Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

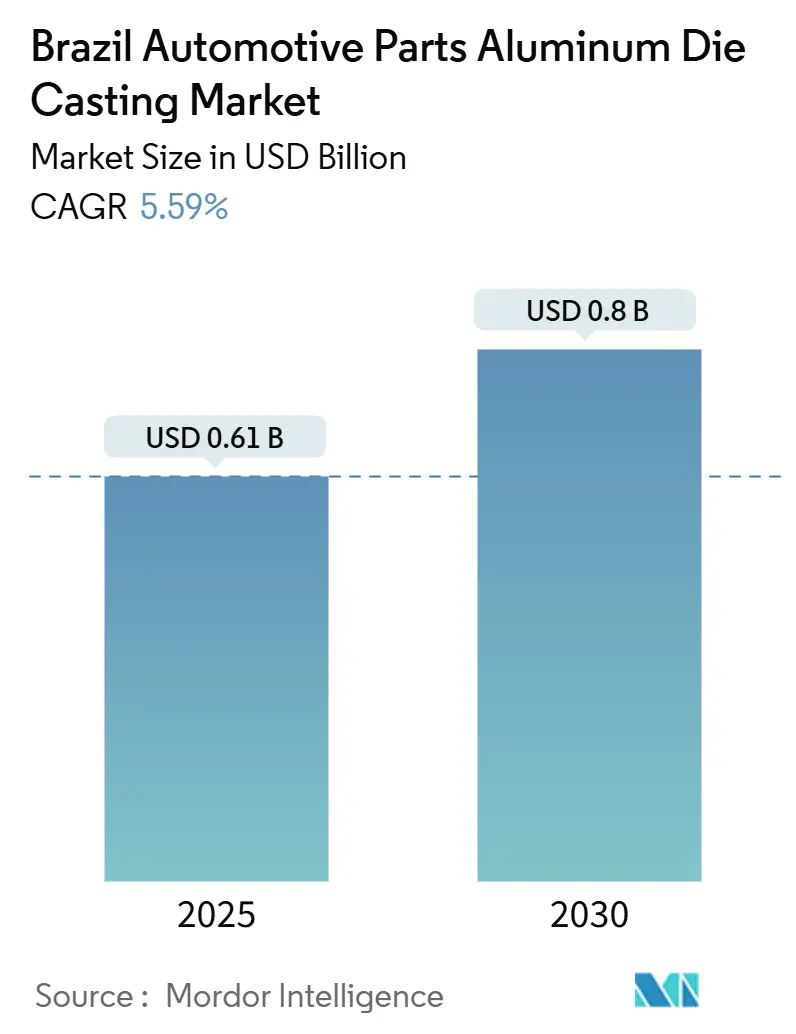

| Market Size (2025) | USD 0.61 Billion |

| Market Size (2030) | USD 0.8 Billion |

| Growth Rate (2025 - 2030) | 5.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Automotive Parts Aluminum Die Casting Market Analysis by Mordor Intelligence

The Brazilian automotive parts aluminum die casting market size is estimated at USD 0.61 billion in 2025 and is projected to grow at a 5.59% CAGR to USD 0.80 billion by 2030, underscoring steady momentum in one of South America’s most technology-intensive manufacturing segments. Strong demand stems from government incentives under the Mover program, OEM near-shoring strategies, and a resilient domestic vehicle pipeline that blends internal-combustion platforms with fast-growing hybrid and battery-electric models. Foundries leverage abundant local bauxite reserves, enhance scrap collection networks, and expand renewable electricity capacity to supply low-carbon castings that help automakers meet increasingly stringent fleet-average CO₂ targets. Process upgrades in high-pressure and vacuum die casting support the production of porosity-free parts for next-generation battery enclosures, while preserving cost competitiveness for legacy engine blocks and transmission housings. Competitive pressure intensifies as global Tier-1s expand their local footprints and domestic specialists automate large-tonnage cells, creating a moderate-concentration environment where quality certification and on-time delivery remain crucial.

Key Report Takeaways

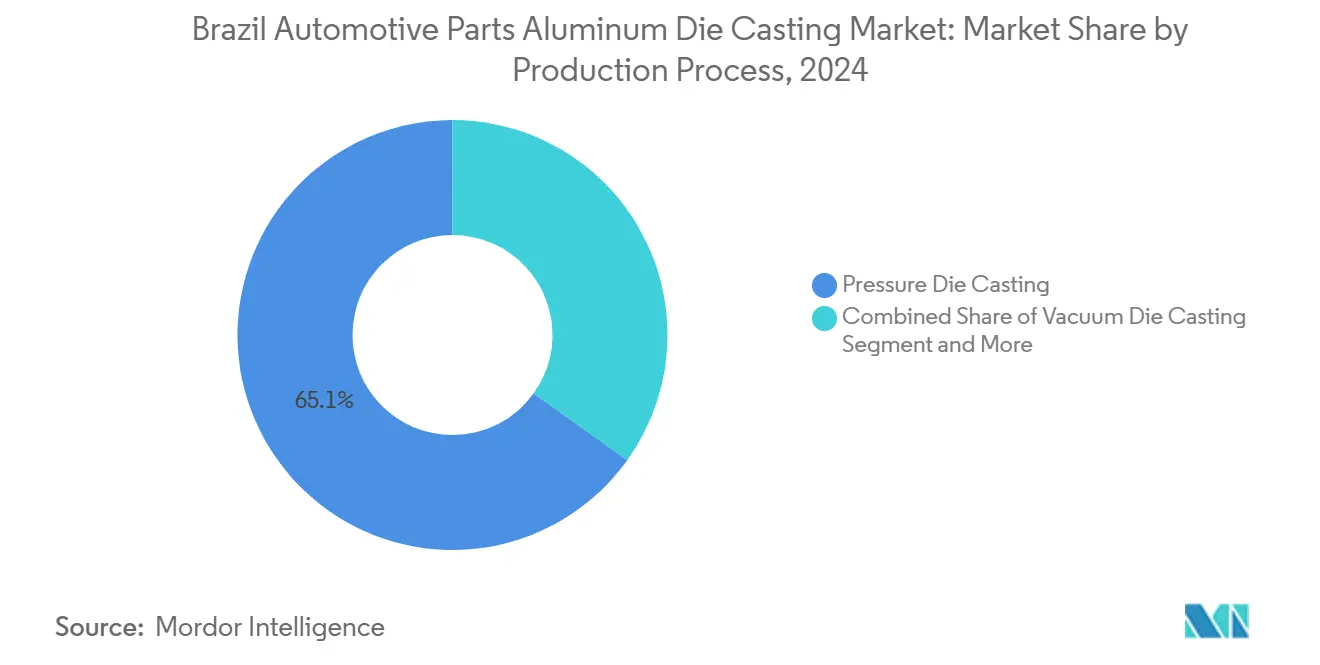

- By production process, pressure die casting led with 65.13% of the Brazilian automotive parts aluminum die casting market share in 2024, while vacuum die casting is projected to expand at 6.85% CAGR through 2030.

- By application type, engine parts held 39.04% of the Brazilian automotive parts aluminum die casting market share in 2024, while e-mobility battery housings and thermal systems are set to grow at a 7.85% CAGR between 2025 and 2030.

- By vehicle type, passenger cars commanded a 54.16% share of the Brazilian automotive parts aluminum die casting market in 2024 and are forecast to register a 6.44% CAGR through 2030.

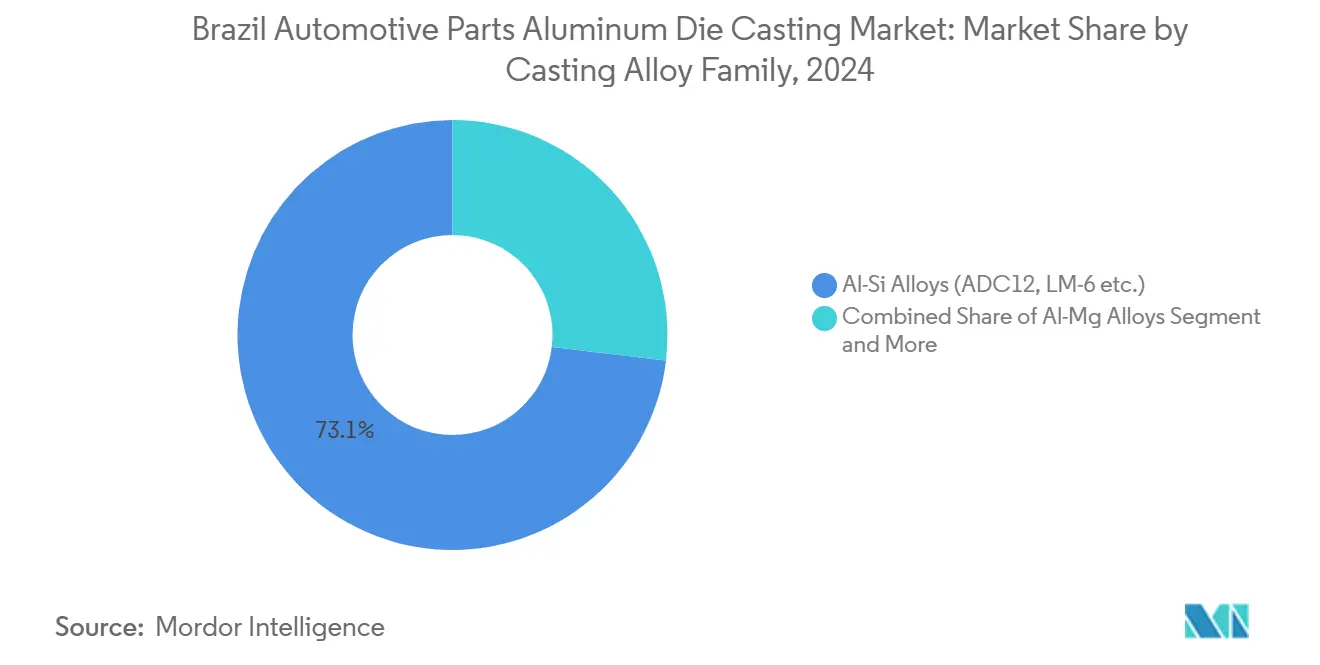

- By casting alloy family, Al-Si families captured 73.11% of the Brazilian automotive parts aluminum die casting market share in 2024, while Al-Mg alloys are expected to rise at a 7.22% CAGR through 2030.

- By end-user, OEM/Tier-1 customers controlled 83.24% of the Brazilian automotive parts aluminum die casting market share in 2024 and are expected to maintain the fastest 6.15% CAGR to 2030 as they deepen local sourcing partnerships.

Brazil Automotive Parts Aluminum Die Casting Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Domestic Production of Vehicles | +1.8% | São Paulo, Paraná, Rio Grande do Sul | Short term (≤2 years) |

| OEM Lightweighting and CO₂ Compliance | +1.2% | São Paulo and Minas Gerais corridors | Medium term (2-4 years) |

| Expansion of Brazil’s EV Volumes | +0.9% | National, led by São Paulo and Santa Catarina | Long term (≥4 years) |

| Incentives for Advanced Casting | +0.8% | Established automotive regions | Medium term (2-4 years) |

| OEM Near-Shoring to Mitigate Risk | +0.7% | Secondary automotive hubs | Short term (≤2 years) |

| Local-Content Rules in Supply Chains | +0.6% | São Paulo, Minas Gerais | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

OEM Lightweighting and CO₂-Target Compliance

Brazilian assemblers intensify lightweighting because the Mover program links IPI Verde tax credits to vehicle emissions reduction targets. Switching from steel to aluminum in structural castings reduces 30-40% of component mass, directly extending hybrid driving range and lowering total vehicle CO₂ emissions. Maxion’s bus battery cradle illustrates the shift, achieving a significant weight cut at cost parity with steel parts. Adoption is reinforced by updated ABNT NBR standards that certify structural integrity for aluminum castings in crash-critical zones. Collectively, these measures enlarge the Brazilian automotive parts aluminum die casting market by favoring high-pressure and vacuum processes that sustain thin-wall geometries without porosity.

Rising Domestic Production of Light Vehicles and Motorcycles

Vehicle assemblers posted a significant jump in auto parts output in December 2024, dwarfing aggregate industrial growth and validating aggressive capacity additions [1]“Monthly Industrial Survey December 2024,” Brazilian Institute of Geography and Statistics, ibge.gov.br. Stellantis, Honda, and other OEMs have announced significant local investment stretching to 2030, underpinning sustained demand for aluminum blocks, housings, and structural pieces. Motorcycle makers also specify aluminum engine and transmission castings to keep curb masses low in Brazil’s bustling two-wheeler market. This surge solidifies the Brazilian automotive parts aluminum die casting market as a core supplier base for both ICE and hybrid platforms.

Expansion of Brazil’s EV / Hybrid Volumes Boosting Battery-Housing Demand

Passenger electric vehicle (EV) registrations have grown significantly and are expected to continue expanding, making a notable contribution to overall car sales in the coming years. Local production lines from BYD and Great Wall Motors require precision aluminum battery trays and e-motor housings that resist thermal runaway while maintaining uniform plate temperatures. Partnerships among SENAI, CBA, and Novelis channel Mover funds toward domestic lithium-ion cell projects, ensuring supply chains integrate cast aluminum plates designed for module rigidity—regulatory accreditation from INMETRO anchors safety compliance, supporting longer-term confidence in local sourcing for electrified drivetrains.

Government Incentives Under “Rota 2030” for Advanced Casting Technologies

The successor Mover program provides BRL 19.3 billion (~USD 3.6 billion) in credits through FNDIT, lowering financing costs for high-pressure and vacuum die casting automation. Iochpe-Maxion secured BRL 357.3 million (~USD 67 million) for digital twins and AI-based defect prediction, showcasing how government capital unlocks productivity gains. BNDES oversight links disbursements to domestic content and technology-transfer benchmarks, accelerating the diffusion of Industry 4.0 practices among mid-sized foundries. This stimulus nurtures a more competitive Brazilian automotive parts aluminum die casting market capable of meeting multinationals’ zero-defect expectations.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminum Ingot Price Volatility | –0.8% | All Brazilian foundries | Short term (≤2 years) |

| High Upfront Capex for Automation | –0.5% | Smaller foundries nationwide | Medium term (2-4 years) |

| Shortage of Skilled Technicians | –0.4% | São Paulo and Santa Catarina clusters | Medium term (2-4 years) |

| Electricity-Price Spikes During Droughts | –0.3% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Aluminum Ingot Price Volatility

Currency fluctuations add a second layer of risk, as many specialized alloys are still imported. CBA’s modernization investment aims to double scrap recovery, allowing more secondary metal to substitute for primary ingot and dampen price shocks. Regulatory alloy standards issued by ANVISA ensure chemical consistency, even as the use of scrap inputs increases. However, cost pressure still reduces near-term earnings across the Brazilian automotive parts aluminum die casting market.

High Upfront CAPEX for HPDC/VDC Cell Automation

Independent foundries face a significant challenge as fully equipped vacuum cells are costly to procure. FNDIT soft loans offset part of the burden, yet collateral and documentation remain onerous. Starcast’s new Guarulhos plant demonstrates a viable path by coupling CQI-27 process control with phased automation, thereby spreading capital over multiple years [2]“Starcast Installs CQI-27 Compliant Line,” Euroguss, euroguss.de. Even so, slow approvals risk delaying capacity upgrades and constraining the Brazilian automotive parts aluminum die casting market during demand peaks.

Segment Analysis

By Production Process: Pressure Die Casting Outperforms Through Versatility

The Brazilian automotive parts aluminum die casting market size for pressure die casting processes retained 65.13% revenue share, thanks to superior repeatability and tight tolerances suited to mass-produced engine and transmission parts. Automated multi-cavity tools operating under high pressure deliver surface finishes that minimize downstream machining and meet stringent porosity limits imposed by OEM quality audits. In contrast, gravity and squeeze variants remain essential for thicker wall sections such as cylinder heads, where slower fill rates prevent hot-tearing defects.

Vacuum die casting posts the fastest 6.85% CAGR because battery tray manufacturers demand near-zero gas entrapment to comply with fire-propagation tests. Foundries incorporate real-time pressure sensors and digital twin simulations to meet these stricter process windows, further modernizing the Brazilian automotive parts aluminum die-casting industry. Semi-solid/rheocasting remains a niche technology but is gaining traction for large, complex gearbox housings that combine low-turbulence flow with fine microstructures for high mechanical strength.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application Type: Engine Parts Hold Lead While Battery Housings Accelerate

Engine parts (engine blocks, cylinder heads, and intake manifolds) captured a 39.04% share of the Brazilian automotive parts aluminum die casting market size in 2024, powered by Brazil’s enduring flex-fuel architecture, where ethanol compatibility calls for corrosion-resistant aluminum substrates. Cylinder heads alone represent a multi-year backlog following HORSE’s introduction of its new line in Curitiba. Yet, growth rates are shifting toward electrification components; e-mobility battery housings and thermal systems are forecast to grow at a 7.85% CAGR through 2030, increasing the Brazilian automotive parts aluminum die casting market size for e-mobility parts by 2030.

These enclosures require intricate cooling channels and strict straightness tolerances of less than 0.2 mm, driving the adoption of CT scanning and in-die vacuum sensors, which are otherwise uncommon in engine casting. Body and structural castings log mid-single-digit expansion tied to platform modularity, where automakers unify cross-members and shock towers across global programs.

By Vehicle Type: Passenger Cars Dominate Volume and Innovation

Passenger cars accounted for a 54.16% share of the Brazilian automotive parts aluminum die casting market size in 2024 and are projected to grow at a 6.44% CAGR as hybrid SUVs enter Brazilian showrooms. Assemblers favor common cylinder-block architectures across sedan and crossover derivatives, amplifying order stability for Tier-1 foundries. Two-wheelers maintain a significant share of the Brazilian automotive parts aluminum die casting industry, as urban congestion continues to make motorcycles attractive, and their engines rely on lightweight aluminum crankcases.

Light commercial vans add volume as e-commerce accelerates final-mile deliveries; OEMs specify thin-wall, die-cast transmission housings that shed kilograms while meeting durability targets. Heavy trucks and buses gradually switch to aluminum cross-members to offset battery weight as EV drivelines penetrate fleet orders, reinforcing broad-based growth for the Brazilian automotive parts aluminum die casting market.

By Casting Alloy Family: Al-Si Leads as Al-Mg Emerges

Al-Si grades, such as ADC12 and LM-6, represented a 73.11% share of the Brazilian automotive parts aluminum die casting market size in 2024, as they offer reliable fluidity and machinability at a modest alloying cost. These alloys underpin legacy engine parts as well as body mounts, where solidification defects must stay below one cc per casting. The Brazilian automotive parts aluminum die casting market size for Al-Mg alloys is projected to expand with a 7.22% CAGR, because greater strength-to-weight ratios suit battery-carrier designs that anchor heavy packs to floor pans.

Al-Cu and specialty alloys remain limited to stress-heavy drive shafts and brake calipers, yet benefit from process advances that reduce copper-induced hot-cracking. Recycling initiatives raise questions about alloy purity; new melt-sorting sensors at Rima Industrial ensure that secondary feedstock meets the ABNT 6834 chemical windows, supporting a secure long-term alloy supply for Brazilian foundries.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: OEM and Tier-1 Concentration Shapes Supply Chain

OEMs/Tier-1 integrators held an 83.24% share of the Brazilian automotive parts aluminum die casting market size in 2024, leveraging long-term agreements that secure capacity and align quality requirements with IATF 16949 audits. Their volumes are projected to expand at a 6.15% CAGR by 2030, as assemblers localize more sub-systems to buffer currency swings and freight risk. Close collaboration often means that engineering teams co-locate near casting cells to shorten product development cycles.

The independent aftermarket share rests at 16.76% but becomes strategic for smaller foundries, allowing them to avoid significant CAPEX. In 2024, Brasil Auto Parts, an export-oriented group, achieved significant immediate sales and is aiming for substantial growth over the coming years. This trajectory underscores a growing global recognition of the quality offered by Brazilian products. Certification to INMETRO standards secures access to domestic replacement networks, underpinning diverse growth avenues inside the Brazilian automotive parts aluminum die casting market.

Geography Analysis

São Paulo anchors the Brazilian automotive parts aluminum die casting market, generating significant revenue due to its dense corridor that places foundries within a 50 km radius of Volkswagen, General Motors, and Ford stamping plants. The state’s SENAI network graduates a significant number of metalworking technicians annually, easing hiring bottlenecks during periods of ramp-up. Well-paved logistics and port proximity enable quick inbound aluminum coil deliveries from CBA and Alcoa smelters as well as efficient export routes to Mercosur.

Santa Catarina logs stronger growth as its Joinville cluster leverages German manufacturing heritage. In the region, several precision toolmakers, including Herten and JN, manufacture aluminum molds annually and maintain ISO 14001 environmental accreditation. With support from the regional development agency FIESC, these toolmakers have implemented energy-efficient melting furnaces, which have significantly enhanced their energy efficiency. This progress has positioned local firms as premium suppliers for battery tray programs intended for industry leaders such as BYD and Great Wall.

Minas benefits from Thyssenkrupp’s Poços de Caldas plant, slated to boost camshaft blanks. At the same time, Paraná hosts HORSE’s new gravity-casting line in Curitiba, which will deliver 210,000 cylinder heads after its 2026 start-up [3]“Investment Announcement Curitiba Plant,” HORSE Powertrain, horse-powertrain.com. Both states attract near-shoring investments seeking lower labor attrition and favorable tax regimes under Sudene incentives. Northern and northeastern regions remain minor contributors due to their thinner supplier bases, but solar-powered mini-foundries near Recife are piloting MMGD schemes that could scale later in the decade.

Competitive Landscape

Moderate concentration defines the Brazilian automotive parts aluminum die casting market. Nemak, WHB Automotive, and Rima Industrial combine integrated smelter access with automated 1,200-ton presses and internal tool shops, enabling 48-hour sample delivery for OEM engineering freezes. Their dominance is challenged by multinational entrants such as Rheinmetall and Linamar that install Industry 4.0 cells with closed-loop shot monitoring.

Strategic positioning now revolves around high-growth EV structures where vacuum die casting is essential. Starcast recently commissioned a CQI-27 compliant 840-ton line that includes laser-guided ladles and AI-based vision sorters, capturing battery housing orders from BYD and Stellantis. Iochpe-Maxion uses FINEP funds to roll out digital twins across its wheel plants, cutting trial-cast iterations by 40% and bringing cross-functional analytics in-house.

Market consolidation looms as smaller foundries face dual pressures of automation, CAPEX, and technician scarcity. Acquisition pipelines are active; WHB scouted regional players in Santa Catarina to gain mold-design depth. Quality marks such as IATF 16949 and ISO 50001 remain gateways to OEM panels, preserving incumbents’ advantage. Export orientation broadens competitiveness; Nemak ships head castings to Mexico under USMCA rules, affirming Brazil’s role in multinational sourcing schemes.

Brazil Automotive Parts Aluminum Die Casting Industry Leaders

Nemak, S.A.B. de C.V.

WHB Automotive S.A.

Rima Industrial S.A.

Wetzel S/A

Form Technologies, Inc. (Dynacast)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Hydro signed a letter of intent with Nemak to co-develop low-carbon aluminum cast products for engine and structural parts, aiming to achieve a 30% carbon reduction by 2030 through the use of renewable electricity and boiler electrification at the Alunorte refinery.

- September 2024: HORSE invested EUR 32.8 million (~USD 37.9 million) to install a gravity-casting line in Curitiba, which will deliver 210,000 aluminum cylinder heads annually by 2026, utilizing inorganic sand to minimize waste.

Brazil Automotive Parts Aluminum Die Casting Market Report Scope

The Brazilian Automotive Parts Aluminum Die Casting Market segments its offerings by Production Process (including Pressure Die Casting and Vacuum Die Casting), Application Type (such as Engine Parts and Body and Structural Parts), Vehicle Type (covering Passenger Cars and Two-Wheelers), Casting Alloy Family (featuring Al-Si Alloys and Al-Mg Alloys), and End-User (Original Equipment Manufacturer (OEM) / Tier-1 Suppliers, and independent aftermarket).

Market forecasts are presented in terms of value (USD).

By Production Process

| Pressure Die Casting |

| Vacuum Die Casting |

| Squeeze Die Casting |

| Gravity Die Casting |

| Semi-solid / Rheocasting |

By Application Type

| Engine Parts |

| Body and Structural Parts |

| Transmission and Driveline Parts |

| E-mobility Battery Housings and Thermal Systems |

| Other Applications (HVAC, Steering, Braking) |

By Vehicle Type

| Passenger Cars |

| Two-Wheelers |

| Three-Wheelers |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles and Buses |

By Casting Alloy Family

| Al-Si Alloys (ADC12, LM-6 etc.) |

| Al-Mg Alloys |

| Al-Cu and Others |

By End-User

| Original Equipment Manufacturer (OEM) / Tier-1 Suppliers |

| Independent Aftermarket |

| By Production Process | Pressure Die Casting |

| Vacuum Die Casting | |

| Squeeze Die Casting | |

| Gravity Die Casting | |

| Semi-solid / Rheocasting | |

| By Application Type | Engine Parts |

| Body and Structural Parts | |

| Transmission and Driveline Parts | |

| E-mobility Battery Housings and Thermal Systems | |

| Other Applications (HVAC, Steering, Braking) | |

| By Vehicle Type | Passenger Cars |

| Two-Wheelers | |

| Three-Wheelers | |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles and Buses | |

| By Casting Alloy Family | Al-Si Alloys (ADC12, LM-6 etc.) |

| Al-Mg Alloys | |

| Al-Cu and Others | |

| By End-User | Original Equipment Manufacturer (OEM) / Tier-1 Suppliers |

| Independent Aftermarket |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the Brazil automotive parts aluminum die casting size in 2025?

The segment is valued at USD 0.61 billion in 2025.

What CAGR is forecast for Brazil automotive parts aluminum die casting between 2025 and 2030?

It is projected to expand at a 5.59% CAGR through 2030.

Which production process currently holds the largest revenue share in Brazil automotive parts aluminum die casting?

Pressure die casting leads with a 65.13% share.

How significant is passenger car demand within Brazil automotive parts aluminum die casting?

Passenger cars account for 54.16% of total revenue and show a 6.44% CAGR outlook.