Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

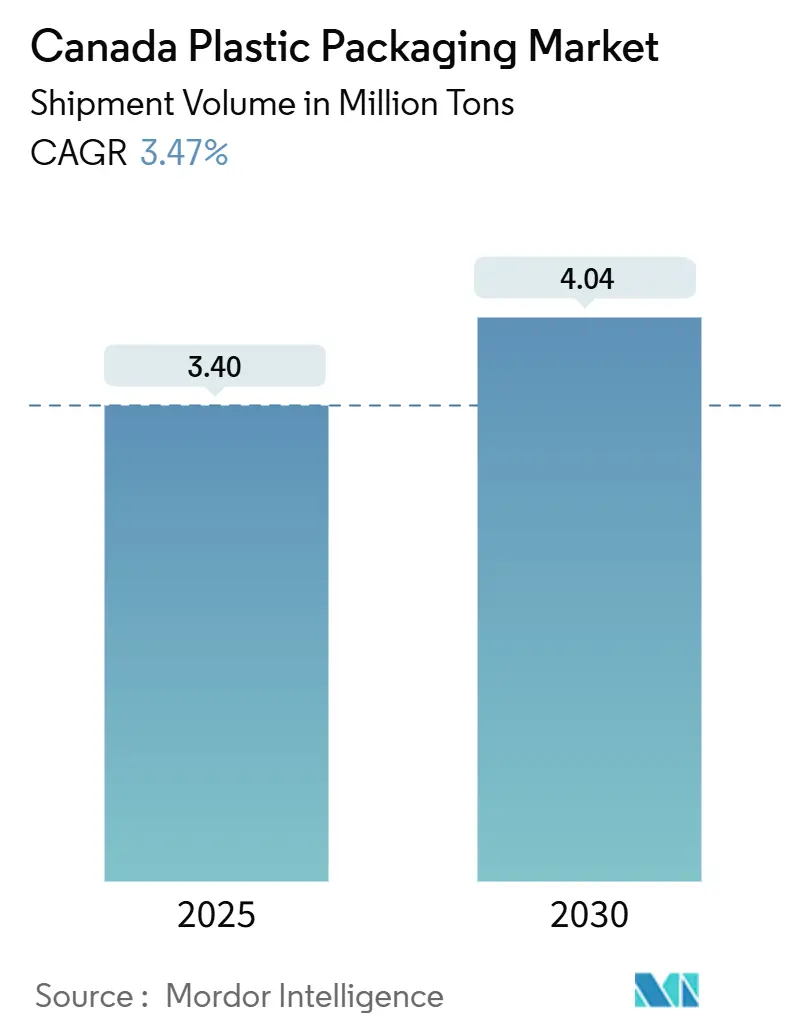

| Market Volume (2025) | 3.40 Million tons |

| Market Volume (2030) | 4.04 Million tons |

| Growth Rate (2025 - 2030) | 3.47% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Plastic Packaging Market Analysis by Mordor Intelligence

The Canada plastic packaging market size stands at 3.40 million tons in 2025 and is forecast to reach 4.04 million tons by 2030, translating into a 3.47% CAGR over the period. The rising demand for convenience foods, the rapid expansion of e-commerce, and regulatory moves favoring recyclable polymers collectively underpin this growth trajectory. Provincial EPR programs are accelerating investments in design for recycling, while smart packaging pilots in pharmaceuticals and perishables signal a growing interest in value-added formats. At the same time, large-scale M&A activity is reshaping supplier power, and volatility in petro-feedstock prices remains a headline risk that can squeeze converter margins.

Key Report Takeaways

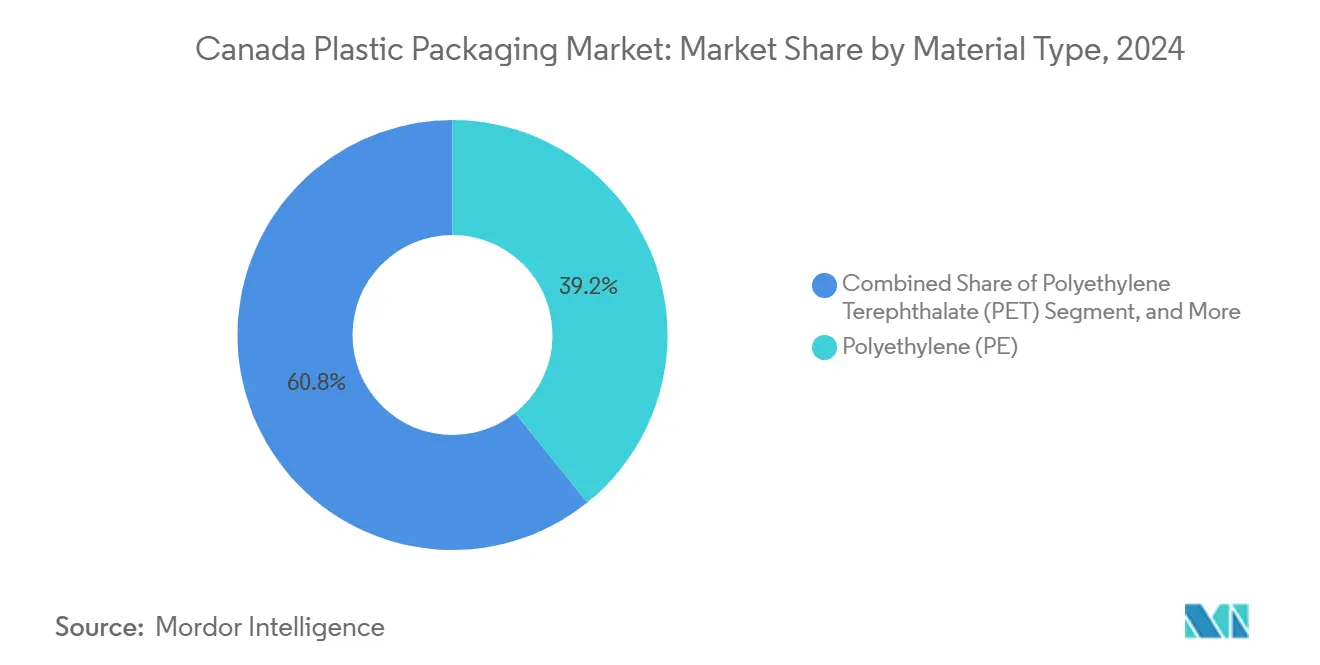

- By material type, polyethylene led with 39.21% of Canada's plastic packaging market share in 2024, and polyethylene terephthalate is projected to expand at a 5.32% CAGR through 2030.

- By packaging type, flexible formats accounted for 57.86% of the Canada plastic packaging market size in 2024, rigid formats are forecast to grow at a 4.75% CAGR between 2025-2030.

- By product form, pouches and sachets held 35.32% share of the Canada plastic packaging market size in 2024, films and wraps are advancing at a 4.93% CAGR through 2030.

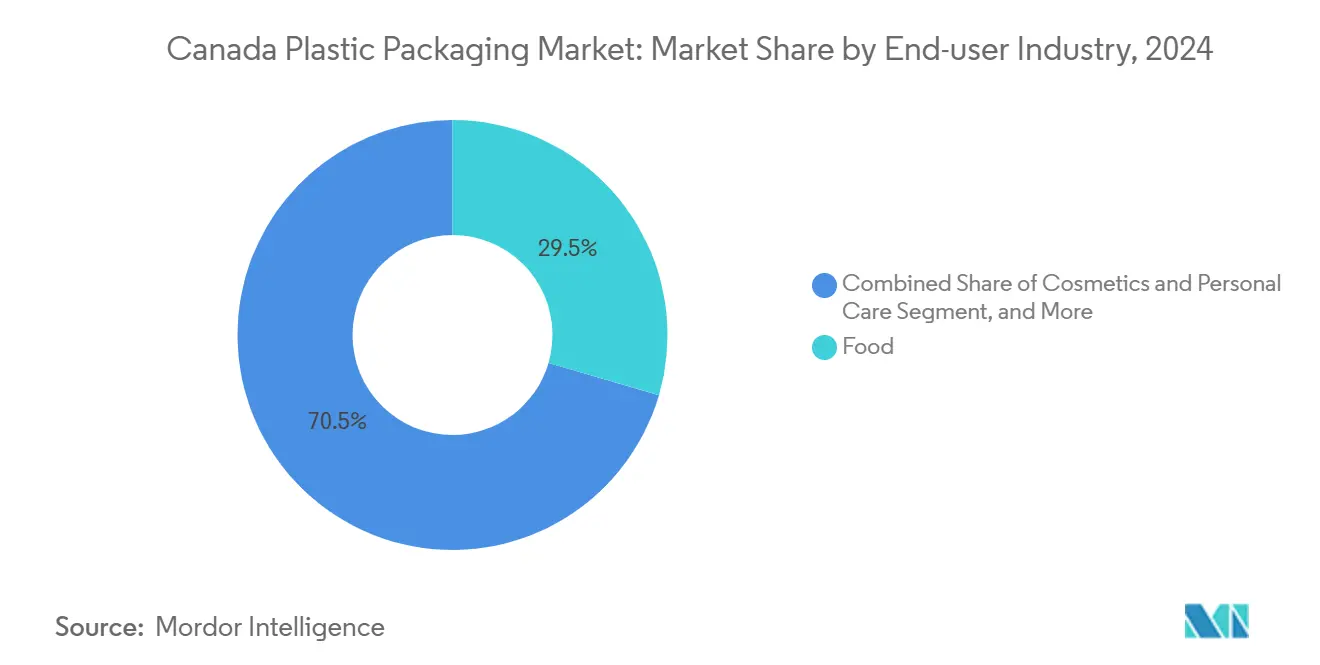

- By end-user industry, food applications represented 29.52% of Canada's plastic packaging market share in 2024, while cosmetics and personal care record the highest projected CAGR at 5.01% through 2030.

- By manufacturing process, extrusion captured 28.32% share of the Canada plastic packaging market size in 2024, whereas thermoforming rises at a 5.62% CAGR to 2030.

Canada Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand from food and beverage industry for convenience packaging | +1.2% | National, concentrated in Ontario and Quebec processing centers | Medium term (2-4 years) |

| Rising e-commerce shipments requiring lightweight protective packaging | +0.8% | National, with early gains in Toronto, Montreal, Vancouver metropolitan areas | Short term (≤ 2 years) |

| Technological advancements in recyclable and bio-based plastics | +0.6% | Ontario innovation clusters, Quebec research centers, BC sustainability initiatives | Long term (≥ 4 years) |

| Provincial EPR harmonization prompting packaging redesign | +0.9% | Ontario, Quebec, Nova Scotia leading implementation | Medium term (2-4 years) |

| Growth of cannabis product packaging with strict compliance needs | +0.4% | National, with concentration in licensed production facilities | Short term (≤ 2 years) |

| Smart packaging adoption for pharma cold-chain monitoring | +0.3% | National pharmaceutical distribution networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand from Food and Beverage Industry for Convenience Packaging

Food processors continue shifting toward portion-controlled and ready-to-eat formats that rely on barrier films and pouches to extend shelf life and reduce waste. Statistics Canada reported that 30.4% of the nation’s plastic consumption in 2024 originated in food applications.[1]Statistics Canada, “Enquête sur l'industrie de la gestion des déchets : réacheminement des déchets, 2022,” statcan.gc.caProducers in Quebec alone shipped CAD 7.8 billion (USD 6.0 billion) of plastic packaging during 2024, demonstrating the scale of this driver. Modified-atmosphere solutions adopted by protein processors in Ontario illustrate how performance requirements keep polyethylene in a leading position. These trends secure a stable demand base even as sustainability pressures mount, anchoring the Canada plastic packaging market.

Rising E-commerce Shipments Requiring Lightweight Protective Packaging

Online retail volumes remain elevated compared with pre-pandemic baselines, and parcel carriers favor lightweight materials that minimize dimensional weight charges. Flexible mailer pouches, padded films, and bubble wraps enable merchants to optimize freight costs across Canada’s long supply chains. Converters emphasize digital printing for brand differentiation during unboxing, an increasingly important marketing touchpoint. E-commerce therefore amplifies demand for materials that balance durability with minimal mass, supporting volume gains in films and wraps across the Canada plastic packaging market.

Technological Advancements in Recyclable and Bio-based Plastics

Universities and resin producers are accelerating R&D on mono-material films, advanced recycling, and bio-polymer blends. NOVA Chemicals opened its Centre of Excellence for Plastics Circularity in Calgary in June 2024, focusing on chemical recycling pathways for polyethylene. The University of Guelph’s seaweed-based resin program secured federal grants in February 2024, aiming at compost-ready food pouches. Continuous material innovation tightens the gap between sustainability mandates and functional performance, enabling converters to meet EPR targets without sacrificing barrier properties.

Provincial EPR Harmonization Prompting Packaging Redesign

Ontario’s Blue Box transition moved 130 communities to producer responsibility by March 2024, with Circular Materials forecasting national alignment by 2027. Quebec codified a broad EPR framework effective January 2025 that extends to industrial and institutional waste streams. Producers now face unified fee structures tied to recyclability and recycled content metrics. The new cost signals prompt lightweighting, color elimination, and mono-material redesign, accelerating sustainable innovation across the Canada plastic packaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal single-use plastics ban increasing regulatory uncertainty | -0.7% | National implementation with provincial variation in enforcement | Short term (≤ 2 years) |

| Volatility in petro-feedstock prices | -0.5% | National, with particular impact on Alberta petrochemical clusters | Medium term (2-4 years) |

| Limited domestic recycling capacity for rPET feedstock | -0.4% | National, concentrated in Ontario and Quebec processing centers | Medium term (2-4 years) |

| Retailer-led reusable packaging pilots reducing single-use demand | -0.3% | National retail chains, urban centers leading adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal Single-use Plastics Ban Increasing Regulatory Uncertainty

The December 2023 federal court ruling that questioned plastic toxicity classifications introduced legal ambiguity, yet the Single-use Plastics Prohibition Regulations remain active pending appeal. Retailers and quick-service outlets are testing fiber and bio-resin substitutes while converters weigh capital allocation for new lines. Divergent provincial enforcement adds complexity for national brands. This policy backdrop tempers near-term demand for legacy checkout bags and cutlery, pressuring volumes in certain low-margin categories within the Canada plastic packaging market.

Volatility in Petro-feedstock Prices

Polyethylene and polypropylene resin prices tracked Brent crude swings and logistic bottlenecks through 2024-2025, squeezing converter spreads. Statistics Canada recorded 5.2% year-over-year inflation in packaging materials by January 2025. Alberta’s ethane-derived resin cluster faces added exposure to export tariffs introduced by the United States in March 2025, covering USD 14.9 billion of Canadian plastics exports. Margin compression can slow investment in new capacity, restricting supply responsiveness in the Canada plastic packaging market.

Segment Analysis

By Material Type: Polyethylene Retains Scale as PET Accelerates

Polyethylene held 39.21% of Canada plastic packaging market share in 2024, a position anchored in its versatility across films, bags, and rigid containers. Converter familiarity with PE, coupled with well-established mechanical recycling streams, sustains high volume usage. The segment also benefits from investment in chemical recycling pilot plants that target post-consumer PE waste, aligning with provincial EPR performance metrics. Meanwhile, polyethylene terephthalate expands at a 5.32% CAGR through 2030, underpinned by beverage bottlers’ shift to lighter PET preforms and bottle-to-bottle recycling initiatives that leverage growing rPET pellet capacity in Ontario and Quebec. The Canada plastic packaging market size tied to PET is therefore poised for above-average growth as deposit return expansions unlock clean feedstock streams. Polypropylene maintains relevance in closure and rigid tub applications, while polystyrene contracts under municipal bans targeting foam service ware. Bio-resin adoption remains nascent but earns attention for compost-ready coffee pod lids and produce containers, signaling future diversification in the Canada plastic packaging market.

The competitive landscape within materials is further shaped by resin price volatility and carbon accounting pressures. Converters source recycled PE and rPET to meet brand owner mandates for 30% post-consumer content in retail packaging by 2030. Such procurement dynamics can widen the cost gap between polymers, influencing substitution patterns. Resin suppliers are responding through mass-balance certified grades that carry lower scope 3 emissions, a factor increasingly weighted in retail tender processes.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Packaging Type: Flexible Solutions Dominate as Rigid Formats Reposition

Flexible formats captured 57.86% of the Canada plastic packaging market size in 2024, reflecting advantageous product-to-package ratios that drive freight savings. Multi-layer films with EVOH or metallized barrier layers lengthen shelf life for meats, cheeses, and ready meals, thereby supporting retailer food waste reduction pledges. Brand owners also leverage stand-up pouches to differentiate in crowded center-store aisles, with resealable closures enhancing user convenience. Regulatory scrutiny of multi-material laminates, however, pushes converters toward polyolefin-only structures compatible with existing film recycling streams.

Rigid packaging maintains robust demand in segments where structural integrity is paramount, such as carbonated soft drinks, household cleaners, and OTC pharmaceuticals. Light-weighting breakthroughs enable HDPE bottle weight cuts of 18% over legacy designs, mitigating resin cost inflation. Deposit return programs in British Columbia and Alberta lift PET bottle recovery rates above 80%, improving rPET availability and lowering lifecycle emissions. The Canada plastic packaging market therefore features a dynamic interplay where rigid suppliers innovate to preserve share while flexible formats continue to proliferate.

By Product Form: Pouches Lead and Films Gain Momentum

Pouches and sachets secured 35.32% share of the Canada plastic packaging market size in 2024, buoyed by snack-food category expansion and consumer affinity for portable single-serve formats. High-definition flexographic printing enhances shelf impact, and degassing valves enable growth in specialty coffee applications. E-commerce further amplifies pouch use due to puncture resistance and minimal void space. Films and wraps experience the highest CAGR at 4.93% through 2030 as warehouse automation and pallet unitization protocols standardize the use of thinner high-stretch films that cut material usage by up to 22%. Supply chain stakeholders also favor recyclable collation shrink over paperboard for efficiency, reinforcing demand momentum in the Canada plastic packaging market.

Bottles and jars retain indispensability in beverages and personal care, especially where tactile cues and resealability affect brand perception. Tray and container volumes rise with ready-meal popularity, leveraging microwave-safe CPET structures. Bag and sack applications span produce, fertilizers, and industrial products, but face pressure from provincial levies on non-reusable grocery bags, prompting thicker multilayer options qualifying as reusable under regulation.

By End-User Industry: Food Dominates, Cosmetics Accelerate

Food applications absorbed 29.52% of Canada plastic packaging market share in 2024, reflecting fundamental needs for product protection and compliance with CFIA labeling rules. Barrier film advances permit protein processors to extend chilled shelf life by up to eight days, reducing retailer shrink. Modified atmosphere technology adoption in fresh produce further cements plastics’ role in waste mitigation strategies. Beverage packaging remains a major sub-segment, with bottle redesign campaigns trimming PET gram weights and incorporating 100% rPET in premium water brands.

Cosmetics and personal care register a 5.01% CAGR to 2030, driven by demand for premium tactile finishes, airless pumps, and travel-size SKUs. Brand owners integrate ocean-bound recycled polymers to bolster ESG credentials, and refill-ready jar systems gain traction among boutique labels. Pharmaceutical demand for child-resistant closures, anti-counterfeit features, and cold-chain monitoring fosters incremental growth, while industrial markets consume heavy-duty sacks, IBC liners, and protective wrap, offering stable though lower-margin volumes inside the Canada plastic packaging market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Manufacturing Process: Extrusion Holds Scale while Thermoforming Outpaces

Extrusion accounted for 28.32% of Canada plastic packaging market share in 2024 through its efficiency in high-volume film, sheet, and profile production. Multi-layer co-extrusion enables oxygen barrier incorporation without adhesive tie layers, simplifying recycling. Process versatility allows converters to run recycled pellet blends up to 35% without compromising optical clarity, suiting EPR fee structures tied to recycled content.

Thermoforming posts a 5.62% CAGR, reflecting demand for lightweight rigid containers in dairy, bakery, and ready-meal categories. Thin-gauge PET and PP roll stock are thermoformed into clamshells and portion trays that align with deposit return streams. Injection molding retains a foothold in caps, closures, and personalized medicine dispensers, while blow molding remains synonymous with beverage and household chemical bottles. Process selection in the Canada plastic packaging market increasingly hinges on life-cycle assessments and the ability to accommodate recycled feedstock without mechanical property loss.

Geography Analysis

Ontario and Quebec together contribute roughly 76% of the Canada plastic packaging market, mirroring their population density, food processing clusters, and transportation links to U.S. customers. Ontario alone accounted for 62% of Canadian plastic waste exports in 2021, underscoring its role as both production hub and waste generator.[2]Sophie Bernard, Florence Lapointe, and Julien Martin, “Where does our plastic waste go” CIRANO, cirano.qc.ca Provincial policy such as the Blue Box overhaul is redirecting material flows toward domestic re-processing, a shift expected to boost local demand for recycled resin in the near term.

Quebec hosts more than 420 plastics establishments employing 21,000 workers, generating CAD 7.8 billion (USD 6.0 billion) in shipments during 2024.[3]Gouvernement du Québec, “Aperçu de l'industrie de la plasturgie,” economie.gouv.qc.ca Its comprehensive EPR program, effective 2025, extends producer fees across commercial streams, incentivizing rapid packaging redesign. British Columbia’s Recycle BC model demonstrates how mandatory stewardship can achieve 95% local processing of collected residential plastics, though the province’s export share dipped to 5% by 2021, reflecting reduced manufacturing scale.

Alberta offers feedstock cost advantages due to ethane and propane availability, yet new U.S. tariffs on Canadian plastics heighten market uncertainty for its export-oriented output. Atlantic provinces remain small but exhibit above-average growth rates as seafood processors seek high-barrier vacuum pouches to safeguard product freshness during trans-Atlantic shipping. Overall, regional variations in policy, feedstock access, and end-market proximity determine growth pockets within the Canada plastic packaging market.

Competitive Landscape

Industry consolidation intensified through 2024 as Amcor agreed to acquire Berry Global for USD 8.4 billion, creating a global powerhouse with expanded Canadian reach. Novolex closed its USD 6.7 billion purchase of Pactiv Evergreen in December 2024, backed by a USD 1 billion co-investment from Canada Pension Plan Investment Board. These moves elevate the combined market share of the top five suppliers toward 55%, tightening buyer options and accelerating technology diffusion.

Strategic focus areas include recycled content certification, mono-material laminate development, and smart sensor integration. ProAmpac’s March 2024 acquisition of Gelpac deepened its Canadian footprint in multiwall paper and woven poly sacks, underscoring interest in hybrid material portfolios. Cascades pursues a fiber-plastic blend strategy to hedge regulatory outcomes, while Winpak emphasizes proprietary co-extrusion for high-barrier lidding. Start-ups in Ontario’s innovation corridor target niche opportunities in cannabis compliance packaging and active freshness indicators. White-space persists in commercializing bio-polymer films at industrial scale, offering disruptor entry points into the Canada plastic packaging market.

Canada Plastic Packaging Industry Leaders

-

Amcor plc

-

Huhtamaki Oyj

-

Sealed Air Corporation

-

Winpak Ltd.

-

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2024: Novolex completed the USD 6.7 billion acquisition of Pactiv Evergreen, supported by Canada Pension Plan Investment Board.

- November 2024: Amcor announced a USD 8.4 billion deal to acquire Berry Global, expanding its North American presence.

- March 2024: ProAmpac acquired Quebec-based Gelpac, retaining local operations and reinforcing its Canadian network.

- March 2024: Ontario transitioned 130 municipalities to producer-led EPR under the Blue Box Regulation.

Canada Plastic Packaging Market Report Scope

Plastic packaging refers to containers, wraps, and materials made from plastic polymers used to protect, preserve, and transport goods. It includes bottles, bags, films, and trays made from PET, HDPE, PVC, LDPE, PP, and PS. These packaging solutions safeguard products, extend shelf life, and aid distribution. Plastic packaging is valued for its versatility, durability, and cost-effectiveness across industries. It serves multiple functions: product protection, contamination prevention, and marketing. However, environmental concerns related to waste management and pollution have led to an increased focus on developing sustainable plastic packaging options.

The Canada Plastic Packaging Market is segmented by type (flexible plastic packaging, rigid plastic packaging), by-products (bottles and jars, trays and containers, pouches, films & wraps, and other product types), and by end-user industry (food, beverage, healthcare, personal care and household and other end-user vertical), The report offers market forecasts and size in volume (tons) for all the above segments.

By Material Type

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Polystyrene and EPS |

| Other Material Types |

By Packaging Type

| Flexible Plastic Packaging |

| Rigid Plastic Packaging |

By Product Form

| Bottles and Jars |

| Trays and Containers |

| Pouches and Sachets |

| Bags and Sacks |

| Films and Wraps |

| Other Product Forms |

By End-User Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

By Manufacturing Process

| Extrusion |

| Injection Molding |

| Blow Molding |

| Thermoforming |

| By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polystyrene and EPS | |

| Other Material Types | |

| By Packaging Type | Flexible Plastic Packaging |

| Rigid Plastic Packaging | |

| By Product Form | Bottles and Jars |

| Trays and Containers | |

| Pouches and Sachets | |

| Bags and Sacks | |

| Films and Wraps | |

| Other Product Forms | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceuticals and Healthcare | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-user Industries | |

| By Manufacturing Process | Extrusion |

| Injection Molding | |

| Blow Molding | |

| Thermoforming |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Canada plastic packaging market in 2025?

The market totals 3.40 million tons in 2025 and is forecast to hit 4.04 million tons by 2030.

What is the current CAGR outlook for Canadian plastic packaging?

The compound annual growth rate stands at 3.47% for 2025-2030 based on prevailing demand and regulatory trends.

Which material leads packaging volumes across Canada?

Polyethylene remains the largest material, holding 39.21% share of total tonnage in 2024.

How are EPR regulations affecting packaging design?

Producer-funded collection fees tied to recyclability are pushing brands toward mono-material structures and higher recycled content.

What segment is growing fastest inside the market?

Polyethylene terephthalate shows the highest material CAGR at 5.32% through 2030, buoyed by beverage bottling and rPET adoption.

Which provinces dominate industry activity?

Ontario and Quebec together represent about 76% of the nation’s plastic packaging demand and production capacity.

Page last updated on: