BYOD Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

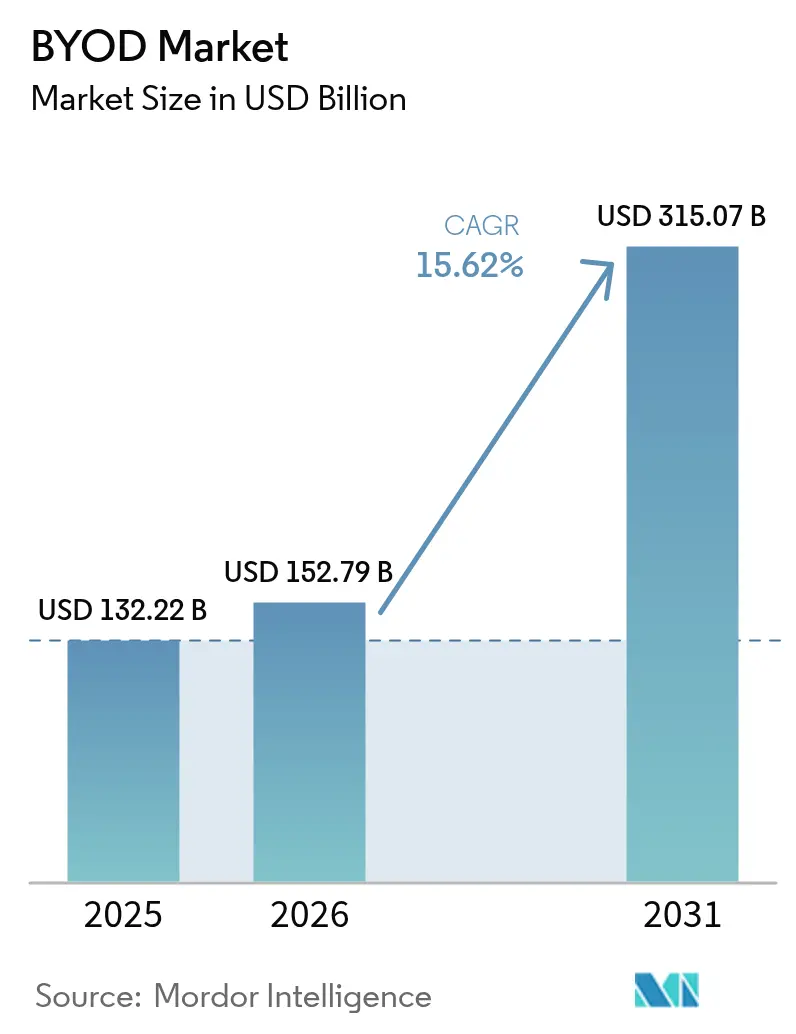

| Market Size (2026) | USD 152.79 Billion |

| Market Size (2031) | USD 315.07 Billion |

| Growth Rate (2026 - 2031) | 15.62% CAGR |

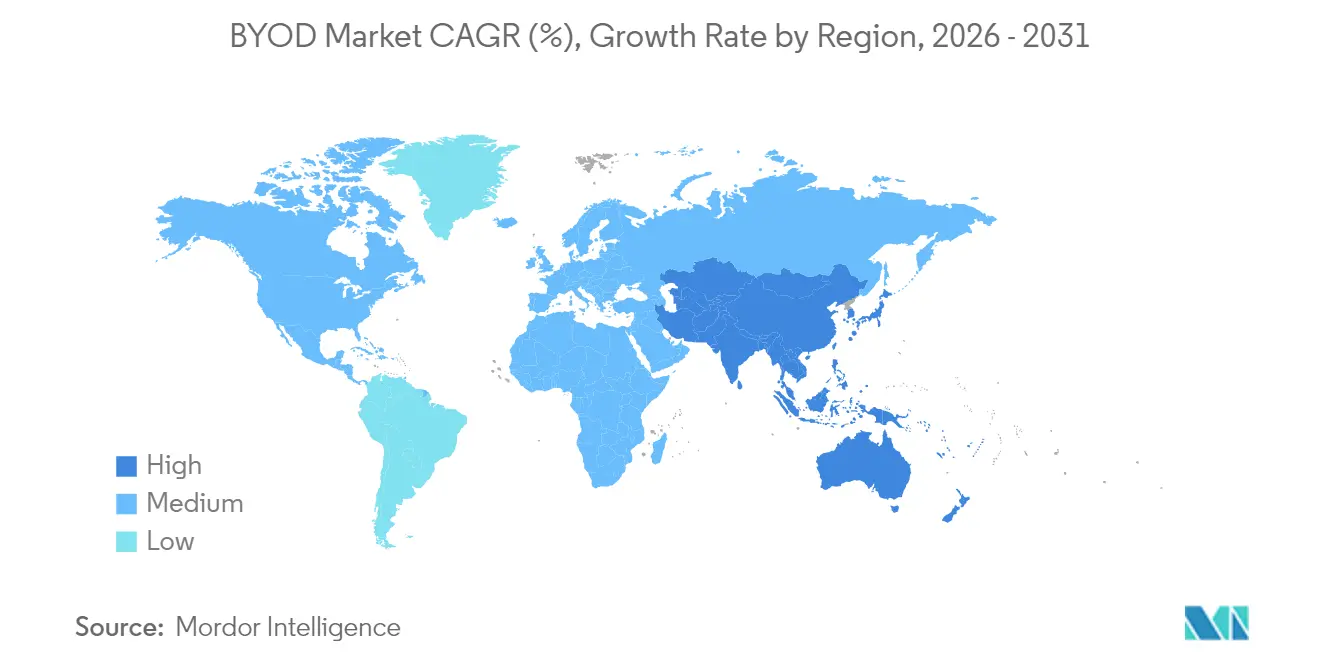

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players_Market.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

BYOD Market Analysis by Mordor Intelligence

The BYOD market size was valued at USD 132.22 billion in 2025 and estimated to grow from USD 152.79 billion in 2026 to reach USD 315.07 billion by 2031, at a CAGR of 15.62% during the forecast period (2026-2031). Demand is accelerating as permanent hybrid-work policies push enterprises to off-load device CAPEX while tightening zero-trust controls. Cloud-native UEM platforms that supervise smartphones, tablets, laptops, and emerging wearables from a single console are replacing legacy on-premise MDM deployments, allowing real-time policy enforcement and AI-assisted threat detection.[1]Microsoft, “Microsoft Intune news at Microsoft Ignite 2024,” MICROSOFT.COM At the same time, commercial 5G rollouts are creating bandwidth for data-intensive mobile workflows, enabling edge-AI capabilities that keep sensitive processing on personal devices and ease employee privacy concerns. Together, these forces are widening market opportunities for vendors that can combine identity-centric security, granular analytics, and pay-as-you-grow licensing models.

Key Report Takeaways

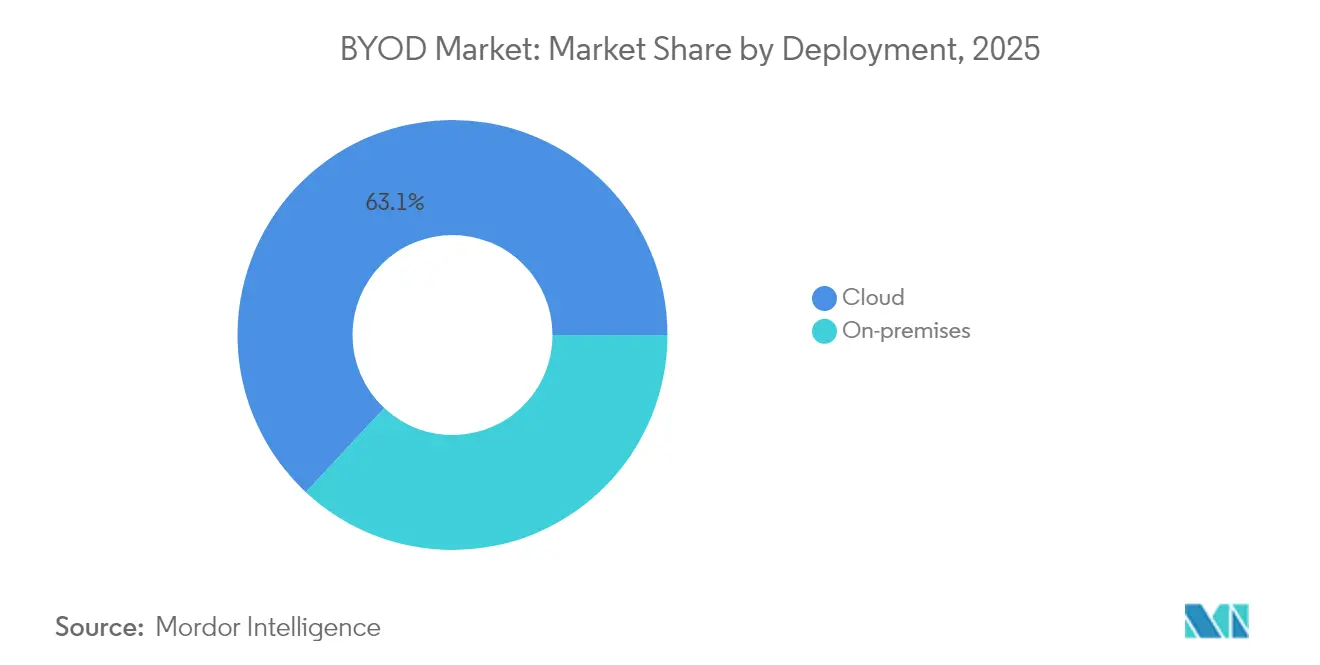

- By deployment, cloud captured 63.05% of BYOD market share in 2025, and the segment is rising at a 16.55% CAGR through 2031.

- By device type, smartphones held 48.02% of the BYOD market share in 2025, while wearables and others are projected to record the fastest 16.12% CAGR.

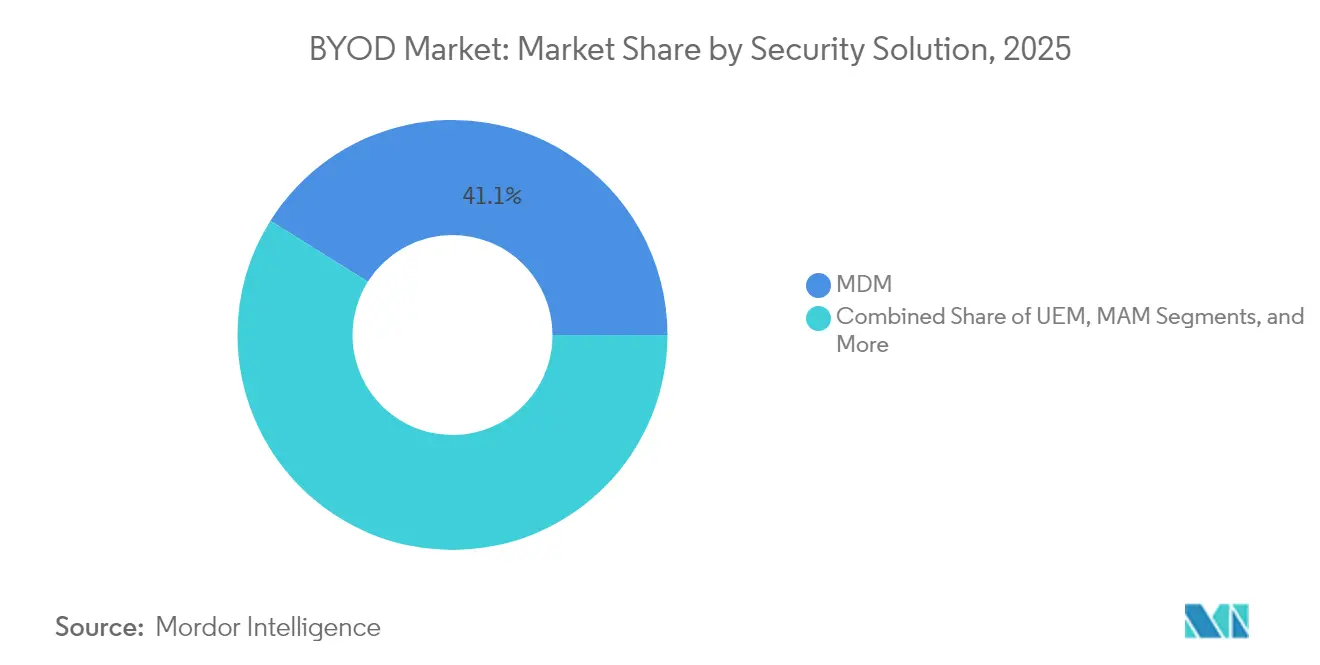

- By security solution, MDM held 41.08% of the BYOD market share in 2025, while UEM are projected to record the fastest 16.05% CAGR.

- By organization size, large enterprises held 57.02% of the BYOD market share in 2025, while SMEs are projected to record the fastest 16.20% CAGR.

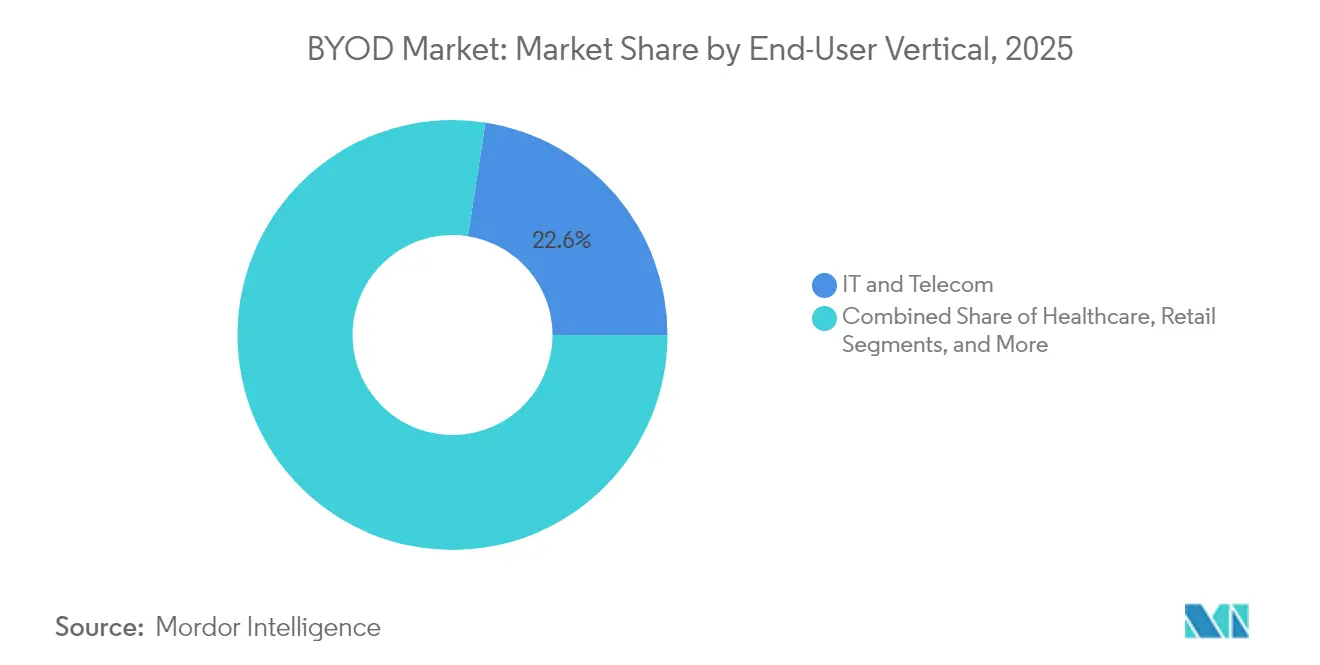

- By geography, North America accounted for 38.10% of the BYOD market size in 2025, whereas Asia Pacific is projected to lead growth at a 16.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global BYOD Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G-enabled smart devices | +3.2% | Global, with early gains in Asia Pacific, North America | Medium term (2-4 years) |

| Hybrid-work policies becoming permanent | +4.1% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Cloud-native UEM replacing legacy MDM | +3.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Zero-trust security mandates in regulated sectors | +2.9% | Global, concentrated in BFSI, Healthcare, Government | Long term (≥ 4 years) |

| Cost-containment pressure in IT budgets (device CAPEX off-load) | +1.7% | Global, particularly SMEs and cost-sensitive verticals | Short term (≤ 2 years) |

| Edge-AI on personal devices enabling secure offline workflows | +0.2% | North America, expanding to Asia Pacific and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G-Enabled Smart Devices Accelerates Enterprise Adoption

Commercial 5G standalone installations across seven APAC nations are enabling low-latency factory automation, near-real-time telemedicine, and video-rich field-service workflows, all of which run smoothly on employee-owned endpoints.[2]GSMA, “Mobile Economy Asia Pacific 2024,” GSMA.COM The GSMA projects that 5G will inject almost USD 130 billion into the APAC economy by 2030, much of it tied to smart-factory and smart-grid applications that rely on unified endpoint management. These data-heavy tasks magnify the need for AI-backed policy orchestration that optimizes bandwidth, automatically classifies sensitive traffic, and enforces compliance on the fly. Enterprises adopting private 5G networks are therefore mandating UEM solutions that combine radio-aware policy setting with behavioral analytics. Device makers are simultaneously embedding dedicated AI inference engines, allowing threat detection and data-loss prevention to run locally, which lowers cloud egress costs and keeps personal information on the edge device.

Hybrid-Work Policies Becoming Permanent Drive UEM Investment

Two-thirds of U.S. and European multinationals have now codified hybrid work as a permanent operating model. That shift forces IT teams to supervise unmanaged laptops, tablets, and phones far outside the corporate network perimeter. Cloud-native Intune tenants grew by double digits in 2024, a trend propelled by zero-touch provisioning that pushes security baselines, certificates, and application sets before the first login. Real-time analytics using Kusto Query Language provide security teams with cross-device telemetry in seconds. AI-supported copilot features triage anomalies and recommend immediate mitigation steps, shortening incident response cycles even when users connect from residential broadband. The outcome is a measurable reduction in help-desk tickets and lower mean-time-to-repair, supporting CIO mandates for leaner endpoint operations.

Cloud-Native UEM Replacing Legacy MDM Systems

Enterprises are sunsetting on-premise MDM stacks that struggle with patch cadence and device heterogeneity. Migration toward SaaS-delivered UEM unlocks rapid feature releases, API-driven automation, and elastic scaling during seasonal workforce peaks. Microsoft, VMware, and IBM each report rising attach rates for identity and analytics add-ons, underscoring buyer preference for consolidated control planes. Modern platforms secure Windows, Android, iOS, macOS, and vision-OS devices side-by-side and provide per-app micro-tunneling to isolate corporate data flows. An expanded VPP API in Apple ecosystems has slashed license assignment requests from 25,000 to 10 per bulk operation, cutting deployment times. Organizations also benefit from built-in compliance dashboards that map policy posture to ISO and GDPR checkpoints, reducing audit preparation effort.

Zero-Trust Security Mandates in Regulated Sectors

Healthcare systems in North America and Europe now insist on device-level attestation before granting access to electronic health-record portals. Government agencies are pursuing similar policies that restrict high-privilege functions to endpoints with verified OS-build numbers and active antimalware signatures. Financial institutions are extending multifactor verification by layering behavioral biometrics that monitor typing cadence and navigation patterns, flagging anomalies without interrupting productivity. AI-infused copilots review privilege elevation requests and suggest approval rules that can be auto-applied, streamlining administrative workload while maintaining audit trails. Such advancements illustrate how zero-trust frameworks have become foundational to large-scale BYOD rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cyber-insurance premiums linked to unmanaged endpoints | -1.8% | North America and EU, with spillover to Asia Pacific | Medium term (2-4 years) |

| Employee privacy pushback on intrusive agents | -1.2% | Global, particularly in EU under GDPR | Short term (≤ 2 years) |

| Fragmentation of OS/firmware versions in emerging markets | -0.9% | Asia Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Looming vendor consolidation post-Broadcom–VMware deal | -0.7% | Global, with early impact in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Cyber-Insurance Premiums Linked to Unmanaged Endpoints

Underwriters are scrutinizing mobile-device hygiene as ransomware claims spike. Organizations with insufficient endpoint visibility face premium hikes of up to 20%. Insurers increasingly require proof of continuous monitoring, policy-based encryption, and verifiable backup routines before binding coverage. Vendors respond by embedding machine-learning anomaly detection and unified reporting across mobile, desktop, and virtual machines. Automated playbooks isolate or wipe high-risk devices, creating actuarial evidence of risk mitigation. Compliance dashboards export attestation reports directly to insurers, reducing manual paperwork and improving renewal outcomes.

Employee Privacy Pushback on Intrusive Agents

European works councils often veto full-device enrollment because it exposes personal photos, messages, and location data. To comply with GDPR and uphold employee trust, enterprises are turning to application-level protection that separates corporate data into encrypted sandboxes without collecting personal telemetry. Selective-wipe features erase only business information during off-boarding, leaving personal files untouched. Edge-AI processing further limits off-device data movement by scanning for malicious activity locally. Clear policies and transparent user prompts have become critical adoption levers, proving that privacy-first design can coexist with strict security mandates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Rapid Adoption of Cloud Control Planes

The cloud segment accounted for 63.05% of BYOD market share in 2025 and is projected to expand at a 16.55% CAGR. Organizations are migrating workloads to SaaS UEM platforms that provide real-time analytics, automated remediation, and policy inheritance across employee-owned smartphones, tablets, and laptops. On-premise implementations persist in air-gapped government labs and certain defense installations, yet capital expense, upgrade cadence, and skilled-labor requirements hamper fresh expansion.

Cloud-native ecosystems offer continuous feature delivery, built-in SOC integrations, and granular role-based access controls that ease separation of duties. Microsoft’s Advanced Analytics module surfaces device compliance trends and auto-suggests conditional-access rules, tightening zero-trust postures within hours. Compliance toolkits map configurations to ISO 27001 and HIPAA checkpoints, producing audit-friendly artifacts on demand. These benefits underpin the deployment segment’s dominance and reinforce the long-term trajectory of the BYOD market.

By Device Type: Diverse Endpoints Expand the Attack Surface

Phones, tablets, and laptops remain the day-to-day productivity core, but wearables and XR headsets are rapidly entering regulated workflows. Hospitals pilot smart glasses for hands-free patient chart retrieval, while factories adopt wrist-worn scanners to streamline inventory checks. Although no single wearable category yet exceeds double-digit BYOD market share, growth is second only to cloud deployment adoption. UEM platforms now support policy-based management of sensors, cameras, and spatial-computing interfaces, reflecting a widening perimeter that must still fit within zero-trust frameworks.

Platform coverage across Windows, Android, iOS, macOS, and vision-OS underscores the requirement for cross-device troubleshooting and software distribution. Real-time patch orchestration, remote freezing, and selective data sharding keep information flows compliant even as employees toggle between devices. As spatial computing matures, expect expanded API hooks that classify visual-field data and restrict screen capture inside regulated environments.

By Security Solution: UEM Displaces Stand-Alone MDM

Mobile Device Management once dominated. Today, unified endpoint management bundles device, application, identity, and analytics layers into one control plane, compressing tool sprawl and licensing overhead. Vendors showcase AI-assisted breach prediction, behavioral biometrics for continuous authentication, and privilege-management modules that authorize time-boxed elevation. Integration with identity providers such as Azure Active Directory allows conditional access based on device risk score and user role, automating decisions that once required manual intervention.

While Mobile Application Management remains popular in privacy-sensitive EU markets, enterprises increasingly see it as a complement rather than a substitute. IAM hooks expose app-level login signals, enabling context-aware policy shifts that revoke tokens if the device becomes non-compliant. The net result: a layered defense strategy that keeps sensitive data contained without hindering user experience.

By Organization Size: Cloud Levels the Playing Field for SMEs

Large enterprises commanded 57.02% of the BYOD market share in 2025 because of vast device estates and mature security programs. Yet SMEs clock a faster 16.20% CAGR as SaaS subscriptions eliminate the need for heavy infrastructure. Zero-touch enrollment and self-service password resets lighten IT service-desk volumes, while pay-as-you-use billing aligns with fluctuating headcount. Intune tenants can now group devices at enrollment time, auto-assigning role-specific apps and policies that once required manual scripting.

SMEs benefit from built-in compliance templates that cover data-loss prevention and multi-factor authentication without dedicated security staff. Large enterprises, meanwhile, integrate telemetry into existing SIEMs, applying machine learning to predict privilege misuse. Across both cohorts, automated patch orchestration and AI-curated insights stand out as cost-justified investments.

By End-User Vertical: Regulated Sectors Lead the Charge

Healthcare providers demand HIPAA-aligned controls that encrypt PHI, restrict clipboard sharing, and enforce strict password policies. Hospitals use biometric access plus real-time risk scoring to verify clinician identity before permitting electronic health-record edits. Financial institutions focus on behavioral authentication and continuous authorization, leveraging machine-learning models to detect out-of-character activity. Government agencies deploy device attestation and geo-fencing to secure access to sensitive citizen data.

Manufacturers apply 5G-powered diagnostic apps and IoT data capture to refine predictive maintenance, pushing the boundaries of device diversity as wearables and AR headsets enter the plant floor. Retailers equip associates with mobile point-of-sale tablets that tie into inventory systems, simplifying omnichannel fulfillment. Cross-vertical expansion underscores the BYOD market’s resilience and its growing necessity across knowledge and operational workflows.

Geography Analysis

North America’s 38.10% BYOD market share stems from early adoption of zero-trust mandates and extensive cloud infrastructure. Financial-services and healthcare entities require continuous compliance evidence, fueling uptake of analytics-driven UEM platforms that inspect every device session. Federal directives referencing NIST 800-207 have further institutionalized zero-trust as a baseline, compelling even mid-market firms to upgrade legacy MDM.

Asia Pacific is the growth engine, advancing at a 16.02% CAGR. GSMA projects the regional mobile economy to surpass USD 1 trillion by 2030 on the back of 5G-enabled enterprise applications. Singapore’s Smart Nation program and Australia’s cyber-resilience policies set benchmarks that ripple across neighboring markets. Vendors with localized data centers and multilingual support command an advantage, given diverse sovereignty rules.

Europe maintains steady momentum driven by GDPR-driven privacy requirements. Works councils often limit device inspection rights, spurring demand for app-centric management and selective-wipe features that respect personal data. The Middle East and Africa trail in share yet exhibit growing interest as governments digitize public services and expand 5G coverage. Across regions, tailored compliance toolkits and in-country data residency remain pivotal selling points.

Competitive Landscape

The BYOD market remains moderately fragmented even as consolidation accelerates. Microsoft consolidates share through continuous Intune enhancements, including AI copilots that suggest remediation steps and privilege rules. VMware’s pending EUC divestiture to KKR injects uncertainty, prompting some Workspace ONE customers to reassess vendor roadmaps.[3]VMware, “VMware Named a Leader in The Forrester Wave: Unified Endpoint Management, Q4 2023,” VMWARE.COM IBM, Cisco, and Samsung Knox invest in identity-first integrations and hardware-rooted attestation to deepen differentiation.

Strategic M&A centers on identity and analytics. Microsoft absorbs niche security startups to extend behavioral detection and compliance automation. Competitors answer with open APIs and marketplace partnerships that plug advanced capabilities into existing stacks. As wearables and XR endpoints proliferate, vendors that can deliver consistent policy enforcement across non-traditional device architectures will command premium valuations.

BYOD Industry Leaders

VMware Inc.

IBM Corporation

SAP SE

Ivanti, Inc. (MobileIron)

Citrix Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Microsoft added Copilot-driven evaluation of privilege-elevation requests in Intune Endpoint Privilege Management, automating rule creation for future approvals.

- February 2025: KKR closed the acquisition of VMware’s End-User Computing division, igniting platform reassessment among Workspace ONE customers.

- November 2024: Microsoft launched Intune Advanced Analytics with KQL support, letting admins run real-time queries and trigger remote actions from the results.

- November 2024: Microsoft rolled out app-protection support for Apple Vision Pro, pairing Conditional Access with Azure Active Directory authentication.

Global BYOD Market Report Scope

Bring your own device (BYOD) is an emerging technological trend wherein employees are encouraged to utilize their own devices to access the company's enterprise system and data. Nowadays, many people and organizations face restrictions with geographical borders and long-distance collaborations within the team. BYOD conveniently manages to connect them and allows access to the required information. BYOD presents new avenues for industry players, thus positively impacting market growth over the forecast period.

The BYOD market is segmented based on deployment, industry verticals, and geography. Based on deployment, the market is segmented into on-premise and cloud. Based on end-user verticals, the market is segmented into retail, healthcare, government, energy and utility, automotive, and other end-user verticals. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa.

The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| On-Premises |

| Cloud |

| Smartphones |

| Tablets |

| Laptops |

| Wearables and Other Endpoints |

| Mobile Device Management (MDM) |

| Unified Endpoint Management (UEM) |

| Mobile Application Management (MAM) |

| Identity and Access Management (IAM) |

| Large Enterprises |

| Small and Mid-Sized Enterprises (SMEs) |

| IT and Telecom |

| Healthcare |

| Government and Public Sector |

| Retail |

| BFSI |

| Manufacturing and Automotive |

| Other End-User Verticals |

| North America |

| South America |

| Europe |

| Asia Pacific |

| Middle East and Africa |

| By Deployment | On-Premises |

| Cloud | |

| By Device Type | Smartphones |

| Tablets | |

| Laptops | |

| Wearables and Other Endpoints | |

| By Security Solution | Mobile Device Management (MDM) |

| Unified Endpoint Management (UEM) | |

| Mobile Application Management (MAM) | |

| Identity and Access Management (IAM) | |

| By Organization Size | Large Enterprises |

| Small and Mid-Sized Enterprises (SMEs) | |

| By End-User Vertical | IT and Telecom |

| Healthcare | |

| Government and Public Sector | |

| Retail | |

| BFSI | |

| Manufacturing and Automotive | |

| Other End-User Verticals | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

How large is the BYOD market in 2026?

The BYOD market size stands at USD 152.79 billion in 2026.

What CAGR is expected for BYOD between 2026 and 2031?

The market is projected to grow at a 15.62% CAGR through 2031.

Which deployment model leads in share?

Cloud deployment leads with 63.05% share, reflecting migration to SaaS-based UEM.

Which region is forecast to be the fastest growing?

Asia Pacific is forecast to rise at a 16.02% CAGR thanks to 5G and digitization programs.

What is driving SME adoption of BYOD solutions?

SMEs favor subscription-based UEM platforms that reduce upfront costs and automate security.

How are insurers influencing BYOD security practices?

Higher cyber-insurance premiums for unmanaged devices are pushing firms to adopt continuous endpoint monitoring and automated remediation.

Page last updated on: