Market Size of Canada Spinal Surgery Devices Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

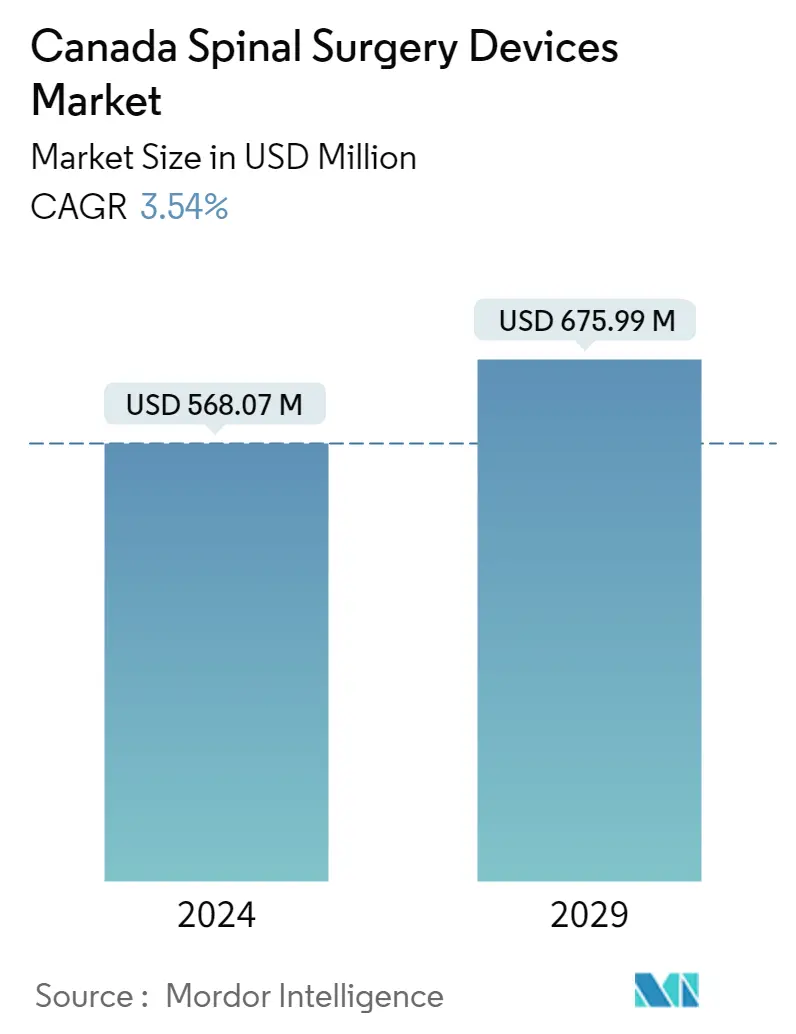

| Market Size (2024) | USD 568.07 Million |

| Market Size (2029) | USD 675.99 Million |

| CAGR (2024 - 2029) | 3.54 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Canada Spinal Surgery Devices Market Analysis

The Canada Spinal Surgery Devices Market size is estimated at USD 568.07 million in 2024, and is expected to reach USD 675.99 million by 2029, growing at a CAGR of 3.54% during the forecast period (2024-2029).

COVID-19 significantly impacted the Canadian spinal surgery devices market in the initial phases, as many surgeries got delayed due to the COVID-19-related lockdowns. Studies showed that while wait times improved over the pandemic period, elective surgeries were delayed, which resulted in longer wait times as health systems prioritized urgent procedures during the pandemic. However, the sector has been recovering significantly in the post-pandemic scenario. Over the last two years, the market recovery has been led by increased spinal deformities, new product launches, and increased demand for spinal surgery devices.

Advancements in technology in spinal surgery equipment, a rise in the aging and obese population with a growing number of spinal deformities, and increasing demand for non-invasive spinal surgery procedures are key elements driving the market growth. For instance,

- As per the World Obesity Atlas 2022, the estimated percentage of adults having obesity in Canada is expected to reach 38.5% in 2030.

- Furthermore, according to the Statistics Canada report, between 2016 and 2021, the number of people aged 85 and older grew by 12%, which was more than twice as high as the growth seen for the overall Canadian population (+5.2%). The geriatric population is more prone to undergo spinal surgeries.

Thus increase in the geriatric population is likely to boost the market growth during the forecast period.

Additionally, the presence of competitors, mergers, research collaborations, and acquisitions boosts market growth as these factors are likely to increase product availability and competition. For instance, in 2021, London-based startup A-Line Orthopaedics, in collaboration with Ontario-based Western University, developed a new spinal implant that could transform an invasive treatment for upper cervical spine fractures.

Thus, due to the rise in the number of technological advances in spinal surgery, and the increase in incidences of obesity and degenerative spinal conditions, the Canada spinal surgery market is anticipated to witness growth over the forecast period. However, the high surgery cost and regulatory restrictions hinder the market growth.

Canada Spinal Surgery Devices Industry Segmentation

As per the scope of the report, spinal surgery devices are devices used to treat spinal injuries or deformities. They help restructure or realign the spine. Generally, spinal surgery is an open procedure in which an extensive incision allows the surgeon to examine the structure of the spine.

The Canadian spinal surgery devices market is segmented by Device Type (Spinal Decompression (Corpectomy, Discectomy, Facetectomy, Foraminotomy, Laminotomy), Spinal Fusion (Cervical Fusion, Interbody Fusion, Thoracolumbar Fusion, Other Device Types), Fracture Repair Devices, Arthroplasty Devices, and Non-fusion Devices). The report offers the value in USD million for the above segments.

| By Device Type | |||||||

| |||||||

| |||||||

| Fracture Repair Devices | |||||||

| Arthroplasty Devices | |||||||

| Non-fusion Devices |

Canada Spinal Surgery Devices Market Size Summary

The Canadian spinal surgery devices market is poised for growth, driven by advancements in technology and an increasing demand for non-invasive procedures. The market has shown resilience in the post-pandemic period, recovering from the delays caused by COVID-19 lockdowns. Key factors contributing to this growth include the rise in spinal deformities, an aging and obese population, and the demand for innovative surgical solutions. The market is characterized by the presence of major players such as Zimmer Biomet, Stryker Corporation, Johnson & Johnson, Medtronic PLC, and Globus Medical, who are actively engaging in mergers, acquisitions, and research collaborations to enhance product offerings and market share. Technological advancements, such as the development of new spinal implants and robotic-assisted surgery platforms, are further propelling the market forward.

The thoracolumbar fusion and arthroplasty devices segments are expected to witness significant growth due to the increasing incidence of degenerative spinal conditions and joint defects. The high cost of surgeries and regulatory challenges pose hurdles, but the ongoing research and development, coupled with increased healthcare spending, are likely to drive market expansion. The market's competitive landscape is marked by strategic partnerships and product launches, which are enhancing the availability and adoption of advanced spinal surgery devices. As healthcare expenditure continues to rise, supported by government funding, the market is anticipated to experience sustained growth, with a focus on improving patient outcomes and operational efficiencies in surgical procedures.

Canada Spinal Surgery Devices Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Increasing Number of Technological Advances in Spinal Surgery

-

1.2.2 Increasing Incidences of Obesity and Degenerative Spinal Conditions

-

-

1.3 Market Restraints

-

1.3.1 Expensive Treatment Procedures

-

1.3.2 Stringent Reimbursement Concerns

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD million)

-

2.1 By Device Type

-

2.1.1 Spinal Decompression

-

2.1.1.1 Corpectomy

-

2.1.1.2 Discectomy

-

2.1.1.3 Facetectomy

-

2.1.1.4 Foraminotomy

-

2.1.1.5 Laminotomy

-

-

2.1.2 Spinal Fusion

-

2.1.2.1 Cervical Fusion

-

2.1.2.2 Interbody Fusion

-

2.1.2.3 Thoracolumbar Fusion

-

2.1.2.4 Other Device Types

-

-

2.1.3 Fracture Repair Devices

-

2.1.4 Arthroplasty Devices

-

2.1.5 Non-fusion Devices

-

-

Canada Spinal Surgery Devices Market Size FAQs

How big is the Canada Spinal Surgery Devices Market?

The Canada Spinal Surgery Devices Market size is expected to reach USD 568.07 million in 2024 and grow at a CAGR of 3.54% to reach USD 675.99 million by 2029.

What is the current Canada Spinal Surgery Devices Market size?

In 2024, the Canada Spinal Surgery Devices Market size is expected to reach USD 568.07 million.