| Study Period | 2024 - 2030 |

| Market Size (2025) | USD 153.65 Billion |

| Market Size (2030) | USD 177.26 Billion |

| CAGR (2025 - 2030) | 2.90 % |

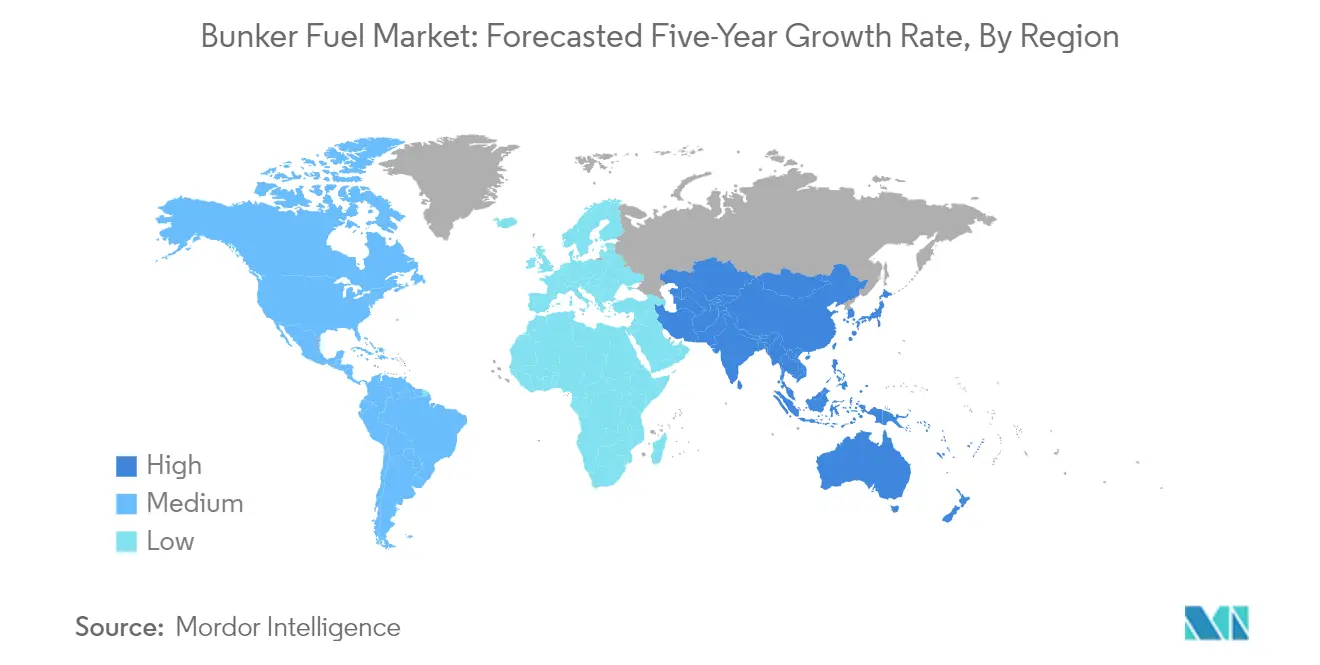

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

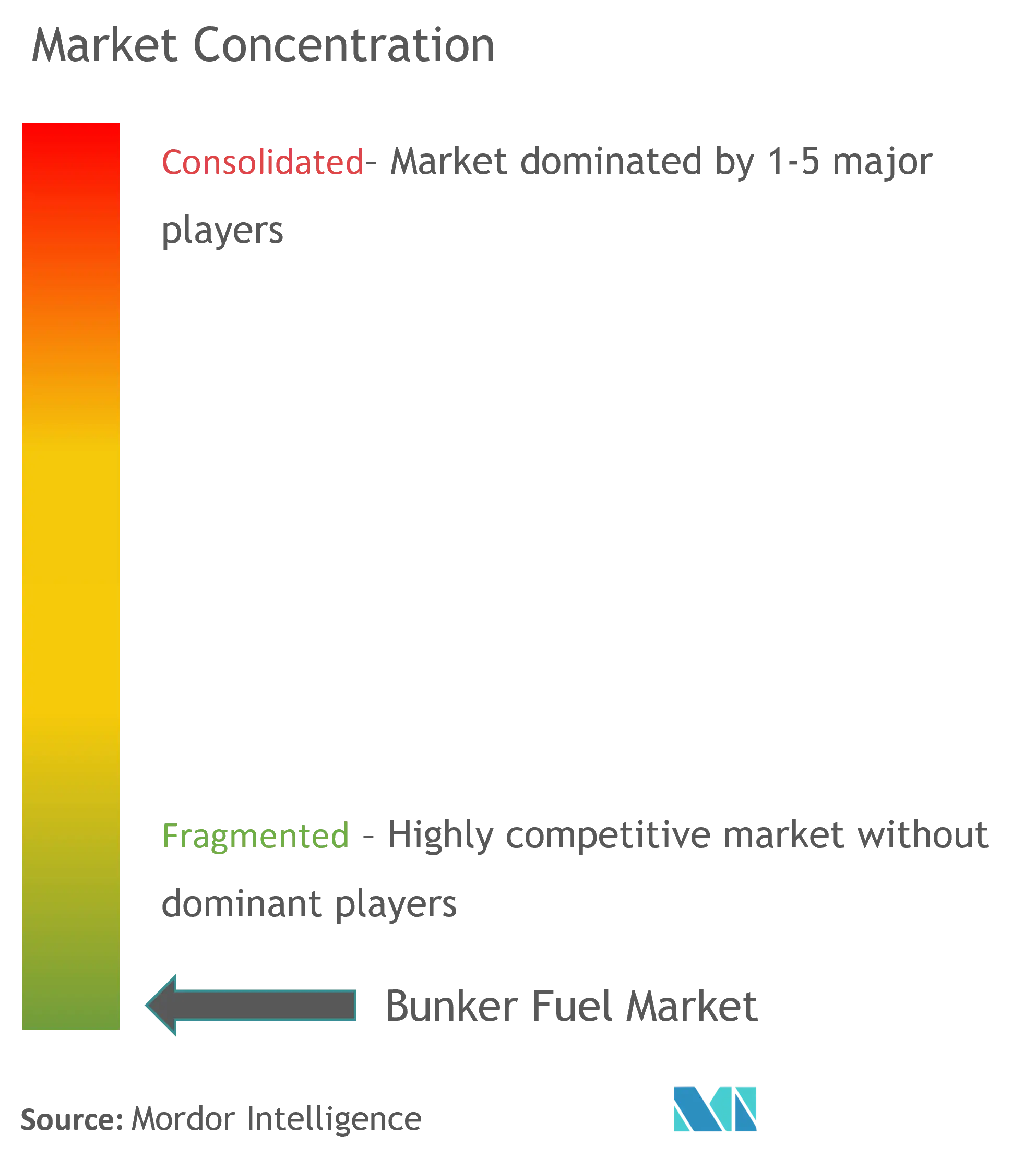

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Bunker Fuel Market Analysis

The Bunker Fuel Market size is estimated at USD 153.65 billion in 2025, and is expected to reach USD 177.26 billion by 2030, at a CAGR of 2.9% during the forecast period (2025-2030).

The bunker fuel industry is undergoing a significant transformation driven by environmental regulations and technological advancements. The shipping industry's commitment to using LNG as a marine fuel continues to grow, with classification society DNV reporting 251 LNG-fueled vessels in operation and 403 more on order or under construction as of 2023. This transition is supported by the development of LNG bunkering infrastructure across major ports globally, with 33 LNG bunkering vessels and 141 LNG ports operational, and an additional 170 LNG ports expected to become operational by the end of 2024.

The maritime sector is witnessing substantial investments in infrastructure modernization and capacity expansion. In 2023, major ports worldwide have reported increased cargo handling capabilities, with the Port of Shanghai reaching over 47.03 million TEU in container throughput. Significant investments are being made in bunker fuel infrastructure, exemplified by ADNOC's expansion of storage capacity in Fujairah through the construction of underground caverns capable of storing 42 million barrels of oil, while Ecomar Energy Solutions and Brooge Petroleum are investing in refining and marine fuel storage facilities.

The industry is experiencing a shift in trade patterns and fuel preferences, particularly in response to environmental regulations. In March 2022, TotalEnergies Marine Fuels achieved a milestone with its first marine bio-VLSFO bunker delivery in Singapore port's waters, demonstrating the growing adoption of alternative fuels. The marine fuel market has also seen the emergence of new bunkering solutions, with companies like Yara International and Azane Fuel Solutions signing commercial agreements in April 2022 to establish carbon-free ammonia fuel bunker networks in Scandinavia.

Port infrastructure development continues to accelerate, with significant investments in modernization and capacity expansion. In September 2021, Aramco Trading Company initiated commercial bunkering operations at the Yanbu Industrial Port, while Maersk Saudi Arabia announced a USD 136 million investment over 25 years to develop the region's first Integrated Logistics Park at Jeddah Islamic Port. These developments are complemented by the growing adoption of digital technologies and automation in port operations, enhancing efficiency and reducing operational costs in the marine fuel supply process.

Bunker Fuel Market Trends

Increasing Natural Gas Trade

The growing adoption of natural gas as a cleaner energy source has significantly driven the bunker fuel market, particularly in the LNG segment. Natural gas has emerged as a preferred alternative to traditional petroleum products and fossil fuels like coal, primarily due to its lower carbon emissions profile. This shift has been particularly evident since the Paris Agreement with the United Nations Framework Convention on Climate Change (UNFCCC), which has prompted governments worldwide to set ambitious CO2 reduction targets and embrace cleaner technologies like renewables and natural gas-fired power plants for electricity generation.

The increasing trade volumes of LNG have created a robust infrastructure network that supports the bunker fuel market. China has emerged as the world's largest LNG importer, recording imports of approximately 79.9 million tons (MT) in 2021, surpassing Japan, which imported 74.3 MT. South Korea has also shown significant growth in LNG imports, with a 15.3% year-on-year increase to 46.1 million tons, driven by the country's transition towards natural gas and renewables to replace coal and nuclear power. This expanding trade network has necessitated the development of specialized vessels and bunkering facilities, creating a positive feedback loop that further drives market growth. Additionally, the market is influenced by marine fuel trading dynamics, which are crucial for understanding bunker fuel price trends.

Understand The Key Trends Shaping This Market

Download PDF

Rising Number of LNG-Fueled Fleet

The maritime industry has demonstrated a strong commitment to adopting LNG as a marine fuel, evidenced by the significant growth in LNG-fueled vessel orders and deliveries. According to classification society DNV, there were 251 LNG-fueled vessels in operation and 403 more on order or under construction in 2021. The industry is projected to have at least 864 LNG-fueled vessels in the global fleet by 2028, representing a substantial transformation in marine fuel preferences. This growth is supported by the expanding LNG bunkering infrastructure, with 33 LNG bunkering vessels and 141 LNG ports operational as of January 2022, and plans for an additional 170 LNG ports to become operational.

The transition to LNG-fueled vessels is further accelerated by the significant environmental benefits and operational advantages they offer. LNG as a marine fuel provides approximately a 23% reduction in greenhouse gas emissions compared to conventional heavy fuel oil, while also reducing sulfur oxide emissions by 100% and nitrogen oxide emissions by about 85%. Recent industry developments highlight this trend, such as Mitsui OSK Lines' agreement in July 2021 to build their first LNG-fueled capesize bulk carrier, equipped with a state-of-the-art WinGD-made dual-fuel slow-speed diesel engine. Additionally, strategic partnerships like the May 2022 agreement between Titan LNG and Brittany Ferries for LNG supply to two new LNG-fueled hybrid Ro-Pax vessels demonstrate the industry's continued commitment to LNG adoption. This shift towards alternative marine fuel options is also supported by the availability of low sulfur fuel oil and very low sulfur fuel oil, which are increasingly being used in conjunction with LNG to meet environmental regulations.

Segment Analysis: Fuel Type

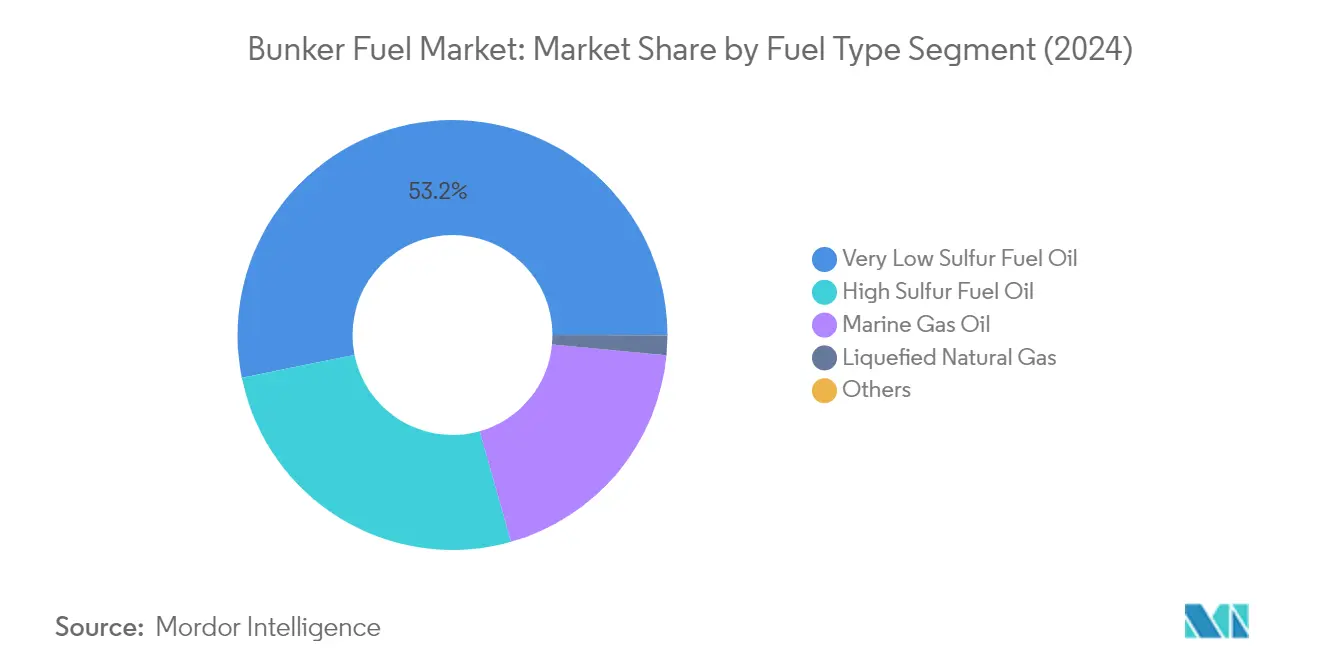

Very Low Sulfur Fuel Oil (VLSFO) Segment in Bunker Fuel Market

Very Low Sulfur Fuel Oil (VLSFO) has emerged as the dominant segment in the global bunker fuel market, commanding approximately 53% market share in 2024. This substantial market position is primarily driven by the International Maritime Organization's (IMO) 2020 regulations mandating a 0.5% sulfur content limit for marine fuels. The segment's leadership is further strengthened by the widespread availability of very low sulfur fuel oil at major ports worldwide and its compatibility with existing ship engines without requiring significant modifications. Major oil companies and refineries have invested heavily in VLSFO production facilities to meet the growing demand, while ports across Europe, Asia-Pacific, and the Americas have expanded their VLSFO bunkering infrastructure. The segment's dominance is also supported by its cost-effectiveness compared to alternative compliant fuels like marine gas oil.

Liquefied Natural Gas (LNG) Segment in Bunker Fuel Market

The Liquefied Natural Gas (LNG) segment is experiencing remarkable growth in the bunker fuel market, driven by increasing environmental regulations and the shipping industry's push towards cleaner fuel alternatives. The segment's expansion is supported by significant investments in LNG bunkering infrastructure across major ports globally, particularly in Singapore, Europe, and North America. The growing order book for LNG-powered vessels, with numerous shipping companies opting for LNG-fueled ships in their new builds, further accelerates this growth. The development of ship-to-ship LNG transfer facilities, establishment of new LNG bunker vessels, and government initiatives promoting LNG as a marine fuel are creating a robust ecosystem for this segment's expansion. Additionally, LNG's ability to reduce greenhouse gas emissions by approximately 23% compared to conventional marine fuels makes it an attractive option for shipping companies aiming to meet future environmental regulations.

Remaining Segments in Fuel Type

The remaining segments in the bunker fuel market include high sulfur fuel oil (HSFO), marine gas oil (MGO), and other alternative fuels such as methanol and biodiesel. HSFO continues to maintain a significant presence in the market, primarily used by vessels equipped with scrubber systems that allow them to comply with emission regulations while using higher sulfur content fuel. Marine Gas Oil serves as a crucial transition fuel, particularly popular among smaller vessels and in regions with stricter emission controls. The alternative fuels segment, though currently small, is gaining attention as the industry explores various options for meeting future environmental regulations. These segments collectively provide a diverse range of options for different vessel types and operational requirements, contributing to the market's overall dynamics and evolution towards cleaner fuel alternatives.

Segment Analysis: Vessel Type

Bulk Carrier Segment in Global Bunker Fuel Market

The bulk carrier segment dominates the global bunker fuel market, accounting for approximately 47% of the total market share in 2024. This dominance is primarily attributed to the massive fleet of bulk carriers operating globally, with around 913 million deadweight tons (dwt) of bulk carriers in operation, representing 42.7% of the global fleet market. The segment's leadership position is further strengthened by increasing commodity trading across the globe and significant projections for growing global seaborne bulk trade. Major ports like the Port of Dampier and Port of Hedland in Australia handle substantial bulk carrier traffic, with the Port of Dampier alone handling 12 million metric tons of iron ore through bulk carriers. The segment's robust performance is also supported by continued investments in new bulk carrier vessels, as demonstrated by recent developments like Kawasaki Heavy Industries' delivery of the bulk carrier World Royal with a capacity of 61,000 DWT.

Tankers Segment in Global Bunker Fuel Market

The tankers segment is experiencing rapid growth in the bunker fuel market, driven by increasing global demand for oil and gas transportation. The segment's growth is fueled by rising investments in new tanker vessels and expanding trade routes. The market is witnessing significant developments in tanker operations, particularly with the surge in single oil tanker freight rates. For instance, vessels like the Pluto Moon, carrying crude oil from Africa to the United Kingdom, have seen substantial rate increases. The growth is further supported by the expansion of tanker fleets globally, with the deadweight tons (dwt) of tanker ships increasing from 601 million dwt in 2020 to 619 million dwt in 2021. The segment's expansion is also driven by the diversification of trade routes and increasing demand for various types of tankers including small tankers, intermediate tankers, medium-range tankers, and very large crude carriers (VLCC).

Remaining Segments in Vessel Type

The container, general cargo, and other vessel types segments play crucial roles in the bunker fuel market. The container segment serves the growing container ship fuel market, handling various industrial products and maintaining steady growth despite market fluctuations. The general cargo segment caters to diverse cargo needs, offering flexibility in operational activities and the ability to carry containers, bulk, or bagged cargo. The other vessel types segment, including passenger ferries, cruise ships, and offshore support vehicles (OSV), contributes to the market's diversity by serving specialized transportation needs and supporting offshore operations. These segments collectively enhance the market's robustness by catering to different maritime transportation requirements and maintaining operational diversity in the global shipping industry.

Bunker Fuel Market Geography Segment Analysis

Bunker Fuel Market in North America

The North American bunker fuel market holds approximately 11% of the global market share in 2024, establishing itself as a significant regional market. The region's strategic position between the North Pacific and North Atlantic routes, which represent the world's first and second-largest trade routes by value, has been instrumental in maintaining its market position. The United States continues to be the dominant force in the region's maritime industry, with almost every state having significant ports. The region's bunker fuel market is characterized by strong infrastructure development, particularly in LNG bunkering facilities, and robust regulatory compliance with IMO 2020 sulfur regulations. The market is further strengthened by Canada's extensive coastline and Mexico's growing maritime trade activities. The presence of major international shipping routes and well-developed port infrastructure continues to drive demand for various types of bunker fuels, including VLSFO, MGO, and LNG. The region's focus on environmental regulations and sustainable shipping practices has led to increased adoption of cleaner fuel alternatives, particularly in emission control areas along the coastlines.

Bunker Fuel Market in Asia-Pacific

The Asia-Pacific bunker fuel market has demonstrated remarkable growth, recording an increase of approximately 85% from 2019 to 2024, establishing itself as the largest regional market globally. The region's dominance is anchored by major maritime nations, including China, Singapore, Japan, and South Korea. Singapore maintains its position as a global bunkering hub, while China's extensive port infrastructure and growing maritime trade continue to drive substantial demand for bunker fuels. The market is characterized by significant investments in bunkering infrastructure, particularly in developing LNG bunkering capabilities and compliant fuel alternatives. The region's robust shipping activities, extensive coastlines, and strategic location along major global trade routes have contributed to its market leadership. The presence of major container ports, growing intra-regional trade, and increasing focus on environmental compliance have shaped the market dynamics. The region's bunker fuel ecosystem is supported by well-developed supply chains, advanced port facilities, and strategic partnerships between major industry players.

Bunker Fuel Market in Europe

The European bunker fuel market is projected to grow by approximately 9% from 2024 to 2029, driven by the region's stringent environmental regulations and leadership in sustainable shipping practices. The region's market is characterized by advanced infrastructure for alternative fuels, particularly in LNG bunkering capabilities. Major ports in Rotterdam, Hamburg, and Antwerp continue to serve as crucial bunkering hubs, offering comprehensive fuel solutions to the maritime industry. The market is shaped by the European Union's ambitious environmental targets and the region's commitment to reducing maritime emissions. The presence of Emission Control Areas (ECAs) in European waters has accelerated the adoption of compliant fuels and innovative bunkering solutions. The region's strong focus on technological advancement, particularly in green hydrogen and ammonia as future marine fuels, positions it at the forefront of sustainable shipping initiatives. The market benefits from well-established regulatory frameworks, sophisticated port infrastructure, and strong collaboration between industry stakeholders.

Bunker Fuel Market in South America

The South American bunker fuel market continues to evolve, driven by Brazil's leadership in the maritime sector and growing regional trade activities. The region's market dynamics are influenced by its strategic position along major shipping routes and significant investments in port infrastructure. The availability of low-sulfur crude oil in Brazil has positioned the region favorably in the global bunker fuel supply chain, particularly for IMO 2020 compliant fuels. The market is characterized by ongoing developments in bunkering infrastructure, particularly in major ports along the Atlantic coast. Regional cooperation and trade agreements have fostered increased maritime activities, supporting steady growth in bunker fuel demand. The market's development is further supported by modernization efforts in port facilities, growing export activities, and increasing focus on environmental compliance. The region's rich natural resources and growing energy sector continue to attract international shipping traffic, sustaining demand for various grades of bunker fuels.

Bunker Fuel Market in Middle East & Africa

The Middle East & Africa bunker fuel market demonstrates strong potential, leveraging its strategic location along major global shipping routes and significant oil production capabilities. The region's market is anchored by major bunkering hubs in the UAE, particularly Fujairah, which serves as a crucial refueling point for vessels traveling between Asia and Europe. The market benefits from the region's substantial oil production capacity and well-developed maritime infrastructure. Growing investments in port facilities and bunkering capabilities, particularly in the Gulf region, continue to enhance the market's competitive position. The African continent's emerging maritime sector, driven by increasing trade activities and port development initiatives, contributes to market growth. The region's focus on diversifying its maritime services and developing LNG bunkering capabilities reflects its adaptation to evolving industry requirements. The market's dynamics are further influenced by the region's strategic importance in global energy trade and its growing role in international shipping routes.

Get Analysis on Important Geographic Markets

Download PDF

Bunker Fuel Industry Overview

Top Companies in Bunker Fuel Market

The bunker fuel market is dominated by major oil and gas conglomerates, including ExxonMobil, Shell, BP, TotalEnergies, and Chevron, alongside specialized marine fuel companies. These companies are increasingly focusing on developing low-sulfur and alternative bunker fuel to comply with IMO regulations while maintaining operational efficiency. Strategic investments in LNG bunkering infrastructure and green fuel technologies demonstrate the industry's commitment to sustainability. Companies are expanding their geographical presence through strategic partnerships and acquisitions, particularly in major maritime routes and emerging markets. The market leaders are also enhancing their digital capabilities, implementing automated solutions for vessel management, and developing innovative services to optimize fuel efficiency and reduce operational costs.

Consolidated Market with Strong Regional Players

The marine fuel industry exhibits a moderately consolidated structure with a mix of global oil majors and regional specialists. The top tier comprises integrated oil and gas companies that leverage their vertical integration capabilities, from refining to distribution, providing them significant competitive advantages in terms of supply chain control and pricing power. Regional players maintain strong positions in specific geographical markets through specialized knowledge of local regulations and established relationships with port authorities and shipping companies. The market has witnessed strategic consolidations through joint ventures and partnerships, particularly in emerging markets and new bunkering hubs.

The competitive dynamics are shaped by the presence of both traditional fuel suppliers and emerging alternative fuel providers. Major oil companies are increasingly acquiring or partnering with smaller, specialized firms to expand their alternative fuel capabilities, particularly in LNG bunkering and biofuels. The market also sees active participation from marine fuel trading companies and independent suppliers who maintain competitive positions through specialized services and flexible pricing strategies. Port operators and maritime service providers are increasingly integrating bunkering services into their offerings, adding another layer of competition to the market structure.

Innovation and Sustainability Drive Future Success

Success in the bunker fuel market increasingly depends on companies' ability to balance traditional fuel supply with investment in sustainable alternatives. Market leaders are strengthening their positions through significant investments in LNG infrastructure, development of low-carbon fuels, and digitalization of operations. For new entrants and smaller players, specialization in niche markets, such as specific geographical regions or alternative fuels, presents viable growth opportunities. The ability to provide comprehensive solutions, including technical support, digital monitoring, and environmental compliance services, is becoming crucial for maintaining competitive advantage.

The market's future competitive landscape will be significantly influenced by environmental regulations and shipping companies' sustainability goals. Companies that can provide cost-effective solutions for emission reduction while maintaining reliable marine fuel supply networks will gain competitive advantages. The increasing focus on supply chain transparency and fuel quality assurance creates opportunities for technology-driven solutions and specialized services. Success factors also include the ability to manage price volatility through hedging mechanisms and long-term supply agreements, while maintaining flexibility to adapt to changing market conditions and customer requirements.

Bunker Fuel Market Leaders

-

Exxon Mobil Corporation

-

BP Plc

-

Royal Dutch Shell Plc

-

Gazpromneft Marine Bunker LLC

-

TotalEnergies SE

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Bunker Fuel Market News

- May 2024: NYK Line collaborated with the Global Centre for Maritime Decarbonization (GCMD), based in Singapore, for a six-month project to trial marine biofuel for bunkering. The companies are expected to test a biofuel blend comprising 24% fatty acid methyl esters (FAME) and very low sulfur fuel oil (VLSFO) on a short-sea vehicle carrier, making stops at various ports.

- April 2024: French oil major TotalEnergies set up a joint venture with the Oman National Oil Company to supply liquified natural gas as a marine fuel. Marsa LNG Gas will cover upstream gas production and downstream gas liquefaction. LNG production is expected to start in the first quarter of 2028.

Bunker Fuel Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increased LNG Trade Worldwide

- 4.5.1.2 Increasing Dependencies over Natural Gas for Power Generation

- 4.5.2 Restraints

- 4.5.2.1 Environmental Concerns and the Strict Regulations Related to Emissions from the Maritime Industry

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5. MARKET SEGMENTATION

-

5.1 Fuel Type

- 5.1.1 High Sulfur Fuel Oil (HSFO)

- 5.1.2 Very Low Sulfur Fuel Oil (VLSFO)

- 5.1.3 Marine Gas Oil (MGO)

- 5.1.4 Liquefied Natural Gas (LNG)

- 5.1.5 Other Fuel Types

-

5.2 Vessel Type

- 5.2.1 Containers

- 5.2.2 Tankers

- 5.2.3 General Cargo

- 5.2.4 Bulk Carriers

- 5.2.5 Other Vessel Types

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 NORDIC

- 5.3.2.6 Turkey

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Fuel Suppliers

- 6.3.1.1 ExxonMobil Corporation

- 6.3.1.2 Shell PLC

- 6.3.1.3 Gazpromneft Marine Bunker LLC

- 6.3.1.4 BP PLC

- 6.3.1.5 PJSC Lukoil Oil Company

- 6.3.1.6 TotalEnergies SE

- 6.3.1.7 Chevron Corporation

- 6.3.1.8 Clipper Oil

- 6.3.1.9 Gulf Agency Company Ltd

- 6.3.1.10 Bomin Bunker Holding GmbH & Co. KG

- 6.3.2 Ship Owners

- 6.3.2.1 AP Moeller Maersk AS

- 6.3.2.2 Mediterranean Shipping Company SA

- 6.3.2.3 China COSCO Shipping Corporation Limited

- 6.3.2.4 CMA CGM Group

- 6.3.2.5 Hapag-Lloyd AG

- 6.3.2.6 Ocean Network Express

- 6.3.2.7 Evergreen Marine Corp Taiwan Ltd

- 6.3.2.8 Yang Ming Marine Transport Corporation

- 6.3.2.9 HMM Co. Ltd

- 6.3.2.10 Pacific International Lines Pte Ltd

- 6.3.3 List of Other Prominent Companies

- 6.3.4 Market Ranking Analysis

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Risisng Demand for Marine Transportation and Increasing Number of Ships in Operation

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Bunker Fuel Industry Segmentation

Bunker fuel is the general term given to any fuel poured into a ship's bunkers to power its engines. Deep-sea cargo ships typically burn the heavy, residual oil left over after gasoline, diesel, and other light hydrocarbons are extracted from crude oil during the refining process.

The bunker fuels market is segmented by fuel type, vessel type, and geography. By fuel type, the market is segmented into high sulfur fuel oil (HSFO), very low sulfur fuel oil (VLSFO), marine gas oil (MGO), liquefied natural gas (LNG), and other fuel types. By vessel type, the market is segmented into containers, tankers, general cargo, bulk carriers, and other vessel types. The report also covers the sizes and forecasts for the bunker fuels market across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Fuel Type | High Sulfur Fuel Oil (HSFO) | ||

| Very Low Sulfur Fuel Oil (VLSFO) | |||

| Marine Gas Oil (MGO) | |||

| Liquefied Natural Gas (LNG) | |||

| Other Fuel Types | |||

| Vessel Type | Containers | ||

| Tankers | |||

| General Cargo | |||

| Bulk Carriers | |||

| Other Vessel Types | |||

| Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Spain | |||

| NORDIC | |||

| Turkey | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Thailand | |||

| Indonesia | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| South Africa | |||

| Nigeria | |||

| Qatar | |||

| Egypt | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Bunker Fuel Market Research FAQs

How big is the Bunker Fuel Market?

The Bunker Fuel Market size is expected to reach USD 153.65 billion in 2025 and grow at a CAGR of 2.9% to reach USD 177.26 billion by 2030.

What is the current Bunker Fuel Market size?

In 2025, the Bunker Fuel Market size is expected to reach USD 153.65 billion.

Who are the key players in Bunker Fuel Market?

Exxon Mobil Corporation, BP Plc, Royal Dutch Shell Plc, Gazpromneft Marine Bunker LLC and TotalEnergies SE are the major companies operating in the Bunker Fuel Market.

Which is the fastest growing region in Bunker Fuel Market?

Middle East and Africa is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Bunker Fuel Market?

In 2025, the Asia Pacific accounts for the largest market share in Bunker Fuel Market.

What years does this Bunker Fuel Market cover, and what was the market size in 2024?

In 2024, the Bunker Fuel Market size was estimated at USD 149.19 billion. The report covers the Bunker Fuel Market historical market size for years: 2024. The report also forecasts the Bunker Fuel Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Bunker Fuel Market Research

Mordor Intelligence provides a comprehensive analysis of the bunker fuel market, utilizing extensive expertise in the marine fuel industry. Our detailed report examines a wide range of ship fuel types, including marine gas oil, heavy fuel oil, and low sulfur fuel oil. The analysis covers essential aspects of marine fuel supply chains, marine fuel bunkering operations, and maritime fuel distribution networks. Our research includes both traditional vessel fuel solutions and emerging alternative marine fuel technologies. These insights are available in an easy-to-read report PDF format.

The report offers valuable intelligence for marine fuel companies and stakeholders across the marine fuel industry. It provides in-depth coverage of marine fuel trading, marine fuel logistics, and marine fuel storage infrastructure. Our analysis includes a detailed examination of container ship fuel consumption patterns and bunker fuel price trends. It also tracks the industry's transition to compliance with very low sulfur fuel oil standards. The comprehensive research supports strategic decision-making for companies involved in marine diesel oil distribution and marine bunker fuel operations. Downloadable insights illuminate current market dynamics and future opportunities.