Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Volume (2025) | 4.75 gigawatt |

| Market Volume (2030) | 8.25 gigawatt |

| Growth Rate (2025 - 2030) | 11.67% CAGR |

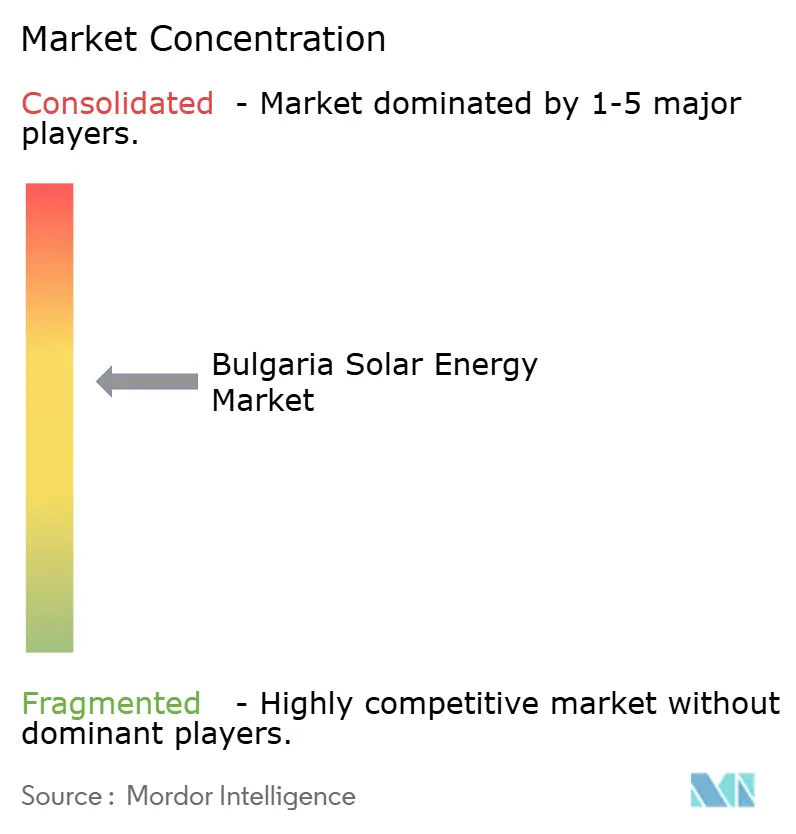

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bulgaria Solar Energy Market Analysis by Mordor Intelligence

The Bulgaria Solar Energy Market size in terms of installed base is expected to grow from 4.75 gigawatt in 2025 to 8.25 gigawatt by 2030, at a CAGR of 11.67% during the forecast period (2025-2030).

Growth is anchored in the nation’s exit from coal, reinforced by the November 2024 auction that awarded 3 GW of new solar rights, nearly doubling the installed base in one round. Declining module prices, record-high household electricity tariffs, and the rise of corporate PPAs together push solar from a supplementary fuel to the backbone of Bulgaria’s post-coal grid.[1]Fraunhofer ISE, “PV Price Monitor Q4 2024,” fraunhofer.de Competition is sharpening as international suppliers fight on price while domestic EPC firms exploit local permitting know-how to secure construction mandates. Grid congestion and a shortage of certified installers remain headwinds, yet hybrid parks pairing PV with storage and a fast-growing rooftop segment temper these risks.

Key Report Takeaways

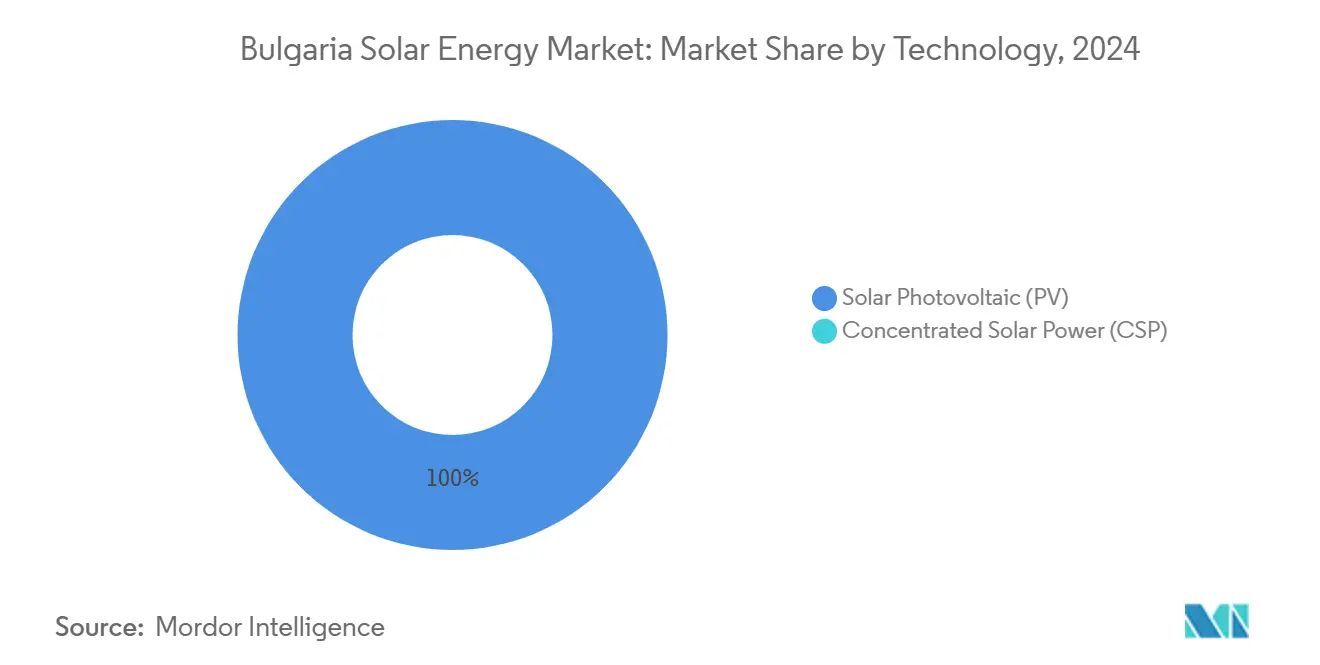

- By technology, solar PV captured 100% of the Bulgarian solar energy market share in 2024 and is set to advance at an 11.7% CAGR through 2030.

- By grid type, on-grid systems accounted for 95.1% of capacity in 2024, while the same segment is forecast to expand at a 12.1% CAGR to 2030.

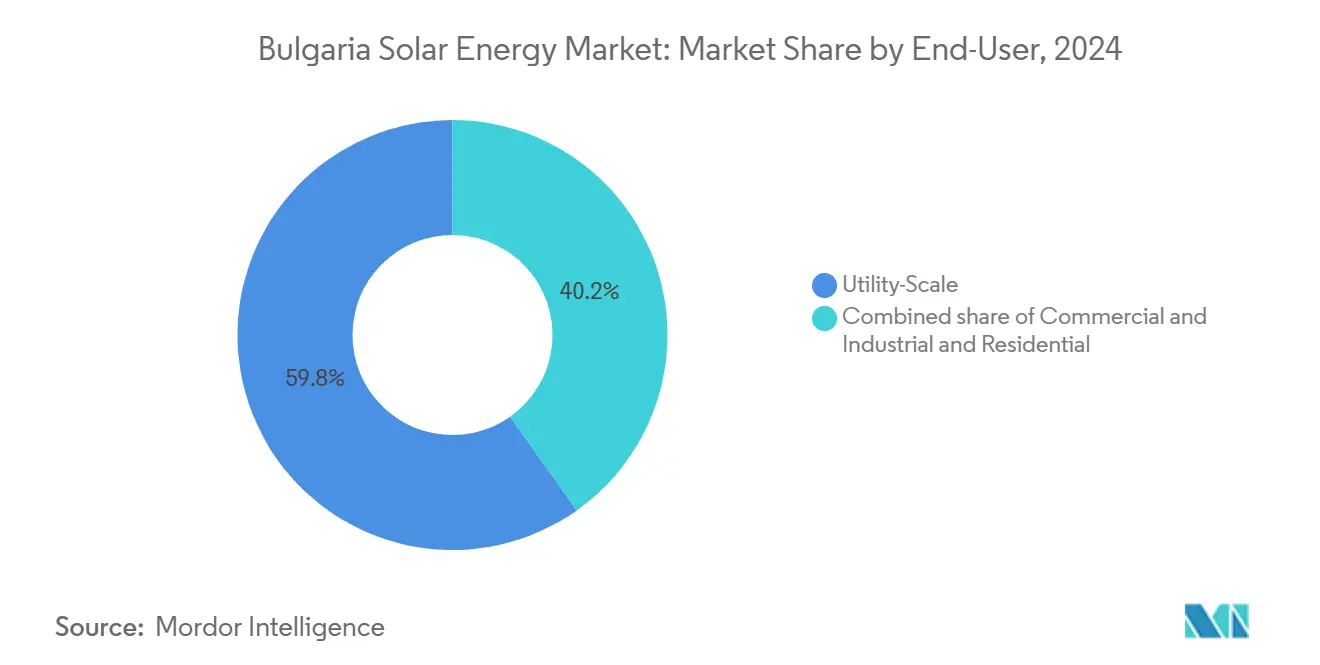

- By end user, utility-scale plants held 59.8% of installed capacity in 2024, whereas the residential segment is poised for the fastest growth at a 14.9% CAGR through 2030.

- By geography, the southern and eastern provinces—Burgas, Stara Zagora, Plovdiv, and Haskovo—contributed roughly 65% of installed capacity in 2024 and will maintain leadership with a double-digit CAGR to 2030.

Bulgaria Solar Energy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal & NECP-linked procurement pipeline | +3.2% | National, south & east focus | Medium term (2-4 years) |

| Corporate PPAs from data centers & heavy industry | +1.8% | National, early in Sofia & Burgas | Medium term (2-4 years) |

| Declining LCOE of mono-PERC & TOPCon modules | +2.5% | National | Short term (≤ 2 years) |

| Grid-constrained hybrid parks pairing PV with batteries | +1.4% | Southern & eastern Bulgaria | Medium term (2-4 years) |

| Agro-PV pilots in the grain belt | +0.9% | Northern & central Bulgaria | Long term (≥ 4 years) |

| Surplus-power monetization via IBEX | +1.3% | National, cross-border to GR & RO | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Green Deal & NECP-linked procurement pipeline

Bulgaria’s National Energy and Climate Plan mandates 27% renewables by 2030, requiring about 5 GW of new solar beyond 2024 levels. The November 2024 auction issued 3 GW of solar rights at EUR 55/MWh, 30% below the former feed-in tariff, proving solar’s cost leadership and pivoting procurement from administratively set rates to competitive tenders. Multilateral lenders have responded: IFC and Raiffeisen Bank International closed EUR 90 million of non-recourse debt for the 225 MW St. George park in October 2024, underscoring confidence in tender-backed pipelines.[2]IFC, “IFC finances St. George Solar Park,” ifc.org Winners must now secure grid capacity within 18 months or forfeit bid bonds, favoring developers with integrated land and EPC teams ESO.BG. This framework compresses project timelines and accelerates commissioning, directly lifting the Bulgarian solar energy market.

Corporate PPAs from data-centres & heavy industry

Rezolv Energy signed Bulgaria’s first virtual PPA in 2024, covering 110 GWh per year for Ardagh Group over 12 years and locking prices around EUR 0.11/kWh, 20% below average industrial tariffs. High tariffs, averaging EUR 0.14/kWh in 2024, make PPAs an immediate hedge for energy-intensive firms. Aurubis Bulgaria earmarked BGN 800 million through 2027 to build 41 MWp of on-site PV, cutting grid purchases by 15%. Data-center operators planning Sofia and Burgas sites require hourly 100% renewable matching by 2025 under corporate mandates, and IBEX’s 15-minute settlement now supports granular certificate tracking IBEX.BG. These corporate deals inject long-term cash flows, lowering financing costs and deepening the Bulgarian solar energy market.

Declining LCOE of mono-PERC & TOPCon modules

Spot prices for PERC fell to EUR 0.10/W and TOPCon to EUR 0.115/W in late 2024, down more than 40% year on year, as Chinese n-type capacity surged to 70% of global output. TOPCon’s 24% efficiency trims balance-of-system costs by about 8% compared with PERC, a decisive advantage for land-constrained sites near substations. Rezolv Energy’s St. George park specified bifacial TOPCon panels, boosting yield 12% on reflective gravel. Lenders now apply a 15% technology-obsolescence haircut to PERC-based projects slated after 2026, nudging developers toward TOPCon and heterojunction. Smart Solar Technologies is building a BGN 240 million factory to supply 900 MW of TOPCon panels annually from 2026, localizing the value chain and underpinning the Bulgarian solar energy market.

Grid-constrained “hybrid parks” pairing PV with batteries

ESO’s April 2025 tender awarded 9.7 GWh of storage across 82 projects, quadruple the offered capacity, confirming storage as the preferred hedge against curtailment. Renalfa’s 25 MW/55 MWh Razlog system, commissioned in June 2024, earns roughly EUR 120,000 per MW annually from frequency regulation, double pure arbitrage revenue. SUNOTEC secured EUR 115 million in September 2025 for a 115 MW PV plus 763 MWh battery project, with a 6.6-hour duration aimed at both energy and capacity markets.[3]IFC, “IFC finances St. George Solar Park,” ifc.org EBRD is structuring a USD 200 million credit line for Bulgarian hybrid parks, which would normalize battery integration in utility solar EBRD.COM. Storage lifts capacity factors and unlocks new revenue streams, strengthening the Bulgarian solar energy market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Distribution-level grid congestion & curtailment risk | -2.1% | Southern & eastern Bulgaria | Short term (≤ 2 years) |

| Slow rooftop permitting for systems <30 kW | -1.3% | Urban areas | Medium term (2-4 years) |

| Scarce domestic workforce of certified PV installers | -0.8% | National | Medium term (2-4 years) |

| Rising land-lease prices near substations | -0.6% | Southern & eastern Bulgaria | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Distribution-level grid congestion & curtailment risk

The 110 kV grid can evacuate only 12 GW nationwide, yet 3.91 GW of solar is already concentrated in the south, forcing ESO to curtail up to 15% of peak PV output during summer 2024. Curtailment costs generators an estimated EUR 8 million and triggered force-majeure claims in several PPAs.[4]ESO, “Grid Curtailment Report 2024,” eso.bg ESO’s 2024-2030 plan budgets BGN 1.2 billion to upgrade 18 substations, but most work will finish only after 2027. Developers are self-funding interim reinforcements. Rezolv Energy built 6 km of 110 kV lines at EUR 4 million to meet commissioning deadlines. The asymmetry is stark: rooftop systems under 30 kW avoid curtailment via net-metering, whereas utility-scale parks bear uncompensated shutdowns, tempering growth in the Bulgarian solar energy market.

Slow rooftop permitting for systems < 30 kW

Amendments to the Energy Act in 2023 capped approval at 30 days for small rooftops, yet municipal offices still demand extra fire-safety and structural certificates, stretching actual timelines to 90-120 days. A 2024 survey found 42% of residential applications delayed by redundant document requests, with 18% abandoned outright.[5]Bulgarian Photovoltaic Association, “Residential PV Survey 2024,” bpva.bg The Energy Ministry began a six-month training program in early 2025 for 200 municipal officials, but coverage remains patchy. This gap slows deployment in the fast-growing residential segment, where subsidies of up to BGN 15,000 shorten payback periods to under six years. Unless local processes align with national law, the Bulgarian solar energy market will forfeit a key growth lever.

Segment Analysis

By Technology: Crystalline Dominance Sustains Rapid Expansion

Solar PV retained a 100% hold on the Bulgarian solar energy market in 2024 and will grow at an 11.7% CAGR to 2030, driven by crystalline-silicon modules trading near EUR 0.10/W. CSP remains absent given Bulgaria’s 1,600 kWh/m² DNI, well below the 2,000 kWh/m² threshold for economic tower projects. TOPCon’s higher efficiency and lower temperature coefficient underpin its 60% share of 2024 additions, while bifacial designs delivered a 12% gain at the St. George brownfield site. Floating PV totals just 3 MW on irrigation ponds owing to regulatory ambiguity over water rights, yet Smart Solar’s local module factory will cut import dependence and may catalyze niche formats.

Aggressive price declines slash turnkey costs to EUR 500/kW for a 100 MW PV plant, one-fifth of an equivalently sized CSP project, locking in PV’s supremacy. Domestic manufacturing, led by Smart Solar Technologies, enhances supply security and creates spillovers for regional exports. These trends collectively enlarge the Bulgarian solar energy market size at both utility and rooftop scales.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Grid Type: On-Grid Dominance Underpins Revenue Certainty

On-grid plants constituted 95.1% of installed capacity in 2024 and are forecast to expand at a 12.1% CAGR, buoyed by CfD contracts and IBEX liquidity. Net-metering credits below 200 kW at retail rates (EUR 0.14/kWh in 2024) create an EUR 0.08/kWh uplift over wholesale tariffs, compressing paybacks to under six years. The recent auction’s EUR 52-58/MWh clearing prices confirm grid parity. Off-grid systems, 4.9% of capacity, serve remote farms and telecom towers where grid extensions exceed EUR 50,000/km.

Hybrid on-grid plants blur traditional boundaries: Renalfa’s Razlog and SUNOTEC’s 763 MWh project operate grid-connected but can island during outages, fetching a 15% PPA premium from industrial buyers seeking resilience. These configurations diversify revenue and enhance the Bulgaria solar energy market size while alleviating curtailment pressure.

By End User: Residential Growth Outstrips Utility-Scale Additions

Utility-scale projects held 59.8% of installed capacity in 2024, yet residential rooftops will post the quickest ascent at a 14.9% CAGR to 2030, catalyzed by grants of up to BGN 15,000 per system and soaring power bills. Household applications jumped to 12,000 systems in 2024 from 4,500 in 2023. The Bulgarian solar energy market size for residential rooftops is set to more than triple by 2030, underscoring the subsidy’s pull and net-metering’s push.

C&I rooftops, roughly 28% of capacity, concentrate in metals, foods, and textiles, where daytime loads dovetail with generation. Aurubis Bulgaria’s 41 MWp roll-out trims grid purchases by 15% while monetizing surplus on IBEX’s intraday platform. Utility-scale parks keep adding sizable blocks. Rezolv Energy’s 225 MW St. George lifted national capacity 5.8 percentage points in 2024, but faces rising land-lease costs near substations, which climbed 40% since 2023. These mixed dynamics reinforce the Bulgaria solar energy market’s diversification and momentum.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Southern and eastern provinces, Burgas, Stara Zagora, Plovdiv, and Haskovo, host 65% of national solar capacity, aided by 1,550-1,600 kWh/m² irradiance and proximity to idle coal-plant substations. The 2024 auction steered 1.8 GW of the 3 GW award into these regions, locking in their dominance. Burgas is emerging as a hybrid hub; TERNA Energy’s 130 MW Vratitsa project will bolt on 50 MWh of storage, highlighting a shift from pure PV to integrated assets.

Northern and central Bulgaria, Pleven, Veliko Tarnovo, Ruse, hold about 20% of capacity but offer lower land rents and host agro-PV pilots like Qn-SOLAR’s 5 MW Svishtov site, which cut soil-moisture loss by 20%. Field trials in Strelcha in August 2025 showed an 8% wheat biomass lift under partial shading, suggesting crop-specific gains that could unlock CAP subsidies if Bulgaria adopts Germany’s 66% yield rule. The Ministry of Agriculture is drafting guidelines for 2026, potentially unleashing 1 GW of dual-use capacity on just 1% of the grain belt’s 2.1 million hectares.

Western Bulgaria, including Sofia and Pernik, supplied only 10% of capacity in 2024 but is rich in data centers and logistics roofs that now favor C&I solar due to high urban tariffs. Transmission bottlenecks exacerbate regional imbalance: southern lines can export only 2.5 GW at midday peaks, whereas northern circuits have 1.2 GW spare headroom. ESO’s north-south 400 kV link between Plovdiv and Pleven, scheduled for 2028, should cut southern curtailment by 60% and create a new corridor for cross-border sales to Romania. The 1,200 MW HVDC to Greece, online since 2023, already lets Bulgarian solar capture EUR 30/MWh price spreads, effectively using the regional grid as a virtual battery.

Competitive Landscape

The EPC segment is moderately concentrated: the top five contractors command about a 55% share, led by Solarpro and Sunotec. Solarpro has delivered over 7 GW across 30 countries and offers 20-year performance guarantees, adding a service moat. Sunotec, with 8.2 GW built worldwide, holds 12% of the European industrial PV construction market and is extending its footprint to Africa and Asia. International module giants JinkoSolar, Trina Solar, Longi Green Energy, and Canadian Solar are bundling turnkey EPC packages, challenging domestic contractors for downstream margins.

Hybrid projects are the new battlefield. Solarpro Technology integrated Bulgaria’s first utility-scale BESS at Razlog, while Hithium supplied the lithium cells, carving an early-mover advantage. The oversubscribed 2025 storage tender will amplify demand for battery-capable EPC teams. Smart Solar Technologies’ upcoming 900 MW panel plant is a strategic play to secure module supply and edge out Chinese imports that covered 75% of 2024 demand. Producer-responsibility rules under the EU’s WEEE Directive increasingly sway RFP scoring, penalizing bidders lacking recycling pathways, and favoring players with established take-back programs, another lever of competitive differentiation. Together, these factors shape a dynamic yet consolidating Bulgarian solar energy market.

Bulgaria Solar Energy Industry Leaders

-

Solarpro Holding PLC

-

Jinko Solar Holdings Ltd.

-

Green Yellow

-

Skytech Energy Ltd

-

Elsol Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: The Dubai Electricity and Water Authority (DEWA) and UAE state-owned renewable power company Masdar have announced financial close on the 1.8GW sixth phase of the Mohammed bin Rashid Al Maktoum Solar Park with costs up to AED 5.5 billion (USD 1.5 billion).

- March 2025: Bulgaria is establishing a EUR 15 million Renewable Hydrogen Centre of Excellence in Stara Zagora, under the H2START project. This initiative aims to advance clean hydrogen technologies and position Bulgaria as a leader in green hydrogen production and export within Europe.

- October 2024: Rezolv Energy, an independent power producer backed by Actis, has secured up to EUR 90 million in debt financing from the International Finance Corporation (IFC) and Raiffeisen Bank International to support the construction of the ‘St. George’s solar park in north-eastern Bulgaria.

- September 2024: Rezolv Energy has awarded Engineering, Procurement, and Construction (EPC) contracts to Solarpro and CMC Europe for a 229 MW solar project in Bulgaria.

Bulgaria Solar Energy Market Report Scope

Solar energy is the energy obtained from the sun's rays converted into thermal or electrical energy. It is the cleanest form of energy that is abundant in nature. Solar energy is harnessed by photovoltaics, heating & cooling, and concentrated solar power. Due to the development of resilient technology, today, solar energy is mainly used to generate electricity by various consumers, including residential, industrial, and commercial.

Bulgaria's solar energy market is segmented by technology type. By technology type, the market is segmented into Solar Photovoltaic (PV) and Concentrated Solar Power (CSP). By grid type, the market is segmented into On-grid and off-grid. By end-user, the market is segmented into Utility-Scale, Commercial and Industrial, and Residential. For each segment, the market sizing and forecasts have been done based on installed capacity (GW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What capacity did Bulgaria install by the end of 2025?

The country will have 4.75 GW of solar online in 2025.

How fast is solar capacity expected to grow by 2030?

Forecasts point to 8.25 GW by 2030, an 11.67% CAGR.

Which segment is expanding the quickest?

Residential rooftops are projected to grow at 14.9% CAGR through 2030.

Why are hybrid solar-plus-storage parks gaining traction?

They mitigate curtailment, unlock frequency-regulation revenues, and improve project bankability.

What is the biggest regulatory hurdle for small rooftops?

Municipal delays still stretch the statutory 30-day permit to as much as 120 days.

How concentrated is the EPC market?

The top five contractors hold roughly 55% of utility-scale construction work.

Page last updated on: