Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

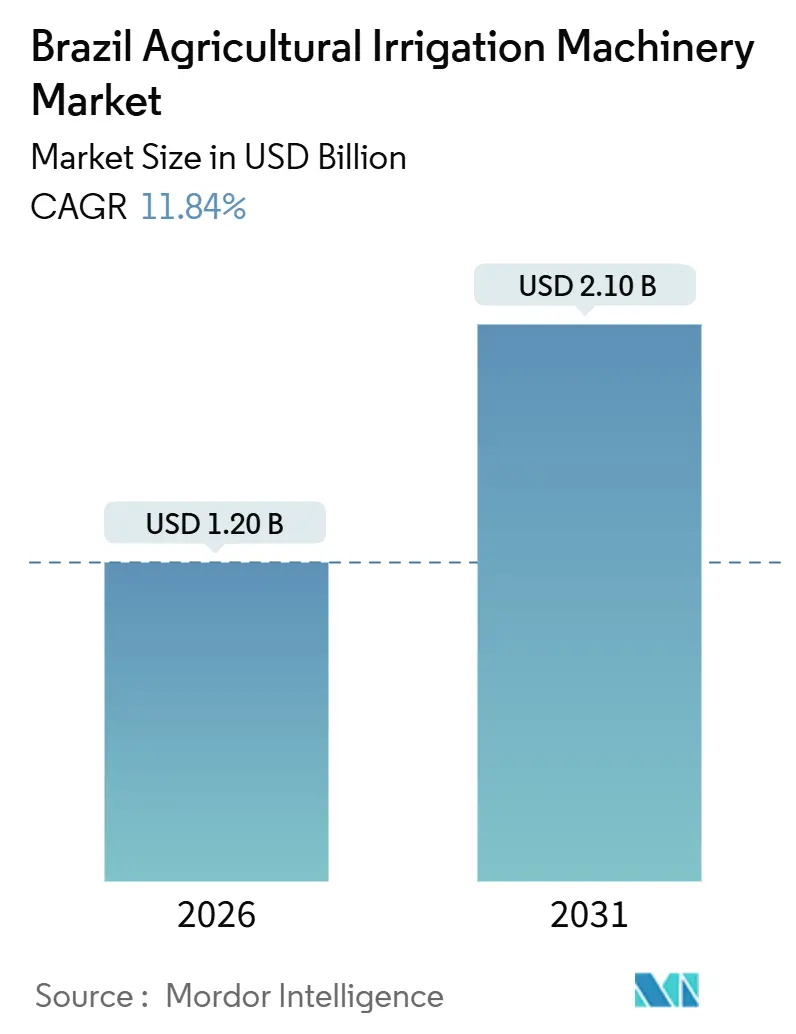

| Market Size (2026) | USD 1.20 Billion |

| Market Size (2031) | USD 2.10 Billion |

| Growth Rate (2026 - 2031) | 11.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Agricultural Irrigation Machinery Market Analysis by Mordor Intelligence

The Brazil agricultural irrigation machinery market size is USD 1.20 billion in 2026 and is forecast to reach USD 2.10 billion by 2031, reflecting an 11.84% CAGR. Demand is accelerating as growers replace flood and surface methods with pressurized systems that cut water use by 30% to 40% while safeguarding yields during recurring droughts. Federal credit lines under Plano Safra and Proirriga have injected USD 520 million (BRL 2.6 billion) into equipment purchases, thereby flattening upfront cost barriers for medium-sized operations. The rapid spread of center-pivot technology across the Cerrado, niche growth in drip solutions for fruit and vegetable belts, and surging adoption of solar-hybrid pumps together underpin the current expansion path. Competitive intensity remains moderate, with the top five companies controlling just over half of the revenue and differentiating themselves through localized factories, digital platforms, and renewable energy integrations.

Key Report Takeaways

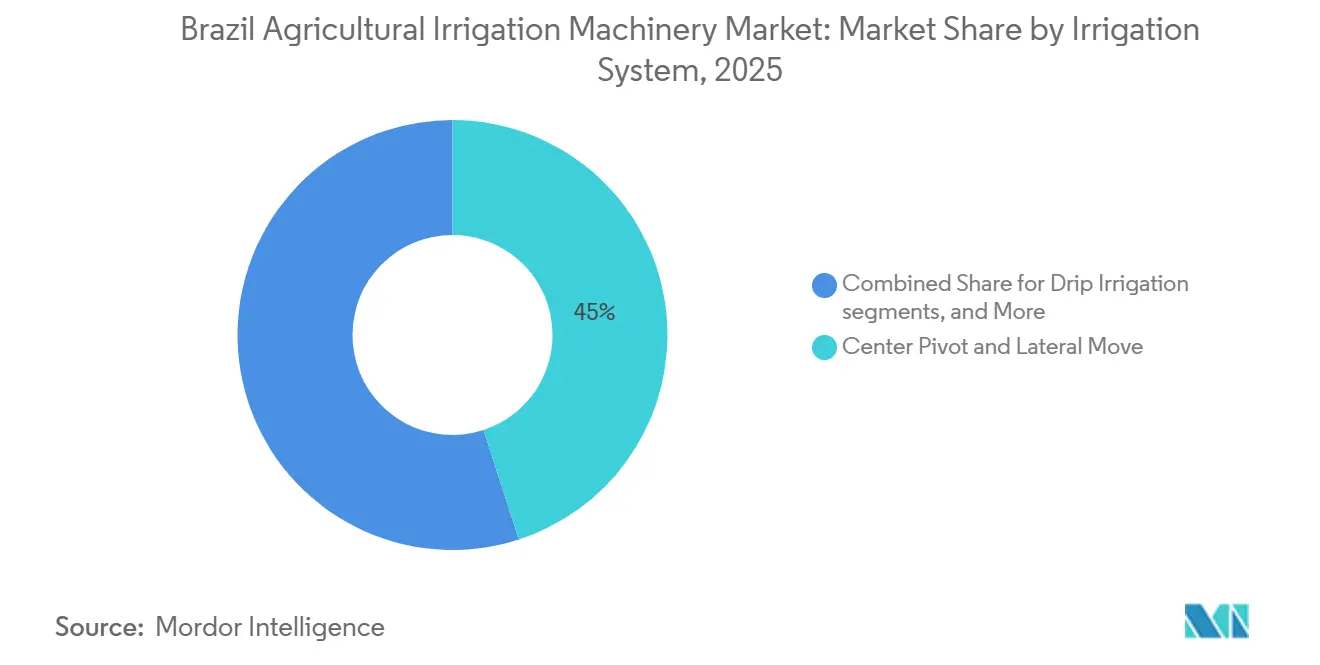

- By irrigation system, center-pivot and lateral-move captured 45% of the Brazil agricultural irrigation machinery market share in 2025, while drip irrigation is projected to post a 15.0% growth through 2031.

- By crop type, cereals and grains accounted for 52% of the Brazil agricultural irrigation machinery market size in 2025, and fruits and vegetables are projected to rise at a 13.0% CAGR to 2031.

- By farm size, large commercial operations held 70% of the Brazil agricultural irrigation machinery market revenue share in 2025, while medium farms are projected to post the fastest growth at 12% CAGR through 2031.

- By component, pumps and motors accounted for 28% of the Brazil agricultural irrigation machinery market size in 2025, while controllers and sensors are advancing at a 16% CAGR between 2026 and 2031.

- By energy source, grid-electric accounted for 60.0% of the Brazil agricultural irrigation machinery market size in 2025, and solar and hybrid systems achieved an 18% CAGR through 2031.

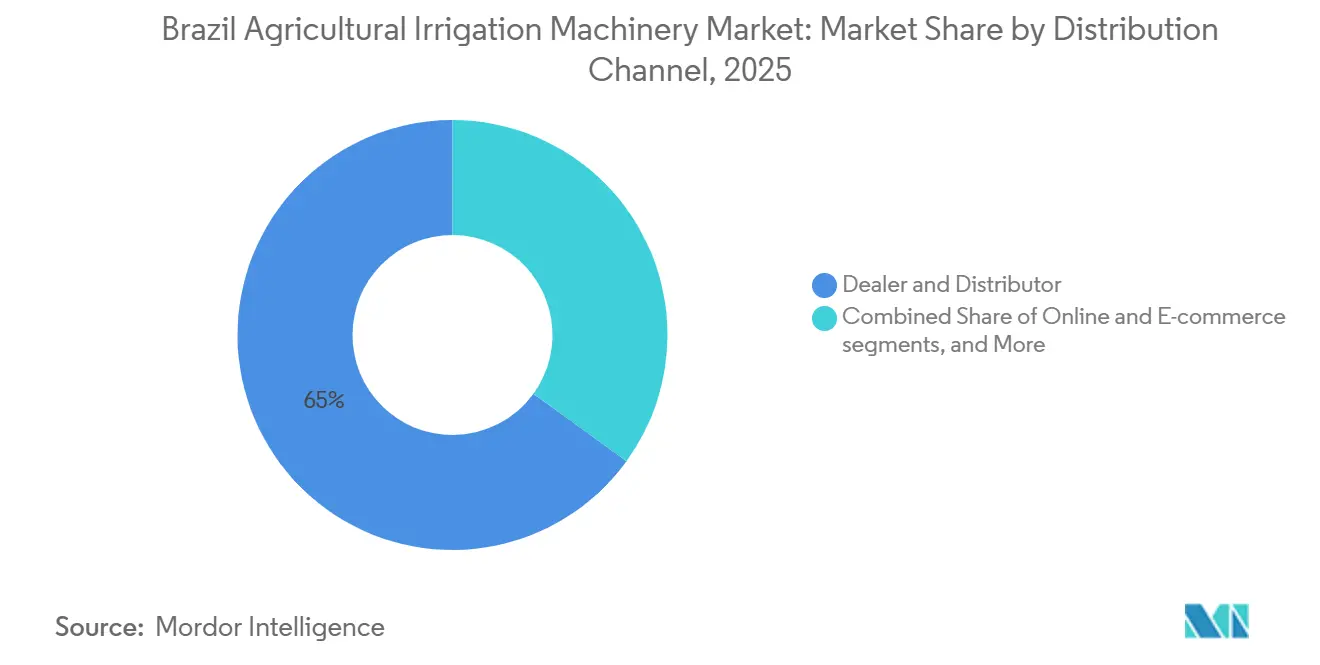

- By Distribution Channel, dealer & distributor accounted for 65% of the Brazil agricultural irrigation machinery market size in 2025, while online & -commerce is projected to post a 19.0% growth through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Agricultural Irrigation Machinery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidized Credit Lines Under Moderinfra And ABC+ | +2.3% | National focus in Mato Grosso, Goiás, São Paulo | Medium term (2–4 years) |

| Expansion of Center-Pivot Irrigated Area In Cerrado | +2.8% | Mato Grosso, Goiás, Tocantins, western Bahia | Long term (≥ 4 years) |

| Precision Agriculture And Remote Monitoring Uptake | +1.9% | São Paulo, Paraná, Mato Grosso | Medium term (2–4 years) |

| Rising Drought Frequency And Climate Variability | +2.1% | São Francisco and Paraná basins, Northeast | Short term (≤ 2 years) |

| Solar-powered Pumping Systems Offsetting Diesel Costs | +1.5% | Grid-constrained rural zones nationwide | Medium term (2–4 years) |

| Sugarcane Rail-cleaner Retrofits For Pivots | +1.2% | São Paulo, Goiás, Minas Gerais | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subsidized Credit Lines Under Moderinfra And ABC+

Federal programs have transitioned irrigation from a cash-based purchase model to a financed asset approach. Plano Safra 2024/25 allocated BRL 475.5 billion (USD 95.1 billion) for rural lending, including BRL 2.6 billion (USD 520 million) designated for irrigation under Proirriga[1]Source: BNDES, “Proirriga Rural Credit Summary,” bndes.gov.br. Low rates of 5% to 7% replace commercial costs above 12%, leading to a 34% year-over-year gain in irrigation loans during the first half of 2025. Medium farms now secure credit in roughly 120 days, compared with more than 180 days in 2023, enabling system payback within five crop cycles.

Expansion of Center-Pivot Irrigated Area In Cerrado

The 2025 report by the Brazilian Agricultural Research Corporation (Embrapa) highlights that the area in Brazil irrigated using central pivots increased from 1.92 million hectares in 2022 to 2.2 million hectares, marking a growth of over 14% in two years. The typical Cerrado pivot spans 65 to 80 hectares, leveraging scale to dilute capital outlays across high-volume soybean and corn rotations. Strong demand drove Valmont’s Uberaba factory to ship 1,240 units in 2024, a 19% annual lift. Yet permit applications in the Araguaia-Tocantins basin climbed 27% in 2025, portending regulatory queues[2]Source: National Water Agency, “Drought Management Reports 2024-25,” ana.gov.

Precision Agriculture And Remote Monitoring Uptake

Digital overlays transform fixed-rate equipment into dynamic tools. Lindsay Corporation’s FieldNET manages 3,200 Brazilian pivots, trimming water use by up to 22% through zone-based dosing. A 2024 survey by the Brazilian Agricultural Research Corporation (Embrapa) found that 84% of large farms used at least one digital tool, and 29% had connected irrigation controllers. Rising labor costs up 31% in Mato Grosso between 2020 and 2024, further accelerating automation.

Rising Drought Frequency And Climate Variability

Brazil endured three severe droughts from 2020 to 2025, cutting rain-fed soybean yields by as much as 25%. Reservoirs in the São Francisco basin fell below 40% in 2024, prompting temporary permit bans for new surface withdrawals. The National Institute for Space Research (INPE) modeling projects a 10% to 15% rainfall decline across the Cerrado by 2040, thereby raising the long-term risk. These shocks are forcing a pivot from open-ditch irrigation, which currently accounts for 5% of equipped land, to pressurized systems that conserve scarce water supplies.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost And Limited Long-term Credit | -1.8% | Medium farms nationwide | Short term (≤ 2 years) |

| Commodity-price Volatility Squeezing Farm Cash Flow | -1.5% | Export-dependent states | Short term (≤ 2 years) |

| Stricter Water License Enforcement In Stressed Sub-basins | -1.2% | São Francisco, Paraná, Araguaia-Tocantins | Medium term (2–4 years) |

| Limited Technical Assistance For O&M Among Mid-size Farms | -0.9% | Nationwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost And Limited Long-term Credit

The installation of a 65-hectare pivot costs between USD 180,000 and USD 250,000, which is equivalent to three to four years of net income for an average medium-sized soybean farm[3]Source: World Bank, “Financing Constraints in Brazilian Agriculture,” worldbank.org. This high upfront cost poses a financial challenge for many farmers. Although Proirriga provides loans at below-market rates, the loan maturities typically do not exceed seven years. As a result, farmers face annual payments exceeding USD 30,000, which can strain their financial resources. Smallholders encounter even greater difficulties, as a 10-hectare drip irrigation system costs between USD 25,000 and USD 35,000. However, financing options are limited, as most lenders do not support projects below USD 50,000, leaving smallholders with fewer viable solutions for irrigation investments.

Commodity-price Volatility Squeezing Farm Cash Flow

Soybean contract prices declined from USD 16.50 to USD 14.50 per bushel in 2024, reducing gross margins for Cerrado growers by 12%. This decline in prices significantly impacted the profitability of soybean farmers, particularly in regions heavily reliant on soybean cultivation. Valmont attributed a 9% year-over-year decline in Brazilian pivot orders during Q3 2024 to "farmer caution," as growers hesitated to invest in new equipment amidst falling margins. Additionally, currency depreciation exacerbated challenges, as the Brazilian real weakened from 4.95 to 5.20 per USD during the same period. This depreciation increased the cost of imported components by 5%, further straining the financial stability of farmers and agricultural businesses reliant on imported machinery and inputs.

Segment Analysis

By Irrigation System: Pivots Dominate, Drip Gains in Specialty Crops

Center-pivot and lateral-move units accounted for 45% of the Brazil agricultural irrigation machinery market in 2025, bolstered by Cerrado farms measuring 200 to 500 hectares and seeking labor savings through automation. Variable-rate retrofits are poised to rise as FieldNET and Trimble integrations enable zone-specific dosing. Sprinkler systems, holding a significant share, concentrate in smaller perennial orchards such as coffee and citrus, where capital costs remain pivotal. Drip, with a 20% share, is accelerating at 15% CAGR on fruit and vegetable acreage across the Northeast semi-arid and São Paulo citrus belt, where high crop value justifies USD 3,500 to 5,000 per-hectare outlays.

Micro-irrigation systems offer efficiency by addressing specific water demands. Rivulis installed subsurface lines across 8,400 hectares during 2024–25, while Stara’s mobile-drip pivot kit is priced 20% lower than global competitors. Surface irrigation methods now represent 5% of installations and are declining due to enforcement by the National Water Agency (ANA) and increasing drought pressures. Furthermore, with the adoption of digital sensors, soil-moisture probes are now pre-installed on 35% of new pivots, compared to 12% in 2020.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop Type: Cereals Lead, Fruits and Vegetables Accelerate

Cereals and grains represented 52% of demand in 2025, buoyed by soybean and corn double-cropping that leans on irrigation to stabilize output during the 5-month Cerrado dry season. The segment will grow near-parity with the overall Brazil agricultural irrigation machinery market through 2031, reflecting durable export pipelines to Asia. Commercial crops, primarily sugarcane and cotton, held a significant share after cereals and grains. Sugarcane irrigation alone is pacing at a higher growth rate as mills chase sucrose premiums. Fruits and vegetables are growing at a 13% CAGR because drip increases export-grade quality, lifting citrus Brix and grape counts.

Pulses and oilseeds, such as black beans, require precise water management during the pod-filling stage to enhance export potential. Effective irrigation during this critical growth phase ensures optimal yield and quality, which are essential for meeting international market standards. Other uses, including pasture and forestry, remain limited to niche markets, with potential for gradual expansion as demand evolves. According to the Brazilian Sugarcane Industry Association (UNICA), the irrigated sugarcane area increased from 7% in 2020 to 12% in 2025, indicating a growing market for irrigation equipment suppliers in the agricultural sector. This growth highlights the increasing adoption of irrigation technologies to improve productivity and sustainability in sugarcane farming.

By Farm Size: Large Operators Dominate, Mid-Tier Gains Momentum

Large commercial operations over 100 hectares captured 70% of 2025 sales, revealing a clear scale bias within the Brazil agricultural irrigation machinery market. These enterprises deploy multiple pivots and integrate fleet-management software that cuts supervisory labor 25% to 30%. Medium farms, growing at a 12% CAGR to 2031, as flexible credit products and smaller 40 to 50 hectare pivots align with their capital ceilings. Smallholders under 20 hectares take up the remaining share, centered on drip for high-value horticulture.

Cooperative models lessen cost friction. A 2024 Paraná pilot had 12 farms jointly finance a lateral-move unit covering 480 hectares, paring individual exposure by 60%. Smallholders still battle thin margins, with loans under USD 50,000 rare, yet targeted subsidy pools could unlock micro-irrigation at a broader scale. Large enterprises continue pushing digital frontiers, bundling sensors, GPS steering, and variable-rate tech for whole-farm orchestration.

By Component: Pumps Lead, Controllers Surge

Pumps and motors delivered 28% of component turnover in 2025, sustained by replacement cycles and the pivot to variable-frequency drives that slash energy use up to 30%. Sprinklers and emitters benefit from rapid drip deployment. Netafim’s pressure-compensated emitter now features on 60% of new Brazilian drip lines. Controllers and sensors represent the fastest-growth rate at 16% CAGR as Internet of Things (IoT) connectivity and falling hardware prices draw mainstream adoption.

Valves and filters hold a small share, supported by the National Water Agency (ANA)'s metering regulations, while pipes, hoses, and structural steel comprise a significant portion. Energy-efficiency labeling, introduced in 2024 for pumps above 10 horsepower, is spurring retrofit spending. Meanwhile, Trimble-enabled GPS receivers in pivot towers promote sub-meter accuracy, enhancing fertigation outcomes for specialty crops in São Paulo’s citrus groves.

By Energy Source: Grid Dominates, Solar Ascends

Grid-electric systems represented 60% of installations in 2025, particularly in São Paulo and Paraná, where power reliability remains high. Diesel pumps continue to be used in frontier regions but are experiencing slower growth due to the unpredictability caused by fuel price volatility. Solar-hybrid systems are growing at a compound annual growth rate (CAGR) of 18% and are projected to gain market share through 2031, driven by declining panel costs and supportive feed-in tariffs. Biogas and wind systems remain niche options, limited by high upfront costs and technical challenges.

The Brazilian Agricultural Research Corporation (Embrapa) estimates that a 65-hectare solar pivot system, costing USD 240,000, can save USD 18,000 annually in energy expenses, resulting in a payback period of 4.3 years, more favorable compared to grid-based or diesel-based systems. Additionally, FieldNET demand-management modules enable irrigation during off-peak hours, reducing electricity bills by 40% and increasing the attractiveness of grid connectivity in areas with mixed tariff structures.

By Distribution Channel: Dealers Prevail, E-Commerce Emerges

Dealers and distributors orchestrated 65% of 2025 revenue within the Brazil agricultural irrigation machinery market, harnessing localized service crews and bundled financing. Direct OEM contracts are skewed toward large farms negotiating multi-pivot orders. Online platforms are surging at a 19% CAGR as transparent pricing and remote diagnostics appeal to tech-savvy mid-size growers.

Rivulis’ Portuguese-language design portal generated 1,800 verified leads in its first year. Lindsay Corporation’s dealer portal accelerates troubleshooting by 30%, while Stara’s Agrishow-launched mobile-drip kit accepted 80 pre-orders at 20% below multinational quotes. Cooperatives and public purchasing schemes round out the remaining 5%, often tying equipment supply to regional development grants.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Cerrado biome, spanning Mato Grosso, Goiás, Tocantins, and western Bahia, holds a significant share of center-pivot capacity as of 2025, driven by large-scale soybean and corn farms that integrate irrigation to sustain double-cropping under an increasingly erratic rainy season. Mato Grosso alone added 14,200 pivot hectares in 2024, reflecting a 9% annual climb. São Paulo followed with a 22% share, concentrating on sugarcane, citrus, and coffee, where drip and micro-sprinkler systems dominate due to higher returns per hectare.

Western Bahia’s MATOPIBA frontier is gaining traction, registering a 21% pivot installation spike in 2024, though licensing bottlenecks in the São Francisco watershed may temper momentum. The Northeast semi-arid zone, anchoring fruit export clusters along the São Francisco Valley, captured 8% of national sales in 2025 due to drip adoption covering 120,000 hectares. Southern states Paraná and Rio Grande do Sul held a combined 12% share, applying irrigation mostly to rice and vegetables, where frequent rainfall still demands supplemental coverage amid yield-critical growth stages[4]Source: IBGE, “Agricultural Census 2025,” ibge.gov.br.

Regional growth is determined by the relationship between water governance and aquifer depth. Guarani and Bambuí reserves underpin the scalability of the Cerrado. However, the National Institute for Space Research (INPE) projects a 10% to 15% decline in rainfall by 2040, which stresses recharge rates. São Paulo’s mature footprint is pivoting to retrofits. Nearly half of citrus growers now layer soil-moisture sensors on top of existing drip irrigation grids, pairing water consumption with an 18% reduction in water usage without sacrificing quality. Meanwhile, cost overruns at the São Francisco River Integration Project hinder the Northeast’s full potential, although the scheme already supplies 160,000 irrigated hectares. In the South, mixed rainfall patterns and smaller field sizes keep demand steady but capped.

Competitive Landscape

The Brazil agricultural irrigation machinery market is moderately concentrated, with the top five companies, including Valmont Industries Inc., Lindsay Corporation, Bauer Group, Netafim Limited, and Rivulis Irrigation Ltd. (Temasek Holdings Limited) are holding a significant market share. Valmont Industries Inc. holds a notable position, supported by its Uberaba plant, a planned 30% capacity expansion by 2025, and a service network spanning 22 states. Lindsay Corporation holds the second-largest share, driven by FieldNET’s 3,200 domestic subscriptions and a parts hub in Campinas that reduces client downtime. Bauer Group has capitalized on the retrofit opportunities in the sugarcane sector, achieving a 25% sales growth in 2024.

Competition in the market focuses on factory localization, precision integrations, and the incorporation of renewable energy solutions. Valmont’s Solbras unit combines photovoltaic technology with irrigation pivots, achieving a 70–80% reduction in operating costs over a ten-year period. Lindsay collaborates with FieldNET Advisor, offering services at an annual fee of USD 3,000 per pivot, generating revenue through agronomic data utilization. Bauer’s rail-cleaner upgrade addresses the issue of trash clogging in sugarcane rows, a persistent operational challenge.

Domestic manufacturers, such as Stara and Jacto, capitalize on local supply chains to price their products 15% to 20% lower than multinational competitors. However, they currently lack advanced digital control systems. Moving forward, opportunities for market growth lie in medium-farm financing, precision retrofitting, and innovations tailored to sugarcane farming, which represent untapped areas for potential market share expansion.

Brazil Agricultural Irrigation Machinery Industry Leaders

Valmont Industries, Inc.

Lindsay Corporation

Bauer Group (Bauer AG)

Netafim Limited (Orbia Advance Corporation)

Rivulis Irrigation Ltd. (Temasek Holdings Limited)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Komet Irrigation expanded Digital and Engineering Capabilities with a New Innovation Hub in Brazil. The hub will focus on developing real-time digital tools to optimize irrigation performance, increase yields, and enhance farm profitability.

- February 2025: Netafim Limited announced the launch of its patented Hybrid Dripline system. This system is the first integral dripline with a built-in outlet. The proprietary technology combines the advantages of integral and online dripper systems, offering a leak-free, clog-resistant, and labor-saving solution for growers worldwide, including Brazil.

- January 2025: Rivulis Irrigation Ltd. has formed an exclusive partnership with Cocamar. This collaboration aims to provide advanced irrigation solutions to farmers, improving water efficiency and increasing crop yields, particularly in response to the challenging weather conditions that have affected Brazilian agriculture in recent years.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Brazil agricultural irrigation machinery market covers all factory-built center-pivot, linear move, sprinkler, and drip systems, together with integrated pumps, drives, pipes, couplers, and control units, sold for in-field crop irrigation across Brazil's five macro-regions.

Scope Exclusion: Portable hoses, standalone sensors, and aftermarket spare parts that are sold outside an original equipment package are not covered.

Segmentation Overview

- By Irrigation System

- Drip Irrigation

- Sprinkler Irrigation

- Center Pivot and Lateral Move

- Micro-Irrigation

- Surface/Flood

- Others

- By Crop Type

- Cereals and Grains

- Commercial Crops

- Fruits and Vegetables

- Pulses and Oil Seeds

- Others

- By Farm Size

- Smallholders (Less than 20 ha)

- Medium Farms (20-100 ha)

- Large Commercial Farms (More than 100 ha)

- By Component

- Pumps and Motors

- Pipes and Hoses

- Sprinklers and Emitters

- Valves and Filters

- Controllers and Sensors

- Others

- By Energy Source

- Grid-Electric

- Diesel

- Solar and Hybrid

- Others

- By Distribution Channel

- Direct OEM Sales

- Dealer and Distributor

- Online and E-commerce

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with irrigation dealers, bank credit officers, and farm-level agronomists across the Central-West, Northeast, and South. Respondents validated adoption hurdles, average selling prices, and replacement cycles, filling data gaps left by desk research and enabling assumption triangulation.

Desk Research

Our analysts first compiled macro- and meso-level inputs from tier-1, non-paywalled sources such as Brazil's National Water Agency irrigated-area survey, IBGE farm machinery census, MAPA import/export filings, and BNDES rural-credit disbursement dashboards. Trade association bulletins (ABIMAQ, ABHR) and reputable press archives accessed through Dow Jones Factiva supplied unit shipments and tender awards, while Questel patent analytics revealed technology diffusion rates. D&B Hoovers financials helped us benchmark leading suppliers' Brazil revenue trails. This list is illustrative; many other public and paid sources informed data collection and cross-checks.

Market-Sizing & Forecasting

We use a top-down model that reconstructs demand from irrigated-hectare pools, applying machinery density ratios by crop and farm size. Results are then corroborated with sampled bottom-up roll-ups of supplier shipments and channel checks. Key variables feeding the model include new irrigated-area additions, machinery replacement interval, average equipment price, rural-credit volumes, and BRL-USD exchange trajectory. Forecasts to 2030 rely on multivariate regression linking equipment uptake to commodity margins, rainfall anomalies, and credit cost, with scenario stress tests reviewed by primary experts.

Data Validation & Update Cycle

Outputs pass multi-layer analyst review, variance checks against independent indicators, and anomaly flagging before sign-off. The study refreshes annually, with interim updates triggered by material events, for example, policy shifts in Plano Safra. Before release, an analyst reruns the latest data sweep so clients receive our most current view.

Credibility Anchor: Why Our Brazil Agricultural Irrigation Machinery Baseline Commands Reliability

Published estimates often diverge because firms pick different product baskets, pricing bases, and forecast cadences.

Key gap drivers here include: some publishers strip out solar-powered pumps, others freeze exchange rates at prior-year averages, and a few report only OEM factory-gate turnover, while Mordor presents end-market equipment value net of VAT but inclusive of bundled controllers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 1.29 B (2025) | Mordor Intelligence | - |

| 0.81 B (2024) | Regional Consultancy A | Excludes drip kits and solar pump assemblies |

| 1.20 B (2024) | Global Consultancy B | Uses retail prices with taxes, constant-2023 FX rates |

| 0.10 B (2024) | Industry Association C | Counts only pivot OEM shipments; smallholder systems omitted |

In sum, Mordor's disciplined scope selection, blended top-down/bottom-up logic, and annual refresh cadence deliver a balanced, transparent baseline that decision-makers can readily trace and replicate.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the Brazil agricultural irrigation machinery market in 2031?

The market is projected to reach USD 2.10 billion by 2031.

Which irrigation system currently holds the largest share?

Center-pivot and lateral-move systems led with 45% share in 2025.

How fast are solar-powered irrigation systems growing?

Solar and hybrid solutions are expanding at an 18% CAGR through 2031.

Which component segment is expanding the quickest?

Controllers and sensors are advancing at a 16% CAGR between 2026 and 2031.

Why are medium-sized farms expected to grow their spending?

Easier access to subsidized credit and smaller pivot models align with their capital profiles, supporting a 12% CAGR.