Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

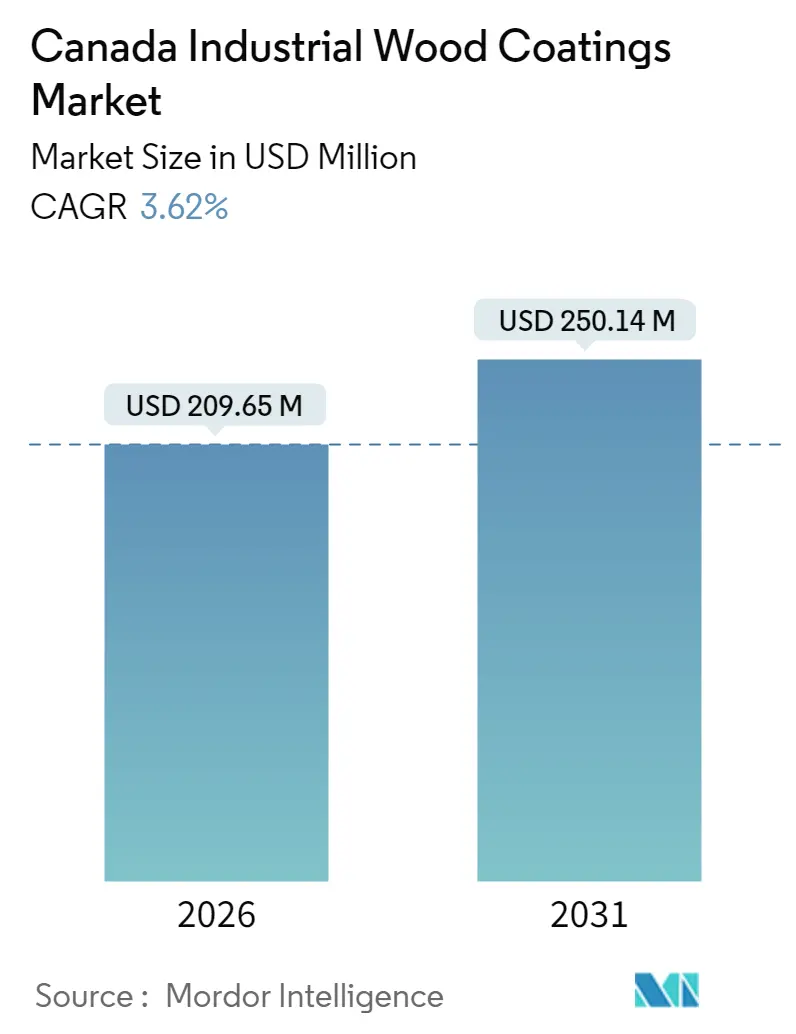

| Market Size (2026) | USD 209.65 Million |

| Market Size (2031) | USD 250.14 Million |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Industrial Wood Coatings Market Analysis by Mordor Intelligence

The Canada industrial wood coatings market was valued at USD 202.32 million in 2025 and estimated to grow from USD 209.65 million in 2026 to reach USD 250.14 million by 2031, at a CAGR of 3.62% during the forecast period (2026-2031). Capacity additions in cross-laminated timber (CLT), sustained residential renovation, and stricter federal procurement preferences for domestic lumber underpin steady volume growth, while lingering port disruption risk and softwood lumber trade friction temper expansion. Adoption of high-solids polyurethane dispersions and UV-LED-curable chemistries signals a decisive pivot toward low-VOC compliance, prompted by SOR/2021-268 limits that took effect in January 2024. Polyurethane resins, already established in flooring and cabinet lines, experience incremental share gains as formulators blend bio-based polyols without compromising hardness or Taber abrasion cycles. Competitive intensity remains moderate because multinational suppliers control key raw material chains; however, regional formulators leverage their proximity to Quebec, Ontario, and British Columbia furniture clusters to win specification-driven contracts. The Canada industrial wood coatings market continues to track a measured pace that balances regulatory pressure, material innovation, and downstream labor shortages.

Key Report Takeaways

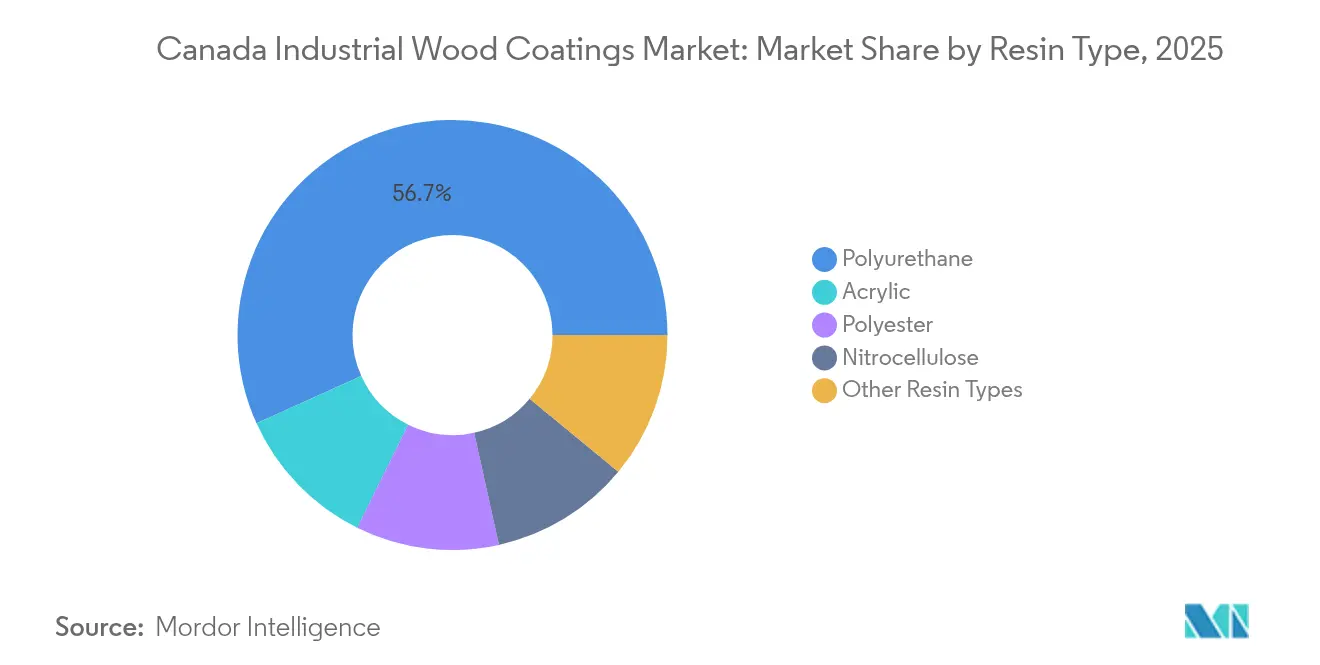

- By resin type, polyurethane captured 56.74% of Canada's industrial wood coatings market share in 2025 and is expected to expand at a 3.92% CAGR through 2031, maintaining its clear dominance.

- By technology, solvent-borne captured 52.61% of Canada's industrial wood coatings market share in 2025, while water-borne systems are forecast to outpace all other platforms at a 4.37% CAGR through 2031, reflecting the direct impact of SOR/2021-268 VOC caps.

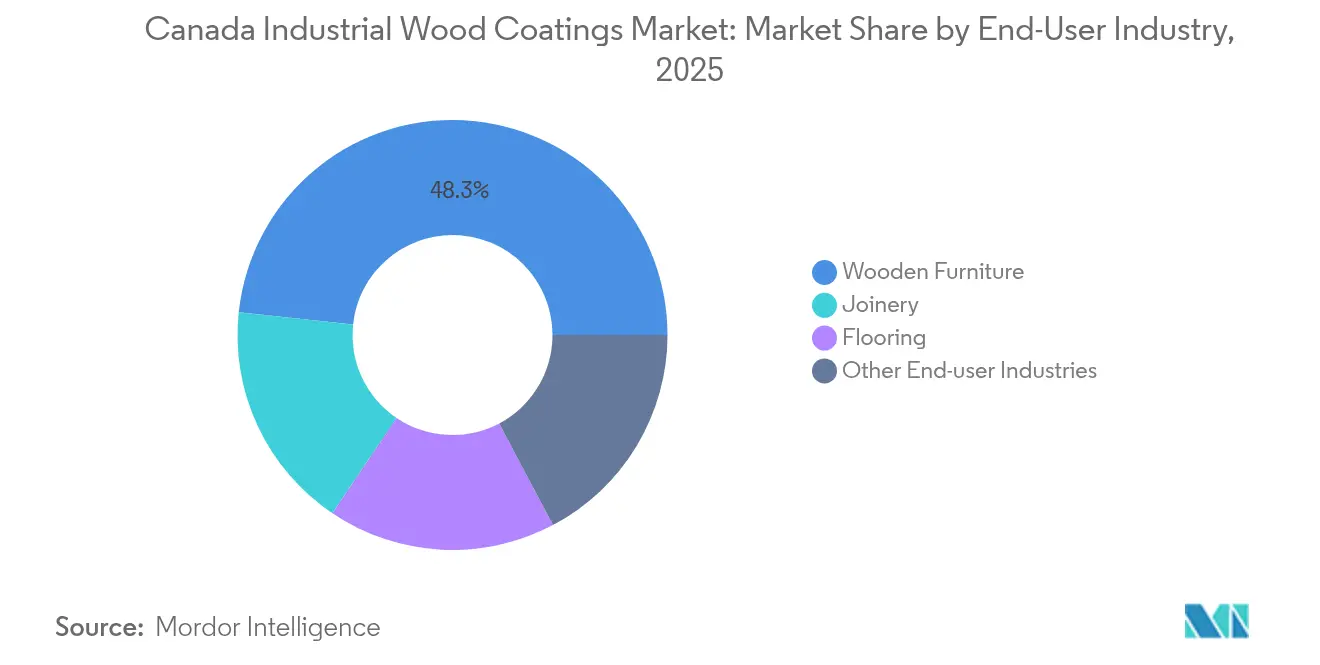

- By end-user industry, wooden furniture accounted for 48.31% of the Canadian industrial wood coatings market size in 2025 and is expected to grow at a 3.98% CAGR during the period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Industrial Wood Coatings Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Wooden Furniture | + 0.8% | National, concentrated in Quebec, Ontario, and British Columbia, furniture clusters. | Medium term (2-4 years) |

| Increasing Construction and Renovation Activities | + 0.7% | National, with stronger momentum in Alberta, Ontario, and the Atlantic provinces | Short term (≤ 2 years) |

| Adoption of Low-VOC and Water-borne Formulations | + 0.9% | National, driven by federal SOR/2021-268 and provincial environmental mandates. | Long term (≥ 4 years) |

| Investment in Modular and Prefabricated Timber Buildings | + 0.6% | National, early gains in British Columbia, Ontario, Nova Scotia | Medium term (2-4 years) |

| Expansion of Mass Timber (CLT) Manufacturing | + 0.7% | British Columbia, Ontario, Nova Scotia, Quebec | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Wooden Furniture

Federal loan guarantees of CAD 700 million and a CAD 500 million diversification fund, introduced in January 2025, stabilize a sector that employs nearly 200,000 people and generates more than CAD 20 billion in GDP. Domestic producers gain share as the Canada Border Services Agency (CBSA) maintains anti-dumping duties of 188.0% on Chinese and 179.5% on Vietnamese upholstered seating, redirecting orders to local upholstery shops. Hardwood flooring leaders invested more than CAD 30 million between 2023 and 2025 to automate grading and finishing lines, cutting per-square-foot finish costs by two-thirds. Factory-applied ultra-matte coats with 10° gloss levels meet commercial fit-out specifications in Toronto and Vancouver, where office-to-residential conversions and cabinetry refits are common. Carpenter shortages—44,700 openings versus 38,800 seekers to 2033—push builders toward turnkey, factory-finished millwork that minimizes on-site labor. These converging factors keep the Canada industrial wood coatings market firmly anchored in furniture demand.

Increasing Construction and Renovation Activities

BuildForce Canada forecasts rising construction and maintenance spending through 2033, with interest-rate cuts in 2024 expected to revive single-family home starts. Provincial initiatives, such as Yukon's CAD 200 million Community-Building Fund and Nunavut’s 1,000-home Nunavut 3000 program, have sustained demand for prefinished joinery across the northern territories. Renovation outlays remain elevated in British Columbia and Atlantic Canada, where aging housing stock drives replacement of millwork, doors, and engineered hardwood. The federally backed “Build Canada Homes” financing stream favors Canadian lumber, locking in coating volumes for domestic panel mills and finish plants. Shortage-driven wage inflation among carpenters further accelerates prefabrication, a trend that directly escalates industrial coating throughput. Collectively, these drivers underpin a positive near-term outlook for the Canadian industrial wood coatings market[1]Government of Canada, “Canadian Occupational Projection System 2024,” canada.ca.

Adoption of Low-VOC and Water-borne Formulations

SOR/2021-268 caps VOC content at 250 g/L in industrial wood finishes, with a March 2025 formaldehyde-testing deadline adding compliance urgency. Water-borne polyurethane dispersions at 50% solids achieve sub-50 g/L VOC while maintaining scratch resistance, narrowing historical performance gaps. AkzoNobel’s RUBBOL WF 3350, launched February 2025, incorporates 20% bio-based content and targets LEED projects that specify GREENGUARD Gold. Axalta’s July 2024 Cerulean range offers drop-in replacement capability for solvent-borne spray systems, lowering conversion cost. Laboratories accredited under ISO/IEC 17025 validate VOC claims and feed third-party Environmental Product Declarations, now common in public-tender documentation. As a result, water-borne chemistries secure rising allocations in purchase frameworks across cabinet, millwork, and furniture factories nationwide, reinforcing long-run growth of the Canada industrial wood coatings market.

Investment in Modular and Prefabricated Timber Buildings

More than CAD 1 billion in federal and provincial capital has been invested in modular and CLT plants since 2024. Element5 doubled Ontario capacity to 100,000 m³ annually, while a new Nova Scotia facility adds 50,000 m³. Modular assembly relocates coating operations to climate-controlled environments that accommodate UV-LED cure lines, where dwell times are typically under five seconds. Ontario’s 2025 Advanced Wood Construction Action Plan embeds procurement preferences for prefabricated components, essentially creating a captive coating pipeline. The National Research Council of Canada is piloting clear intumescent finishes that maintain wood grain while meeting mid-rise fire-rating codes, widening use cases, and lifting volume potential for specialty topcoats.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC Emission Regulations | -0.5% | National, with stricter provincial enforcement in Quebec, British Columbia | Short term (≤ 2 years) |

| Availability of Alternative Non-wood Materials | -0.3% | National, concentrated in the commercial furniture and flooring segments | Medium term (2-4 years) |

| Volatile Petrochemical Resin Prices | -0.4% | National, affecting all coating formulators reliant on imported feedstocks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent VOC Emission Regulations

The January 2024 VOC cap and March 2025 formaldehyde benchmark impose new testing, labeling, and formulation costs. Small and mid-sized regional formulators must either purchase chromatography equipment or outsource compliance audits, which raises their per-gallon cost structures. Disparate provincial thresholds—tighter in Quebec and British Columbia—complicate inventory planning and lengthen product-approval cycles. Extended dry times in early-generation water-borne systems necessitate that floorboard factories reconfigure stacking conveyors, resulting in reduced productivity until operators become accustomed. Some niche suppliers consider mergers with vertically integrated multinationals to amortize compliance overheads, potentially reducing price competition in custom-color batches[2]Environment and Climate Change Canada, “SOR/2021-268 Volatile Organic Compound Regulations,” canada.ca .

Availability of Alternative Non-wood Materials

High-pressure laminate and luxury vinyl tile capitalize on moisture resistance and reduced maintenance, siphoning share from solid hardwood in commercial corridors. Metal-frame furniture gains favor in hospitality projects seeking durability over classic wood appeal. Recycling challenges for melamine-urea-bonded panels deter architects under circular-economy mandates, nudging them toward recyclable steel. These material substitutions cap incremental top-line upside for the Canada industrial wood coatings market, particularly in office and institutional fit-outs.

Segment Analysis

By Resin Type: Polyurethane Dominance Anchored in Performance

Polyurethane held 56.74% of Canada's industrial wood coatings market share in 2025 and is forecast to advance at a 3.92% CAGR to 2031. The resin’s superior abrasion resistance is evident in Mercier’s Generations Intact 2500 finish, which withstands 2,500 Taber cycles, double the industry’s 1,000-cycle benchmark. Flooring mills exploit this durability to extend residential warranties to 50 years, a critical differentiator in premium segments. Compatibility with water-borne systems allows formulators to maintain compliance without abandoning established supply chains. Hybrid PU–acrylic blends, such as AkzoNobel’s Selva Pro, offer a lower cost while meeting the 10° ultra-matte aesthetic trends prevalent in kitchen cabinetry. Bio-based polyols derived from vegetable oil and lignin enter pilot scale, promising to cut fossil-carbon footprints while retaining chemical crosslink density. Research consortia are exploring cellulose-nanocrystal reinforcement to reduce aluminum-oxide filler loadings, potentially lowering raw material costs. Niche chemistries—such as nitrocellulose and polyester—continue to be restricted because their flammability and VOC profiles exceed Canadian thresholds, limiting their usage to specialty applications, including guitar restoration and antique furniture restoration.

Acrylic systems occupy value segments where rapid sand-and-recoat cycles outweigh long-term abrasion metrics. Polyester powder on medium-density fiberboard (MDF) remains confined to North American lead times and color palette constraints, although Tiger Coatings demonstrates 110 °C cure profiles that preserve substrate integrity. The increased adoption of UV-LED lines, which require PU oligomers with tailored photoinitiators, fosters demand for specialty feedstocks from Covestro and Allnex. The Canada industrial wood coatings market size for polyurethane is therefore positioned for incremental gains as performance thresholds and regulatory compliance converge on the same molecular platform.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: Water-borne Surge Amid Regulatory Tailwinds

Solvent-borne finishes commanded 52.61% revenue in 2025, yet water-borne rivals are on track for a 4.37% CAGR to 2031, outstripping the overall Canada industrial wood coatings market by more than 60 basis points. Stricter emission ceilings incentivize processors to retrofit spray booths with high-efficiency air make-up units, ensuring quick adoption across cabinet and millwork plants. High-solids water-borne polyurethanes provide 4 mil wet-film builds in a single pass, narrowing cycle-time spreads with solvent grades. Axalta’s Cerulean topcoat line utilizes nano-dispersion technology to ensure uniform pigment distribution, thereby eliminating mud cracking on deep-grain oak. UV finishes, representing a smaller but influential niche, achieve 100% solids with instant cure; however, the capital outlay for lamp arrays slows conversion among smaller job shops. LED modules, however, boast 60% lower energy draw than mercury-arc predecessors and emit negligible ozone, making them attractive for futureproofing.

Powder coatings on MDF remain experimental because gloss levels below 15° are challenging; nonetheless, pilot lines in Quebec run textured whites that meet value-furniture price points. Oil-modified urethanes persist in boutique heritage restoration, where solvent aroma is tolerated for classic patina. Looking forward, the interplay between water-borne and UV systems will define product-mix evolution, with LED-ready chemistries acting as the bridge technology that accelerates VOC-free adoption within the Canada industrial wood coatings market.

By End-User Industry: Furniture Leads, Joinery and Flooring Follow

Wooden furniture accounted for 48.31% of 2025 demand and is projected to grow at a rate of 3.98% per year to 2031, outpacing macroeconomic GDP expansion. Loan guarantees and procurement mandates announced in 2025 insulate local manufacturers from import competition, particularly after the CBSA’s imposition of upholstered-seating duties. Automated spray lines now integrate vision-guided robotics, enabling four-head reciprocators to process 240 chair frames per hour, versus 150 on legacy rigs. Joinery and architectural millwork secure the next-largest slice, driven by office-to-residential retrofits that specify prefinished trim to shorten turnover. Flooring producers are embracing factory-applied ultra-matte coats that accommodate radiant heating, with Mirage’s TruBalance Lite planks supporting floating installations across grade levels.

Labor scarcity reshapes end-user buying behavior. With 5,900 more carpenter vacancies than job seekers projected through 2033, builders are gravitating to pre-lacquered moldings and panels that reduce on-site finishing hours. The Canada industrial wood coatings market size allocated to flooring also gains as engineered hardwood edges out solid lumber in climate-swing provinces, leveraging dimensional stability. Decking, siding, and mass-timber structural elements round out demand, creating a diversified substrate mix that shields suppliers from segment-specific downturns.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Quebec, Ontario, and British Columbia are the key markets for industrial wood coating in Canada, driven by dense clusters of furniture and flooring production. Quebec hosts approximately 39,500 carpenters and marquee producers, such as Mercier and Lauzon, whose combined CAD 25 million in automation upgrades since 2023 have streamlined lacquer consumption and elevated finish consistency. Ontario’s 36,250 carpenters, paired with Element5’s 100,000-m³ CLT plant and the 2025 Advanced Wood Construction Action Plan, cement the province as the fastest-growing geographic node. British Columbia’s 20,150 carpenters align with Kalesnikoff’s CAD 34 million expansion, but timber-supply constraints, evidenced by Canfor’s sawmill closures, inject localized feedstock risk.

Prairie provinces contribute steady, if smaller, volumes. Alberta’s CAD 2.25 million Value-Added Wood program nudges veneer and panel shops toward higher-margin UV finishes, while Manitoba and Saskatchewan maintain niche cabinetry businesses supplying regional homebuilders. Atlantic Canada benefits from Nova Scotia’s 50,000-m³ CLT plant, which seeds demand for protective sealers on load-bearing panels shipped across the Maritimes. Northern territories remain project-driven; Nunavut’s 1,000-home initiative and Yukon’s infrastructure fund specify prefinished timber to mitigate harsh-weather installation windows. These geographic dynamics reinforce a stable base for the Canada industrial wood coatings market, although port chokepoints in Vancouver and road freight over the Ambassador Bridge remain systemic vulnerabilities.

Competitive Landscape

Canada's Industrial wood coatings market is moderately consolidated, with regional players using proximity advantages to win custom color-matching contracts in Quebec and British Columbia. Smaller formulators face rising compliance costs; consolidation looms as SOR/2021-268 lab-testing expenses mount. Meanwhile, innovation white-space clusters around UV-LED chemistries, clear intumescent coats for CLT, and lignin-derived polyols. Strategic alliances between resin manufacturers and machine builders aim to deliver turnkey UV-LED lines that reduce energy consumption by 60% and floor space by 30%, appealing to mid-sized furniture plants upgrading from solvent-based lines.

Canada Industrial Wood Coatings Industry Leaders

The Sherwin Williams

Akzo Nobel N.V.

PPG Industries Inc.

Axalta Coating Systems

RPM International Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: AkzoNobel launched RUBBOL WF 3350, a sprayable water-borne coating with 20% bio-based content that meets sub-50 g/L VOC requirements, targeting LEED-specified furniture and joinery projects.

- January 2025: AkzoNobel rolled out the Selva Pro polyurethane–acrylic system for kitchens, bathrooms, and millwork through the Chemcraft distributor network, focusing on renovation demand in aging housing stock.

- July 2024: Axalta introduced the Cerulean water-borne range of topcoats and undercoats designed as drop-in replacements for solvent systems in furniture and cabinet factories.

Canada Industrial Wood Coatings Market Report Scope

By Resin Type

| Acrylic |

| Nitrocellulose |

| Polyester |

| Polyurethane |

| Other Resin Types |

By Technology

| Water-Borne |

| Solvent-Borne |

| UV Coatings |

| Powder Coatings |

By End-User Industry

| Wooden Furniture |

| Joinery |

| Flooring |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Nitrocellulose | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By Technology | Water-Borne |

| Solvent-Borne | |

| UV Coatings | |

| Powder Coatings | |

| By End-User Industry | Wooden Furniture |

| Joinery | |

| Flooring | |

| Other End-user Industries |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast value of the Canada industrial wood coatings market in 2031?

The market is projected to reach USD 250.14 million by 2031.

Which resin holds the largest share in Canadian wood-coating applications?

Polyurethane accounts for 56.74% of the 2025 demand and is expected to retain its leadership position.

Why are water-borne coatings growing faster than solvent-borne in Canada?

SOR/2021-268 VOC limits, coupled with formaldehyde regulations effective as of March 2025, are prompting factories to adopt low-emission water-borne chemistries.

How will mass-timber construction influence coating demand?

More than 150,000 m³ of new CLT capacity is expected to boost demand for factory-applied protective finishes on structural panels.

Which provinces generate the highest consumption of industrial wood coatings?

Quebec, Ontario, and British Columbia together account for over 70% of market revenue in 2026.