Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

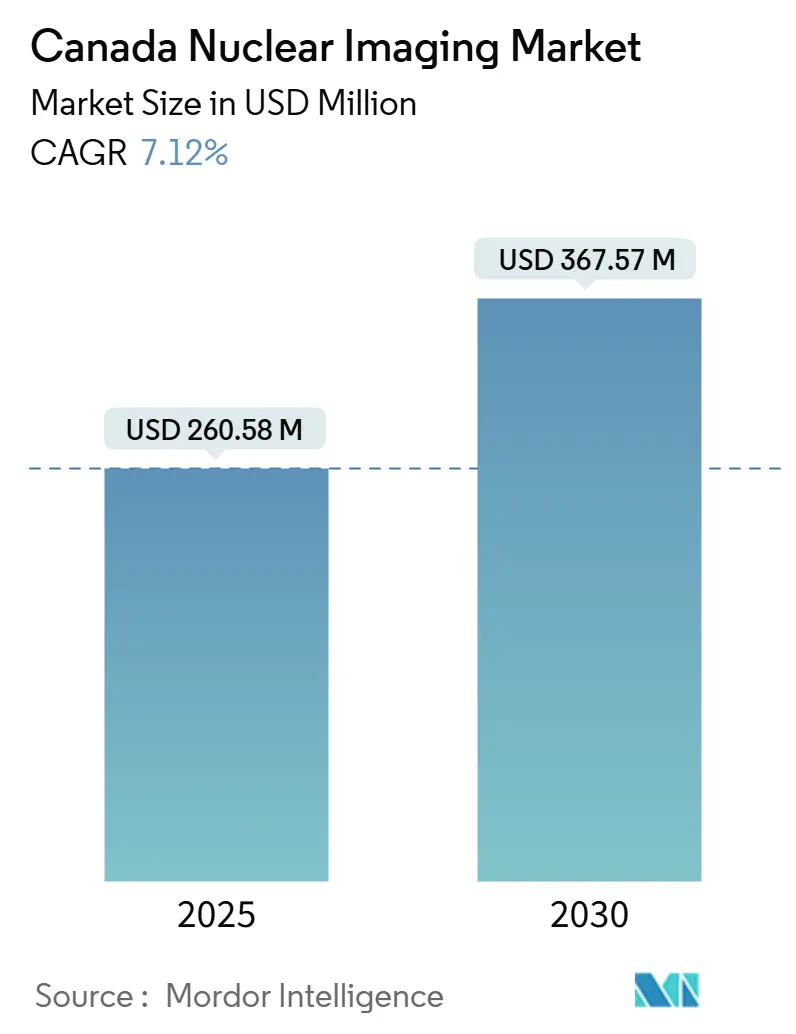

| Market Size (2025) | USD 260.58 Million |

| Market Size (2030) | USD 367.57 Million |

| Growth Rate (2025 - 2030) | 7.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Nuclear Imaging Market Analysis by Mordor Intelligence

The Canada nuclear imaging market size is valued at USD 260.58 billion in 2025 and is expected to reach USD 367.57 billion by 2030, advancing at a 7.12% CAGR over the forecast period. Federal funding for domestic molybdenum-99, the expansion of provincial cyclotron networks, and increasing adoption of hybrid PET/CT and SPECT/CT scanners underpin this steady growth. Equipment modernization cycles are shortening as hospitals retire aging gamma cameras in favor of faster, lower-dose platforms, while CADTH’s fast-track approval pathway accelerates market entry for novel radiotracers. Market participants also benefit from the government’s focus on reducing imaging wait times, especially for cardiovascular and oncology indications, creating consistent demand across public and private centers. Strategic acquisitions—most recently BWXT’s purchase of Kinectrics and Telix’s acquisition of ARTMS—signal investor confidence in Canada’s isotope ecosystem. Nevertheless, geographic service gaps in the North and persistent technologist shortages temper near-term capacity expansion.

Key Report Takeaways

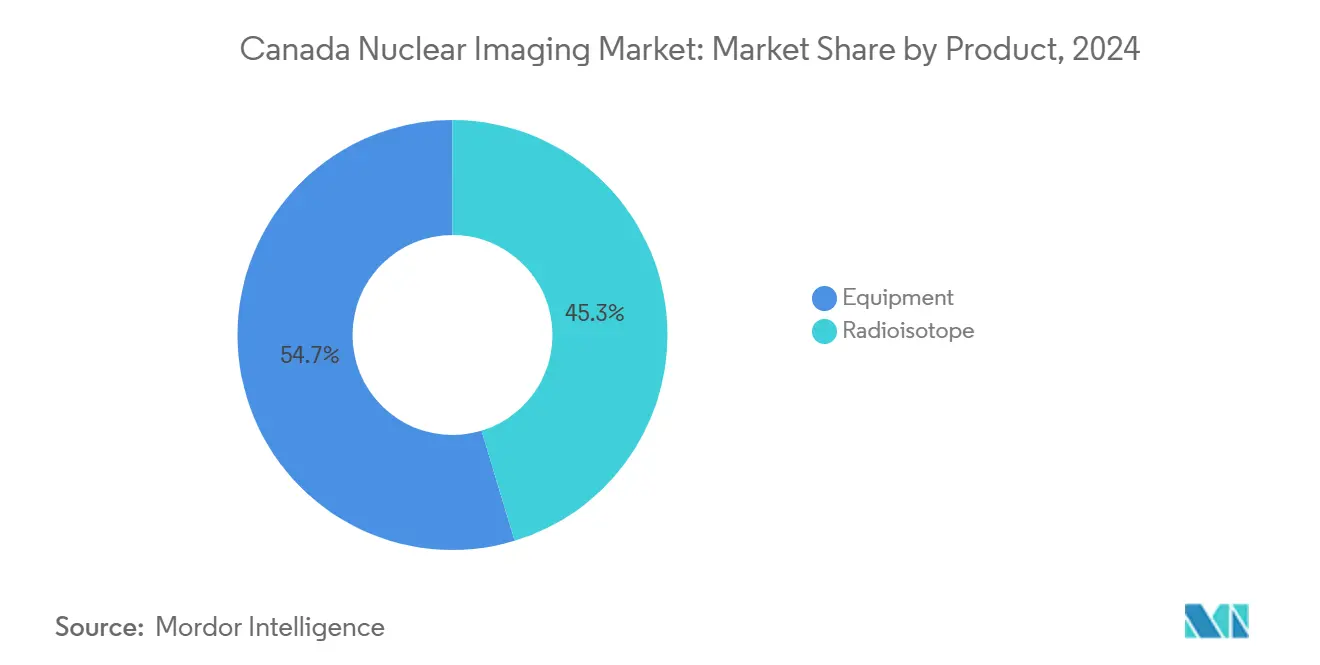

- By product category, equipment held 54.67% of the Canada nuclear imaging market share in 2024, radioisotopes are projected to expand at a 7.34% CAGR through 2030.

- By application, cardiology represented 38.89% of revenue in 2024; neurology applications are forecast to grow at 7.89% CAGR to 2030.

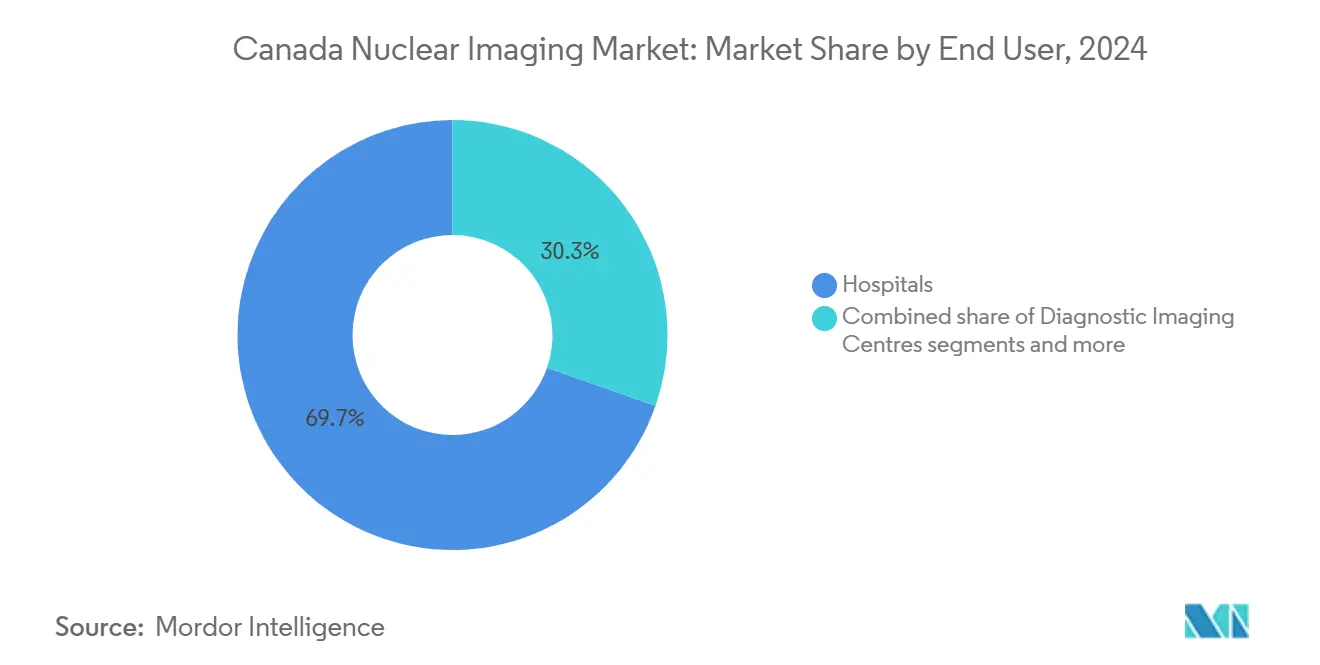

- By end user, hospitals commanded 69.67% of the Canada nuclear imaging market size in 2024, while diagnostic imaging centers are set to advance at an 8.01% CAGR between 2025-2030.

Canada Nuclear Imaging Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid PET/CT & SPECT/CT adoption | +1.8% | Ontario, British Columbia | Medium term (2-4 years) |

| Rising CVD & oncology prevalence | +2.1% | All provinces, higher in aging regions | Long term (≥ 4 years) |

| CADTH fast-track radiotracer approvals | +1.2% | National | Short term (≤ 2 years) |

| Public–private cyclotron build-out | +1.5% | Ontario, British Columbia, Alberta | Medium term (2-4 years) |

| AI-enabled dose-reduction software | +0.9% | Urban academic medical centers | Short term (≤ 2 years) |

| Federal funding for domestic Mo-99 | +1.3% | Ontario (Darlington), British Columbia (TRIUMF) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift to Hybrid PET/CT & SPECT/CT Scanners

Nationwide installations of hybrid systems climbed from 57 to 60 units in the past fiscal year, supporting 156,320 examinations, as clinicians increasingly demand fused functional and anatomic data for precise lesion localization. Siemens Healthineers’ Symbia Pro.specta integrates quantitative SPECT with CT attenuation correction, cutting scan times by up to 50% and enabling theranostics workflows. Provincial uptake is strongest in Ontario and Quebec, while Atlantic provinces struggle to finance upgrades. AI orchestration platforms such as the Rad AI-MIC Medical Imaging partnership reduce report turnaround and mitigate radiologist fatigue. Health Canada’s risk-based framework for AI medical devices balances safety with rapid clinical deployment, catalyzing further hybrid adoption.

Rising Prevalence of CVD & Oncology Cases

Cardiovascular disease remains Canada’s top mortality driver, and oncology incidence continues to rise, pushing nuclear cardiology and PET oncology referrals upward. Wait times for non-urgent myocardial perfusion scans vary widely—from 4 days in urban Ontario to 158 days in rural Saskatchewan—highlighting unmet demand. In January 2025, Cancer Care Ontario began reimbursing radioligand therapy for metastatic prostate cancer, linking diagnostic imaging more closely with therapeutic pathways. The London Health Sciences Centre’s first-in-Canada administration of actinium-225 DOTATATE underscores Canada’s leadership in alpha therapy research. Clinical trials like McGill’s LuMIERE study further integrate imaging and therapy, reinforcing long-term demand for sophisticated scanners and tracers.

CADTH Fast-Track Approvals for Novel Radiotracers

Health technology assessments now conclude in as little as 120 days, enabling quicker provincial listing of innovative agents. Health Canada approved Voranigo for Grade 2 astrocytoma under Priority Review in 2024, demonstrating the effectiveness of the accelerated track. Telix’s Illuccix label expansion reached market only six months after U.S. clearance, illustrating international regulatory harmonization. Research hubs at the University of Toronto and CAMH, funded with USD 3 million from Mitacs, shorten bench-to-bedside cycles for new tracers. Faster approvals stimulate domestic isotope output, supporting the Canada nuclear imaging market.

Growing Public-Private Cyclotron Capacity Build-Out

Over 50 nuclear pharmacies and several on-site cyclotrons operated by Jubilant Radiopharma exemplify the distributed production model now displacing legacy reactor supply chains. British Columbia committed CAD 50.5 million to a new BC Cancer cyclotron and radiopharmacy, while Darlington’s reactor will soon generate Mo-99 and Lu-177 at commercial scale. Indigenous partnerships, such as the Saugeen Ojibway Nation-Bruce Power lutetium-177 initiative, promote local economic development alongside isotope output. The Canadian Nuclear Safety Commission’s licensing regime maintains rigorous safety standards without stifling innovation.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short half-life isotope logistics in remote provinces | -1.4% | Northern territories, remote indigenous communities | Long term (≥ 4 years) |

| Capital-intensive replacement cycle of legacy gamma cameras | -0.8% | National, with higher impact in smaller hospitals | Medium term (2-4 years) |

| Limited reimbursement for theranostic procedures | -0.6% | Provincial variations, particularly Atlantic provinces | Short term (≤ 2 years) |

| Skilled-labour shortages in nuclear-medicine technologists | -1.1% | National, with acute shortages in rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short Half-Life Isotope Logistics in Remote Provinces

Technetium-99m’s six-hour half-life challenges distribution to northern hospitals that lie 1,200 km or more from cyclotron hubs. The Winnipeg Great-West Life PET/CT Center relies on charter flights and just-in-time scheduling to avoid canceled scans, inflating operational costs. Indigenous patients travel a median 268 km for radiotherapy, magnifying inequality. Although mobile imaging units reduce travel, weather and road conditions in winter months often ground outreach programs. Establishing northern cyclotrons would shrink travel by an estimated 3 million km over ten years, but capital outlays and limited personnel remain hurdles.

Skilled-Labor Shortages in Nuclear Medicine Technologists

Canada recorded 78,600 unfilled healthcare positions in Q3 2024, with nuclear medicine among the hardest roles to staff. CAMRT-certified technologists take four years to train, limiting short-term supply. Immigration pathways add talent, yet credential recognition and language requirements delay workforce entry. AI denoising tools lighten workloads but require retraining, temporarily straining existing staff. Urban centers poach rural professionals with higher wages, widening geographic disparities.

Segment Analysis

By Product: Infrastructure Modernization Drives Equipment Leadership

Equipment retained 54.67% of the Canada nuclear imaging market share in 2024, supported by provincial capital budgets earmarked for hybrid scanner refresh cycles. Average PET/CT age fell to 7.2 years as Ontario and Quebec replaced legacy gamma cameras with compact SPECT/CT systems such as the Symbia Evo Excel, which offers a 30% larger bore and improved patient comfort. Hospitals increasingly adopt vendor service contracts that guarantee 98% uptime, shifting purchasing criteria toward lifecycle cost over sticker price. Meanwhile, radioisotopes climbed at a 7.34% CAGR thanks to increased theranostic use and native isotope output, positioning Canada as a net exporter of Lu-177 by 2028. Health Canada’s device licensing ensures scanners comply with radiation standards, allowing rapid introduction of AI-ready consoles.

Continued clinical validation of quantitative SPECT drives incremental upgrades across cardiac centers, while oncology departments prioritize digital PET for low-dose protocols. Emerging portable gamma cameras target rural emergency departments that cannot justify full-size scanners, creating a long-tail opportunity for niche vendors. Domestic Mo-99 production enhances procurement resilience, shielding sites from historical reactor outages. Collectively, the equipment and isotope streams solidify the revenue foundation for the Canada nuclear imaging market.

By Application: Cardiology Dominance Amid Neurology Acceleration

Cardiology accounted for 38.89% of revenue in 2024, reflecting mature reimbursement pathways and well-established referral patterns for myocardial perfusion imaging using technetium-99m sestamibi. National benchmarks target a 24-hour turnaround for emergent scans, but regional bottlenecks persist in Saskatchewan and Atlantic Canada. Neurology posted the fastest CAGR at 7.89%, driven by PET tracers that bind tau and beta-amyloid, alongside Health Canada’s approval of Alzheimer’s-focused agents such as MK-6240 following Lantheus’s acquisition of Cerveau Technologies. Oncology maintains strong momentum as radioligand therapies require pre- and post-treatment imaging, boosting PET volumes for prostate and neuroendocrine cancer.

Growth in endocrine and adrenal imaging comes from University of Calgary research that links nuclear imaging to rare adrenal disorders. AI-assisted reading reduces report time by 40% for lymphoma staging, freeing radiologists to focus on complex cases. CADTH’s horizon scanning flags emerging applications, guiding provinces in expanding coverage to neuropsychiatric disorders by 2027.

By End User: Hospitals Anchor Volumes While Out-of-Hospital Sites Scale Fast

Hospitals controlled 69.67% of the Canada nuclear imaging market size in 2024, underpinned by radiopharmacy suites, strict Canadian Nuclear Safety Commission licensing, and higher procedure complexity. Teaching hospitals often integrate research cyclotrons, making them self-sufficient for PET tracers. Diagnostic imaging centers are projected to grow at 8.01% CAGR as provinces outsource routine bone scans and thyroid studies to relieve hospital backlogs. Saskatchewan pilots require private centers to meet public scan quotas, illustrating policy leverage to expand capacity without compromising equity.

Academic institutes like TRIUMF partner with vendors to co-develop next-generation isotopes, generating revenue via intellectual property agreements. Staff shortages constrain throughput across all end users, prompting greater reliance on remote radiology reads. Instruments older than ten years experience a 15% failure rate, accelerating replacements. As AI reduces repeat scans and enhances scheduling, outpatient centers may gain share, yet hospitals will remain the primary hub for complex hybrid imaging and radionuclide therapy.

Geography Analysis

Ontario leads installation counts with 157 MRI units and the PET Scans Ontario registry coordinating OHIP-funded services. Despite scale, PET utilization sits at only 1,600 exams per million residents versus the national 3,300, indicating untapped volume growth. Quebec prohibits private MRI funding, centralizing nuclear imaging in university hospitals; its 123 MRI units deliver high absolute capacity yet leave rural Abitibi-Témiscamingue underserved. British Columbia positions itself as a Western Canada isotope hub with the CAD 50.5 million BC Cancer cyclotron complex and TRIUMF’s expanded research lines.

The Prairies rely on Jubilant’s Winnipeg and Edmonton radiopharmacies for PET-FDG supply, but long drives and winter weather cause occasional dose losses. Atlantic provinces import tracers from Quebec, and single-scanner facilities in New Brunswick and Nova Scotia lead to periodic scheduling disruptions. The Northern territories face the most severe gaps; over 84% of indigenous communities reside beyond a one-hour drive from radiotherapy centers, highlighting the need for mobile gamma camera fleets. Federal programs like NIICO aim to double isotope production and alleviate regional supply shocks, yet workforce pipelines must also expand to ensure service uptake. Cross-border referral to U.S. centers in Minnesota and North Dakota persists for advanced therapies, but domestic capacity is likely to displace outbound flow as cyclotrons multiply.

Competitive Landscape

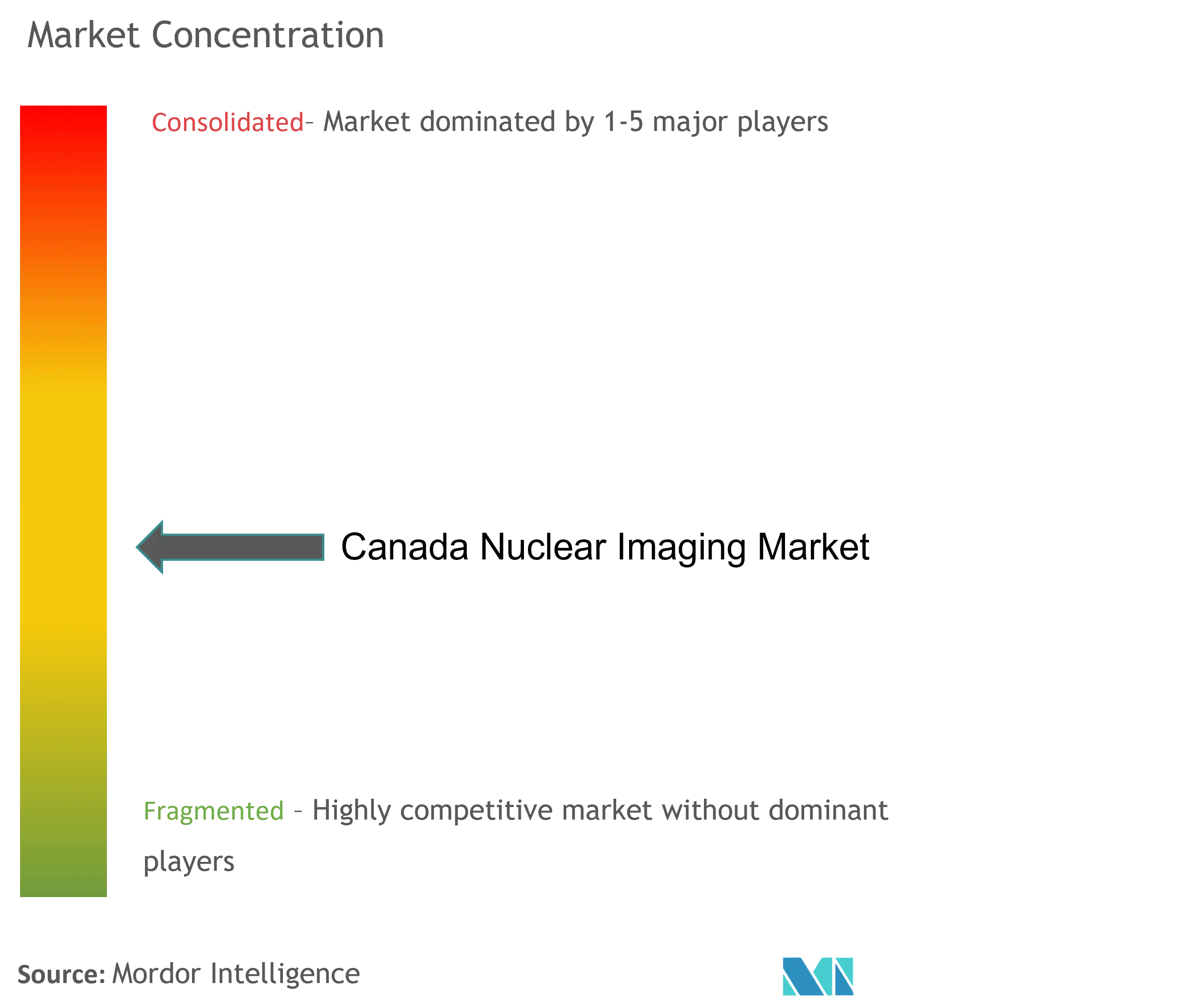

The market shows moderate concentration. GE HealthCare, Siemens Healthineers, Philips, and Canon supply the majority of scanners, while domestic players dominate isotopes and services. GE HealthCare’s USD 183 million buyout of Nihon Medi-Physics enhances its radiopharma footprint, and its pending MIM Software acquisition integrates AI analytics into installed bases. Siemens Healthineers recorded EUR 22.36 billion in fiscal 2024 revenue, driven by strong imaging demand and new SPECT/CT launches.

Jubilant Radiopharma’s 50 nuclear pharmacies secure last-mile distribution, while Advanced Cyclotron Systems and Nordion supply turnkey accelerators and cobalt-60 sources. BWXT’s USD 525 million purchase of Kinectrics doubles its commercial workforce and deepens expertise in CANDU reactor services, aligning isotope production with national energy infrastructure. Start-ups focusing on AI triage and micro-dose PET tracers attract venture funding, yet regulatory hurdles remain high. Competitive differentiation now hinges on theranostic readiness, AI workflow efficiency, and service uptime guarantees.

Canada Nuclear Imaging Industry Leaders

Bracco Imaging Spa

GE Healthcare

Koninklijke Philips N.V.

Siemens AG

Canon Medical Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Ontario launched the Nuclear Isotope Innovation Council of Ontario, targeting doubled isotope output by 2030

- May 2025: Darlington cleared to produce Lu-177 and Y-90 isotopes, expanding therapeutic capacity

Canada Nuclear Imaging Market Report Scope

Nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. These radiopharmaceuticals are used in diagnosis and therapeutics. They are small substances that contain a radioactive substance used in the treatment of cancer and cardiac and neurological disorders.

Canada's nuclear imaging market is segmented by product and application. based on product the market is segmented as equipment and diagnostic radioisotope. Based on application the market is segmented as an application SPECT application and PET application. The report offers the value (in USD) for the above segments.

By Product

| Equipment | ||

| Radioisotope | SPECT Radioisotopes | Technetium-99m (TC-99m) |

| Thallium-201 (TI-201) | ||

| Gallium (Ga-67) | ||

| Iodine (I-123) | ||

| Other SPECT Radioisotopes | ||

| PET Radioisotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (RB-82) | ||

| Other PET Radioisotopes | ||

By Application

| Cardiology |

| Neurology |

| Thyroid |

| Oncology |

| Other Applications |

By End User (Value)

| Hospitals |

| Diagnostic Imaging Centres |

| Academic & Research Institutes |

| By Product | Equipment | ||

| Radioisotope | SPECT Radioisotopes | Technetium-99m (TC-99m) | |

| Thallium-201 (TI-201) | |||

| Gallium (Ga-67) | |||

| Iodine (I-123) | |||

| Other SPECT Radioisotopes | |||

| PET Radioisotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (RB-82) | |||

| Other PET Radioisotopes | |||

| By Application | Cardiology | ||

| Neurology | |||

| Thyroid | |||

| Oncology | |||

| Other Applications | |||

| By End User (Value) | Hospitals | ||

| Diagnostic Imaging Centres | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What is the current value of the Canada nuclear imaging market?

The market is valued at USD 260.58 billion in 2025 and is projected to reach USD 367.57 billion by 2030.

Which product segment leads revenue?

Equipment accounts for 54.67% of revenue, reflecting ongoing scanner modernization across provinces.

Which application area is growing the fastest?

Neurology imaging shows the highest CAGR at 7.89% through 2030 due to expanded Alzheimers and tau tracer use.

How are workforce shortages being addressed?

Ottawa allocated USD 14.3 million to credential internationally trained professionals, and AI workflow tools reduce technologist workload.

Why is domestic isotope production important?

Local Mo-99 and Lu-177 output reduces dependence on foreign reactors and secures supply for both diagnostics and therapeutic radiopharmaceuticals.

Which provinces are investing most heavily in new cyclotrons?

Ontario and British Columbia lead investments, with projects at Darlington and BC Cancer receiving significant provincial and federal funding.

Page last updated on: