| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| CAGR | 6.20 % |

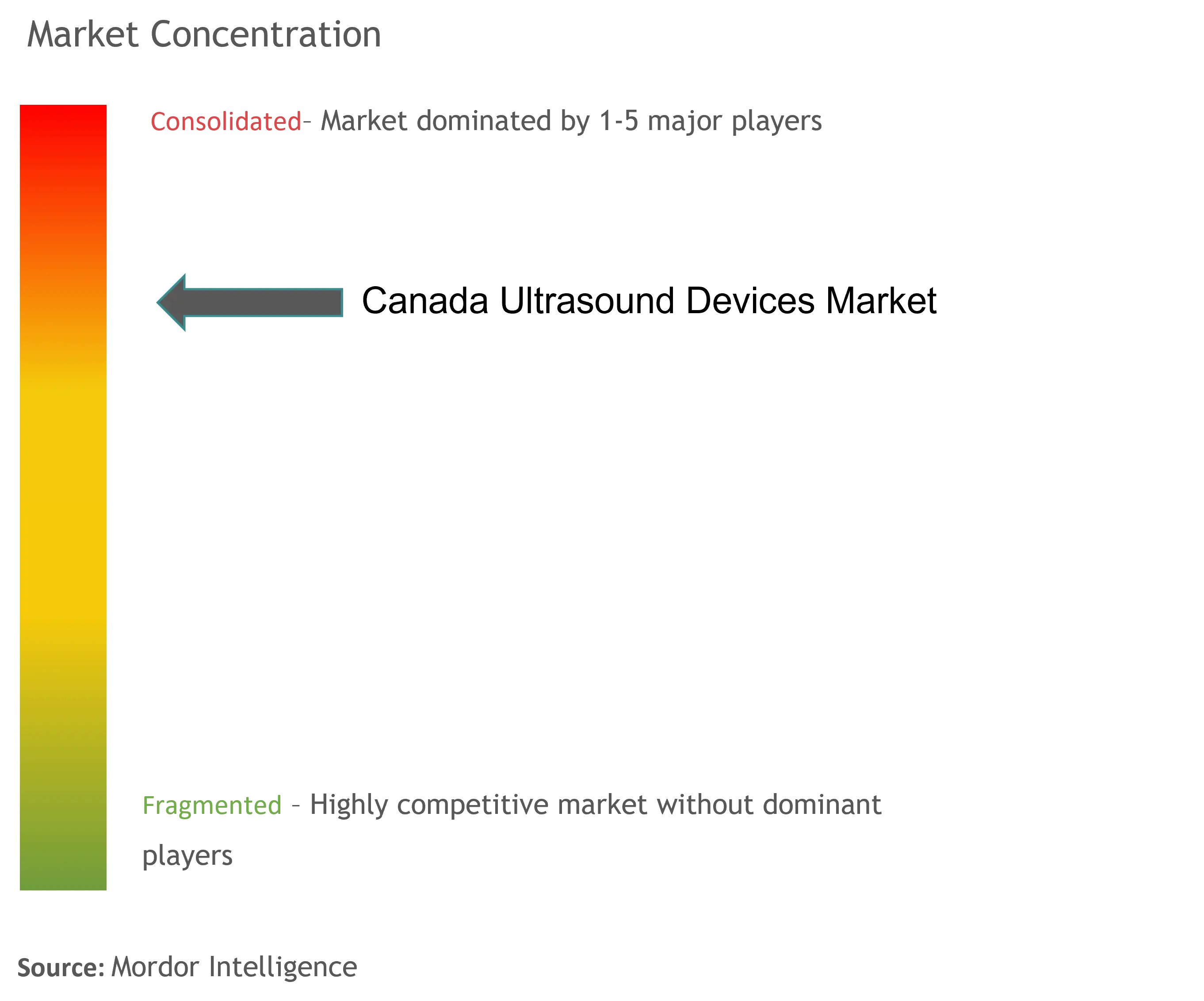

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Ultrasound Devices Market Analysis

The Canada Ultrasound Devices Market is expected to register a CAGR of 6.2% during the forecast period.

The Canadian ultrasound devices industry is experiencing significant transformation driven by technological innovation and healthcare modernization. Advanced imaging capabilities, artificial intelligence integration, and improved connectivity features are reshaping diagnostic capabilities across healthcare facilities. The emergence of point-of-care ultrasound equipment systems has particularly revolutionized bedside diagnostics, enabling faster decision-making and improved patient care outcomes. Healthcare providers are increasingly adopting these advanced systems to enhance diagnostic accuracy and streamline workflow efficiency, particularly in emergency and critical care settings.

The market landscape is witnessing a surge in strategic partnerships and product innovations from key industry players. In June 2023, Butterfly Network achieved a significant milestone with the approval of their second-generation iQ+ device, featuring advanced Ultrasound-on-Chip technology in Canada. Similarly, PENTAX Medical's launch of their Performance Endoscopic Ultrasound (EUS) system, combining the Arietta 65 PX ultrasound scanner with J10 Series ultrasound gastroscopes, demonstrates the industry's commitment to technological advancement. These developments are significantly enhancing diagnostic capabilities and improving healthcare delivery across various medical specialties.

The growing prevalence of chronic conditions is substantially influencing market dynamics and driving demand for advanced diagnostic solutions. According to the Kidney Foundation Canada's January 2022 report, approximately one in ten Canadians, representing 4 million people, are affected by kidney disease. This high disease burden has intensified the need for sophisticated medical ultrasound devices capable of detailed organ visualization and accurate diagnosis. Healthcare facilities are increasingly investing in advanced ultrasound devices to meet these growing diagnostic requirements and improve patient outcomes.

The industry is experiencing a notable shift toward portable and compact ultrasound equipment, reflecting the growing demand for flexible diagnostic solutions. Manufacturers are focusing on developing user-friendly interfaces and ergonomic designs to enhance operator comfort and efficiency. The integration of cloud-based solutions and remote diagnostic capabilities is enabling healthcare providers to extend their services to remote locations and underserved communities. These technological advancements are not only improving accessibility to diagnostic services but also contributing to more efficient healthcare delivery models across Canada.

Ultrasound Devices Market Trends

Rising Prevalence of Chronic Diseases and Cancer

The increasing burden of chronic diseases and cancer in Canada serves as a primary driver for the ultrasound devices market. According to a November 2022 report by the Government of Canada, approximately 223,900 Canadians were diagnosed with cancer in 2022, with prostate cancer remaining the most diagnosed form, accounting for 46% of all cancer diagnoses. The report further highlighted that breast cancer affects one in every eight women during their lifetime in Canada, emphasizing the critical need for early detection and diagnostic capabilities. This rising disease burden has created an increased demand for advanced diagnostic tools, particularly ultrasound devices that offer non-invasive and reliable screening options.

The prevalence of cardiovascular diseases and musculoskeletal disorders has also contributed significantly to the demand for ultrasound devices. These conditions require regular monitoring and diagnostic imaging for effective treatment planning and progress assessment. The versatility of ultrasound technology in diagnosing various conditions, from cardiovascular issues to musculoskeletal problems, has made it an indispensable tool in the Canadian healthcare system, driving its adoption across medical facilities nationwide.

Understand The Key Trends Shaping This Market

Download PDF

Technological Advancements and Strategic Initiatives

The integration of artificial intelligence and advanced imaging capabilities has revolutionized the ultrasound devices market in Canada. Strategic partnerships and innovations have played a crucial role in market expansion, as exemplified by the December 2021 collaboration between Medo, Medical Imaging Consultants (MIC), and Western Canada to revolutionize diagnostic imaging through AI integration. Additionally, the approval of NovaGuide intelligent ultrasound by Health Canada has introduced real-time brain blood flow monitoring capabilities, demonstrating the market's technological progression. These advancements have significantly improved diagnostic accuracy and efficiency, making ultrasound devices more valuable in clinical settings.

The continuous development of innovative solutions is further evidenced by breakthrough research and development initiatives. For instance, in May 2022, the University of Alberta experts developed a pioneering 2D ultrasound system specifically designed for dental offices, expanding the application scope of ultrasound technology. The market has also witnessed numerous strategic partnerships between healthcare facilities and technology providers, fostering the development and implementation of cutting-edge ultrasound solutions. These collaborations have not only enhanced the accessibility of advanced ultrasound technologies but have also contributed to improving patient care standards across Canada.

Growing Aging Population

The expanding elderly population in Canada has emerged as a significant driver for the ultrasound devices market. The aging demographic typically requires more frequent medical imaging for various age-related conditions, including cardiovascular diseases, musculoskeletal disorders, and cancer screening. This population segment's increasing healthcare needs have spurred the demand for advanced diagnostic tools, particularly ultrasound devices that offer safe and non-invasive examination options.

The healthcare requirements of the elderly population have also influenced the development of specialized ultrasound applications and features. Medical facilities are increasingly investing in ultrasound equipment that offers enhanced visualization capabilities and specialized scanning modes suitable for geriatric care. The portability and versatility of modern ultrasound devices have made them particularly valuable in providing point-of-care diagnostics for elderly patients, whether in hospitals, clinics, or long-term care facilities, driving the market's growth in response to this demographic trend.

Increasing Healthcare Infrastructure Development

The ongoing modernization and expansion of healthcare infrastructure in Canada have significantly contributed to the growth of the ultrasound devices market. Healthcare facilities are increasingly investing in advanced diagnostic equipment, including state-of-the-art ultrasound systems, to enhance their diagnostic capabilities and improve patient care. This infrastructure development is evidenced by strategic partnerships between healthcare providers and medical technology companies, focusing on comprehensive equipment modernization programs.

The emphasis on improving healthcare accessibility has led to the establishment of new diagnostic centers and the upgrading of existing facilities with modern ultrasound equipment. Healthcare institutions are adopting integrated healthcare solutions that incorporate advanced ultrasound technologies, enabling better patient care coordination and diagnostic accuracy. These infrastructure improvements, coupled with the increasing focus on preventive healthcare, have created a robust environment for the growth of the ultrasound devices market in Canada, supporting both urban and rural healthcare delivery systems.

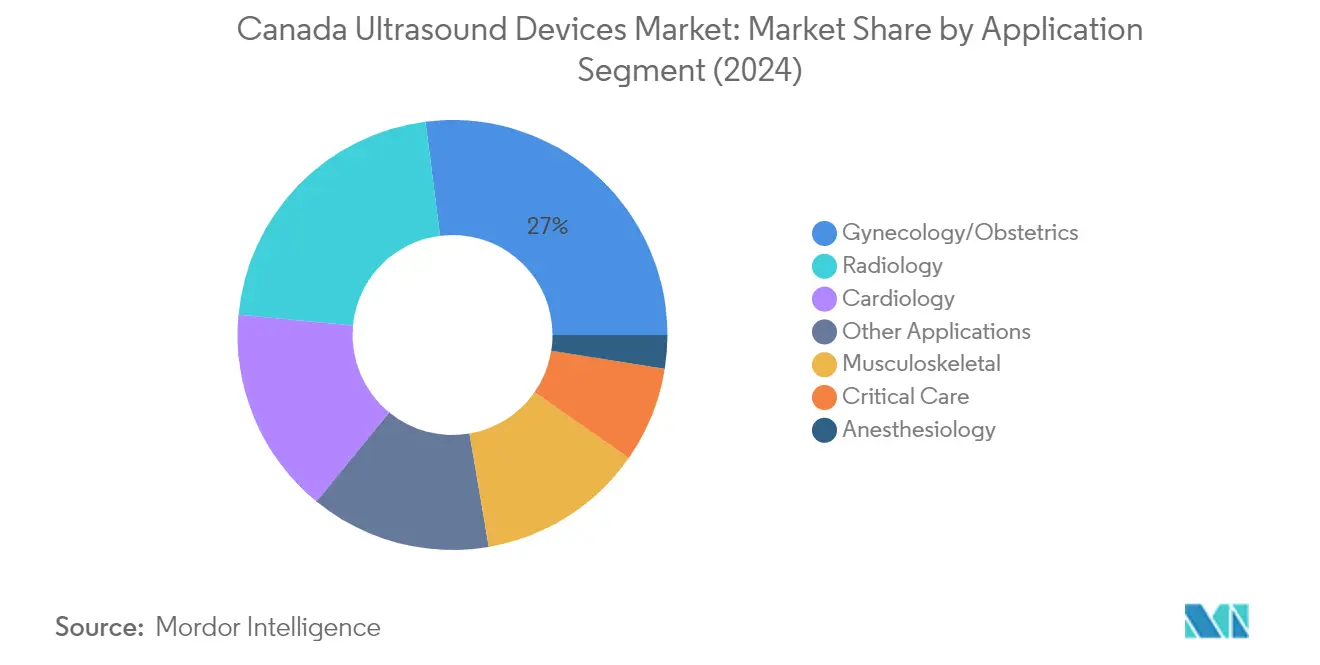

Segment Analysis: By Application

Gynecology/Obstetrics Segment in Canada Ultrasound Devices Market

The Gynecology/Obstetrics segment dominates the Canada ultrasound devices market, holding approximately 27% market share in 2024. This significant market position is driven by the rising prevalence of women's health-related diseases such as breast cancer and precancerous diseases of reproductive organs. The segment's growth is further supported by increasing patient preference for minimally invasive procedures and technological advancements in ultrasound equipment, such as 3D and 4D imaging capabilities. The rising cases of infertility in Canada, affecting approximately 16% of Canadian couples, have also contributed to the increased demand for gynecological medical ultrasound devices for diagnostic purposes. Additionally, the segment benefits from the comprehensive coverage of women's health services in Canada's healthcare system and the growing emphasis on preventive care and early disease detection.

Anesthesiology Segment in Canada Ultrasound Devices Market

The Anesthesiology segment is emerging as the fastest-growing segment in the Canadian ultrasound devices market, projected to grow at approximately 7% during 2024-2029. This remarkable growth is primarily driven by the increasing adoption of ultrasound-guided peripheral nerve blockade and vascular access applications in anesthesiology. The segment's expansion is further supported by ongoing research and development in point-of-care ultrasound (POCUS) applications for perioperative medicine. The implementation of new POCUS curricula across Canadian medical institutions and the growing emphasis on competency-based training programs are contributing to increased utilization of anesthesia ultrasound systems. Additionally, technological advancements in ultrasound systems specifically designed for anesthesia applications are further accelerating the segment's growth.

Remaining Segments in Application Market

The remaining segments in the Canadian ultrasound devices market include Radiology, Cardiology, Musculoskeletal, Critical Care, and Other Applications, each serving distinct medical needs. The Radiology segment maintains a strong presence due to its widespread use in diagnostic imaging and cancer detection. The Cardiology segment is driven by the increasing prevalence of cardiovascular diseases and the growing adoption of advanced cardiac imaging technologies. The Musculoskeletal segment benefits from rising cases of orthopedic conditions and sports injuries, while the Critical Care segment is expanding due to the increasing adoption of point-of-care ultrasound in emergency and intensive care settings. Other Applications encompass various specialized uses, including thyroid, liver, and gastrointestinal imaging.

Segment Analysis: By Technology

3D and 4D Ultrasound Segment in Canada Ultrasound Devices Market

The 3D and 4D ultrasound segment dominates the Canada ultrasound devices market, commanding approximately 46% of the market share in 2024. This significant market position is attributed to the superior visualization capabilities these systems offer, particularly in fetal imaging and cardiac applications. The technology allows for enhanced visualization of fetal heart structures through virtual planes, potentially increasing defect detection rates compared to traditional 2D imaging. Healthcare providers across Canada are increasingly adopting these advanced imaging systems due to their ability to provide detailed volumetric imaging and real-time movement visualization, particularly beneficial in complex diagnostic procedures and maternal-fetal medicine.

High-intensity Focused Ultrasound Segment in Canada Ultrasound Devices Market

The high-intensity focused ultrasound (HIFU) segment is emerging as the fastest-growing technology segment in the Canadian ultrasound devices market, projected to grow at approximately 7% CAGR from 2024 to 2029. This growth is primarily driven by its increasing adoption in non-invasive tumor treatment applications, particularly in treating solid tumors and uterine fibroids. The technology's precision in tissue ablation and its effectiveness in treating both primary and metastatic tumors have made it an attractive option for healthcare providers. Research institutions in Canada, including the University of Waterloo, are actively investigating HIFU applications in cancer treatment at the cellular level, which is expected to further drive innovation and adoption in this segment.

Remaining Segments in Technology

The 2D ultrasound and Doppler imaging segments continue to play vital roles in the Canadian ultrasound devices market. 2D ultrasound maintains its position as a fundamental imaging technology, particularly valued for its reliability in routine diagnostic procedures and point-of-care applications. Doppler imaging, with its specialized capability in blood flow visualization and measurement, remains crucial for cardiovascular diagnostics and vascular studies. Both technologies continue to evolve with improvements in image quality and processing capabilities, serving as essential tools in various clinical settings from emergency departments to specialized cardiac care units.

Segment Analysis: By Type

Stationary Ultrasounds Segment in Canada Ultrasound Devices Market

Stationary ultrasound systems continue to dominate the Canadian ultrasound devices market, holding approximately 70% of the total market share in 2024. The significant market position of stationary ultrasound systems can be attributed to their widespread adoption in hospitals, clinics, and diagnostic centers across Canada. These systems offer superior image quality and advanced configurations tailored to specific applications like cardiovascular, echocardiography, vascular, and OB/GYN studies. The increasing healthcare expenditure directed towards sophisticated ultrasound equipment and the high prevalence of chronic diseases across all age groups, particularly among the aging population, has sustained the demand for stationary ultrasound devices. Additionally, the continuous technological advancements in stationary systems, offering enhanced imaging capabilities and improved diagnostic accuracy, have further strengthened their market position in Canadian healthcare facilities.

Portable Ultrasounds Segment in Canada Ultrasound Devices Market

The portable ultrasound segment is experiencing robust growth in the Canadian market, projected to grow at approximately 7% during the forecast period 2024-2029. This accelerated growth is driven by several key factors, including the increasing demand for point-of-care diagnostics, particularly for the growing geriatric population requiring at-home care services. The segment's expansion is further supported by technological advancements in portable devices, offering improved image quality and functionality while maintaining mobility. These devices have become increasingly valuable in emergency medicine, remote healthcare settings, and bedside diagnostics, eliminating the need for patient transfer to radiology departments. The adoption of portable ultrasound devices has been particularly notable in rural and remote areas of Canada, where they serve as crucial diagnostic tools in primary healthcare settings. The segment's growth is also bolstered by the rising awareness about the availability and benefits of portable ultrasound devices among healthcare providers and the increasing integration of these devices in various medical specialties.

Ultrasound Devices Industry Overview

Top Companies in Canada Ultrasound Devices Market

The Canadian ultrasound devices market features prominent global players, including Fujifilm Holdings, Canon Medical Canada, GE Healthcare, Philips Healthcare, Samsung Medison, and Siemens Healthineers. These companies demonstrate a strong commitment to product innovation through the continuous development of advanced imaging technologies, particularly in 3D/4D imaging and AI integration. Strategic partnerships with healthcare providers and research institutions remain central to market penetration, while operational agility is enhanced through localized service networks and customized solutions for different clinical applications. Companies are increasingly focusing on portable and point-of-care ultrasound solutions, reflecting the growing demand for flexible diagnostic capabilities. The competitive landscape is characterized by substantial investments in research and development, with an emphasis on developing specialized applications for various medical specialties and improving workflow efficiency through digital integration.

Global Leaders Dominate Canadian Ultrasound Market

The Canadian ultrasound market share exhibits a highly consolidated structure dominated by multinational medical technology conglomerates with an established global presence and comprehensive product portfolios. These major players leverage their extensive research capabilities, established distribution networks, and strong brand recognition to maintain their market positions. The market demonstrates significant barriers to entry due to high technological requirements, stringent regulatory standards, and the need for substantial capital investments in research and development. Local companies primarily operate as distributors or specialized service providers, partnering with global manufacturers to enhance market reach.

The market is characterized by strategic acquisitions and partnerships aimed at expanding product portfolios and strengthening technological capabilities. Companies are increasingly focusing on vertical integration strategies to maintain control over their supply chains and enhance operational efficiency. Cross-border collaborations and technology transfers play a crucial role in market dynamics, with established players actively seeking partnerships with innovative startups and research institutions to accelerate product development and market expansion. The competitive environment encourages continuous innovation and service improvement to maintain market relevance and meet evolving healthcare needs.

Innovation and Service Excellence Drive Success

Success in the Canadian ultrasound devices market increasingly depends on companies' ability to deliver comprehensive solutions that combine advanced imaging capabilities with enhanced workflow efficiency and cost-effectiveness. Market leaders are focusing on developing integrated platforms that offer seamless connectivity, artificial intelligence-driven diagnostics, and improved user experience. The ability to provide specialized applications for different medical specialties while maintaining system versatility has become crucial for market success. Companies must also demonstrate strong after-sales support, training programs, and technical assistance to build long-term relationships with healthcare providers.

Future market success will be determined by companies' ability to adapt to evolving healthcare delivery models and changing customer preferences. Key factors include the development of portable and point-of-care solutions, integration with hospital information systems, and the ability to provide value-based healthcare solutions. Regulatory compliance and quality assurance remain critical considerations, particularly as healthcare providers increasingly focus on patient safety and clinical outcomes. Companies must also address growing concerns about cybersecurity and data privacy while maintaining system reliability and performance. The ability to provide comprehensive training and education programs for healthcare professionals will continue to be a significant differentiator in the market.

Ultrasound Devices Market Leaders

-

GE Healthcare

-

Fujifilm Holdings Corporation

-

Canon Medical Systems

-

Koninklijke Philips N.V.

-

Hologic Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Ultrasound Devices Market News

- In March 2023, the University of Western Ontario developed AI-powered bedside lung ultrasound in Canada. Point-of-care lung ultrasound, performed right at the bedside, can be life-saving for critically ill patients. It can help diagnose several medical conditions, such as congestive heart failure, pneumonia, pleural effusion, and pneumothorax, much faster than traditional methods and with little discomfort to the patient.

- In June 2022, the University of Alberta and the Department of Radiology and Diagnostic Imaging collaborated to develop three-dimensional images to aid further in the detection of dental disease.

Ultrasound Devices Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Technological Advancements and Increasing Number of Healthcare Providers

- 4.2.2 Increasing Incidences of Chronic Diseases

-

4.3 Market Restraints

- 4.3.1 Strict Regulations

- 4.3.2 Lack of Skilled Labor to Handle the Advanced Equipment

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

-

5.1 By Application

- 5.1.1 Anesthesiology

- 5.1.2 Cardiology

- 5.1.3 Gynecology/Obstetrics

- 5.1.4 Musculoskeletal

- 5.1.5 Radiology

- 5.1.6 Critical Care

- 5.1.7 Other Applications

-

5.2 By Technology

- 5.2.1 2D Ultrasound Imaging

- 5.2.2 3D and 4D Ultrasound Imaging

- 5.2.3 Doppler Imaging

- 5.2.4 High-intensity Focused Ultrasound

-

5.3 By Type

- 5.3.1 Stationary Ultrasound

- 5.3.2 Portable Ultrasound

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Canon Medical Systems Corporation

- 6.1.2 Fujifilm Holdings Corporation

- 6.1.3 GE Healthcare

- 6.1.4 Koninklijke Philips NV

- 6.1.5 Siemens Healthineers

- 6.1.6 Carestream Health Inc.

- 6.1.7 Samsung Electronics Co. Ltd

- 6.1.8 Hologic Inc.

- 6.1.9 Mindray Medical International Limited

- 6.1.10 Esaote SpA

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Ultrasound Devices Industry Segmentation

As per the scope of the report, a diagnostic ultrasound, also known as sonography, is an imaging technique that uses high-frequency sound waves to produce images of the different structures inside the body. They are being utilized to assess various conditions in the kidney, liver, and other abdominal disorders. They are also majorly used in chronic diseases, including heart disease, asthma, cancer, and diabetes. Canada Ultrasound Devices Market is Segmented by Application (Anesthesiology, Cardiology, Gynecology/Obstetrics, Musculoskeletal, Radiology, Critical Care, and Other Applications), Technology (2D Ultrasound Imaging, 3D and 4D Ultrasound Imaging, Doppler Imaging, and High-intensity Focused Ultrasound), Type (Stationary Ultrasound and Portable Ultrasound). The report offers the value (in USD million) for the above segments.

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology/Obstetrics | |

| Musculoskeletal | |

| Radiology | |

| Critical Care | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D and 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-intensity Focused Ultrasound | |

| By Type | Stationary Ultrasound |

| Portable Ultrasound |

Need A Different Region or Segment?

Customize Now

Ultrasound Devices Market Research FAQs

What is the current Canada Ultrasound Devices Market size?

The Canada Ultrasound Devices Market is projected to register a CAGR of 6.20% during the forecast period (2025-2030)

Who are the key players in Canada Ultrasound Devices Market?

GE Healthcare, Fujifilm Holdings Corporation, Canon Medical Systems, Koninklijke Philips N.V. and Hologic Inc. are the major companies operating in the Canada Ultrasound Devices Market.

What years does this Canada Ultrasound Devices Market cover?

The report covers the Canada Ultrasound Devices Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Canada Ultrasound Devices Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Canada Ultrasound Devices Market Research

Mordor Intelligence provides a comprehensive analysis of the Canada ultrasound devices industry, utilizing our extensive expertise in healthcare technology research. Our detailed report explores the full range of ultrasound devices and medical ultrasound technologies. This includes sonography devices and specialized equipment like dental ultrasonic systems. The analysis covers major industry players, such as Canon Medical Canada, and offers detailed insights into various ultrasound equipment segments within the Canadian healthcare sector.

This authoritative report, available as an easy-to-download PDF, offers stakeholders crucial insights into the expanding size of the ultrasound market and emerging opportunities. Our analysis assists healthcare providers, manufacturers, and investors in understanding current industry dynamics and future growth potential in the Canadian market. The report examines technological advancements, regulatory frameworks, and competitive landscapes. It provides actionable intelligence for strategic decision-making in the medical ultrasound sector. Stakeholders gain access to comprehensive data on market dynamics, investment opportunities, and technological innovations shaping the industry's future.