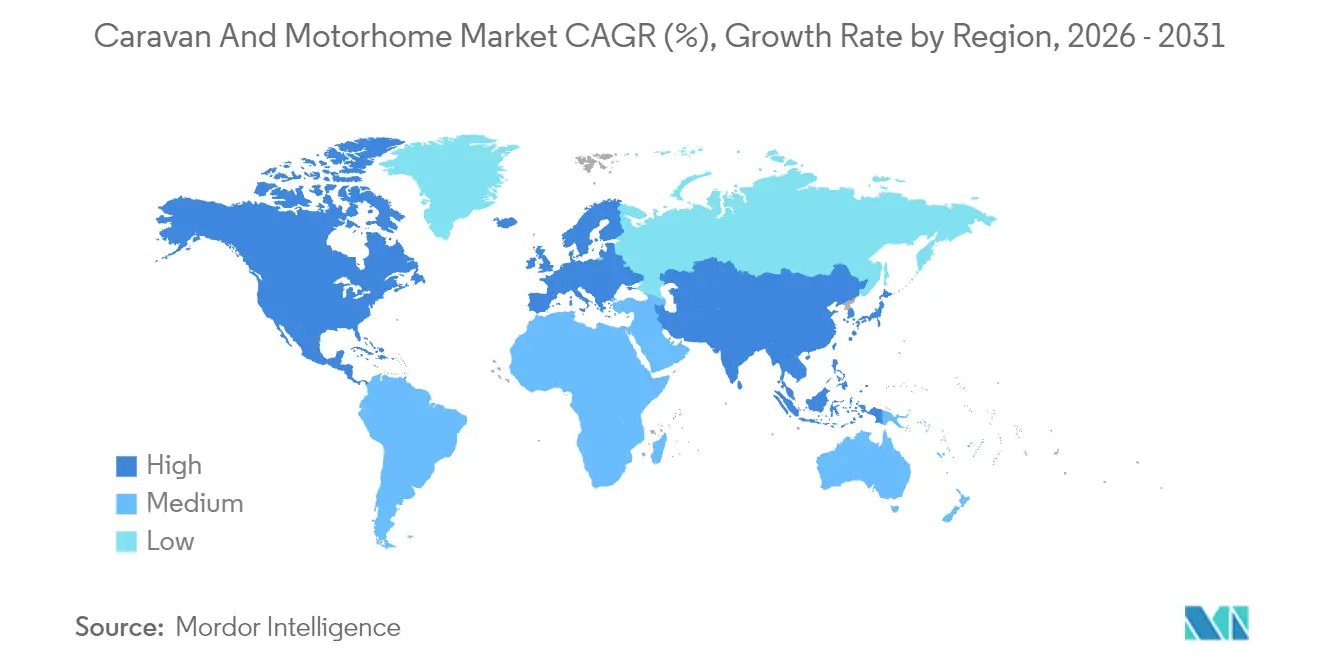

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Caravan And Motor Home Market Analysis by Mordor Intelligence

The Caravan And Motor Home Market size in 2026 is estimated at USD 63.68 billion, growing from 2025 value of USD 59.60 billion with 2031 projections showing USD 88.65 billion, growing at 6.84% CAGR over 2026-2031. Continued growth aligns with rising demand for experiential travel, the spread of remote-work lifestyles, and sustained interest in domestic road trips that gained traction during the pandemic. Technological advances such as modular chassis platforms and 48-volt DC electrical systems enhance off-grid capability. At the same time, demographic shifts toward millennial and Gen-Z buyers inject fresh spending power into the Caravan And Motor Home Market. North America retains leadership because of a mature RV culture and expansive campground infrastructure. In contrast, the Asia-Pacific region registers the fastest regional expansion as disposable incomes and outdoor recreation participation climb. Competitive intensity rises as European brands globalize and new entrants focus on electric and modular formats that traditional hospitality options struggle to match.

Key Report Takeaways

- By product type, caravans led the Caravan And Motor Home Market with 61.34% of the share in 2025, while motorhomes are forecast to advance at an 8.08% CAGR through 2031.

- By propulsion, internal-combustion models commanded 91.74% of the Caravan And Motor Home Market share in 2025, but battery-electric units are projected to expand at a 8.94% CAGR by 2031.

- By length, sub-6-meter units captured 46.72% of the Caravan And Motor Home Market share in 2025, whereas 6-to-8-meter models are set for a 7.29% CAGR to 2031.

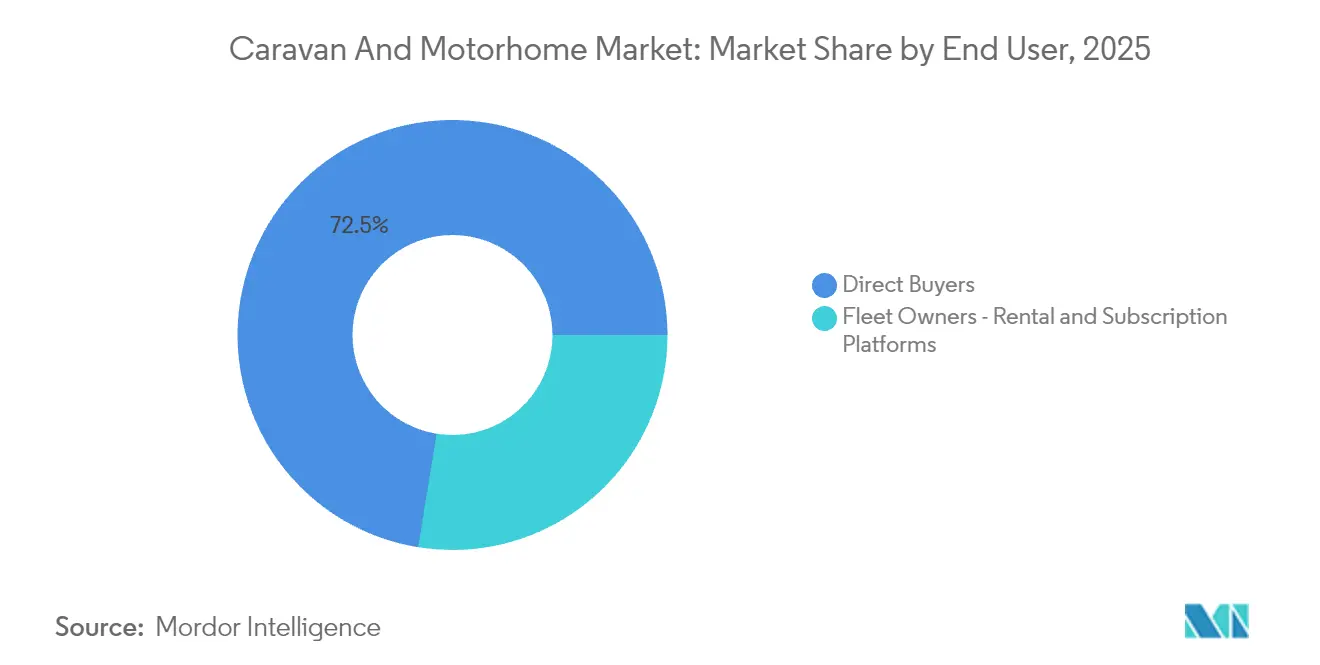

- By end user, direct buyers held a 72.45% of the Caravan And Motor Home Market share in 2025; fleet and rental operators are expected to post a 7.05% CAGR growth through 2031.

- By sales channel, franchise dealerships accounted for 64.88% of the Caravan And Motor Home Market share in 2025, while online direct-to-consumer sales should climb at an 8.43% CAGR during the forecast period.

- By geography, North America controlled 53.25% of the Caravan And Motor Home Market revenue in 2025, yet Asia-Pacific is set to deliver an 8.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Caravan And Motor Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic and Outdoor Travel Boom | +1.2% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Millennial/Gen-Z RV Uptake | +1.0% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Remote Work–RV Lifestyle | +0.8% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Modular RV Platforms | +0.6% | North America and Europe, early adoption | Long term (≥ 4 years) |

| 48V Off-Grid Systems | +0.7% | Global, led by North America | Medium term (2-4 years) |

| OEM–Campground Booking APIs | +0.5% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Domestic and Outdoor Travel Post-COVID

The recent industry survey highlights a growing preference for planned camping and road trips, reflecting a shift from international to domestic travel. Safety concerns, border complexities, and the cost-effectiveness of local exploration drive this trend. RV camping continues to gain popularity, helping stabilize the Caravan And Motor Home Market amid broader economic uncertainties. Well-developed campground networks in North America and Europe offer convenience comparable to hotels, enhancing the appeal of RV travel. For many families, owning an RV is a strategic way to manage unpredictable travel costs, reinforcing long-term demand.

Surging Millennial and Gen-Z RV Ownership

The average RV buyer’s age fell from 53 to 49 years as millennials and Gen-Z consumers elevated adventure travel over asset accumulation, positioning younger cohorts to influence design and marketing strategies [1]“RV Ownership Demographic Study,”, RV Industry Association, rvia.org. Most owners aged 35-54 prioritize connectivity, sustainability, and flexible interiors, steering manufacturers toward lighter materials, solar integration, and modular furniture. Social media further amplifies demand, as peer reviews and influencer content normalize full-time or hybrid nomadic lifestyles. Lenders have responded with term structures that mirror auto financing, helping first-time buyers surmount high ticket prices. Continuous engagement through upgrades and digital features improves retention and feeds repeat purchases, supporting sustained Caravan And Motor Home Market growth.

Rise in Remote-Work-Enabled “Work-From-RV” Lifestyle

Most RV owners now work remotely, and many remote professionals employ their units as mobile offices, redefining usage patterns beyond seasonal recreation. Extended stay durations validate investments in premium connectivity, lithium battery banks, and ergonomic workspaces that were previously optional. Motorhomes benefit most, as integrated cab-to-cabin environments streamline transitions between driving and working, underpinning their faster growth outlook. Manufacturers incorporate 5G antennas, modular desks, and sound-insulated zones to meet productivity demands. The Caravan And Motor Home Market gains stickiness because users who blend work and travel log higher annual mileage, accelerating replacement cycles and aftermarket spending.

Emergence of Modular, Upgradable RV Platforms

AC Future’s AI-THt trailer, which expands from 195 to 400 square feet and retails at USD 148,000, illustrates how adaptable footprints add value across life stages[2]“AI-THt Expandable Trailer Overview,”, AC Future, acfuture.io. Happier Camper’s Adaptiv system lets owners reconfigure interiors for cargo, family, or luxury use, extending utility without buying a second unit. Upgradability lowers lifetime costs and keeps vehicles technologically current, feeding a secondary market for modules and third-party accessories. Younger buyers gravitate toward flexible layouts, ensuring the trend carries long-term upside. Manufacturers that build open-architecture chassis can monetize post-sale enhancements, creating annuity-like revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High RV Ownership Costs | -0.8% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Rate-Sensitive Financing | -0.6% | North America and Europe, developed markets | Short term (≤ 2 years) |

| DIY and Rental Competition | -0.4% | Global, concentrated in urban markets | Medium term (2-4 years) |

| Grid Limits in Parks (High-Capacity RVs) | -0.3% | North America, expanding to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Purchase and Ownership Cost

The cost of financing new and used RV units is placing significant pressure on household budgets. Additional expenses like insurance, maintenance, and storage often lead to early resale, dampening customer satisfaction and reducing positive word-of-mouth. Despite strong lifestyle alignment with RV travel, younger buyers are susceptible to pricing due to limited disposable income. Oversupply in some markets has led to notable price corrections, underscoring how elevated prices can amplify volatility. The industry continues to face the challenge of managing affordability without compromising profitability.

Competition From DIY Van Conversions and Peer-To-Peer Rentals

Platforms such as Camplify and Indie Campers let casual travelers rent without owning, reducing the number of prospective first-time buyers. Do-it-yourself conversions appeal to budget-minded or creative users who desire bespoke interiors at a lower cost. Rental fleets proliferate in gateway cities, offering trial experiences that sometimes satisfy rather than stimulate purchase intent. Traditional OEMs must either cultivate their own rental channels or risk ceding share. The rise of access-over-ownership models introduces structural elasticity into the Caravan And Motor Home Market’s volume outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Caravans Lead Despite Motorhome Momentum

Caravans captured 61.34% of the Caravan And Motor Home Market revenue in 2025 as value-minded buyers favored lower acquisition costs and the flexibility of using the tow vehicle for daily transit. Within this segment, travel trailers span budget to luxury price points, broadening appeal, while fifth-wheel units attract full-time users seeking residential comfort. Folding campers, though lighter and garage-friendly, lose share as customers graduate to hard-sided models that offer better insulation and security. Motorhomes, however, are forecast for an 8.08% CAGR through 2031, eclipsing the broader Caravan And Motor Home Market pace thanks to integrated living-driving layouts that ease spontaneous travel. Class B vans stand out among urban adventurers for parking convenience, whereas Class A coaches draw retirees and digital nomads willing to invest in spacious interiors.

Growing millennial interest in turnkey solutions benefits motorhomes, incorporating driver-assistance tech, solar arrays, and smart-home controls more readily than towables. Thor Industries’ hybrid Class A prototype and Jayco’s USD 460,000 Embark EV illustrate premium adoption of integrated propulsion and living systems. Caravan makers counter with lighter composite walls and modular interiors to close the innovation gap. As campsite booking APIs and solar-storage packages become standard, product differentiation hinges on digital ecosystems as much as floor plans. Consequently, caravans will retain volume leadership, but motorhomes will set the technological agenda of the Caravan And Motor Home Market.

By Propulsion: Electric Transition Accelerates Despite ICE Dominance

Internal combustion engine models retained 91.74% of the Caravan And Motor Home Market revenue in 2025, reflecting well-established fueling networks and proven durability. Yet battery-electric RVs are projected for a 8.94% CAGR through 2031, well above the overall Caravan And Motor Home Market size trajectory, as environmental regulations tighten and battery costs fall. Early entrants like Lightship’s aerodynamic travel trailer highlight demand for silent operation and low running costs. Hybrid systems serve as a bridge, pairing combustion engines for range with electric motors for campground maneuverability and quiet overnight power.

Fleet rental firms adopt electrics fastest, using predictable routes and depot charging to mitigate infrastructure gaps. Consumer adoption remains sensitive to national park charging restrictions and upfront pricing, but state and provincial incentives improve ROI metrics annually. Manufacturers leverage commercial EV chassis from Ford E-Transit or Mercedes eSprinter platforms to shorten development cycles. Lighter packs free interior space as battery density rises, easing the length-regulation tension. Overall, combustion will dominate this decade, yet electrification sets the innovation narrative for the Caravan And Motor Home Market.

By Length: Compact Units Dominate While Mid-Size Grows

Vehicles under 6 meters garnered 46.72% of the Caravan And Motor Home Market revenue 2025, favored in Europe and Japan for maneuverability on narrow roads and compatibility with passenger-car licenses. Pop-top roofs and slide-outs maximize space without breaching length caps, keeping the segment relevant among city dwellers. The 6-to-8-meter band, however, should log a 7.29% CAGR through 2031, balancing livable interiors with campground accessibility. Younger families and remote workers view this size as a sweet spot that fits most national-park pads yet supports separate sleeping and working zones.

Units over 8 meters cater to luxury buyers but face growing restrictions from campgrounds limiting vehicle length for turnover efficiency. Average stall sizes in the United States parks have not expanded in two decades, compounding constraints for large rigs. Electric drive trains may upend the calculus by relocating power components under the floor, reclaiming cabin space without extending length. Thus, mid-size gains will reflect regulatory realities and changing lifestyle expectations within the Caravan And Motor Home Market.

By End User: Fleet Rental Growth Challenges Direct Ownership

Direct purchasers still accounted for 72.45% of the Caravan And Motor Home Market revenue in 2025, valuing personal customization and the freedom to embark at will. Fleet and rental operators, though, are projected to grow 7.05% annually, leveraging sharing-economy platforms to monetize idle capacity. Peer-to-peer networks like Camplify add scale with minimal capital, matching vehicles to regional demand spikes. Manufacturers pursue bulk deals with rental fleets to stabilize factory utilization, albeit at thinner margins.

Rental exposure is product discovery, turning some renters into future buyers and satisfying occasional users who forego ownership. Remote workers often experiment via rentals before committing, a trend that may elongate sales funnels. OEMs experiment with subscription models that blend ownership and rental, supplying flexibility without relinquishing customer lifetime value. Consequently, fleet channels will accelerate but not eclipse direct Caravan And Motor Home Market ownership.

By Sales Channel: Online Direct Sales Accelerate

Franchise dealerships produced 64.88% of the Caravan And Motor Home Market revenue in 2025, supported by financing arrangements, trade-in services, and regional service centers. Younger consumers, however, drive an 8.43% CAGR in direct-to-consumer online transactions, drawn by transparent pricing and customization tools. Electric-focused startups bypass dealer mark-ups, offering mobile service vans instead of fixed shops. In response, legacy OEMs integrate e-commerce configurators while retaining dealers for delivery and service.

Company-owned showrooms occupy a hybrid niche, enabling immersive brand experiences yet retaining control over margins. As products become more software-defined, over-the-air updates diminish reliance on dealer workshops, boosting the appeal of online channels. Still, the complexity of RV financing and insurance keeps brick-and-mortar relevant, ensuring a multichannel equilibrium for the Caravan And Motor Home Market.

Geography Analysis

North America controlled 53.25% of the Caravan And Motor Home Market revenue in 2025, underpinned by deep-rooted RV culture, vast public lands, and financing structures that ease high-ticket purchases. The United States shipments climbed in 2025 and are projected to grow in the coming years, signaling resilient domestic demand despite higher interest rates. Canada contributes specialized composite-panel suppliers and a growing cohort of full-time digital nomads, strengthening regional aftermarket ecosystems. National park entry fees and campground upgrades funnel public funds into site expansion, supporting usage growth. The Caravan And Motor Home Market also benefits from the widespread availability of Class B conversions that suit urban storage restrictions.

Europe advanced steadily, led by Germany. Compact layouts remain essential due to narrow roads and stringent emission zones. Italy and Spain focus on agri-tourism sites that welcome RVs, diversifying overnight options beyond commercial campgrounds. Scandinavian countries see higher electric adoption spurred by renewable energy incentives, adding a technology edge to the region’s Caravan And Motor Home Market.

Asia-Pacific records the fastest 8.55% CAGR through 2031, propelled by rising disposable income and evolving tourism policies. Japan’s RV market is growing, featuring innovations like electric pop-up roofs that preserve garage height limits. China’s middle class shows growing interest, supported by government promotion of domestic tourism corridors, yet infrastructure gaps persist in western provinces. Australia’s mature caravan scene benefits from peer-to-peer rentals, with Camplify’s fleet expansion driving utilization. Emerging markets like South Korea and India invest in roadway rest areas with RV hookups, establishing early-stage demand. Overall, infrastructural progress and lifestyle shifts keep the Asia-Pacific pivotal to future Caravan And Motor Home Market size growth.

Competitive Landscape

Thor maintained its leadership despite competitive pressures, particularly from Forest River, which gained ground in key retail channels like Camping World. Vertical integration is a common strategy as leading OEMs acquire component suppliers to shield margins from input-cost swings. Investments in electric propulsion and modular interiors differentiate product portfolios and justify premium pricing. European manufacturers such as Trigano and Knaus Tabbert expand export footprints, intensifying North American rivalry while cultivating Asia-Pacific dealerships.

Disruptive entrants emphasize direct online sales, subscription models, and electric platforms. Lightship positions its battery-powered trailer as a technology point of reference, while RollAway targets rental fleets with zero-emission coaches. API tie-ups with Hipcamp and Spot2Nite signal a shift toward service-based ecosystems, prompting OEMs to hire software staff traditionally absent in vehicle manufacturing. Quality control remains under scrutiny; a string of NHTSA recalls in 2024 spotlighted electrical-system and axle faults, making reliability a brand differentiator [3]“RV Safety Recalls 2024,”, National Highway Traffic Safety Administration, nhtsa.gov.

Capital markets judge performance closely. European OEMs hedge with aftermarket parts and rental subsidiaries that generate counter-cyclical income. As electrification ramps up, battery sourcing and charging-infrastructure alliances become strategic imperatives, suggesting future partnerships between RV makers and energy providers. Competitive dynamics, therefore, hinge on technology adoption speed, ecosystem breadth, and global distribution reach within the Caravan And Motor Home Market.

Caravan And Motor Home Industry Leaders

Thor Industries Inc.

Forest River Inc.

Winnebago Industries Inc.

Trigano SA

Knaus Tabbert AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: THOR Industries, Inc., a frontrunner in the recreational vehicle (RV) sector, unveiled the Embark®, the world's inaugural range-extended electric Class A motorhome, crafted by Entegra Coach®. This launch underscores a pivotal achievement in THOR's five-year quest towards electrification.

- July 2025: Renault, a frontrunner in Europe's light commercial vehicle arena, joined forces with Ahorn Camp, a prominent German motorhome brand, to launch a cutting-edge motorhome series. The new Renault Master, set for mass production by the Erwin Hymer Group, has been exclusively chosen by Ahorn Camp. Enthusiasts can find these models showcased at Ahorn Camp's showrooms and Renault Pro+ dealers throughout Europe.

Global Caravan And Motor Home Market Report Scope

Caravans are most commonly used as temporary accommodation while traveling. However, some people use them as their main residence due to benefits like easily towable units, low fuel consumption, lower maintenance and insurance costs, and depreciation value.

The caravan and motorhomes market is segmented by product type, end user, and geography. By product type, the market is segmented into caravans and motorhomes. By caravan type, the market is segmented into travel trailers, fifth-wheel trailers, folding camp trailers, and truck campers. By motorhome type, the market is sub-segmented into Type A, Type B, and Type C. By end user, the market is segmented into direct buyers and fleet owners. By geography, the market covers North America, Europe, Asia-Pacific, and the Rest of the World. For each segment, the market size and forecasts are based on the value (USD).

| Caravan | Travel Trailers |

| Fifth-Wheel Trailers | |

| Folding Camp Trailers | |

| Truck Campers | |

| Motorhome | Class A |

| Class B (Van Conversions) | |

| Class C |

| Internal-Combustion Engine (ICE) |

| Hybrid (Parallel / Series) |

| Battery-Electric RV |

| Below 6 meters |

| 6-8 meters |

| Above 8 meters |

| Direct Buyers |

| Fleet Owners - Rental and Subscription Platforms |

| Franchise Dealerships |

| Company-Owned Stores |

| Online Direct-to-Consumer |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| Australia | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Caravan | Travel Trailers |

| Fifth-Wheel Trailers | ||

| Folding Camp Trailers | ||

| Truck Campers | ||

| Motorhome | Class A | |

| Class B (Van Conversions) | ||

| Class C | ||

| By Propulsion | Internal-Combustion Engine (ICE) | |

| Hybrid (Parallel / Series) | ||

| Battery-Electric RV | ||

| By Length | Below 6 meters | |

| 6-8 meters | ||

| Above 8 meters | ||

| By End User | Direct Buyers | |

| Fleet Owners - Rental and Subscription Platforms | ||

| By Sales Channel | Franchise Dealerships | |

| Company-Owned Stores | ||

| Online Direct-to-Consumer | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| Australia | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the Caravan And Motor Home Market?

The Caravan And Motor Home Market size reached USD 63.68 billion in 2026 and is forecast to hit USD 88.65 billion by 2031.

Which region leads sales of caravans and motorhomes?

North America held 53.25% of global revenue in 2025 thanks to established RV culture and campground networks.

Which segment is expanding fastest by propulsion?

Battery-electric RVs are projected to grow at a 8.94% CAGR through 2031, outpacing all other propulsion types.

Are online channels becoming significant for RV sales?

Yes; direct-to-consumer online sales are forecast to rise at an 8.43% CAGR, driven by younger buyers seeking transparent pricing and customization tools.

Page last updated on: