| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 13.41 Billion |

| Market Size (2030) | USD 15.69 Billion |

| CAGR (2025 - 2030) | 3.20 % |

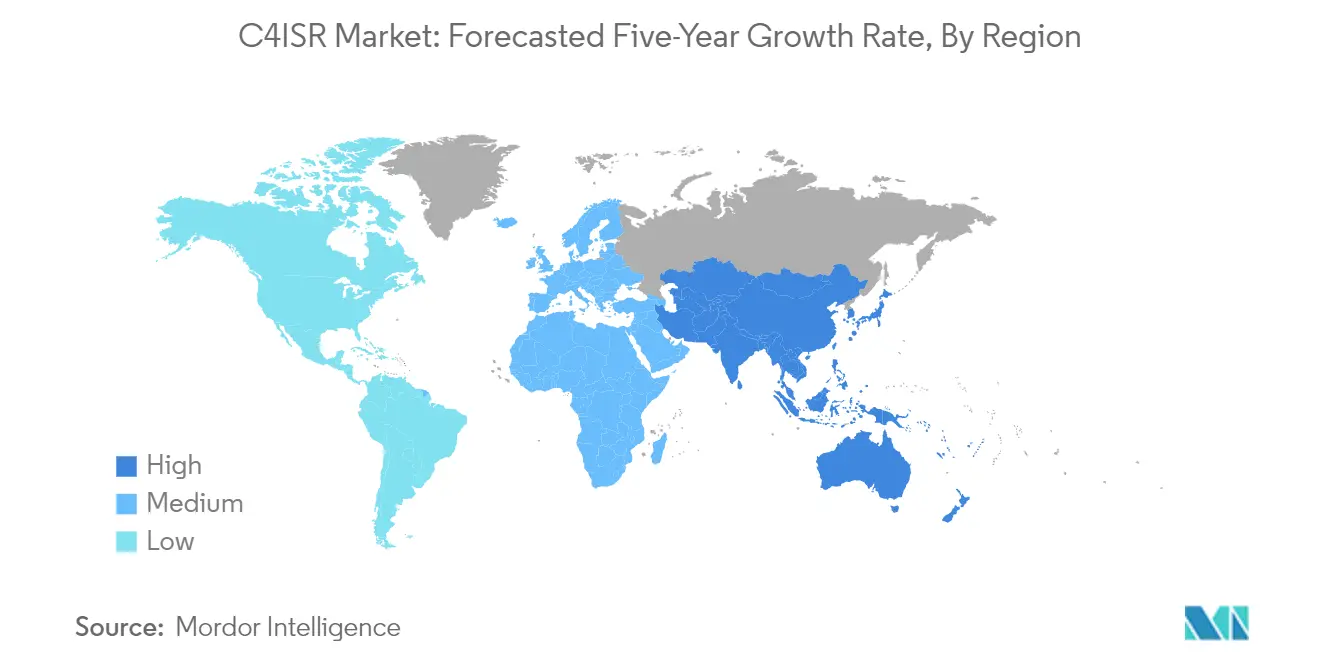

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

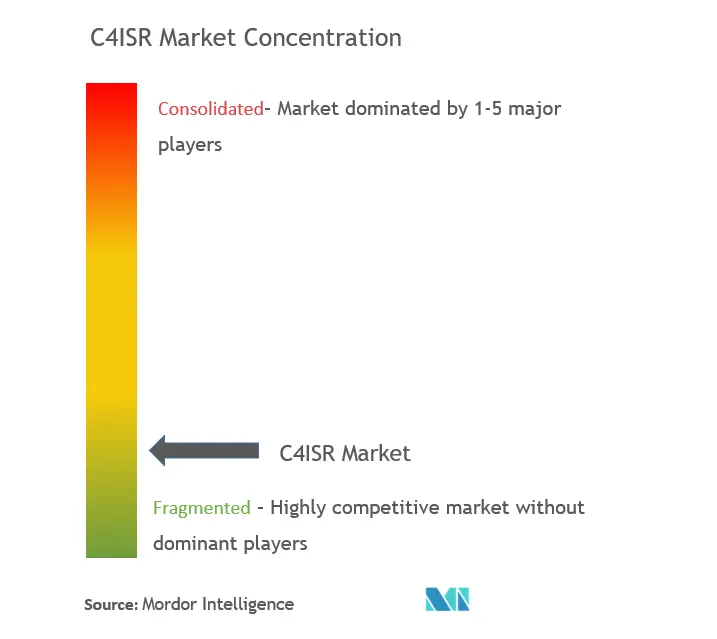

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

C4ISR Market Analysis

The C4ISR Market size is estimated at USD 13.41 billion in 2025, and is expected to reach USD 15.69 billion by 2030, at a CAGR of 3.2% during the forecast period (2025-2030).

The C4ISR industry is experiencing a fundamental transformation driven by the increasing complexity of modern warfare and rapid technological advancement. The global defense landscape has witnessed unprecedented changes, reflected in the substantial increase in worldwide military expenditure, which reached USD 2,113 billion in 2021, with the five largest military spenders accounting for 62% of total global spending. This significant investment has catalyzed the development of sophisticated C4ISR systems, particularly in areas such as artificial intelligence integration, autonomous capabilities, and enhanced surveillance technologies. The evolution of asymmetric warfare has necessitated more advanced and integrated command and control systems, pushing military forces worldwide to adopt more sophisticated C4ISR solutions.

The industry is witnessing a dramatic shift toward miniaturization and enhanced accuracy in ISR systems and payloads, revolutionizing their deployment across various platforms. Military organizations are increasingly focusing on developing and implementing open-architecture ISR systems, which offer greater flexibility and interoperability between different platforms and systems. The integration of intelligence-gathering sensors with enhanced surveillance range and capabilities has become a cornerstone of modern military operations, enabling better situational awareness and decision-making capabilities for military personnel. This transformation is particularly evident in the growing adoption of unmanned systems and platforms with autonomous capabilities.

A significant trend reshaping the C4ISR landscape is the integration of artificial intelligence and machine learning technologies into existing platforms. Military forces are increasingly leveraging AI-powered systems for data analysis, threat detection, and decision support, marking a paradigm shift in how military operations are conducted. The United States, leading this technological revolution, has allocated substantial resources to AI initiatives, with the Pentagon's budget proposal counting 600 individual AI efforts across the Department of Defense, marking a 50% increase over previous years. This integration of AI technologies is enabling faster processing of sensor data, automatic creation of targeting data for potential threats, and more efficient recommendation of weapon systems for response.

The industry faces significant challenges in managing and processing the unprecedented volume of data generated by advanced C4ISR systems. Military organizations are investing heavily in developing robust data management and analysis capabilities to effectively utilize the massive amounts of information collected by various sensors and platforms. The focus has shifted toward developing integrated solutions that can handle multi-domain operations, combining data from air, land, sea, space, and cyber domains. This integration challenge has spurred innovation in areas such as quantum communications, big data analytics, and 5G communications, creating new market segments and business opportunities while simultaneously addressing the growing complexity of modern military operations.

C4ISR Market Trends

GROWTH IN THE GLOBAL DEFENSE EXPENDITURE

The continuous rise in global defense expenditure has become a significant driver for the C4ISR market, with military spending reaching USD 2113 billion in 2021, representing a 12% increase compared to 2012 levels. This substantial increase in defense budgets has enabled countries to invest heavily in enhancing their C4ISR capabilities through either indigenous development or procurement from global vendors. The five largest military spenders in 2021, including the United States, China, India, the United Kingdom, and Russia, together accounted for 62% of world military spending, demonstrating the strong financial backing available for advanced military technologies and systems.

The increased military spending has particularly benefited the development and procurement of sophisticated C4ISR systems, as countries strive to enhance their combat and support capabilities. This is evidenced by recent developments such as Northrop Grumman's completion of Thermal Vacuum tests on the Arctic Satellite Broadband Mission in November 2023, demonstrating the ongoing investment in advanced communication and surveillance capabilities. Furthermore, the allocation of significant portions of defense budgets specifically for C4ISR systems, such as the US Pentagon's USD 12.7 billion allocation for command, control, communications, computers, and intelligence systems in FY 2023, highlights the priority given to these critical military capabilities.

Understand The Key Trends Shaping This Market

Download PDF

GROWING FOCUS ON ENHANCING CAPABILITIES THROUGH MODERNIZATION

The increasing complexity of modern warfare has driven nations to prioritize the modernization of their C4ISR capabilities, particularly in response to evolving asymmetric threat environments. This modernization effort is evident in recent developments, such as the February 2023 contract awarded to Maxar Technologies worth USD 192 million by the National Geospatial-Intelligence Agency to provide commercial satellite imagery and three-dimensional data services to US allies. The focus on modernization extends across multiple domains, including the integration of artificial intelligence, enhancement of real-time intelligence gathering capabilities, and improved situational awareness systems.

The modernization drive is further exemplified by the development of advanced technologies like High-Altitude Pseudo Satellites (HAPS), which represent a significant advancement in bridging the gap between traditional satellites and drones. These systems provide more economical alternatives while maintaining high-performance capabilities in delivering voice, video, and broadband services. Additionally, the integration of emerging technologies such as artificial intelligence has enhanced the effectiveness of C4ISR operations, enabling real-time intelligence processing and automated target analysis, demonstrating the continuous evolution and modernization of military capabilities.

ADVANCEMENTS IN NETWORK CENTRIC WARFARE (NCW) TECHNOLOGIES

The evolution of Network Centric Warfare technologies has emerged as a crucial driver for the global C4ISR market forecast, fundamentally transforming how military forces communicate, disseminate intelligence, and coordinate resources against increasingly unpredictable threats. This advancement is exemplified by recent developments in integrated battle management systems, such as Elbit Systems UK's TORCH-X-based solution deployment in 2023, which enables effective coordination of air assets into complex land and joint battlespace operations. The implementation of NCW technologies has significantly enhanced military forces' ability to achieve information dominance and create comprehensive situational awareness at all levels.

The advancement in NCW technologies has also led to the development of sophisticated networks that can extract data from multiple feeds to assimilate into a single combined intelligence picture. These networks amplify the effect of data collection by individual C4ISR systems, as overlaying the feeds of multiple systems enhances situational awareness beyond the capabilities of individual systems. The focus has shifted toward developing systems that can capture minimum essential information and transform it into actionable intelligence through the integration of sophisticated sensors and subsystems. This evolution in NCW capabilities has driven the demand for more advanced C4ISR systems that can support joint operations and enable effective multi-domain operations.

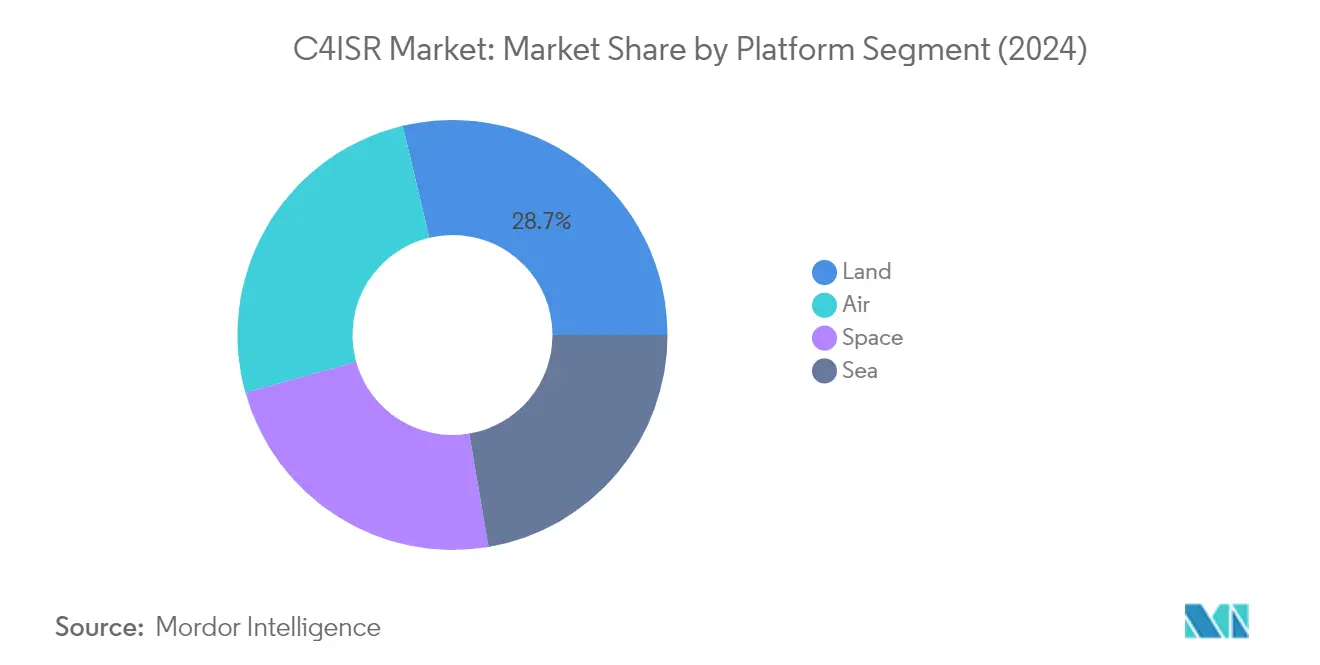

Segment Analysis: Platform

Land Segment in C4ISR Market

The land segment maintains its dominant position in the C4ISR market, accounting for approximately 30% market share in 2024. This leadership position is driven by the increasing demand for C4ISR systems to enhance situational awareness at land borders worldwide. Military forces are actively investing in the integration and modernization of geospatial intelligence, combat management systems, unmanned ground vehicles (UGVs), and communication systems to enhance the situational awareness of military personnel. The segment's growth is further supported by the widespread adoption of software-defined radios for infantry soldiers and armored vehicles, ensuring secure communication channels between ground-to-air and ground-to-ground platforms. Additionally, the importance of human-portable EO/IR sensors for gathering battlefield information continues to rise, with tactical information being collected through systematic observation by deployed soldiers. The global land platforms market size is expected to continue its expansion due to these advancements.

Space Segment in C4ISR Market

The space segment is projected to demonstrate the highest growth rate of approximately 6% during the forecast period 2024-2029, driven by robust investments from countries like the United States, Russia, and China in adopting space-based systems for enhanced situational awareness, secure communications, and threat detection capabilities. The emergence of pseudo-high-altitude satellites (HAPS) has effectively bridged the gap between drones and satellites in terms of coverage and cost efficiency. These systems incorporate the best aspects of terrestrial and satellite-based communication systems, eliminating capacity and performance limitations of traditional satellites by efficiently delivering voice, video, and broadband services at more economical pricing versus conventional geostationary satellites. The segment's growth is further accelerated by increasing investments in small satellite constellations in low-earth orbit (LEO) to obtain enhanced space-based situational awareness capabilities within the C4ISR systems market.

Remaining Segments in Platform Segmentation

The air and sea segments continue to play crucial roles in the C4ISR market ecosystem. The air segment encompasses both crewed and uncrewed aerial ISR systems, providing extensive capabilities for combat decision-makers during crisis situations. These platforms synchronize planning and operation components through analysis and production capabilities to enable current and future operations. Meanwhile, the sea segment focuses on enhancing maritime domain awareness through advanced command and control systems, integrated sensor suites, and naval electronic warfare capabilities. Both segments are witnessing continuous technological advancements in areas such as multi-spectral sensing, autonomous operations, and integrated communication systems.

Segment Analysis: Purpose

ISR Segment in C4ISR Market

The Intelligence, Surveillance, and Reconnaissance (ISR) segment dominates the C4ISR market, commanding approximately 62% of the total market share in 2024. This significant market position is driven by the increasing adoption of advanced ISR systems across military forces worldwide for enhanced situational awareness and decision-making capabilities. The segment's prominence is further strengthened by the growing deployment of unmanned aerial vehicles (UAVs), maritime patrol aircraft, and space-based surveillance systems for various military applications. Military organizations are increasingly investing in sophisticated ISR platforms equipped with advanced sensors, imaging systems, and data processing capabilities to maintain strategic advantages in modern warfare scenarios. The integration of artificial intelligence and machine learning technologies in ISR systems has also contributed to the segment's market leadership by enabling more efficient data analysis and threat detection capabilities.

C4 Segment in C4ISR Market

The Command, Control, Communications, and Computer (C4) segment is projected to exhibit the highest growth rate in the C4ISR market during the forecast period 2024-2029, with an approximate growth rate of 4%. This accelerated growth is primarily attributed to the increasing focus on network-centric warfare capabilities and the modernization of military communication infrastructure. The segment is witnessing substantial investments in developing advanced command and control systems that enable seamless integration of multi-domain operations. The adoption of 5G technology, software-defined radios, and cloud computing solutions is revolutionizing military communications, driving the segment's growth. Furthermore, the emphasis on developing secure and resilient communication networks to counter cyber threats has led to increased spending on advanced C4 systems, contributing to the segment's rapid expansion.

Remaining Segments in Purpose Segmentation

The Electronic Warfare (EW) segment plays a crucial role in the C4ISR market by providing critical capabilities for electromagnetic spectrum operations and counter-electronic warfare measures. This segment encompasses various technologies and systems designed to detect, intercept, and counter enemy electronic systems while protecting friendly forces' electronic capabilities. The increasing sophistication of electronic threats and the growing importance of electromagnetic spectrum dominance in modern warfare continue to drive innovations in EW systems. Military forces worldwide are investing in advanced jamming systems, electronic protection measures, and signals intelligence capabilities to maintain technological superiority in contested electromagnetic environments.

C4ISR Market Geography Segment Analysis

C4ISR Market in North America

North America represents a dominant force in the global C4ISR market, driven by substantial military investments and technological advancement initiatives. The United States and Canada form the core of this regional market, with both countries actively pursuing modernization of their defense capabilities. The region's market dynamics are shaped by ongoing military modernization programs, an increasing focus on network-centric warfare capabilities, and the integration of advanced technologies like artificial intelligence and machine learning in C4ISR systems. Both countries maintain robust defense relationships and frequently collaborate on joint military initiatives, contributing to the regional market's growth.

C4ISR Market in United States

The United States C4ISR market maintains its position as the largest market in North America, commanding approximately 85% of the regional market share. The country's dominance is underpinned by its extensive military infrastructure, substantial defense budget, and leadership in technological innovation. The U.S. Department of Defense continues to prioritize C4ISR capabilities through various programs, including the Joint All-Domain Command and Control (JADC2) initiative. The nation's strong industrial base, featuring major defense contractors and technology companies, further reinforces its market leadership. The U.S. military's focus on maintaining technological superiority across all domains—air, land, sea, space, and cyber—drives continuous investment in advanced C4ISR systems.

C4ISR Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 3% during 2024-2029. The country's market expansion is driven by its comprehensive military modernization initiatives and increasing focus on Arctic sovereignty protection. Canada's defense strategy emphasizes enhanced surveillance capabilities, particularly in its vast northern territories. The country's investment in advanced C4ISR systems is further supported by its participation in international defense cooperation programs and its commitment to NATO obligations. Canadian forces are actively upgrading their C4ISR capabilities through various programs, including the acquisition of new surveillance aircraft and the modernization of existing systems.

C4ISR Market in Europe

The European C4ISR market demonstrates significant dynamism, characterized by increasing defense cooperation among nations and ongoing modernization efforts. The region's market landscape is shaped by key players including the United Kingdom, Germany, France, and Russia, each contributing distinct capabilities and requirements. The European market is particularly influenced by NATO's standardization requirements and the growing emphasis on interoperability among allied forces. Regional tensions and evolving security challenges continue to drive investments in advanced C4ISR capabilities across European nations.

C4ISR Market in Russia

Russia maintains its position as the largest C4ISR market in Europe, holding approximately 27% of the regional market share. The country's significant market presence is supported by its extensive military modernization programs and indigenous defense industrial base. Russia's focus on developing advanced electronic warfare capabilities and integrated command and control systems demonstrates its commitment to maintaining military technological parity. The nation's strategic emphasis on network-centric warfare capabilities and the development of advanced surveillance systems continues to drive market growth.

C4ISR Market in United Kingdom

The United Kingdom emerges as one of the fastest-growing markets in Europe, with a projected growth rate of approximately 3% during 2024-2029. The UK's market expansion is driven by its comprehensive defense modernization initiatives and increasing focus on digital transformation in military operations. The country's investment in advanced C4ISR systems is supported by its strong defense industrial base and commitment to maintaining technological superiority. British forces are actively pursuing various programs to enhance their command, control, and intelligence capabilities across all operational domains.

C4ISR Market in Asia-Pacific

The Asia-Pacific region represents a rapidly evolving market for C4ISR systems, characterized by increasing defense modernization initiatives and growing regional security challenges. Key markets including China, India, Japan, and South Korea are driving significant developments in the sector. The region's market dynamics are influenced by various factors including territorial disputes, maritime security concerns, and the modernization of military forces. The emphasis on indigenous development capabilities and strategic partnerships with international defense contractors continues to shape the market landscape.

C4ISR Market in China

China maintains its position as the dominant force in the Asia-Pacific C4ISR market, driven by its comprehensive military modernization program and significant investments in advanced technologies. The country's focus on developing indigenous capabilities across all domains of military operations has strengthened its market position. China's strategic emphasis on network-centric warfare capabilities and the integration of artificial intelligence in military systems continues to drive market growth. The nation's development of advanced surveillance and reconnaissance systems reflects its commitment to enhancing its military technological capabilities.

C4ISR Market in South Korea

South Korea emerges as the fastest-growing market in the Asia-Pacific region, driven by its robust defense modernization initiatives and increasing focus on technological advancement. The country's investment in C4ISR systems is supported by its strong electronics and technology industrial base. South Korean forces are actively pursuing various programs to enhance their command, control, and intelligence capabilities, particularly in response to regional security challenges. The nation's emphasis on developing advanced electronic warfare capabilities and integrated command systems demonstrates its commitment to military modernization.

C4ISR Market in Latin America

The Latin American C4ISR market demonstrates steady development, with Brazil and Mexico emerging as key players in the region. The market is characterized by an increasing focus on border security, counter-narcotics operations, and military modernization initiatives. Brazil stands out as both the largest and fastest-growing market in the region, driven by its comprehensive military modernization programs and emphasis on developing indigenous defense capabilities. The region's market dynamics are influenced by various factors including economic conditions, security challenges, and the need to upgrade aging military equipment. Countries in the region are increasingly focusing on enhancing their surveillance and reconnaissance capabilities, particularly for maritime patrol and border security operations.

C4ISR Market in Middle East & Africa

The Middle East & Africa region presents a dynamic market for C4ISR systems, with the United Arab Emirates, Saudi Arabia, and Turkey emerging as key players. The market is characterized by significant investments in military modernization and the adoption of advanced defense technologies. Saudi Arabia maintains its position as the largest market in the region, while the United Arab Emirates shows the fastest growth trajectory. The region's market dynamics are influenced by ongoing regional tensions, modernization initiatives, and the need for enhanced surveillance and security capabilities. Countries in the region are increasingly focusing on developing indigenous defense capabilities while maintaining strategic partnerships with international defense contractors.

Get Analysis on Important Geographic Markets

Download PDF

C4ISR Industry Overview

Top Companies in C4ISR Market

The C4ISR market is characterized by intense innovation and strategic maneuvering among leading players, including BAE Systems, Lockheed Martin, Northrop Grumman, Raytheon, and L3Harris Technologies. These companies are heavily investing in next-generation technologies like artificial intelligence, quantum communications, and advanced networking capabilities to enhance their product portfolios. There is a strong focus on developing integrated multi-domain C4ISR systems that can operate seamlessly across air, land, sea, space, and cyber domains. Companies are pursuing strategic partnerships and collaborations to access new technologies and markets, while also emphasizing internal R&D to maintain competitive advantages. The industry is witnessing increased investment in the miniaturization of components, enhancement of electronic warfare capabilities, and development of sophisticated command and control systems. Market leaders are also expanding their geographical presence through local partnerships and establishing regional centers of excellence to better serve military customers worldwide.

Consolidated Market with High Entry Barriers

The C4ISR market demonstrates high consolidation, with major defense contractors dominating the landscape through their established relationships with military customers and extensive technological capabilities. These large conglomerates leverage their diverse portfolios, substantial R&D budgets, and long-standing government relationships to maintain their market positions. The industry has significant barriers to entry due to the complex nature of military specifications, stringent regulatory requirements, and high capital investments needed for product development. Many smaller specialized players operate in niche segments, often serving as suppliers or technology partners to the larger prime contractors.

The market is characterized by strategic mergers and acquisitions aimed at expanding technological capabilities and market reach. Companies are actively acquiring specialized firms in areas like artificial intelligence, cybersecurity, and advanced electronics to strengthen their C4ISR offerings. There is also a trend of vertical integration, with major players acquiring key component manufacturers to secure their supply chains and enhance control over critical technologies. The industry structure favors established players who can manage complex military programs and maintain the necessary security clearances and certifications required for defense contracts.

Innovation and Integration Drive Future Success

Success in the C4ISR market increasingly depends on companies' ability to deliver integrated solutions that can operate across multiple domains while maintaining cybersecurity and operational effectiveness. Incumbent players need to continuously invest in emerging technologies and maintain strong relationships with military customers while adapting to evolving battlefield requirements. Companies must focus on developing modular, scalable architectures that can accommodate future upgrades and integrate with existing military infrastructure. The ability to provide comprehensive support services, including training, maintenance, and system upgrades, is becoming increasingly important for maintaining C4ISR market share.

For new entrants and smaller players, success lies in identifying specialized niches where they can develop unique capabilities or technologies that complement the offerings of larger contractors. Companies need to navigate complex regulatory environments while maintaining the agility to respond to rapidly changing military requirements. The increasing focus on network-centric warfare and multi-domain operations creates opportunities for innovative solutions in areas like data analytics, artificial intelligence, and autonomous systems. Building strong partnerships with established players and maintaining close relationships with military research organizations can provide crucial advantages in this highly competitive market.

C4ISR Market Leaders

-

General Dynamics Corporation

-

Northrop Grumman Corporation

-

L3Harris Technologies Inc.

-

RTX Corporation

-

THALES

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

C4ISR Market News

November 2023: Northrop Grumman Corporation received a contract from the US Navy (USN) to develop the cockpit and computer architecture of the new generation of the advanced Hawkeye (E-2D) aircraft (Delta System Software Configuration (DSSC) 6) for use by the US Marine Corps (USMC) and the US Air Force (USAF) until 2028.

October 2023: The UK announced that it was to start trials of a new 16-protector surveillance aircraft. The aircraft would undergo test flights until entering service in late 2024. A new uncrewed RAF aircraft is capable of global surveillance operations.

C4ISR Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Platform

- 5.1.1 Air

- 5.1.2 Land

- 5.1.3 Sea

- 5.1.4 Space

-

5.2 Purpose

- 5.2.1 Command, Control, Communications, and Computer (C4)

- 5.2.2 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.2.3 Electronic Warfare (EW)

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Turkey

- 5.3.5.4 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 Lockheed Martin Corporation

- 6.2.2 Northrop Grumman Corporation

- 6.2.3 Elbit Systems Ltd

- 6.2.4 BAE Systems PLC

- 6.2.5 Saab AB

- 6.2.6 THALES

- 6.2.7 RTX Corporation

- 6.2.8 L3Harris Technologies, Inc.

- 6.2.9 CACI INTERNATIONAL INC.

- 6.2.10 General Dynamics Corporation

- 6.2.11 Honeywell International Inc.

- 6.2.12 The Boeing Company

- 6.2.13 Leidos

- 6.2.14 Israel Aerospace Industries Ltd.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

C4ISR Industry Segmentation

C4ISR (command, control, communications, computer, intelligence, surveillance, and reconnaissance) refers to systems, procedures, and techniques used to collect and disseminate battlefield information.

The C4ISR market is segmented by platform, purpose, and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). By platform, the market is segmented into air, land, sea, and space. By purpose, the market is classified into command, control, communications, computer (C4), intelligence, surveillance, and reconnaissance (ISR), and electronic warfare (EW)). The report also covers the market sizes and forecasts for the C4ISR market in major countries across different regions.

For each segment, the market sizing and forecasts have been done based on value (USD).

| Platform | Air | ||

| Land | |||

| Sea | |||

| Space | |||

| Purpose | Command, Control, Communications, and Computer (C4) | ||

| Intelligence, Surveillance, and Reconnaissance (ISR) | |||

| Electronic Warfare (EW) | |||

| Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Latin America | Brazil | ||

| Mexico | |||

| Rest of Latin America | |||

| Middle-East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

C4ISR Market Research FAQs

How big is the C4ISR Market?

The C4ISR Market size is expected to reach USD 13.41 billion in 2025 and grow at a CAGR of 3.20% to reach USD 15.69 billion by 2030.

What is the current C4ISR Market size?

In 2025, the C4ISR Market size is expected to reach USD 13.41 billion.

Who are the key players in C4ISR Market?

General Dynamics Corporation, Northrop Grumman Corporation, L3Harris Technologies Inc., RTX Corporation and THALES are the major companies operating in the C4ISR Market.

Which is the fastest growing region in C4ISR Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in C4ISR Market?

In 2025, the North America accounts for the largest market share in C4ISR Market.

What years does this C4ISR Market cover, and what was the market size in 2024?

In 2024, the C4ISR Market size was estimated at USD 12.98 billion. The report covers the C4ISR Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the C4ISR Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

C4ISR Market Research

Mordor Intelligence provides a comprehensive analysis of the C4ISR market through detailed research and consulting expertise. Our extensive coverage examines global C4ISR market dynamics, including the implementation of C4ISR systems across various sectors. The report, available as an easy-to-download PDF, offers an in-depth analysis of land-based C4ISR applications and explores emerging trends in C4ISR systems market development.

Stakeholders benefit from our thorough analysis of the global C5ISR market forecast and gain regional insights into the United States C4ISR market and South America C5ISR market developments. The report examines crucial aspects of C4ISR servers deployment and integration, while providing detailed projections of global C4ISR market size. Our comprehensive assessment includes an analysis of the land platforms market and segmentation of the C5ISR market by end use, delivering actionable intelligence for strategic decision-making.