Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

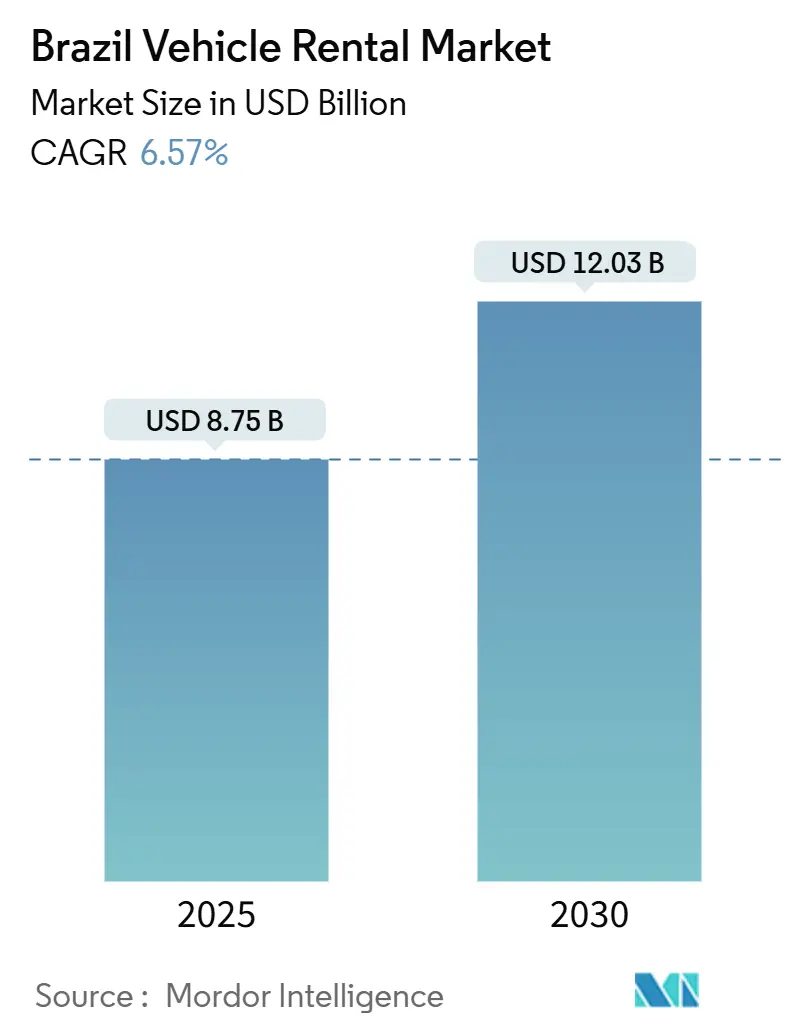

| Market Size (2025) | USD 8.75 Billion |

| Market Size (2030) | USD 12.03 Billion |

| Growth Rate (2025 - 2030) | 6.57% CAGR |

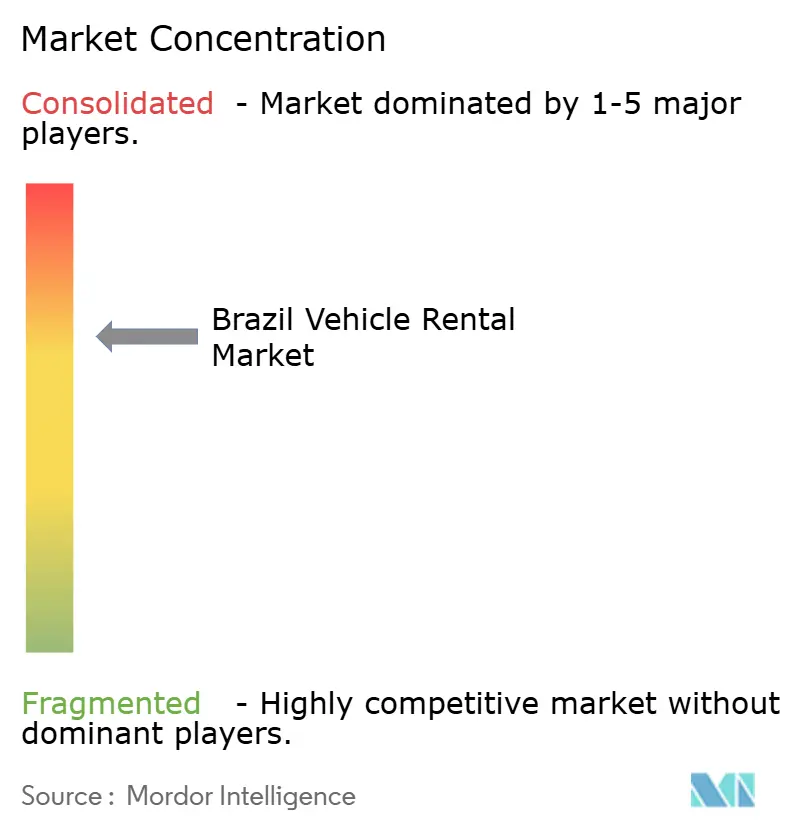

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Vehicle Rental Market Analysis by Mordor Intelligence

The Brazil vehicle rental market size reached USD 8.75 billion in 2025 and is projected to expand to USD 12.03 billion by 2030, registering a 6.57% CAGR. This outlook is underpinned by the rebound of domestic leisure trips, the rapid digitalization of booking channels, and corporate preference for outsourced fleets. Passenger-car rentals lead demand because they match both tourist and business travel requirements, while electric-vehicle uptake is growing on the back of favorable Chinese OEM financing. Fleet operators are also scaling quickly as companies convert capital expenditure into operating leases to navigate Brazil’s high-interest-rate environment. The Southeast region keeps the largest revenue base, yet the Northeast is catching up thanks to new low-cost airline routes that push fly-drive itineraries and lift overall utilization rates across the Brazil vehicle rental market.

Key Report Takeaways

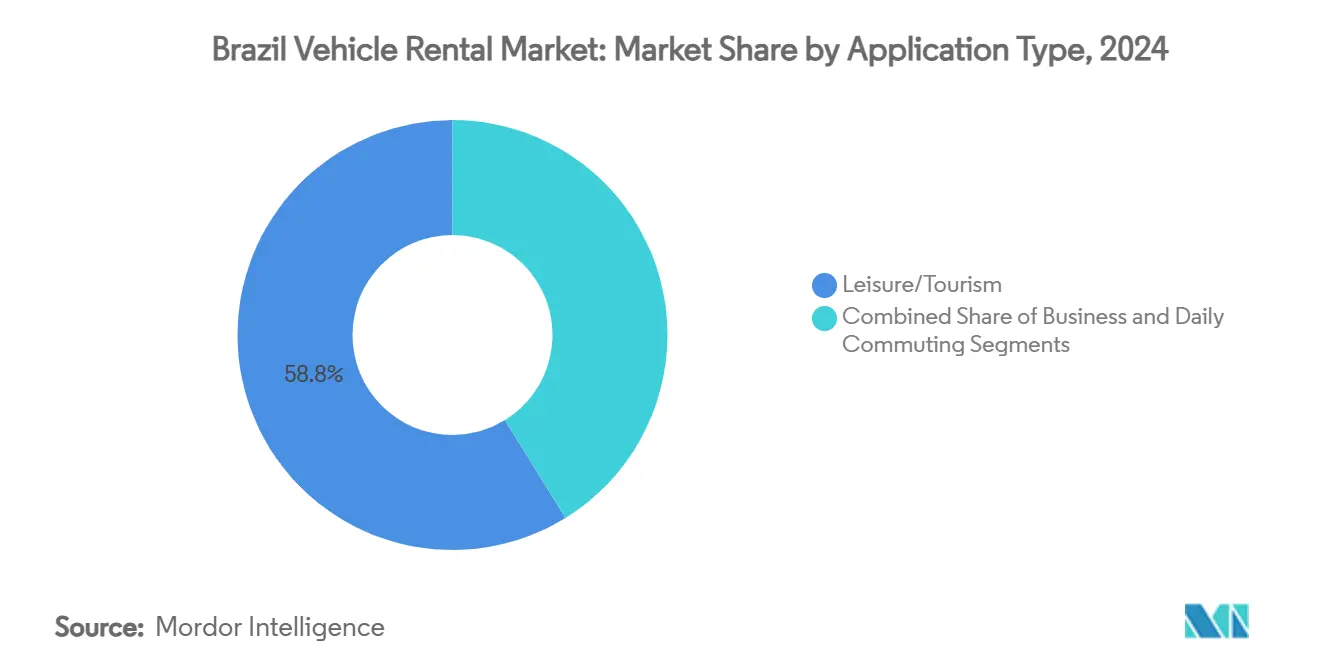

- By application type, leisure/tourism led with 58.76% of the Brazil vehicle rental market share in 2024; daily commuting is projected to advance at a 7.12% CAGR to 2030.

- By booking type, online channels captured 65.88% of the Brazil vehicle rental market share in 2024, and are forecast to grow at a pace of 7.25% through 2030.

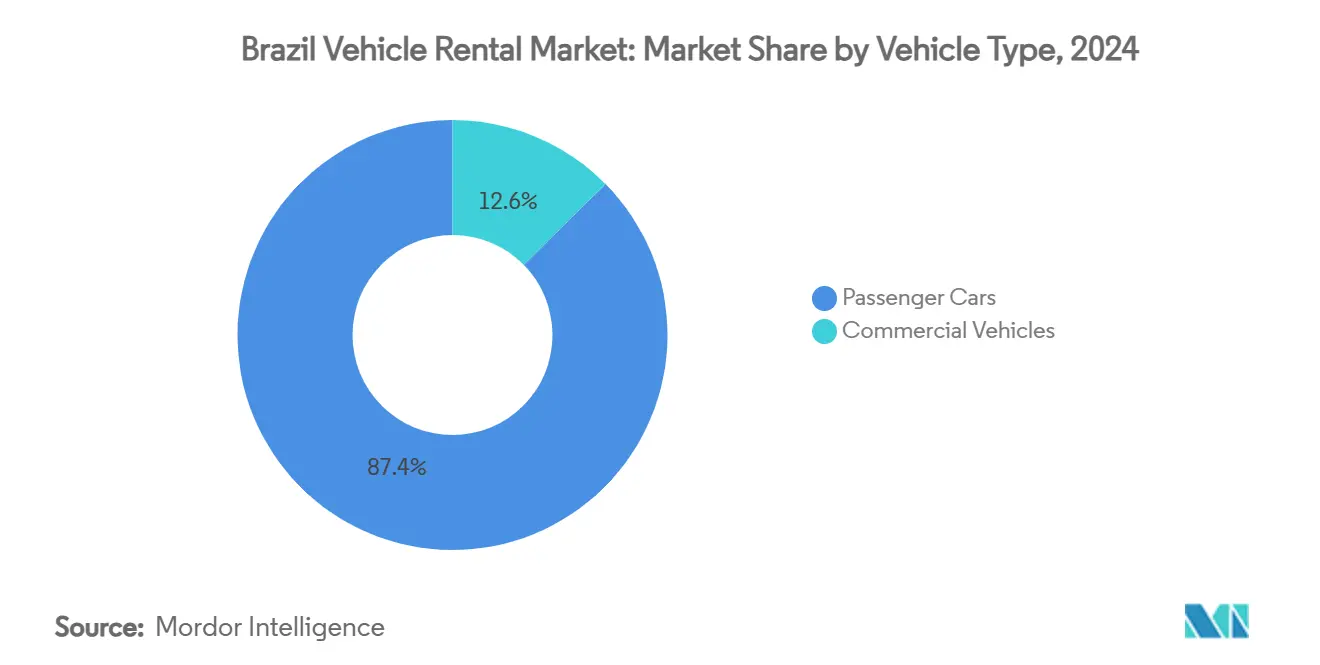

- By vehicle type, passenger cars accounted for 87.44% of the Brazil vehicle rental market size in 2024 and are forecast to grow at a 6.82% CAGR through 2030.

- By end user, tour operators held 63.09% of the Brazil vehicle rental market share in 2024, fleet operators commanded the fastest 9.46% CAGR between 2025-2030.

- By region, Southeast Brazil retained 53.66% of the Brazil vehicle rental market share in 2024, whereas the Northeast is set to grow at an 8.55% CAGR to 2030.

Brazil Vehicle Rental Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in Domestic Leisure Tourism Post-COVID | +1.8% | National; strong in Southeast and Northeast | Medium term (2-4 years) |

| Rapid Uptake of Online and Mobile Booking Channels | +1.2% | Nationwide urban centers | Short term (≤ 2 years) |

| Corporate Shift Toward Fleet-Outsourcing Models | +1.0% | Southeast and South metros | Long term (≥ 4 years) |

| Low-Cost Airline Expansion Spurring Fly-Drive Demand | +0.9% | Northeast and Central-West | Medium term (2-4 years) |

| Subscription/Fractional Ownership Models | +0.6% | Major Southeast cities | Long term (≥ 4 years) |

| Chinese OEM Financing Catalyzing EV Fleet Electrification | +0.4% | Nationwide; early in Southeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Boom in Domestic Leisure Tourism Post-COVID

Brazilian travel and tourism contributed USD 167.6 billion to GDP in 2025, equal to 7.7% of national output [1]“Economic Impact 2025 Brazil,” World Travel & Tourism Council, wttc.org. Leisure trips represent 89.9% of total travel spend, lengthening average stays to 13.1 nights and pushing longer vehicle-rental periods. Government promotion programs such as the 2025-2027 “Plano Brasis” reinforce this trajectory by aiming to attract 8 million foreign visitors. Extended itineraries across coastal, rainforest, and cultural attractions translate into higher revenue per customer for rental operators.

Rapid Uptake of Online and Mobile Booking Channels

Localiza’s Fast Digital Pickup system lets customers collect cars in under five minutes, showing how users' experience and queue elimination foster conversion [2]“Fast Digital Pickup Launch Press Release,” Localiza Rent a Car, localiza.com. Mobile commerce adoption among younger travelers creates data feedback loops, enabling dynamic pricing and fleet-allocation efficiency. As a result, companies that invest in seamless apps and contactless pick-up solutions are capturing disproportionate growth within the Brazil vehicle rental market.

Corporate Shift Toward Fleet-Outsourcing Models

The fleet operator end-user category is expanding because enterprises offload vehicle ownership complexity. Firms like JSL Logistica manage more than 16,400 cars, underscoring scale advantages in telematics, maintenance, and residual-value optimization. Outsourcing converts large capital commitments into predictable operating expenses, an attractive proposition in a 13.25% SELIC-rate environment [3]“Monetary Policy Minutes, 2025,” Banco Central do Brasil, bcb.gov.br .

Low-Cost Airline Expansion Spurring Fly-Drive Demand

National jet-fuel consumption surpassed pre-pandemic volumes as of April 2024, evidencing a strong domestic aviation recovery. Low-fare carriers have opened routes to secondary coastal airports, particularly in the Northeast, prompting fly-drive packages. New airlift into Fortaleza, Salvador, and Recife lifts vehicle-rental pickup volumes at these gateways and contributes to the Northeast’s forecast-leading growth.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Interest-Rate Environment Inflating Fleet CAPEX | -1.2% | National | Medium term (2-4 years) |

| Stricter Vehicle-Emission Standards Raising Costs | -0.8% | National | Short term (≤ 2 years) |

| Airport Kerb-Side Restrictions Limiting Pick-Ups | -0.4% | Sao Paulo, Rio de Janeiro, Brasilia | Short term (≤ 2 years) |

| Cyber-Risk on Connected Rental Fleets Inflating Insurance | -0.3% | Urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Interest-Rate Environment Inflating Fleet CAPEX

With the SELIC benchmark at 13.25% in 2025, vehicle-loan rates range between 11.58% and 29.22%, driving higher monthly lease costs. Many operators are deferring fleet renewals, risking older average vehicle age and higher maintenance outlays. Elevated borrowing costs also raise the hurdle rate for geographic expansion, slowing penetration in low-density markets.

Stricter Vehicle-Emission Standards Raising Costs

The PROCONVE L8 rules, effective January 2025, require lower fleet-average tailpipe emissions, increasing acquisition prices for compliant models. Rental firms must accelerate replacement cycles or diversify into hybrids and EVs, elevating depreciation charges. Operators that embed vehicle-level emission tracking gain an edge in corporate tenders but may face near-term margin pressure.

Segment Analysis

By Application Type: Leisure Rentals Drive Volume While Commuting Accelerates

Leisure and tourism applications delivered 58.76% of revenue in 2024, equal to the largest slice of the Brazil vehicle rental market share. Extended stays averaging 13.1 nights translate into longer contracts and higher revenue per booking. Business travel delivers consistent weekday utilization, especially around São Paulo’s financial hubs, while the daily-commuting subsegment is forecast to grow at a 7.12% CAGR on the back of flexible-use subscriptions.

Longer leisure itineraries reinforce weekend demand peaks, helping operators lift overall fleet utilization across seasons. The commuting category benefits from urban congestion policies that deter private-car ownership, positioning subscription platforms as cost-effective alternatives. Corporate-travel demand remains stable but is increasingly met through outsourced fleet contracts rather than individual rentals, a shift that reshapes pricing and service packages within the Brazil vehicle rental market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Booking Type: Digital Dominance Redefines Customer Journey

Online reservations held 65.88% of transactions in 2024 and are scaling at 7.25% CAGR, confirming that intuitive apps and instant confirmation are now table stakes. Offline channels maintain traction in niche scenarios such as high-touch corporate accounts and first-time foreign visitors.

Dynamic pricing algorithms enabled by real-time demand data help minimize idle inventory and safeguard yields. Conversely, offline counters at airports face staffing-cost pressures yet remain vital for ancillary-service upselling. The shift compels every operator in the Brazil vehicle rental market to invest in cybersecurity, omnichannel loyalty programs, and API connectivity with airlines and OTAs.

By Vehicle Type: Passenger Cars Retain Leadership as EV Share Climbs

Passenger cars contributed 87.44% to the Brazil vehicle rental market size in 2024, growing at 6.82% CAGR through 2030 as they fit both leisure and corporate use cases. Compact sedans drive volume, but premium SUVs capture outsized profitability. Commercial-vehicle rentals serve parcel-delivery and tour-group niches, delivering steady if smaller revenue streams.

Electrification is starting to reshape the passenger-car mix; BYD’s financing packages reduce upfront costs while lower operating expenses appeal to ESG-minded customers. Commercial-van electrification remains nascent due to payload concerns, but pilot programs are underway for urban last-mile fleets. Connectivity and ADAS features are emerging as must-have specifications in new procurement tenders across the Brazil vehicle rental market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Fleet Operators Gain Momentum Amid Outsourcing Wave

Tour operators captured 63.09% of revenue in 2024 by aligning with hotel and airline packages, yet their share is eroding slowly as direct digital bookings rise. Fleet-management specialists are expanding at 9.46% CAGR, converting fixed-asset ownership into service contracts for corporations seeking balance-sheet lightness.

Higher service complexity around telematics analytics, fuel controls, and sustainability reporting boosts switching costs and cements long-term client relationships. Smaller independent renters face scale disadvantages in financing and technology integration, prompting industry consolidation corridors. The evolving client base necessitates customized service-level agreements and flexible mileage bands across the Brazil vehicle rental market.

Geography Analysis

Southeast Brazil produced 53.66% of industry turnover in 2024 thanks to the economic heft of Sao Paulo and Rio de Janeiro, mature airport infrastructure, and the headquarters clusters of major rental brands. Dense corporate travel keeps weekday utilization high, while affluent domestic tourism supports premium vehicle categories and drives early electric-vehicle adoption.

The Northeast is on track for an 8.55% CAGR, catalyzed by budget-airline connectivity that now links Salvador, Fortaleza, and Recife to secondary domestic origins. Public-private tourism investment programs have upgraded roads and hospitality capacity, unlocking coastal and cultural circuits where rental cars remain the most practical mobility solution. Improved airport facilitation and pre-booked digital channels reduce wait times and improve customer satisfaction, aiding repeat business growth within the Brazil vehicle rental market.

South and Central-West regions post steady mid-single-digit growth anchored in agribusiness, eco-tourism, and cross-border itineraries into Argentina and Paraguay. Lower population density implies longer average trip distances, which boosts mileage revenue per contract but requires larger station footprints. Operators deploy flexible re-allocation of idle capacity between grain-harvest logistics peaks and holiday-season tourist surges, balancing fleet productivity year-round.

Competitive Landscape

Localiza’s merger with Unidas formed a fleet of roughly 631,639 vehicles, granting multi-segment leadership in car rental, long-term leasing, and used-car de-fleeting channels. A vertically integrated model encompassing proprietary sales yards and reconditioning centers helps control residual-value risk and supports aggressive fleet‐renewal cycles. Movida remains the second largest incumbent, though Q4 2023 losses of R$588 million prompted strategic cost reviews and accelerated used-car liquidations.

Multinational brands such as Hertz, Avis Budget, Enterprise, and Sixt concentrate on premium travelers at major gateways, leveraging global loyalty schemes. Domestic challengers like FOCO Rent a Car offer value-oriented propositions in regional airports, while subscription-focused newcomers such as Turbi attract urban millennials through app-driven monthly packages. Competitive tension is intensifying around fleet electrification, where early access to subsidized EV supply is a differentiator in corporate tenders within the Brazil vehicle rental market.

Technology investment forms the new battleground. Localiza deploys AI-based demand forecasting to trim idle inventory, whereas Movida is rolling out end-to-end digital onboarding for corporate clients. Smaller firms collaborate with fintech to bundle insurance, telemetry, and flexible credit scoring, thereby addressing an underserved SME segment. The interplay between scale economies in procurement and agility in niche service design will shape market share over the next cycle.

Brazil Vehicle Rental Industry Leaders

-

Localiza Rent a Car S.A.

-

Movida Participacoes

-

Avis Budget Group

-

FOCO Rent a Car

-

Enterprise Holdings

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2024: Addiante, a Gerdau–Randoncorp joint venture, earmarked more than R$ 1 billion for heavy-vehicle rentals over two years, including a sale-and-leaseback deal covering Ambipar’s truck fleet.

- February 2024: Daimler Truck announced plans to launch its first truck-rental program in Brazil after investing R$ 200 million to seed a 100-unit fleet that will double by year-end.

Brazil Vehicle Rental Market Report Scope

Vehicle rentals contain a car booked in person, by mobile through the mobile application, or offline. A vehicle rental service is a service that helps customers rent a vehicle for short periods or longer duration. A short period generally ranges from a few hours to a few weeks.

The Brazilian vehicle rental market is segmented by application type, booking type, vehicle type, and end user. By application type, the market is segmented into leisure/tourism, business, and fleet outsourcing. By booking type, the market is segmented into online and offline. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By end user, the market is segmented into fleet operator and tour operator.

The report offers market size and forecasts in value (USD) for all the abovementioned segments.

By Application Type

| Leisure/Tourism |

| Business |

| Daily Commuting |

By Booking Type

| Online |

| Offline |

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

By End User

| Tour Operators |

| Fleet Operators |

By Region

| Southeast |

| South |

| Northeast |

| North |

| Central-West |

| By Application Type | Leisure/Tourism |

| Business | |

| Daily Commuting | |

| By Booking Type | Online |

| Offline | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By End User | Tour Operators |

| Fleet Operators | |

| By Region | Southeast |

| South | |

| Northeast | |

| North | |

| Central-West |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Brazil vehicle rental market?

The market generated USD 8.75 billion in 2025 and is projected to reach USD 12.03 billion by 2030.

Which segment holds the largest Brazil vehicle rental market share?

Leisure and tourism rentals account for 58.76% of revenue, making them the dominant application type.

How fast is the online booking channel growing?

Online reservations are expanding at a 7.25% CAGR through 2030, already controlling 65.88% of all bookings.

Which region is the fastest growing for vehicle rentals in Brazil?

The Northeast is forecast to grow at an 8.55% CAGR thanks to new low-cost airline routes and tourism investments.

Page last updated on: