Bottle-Capping Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

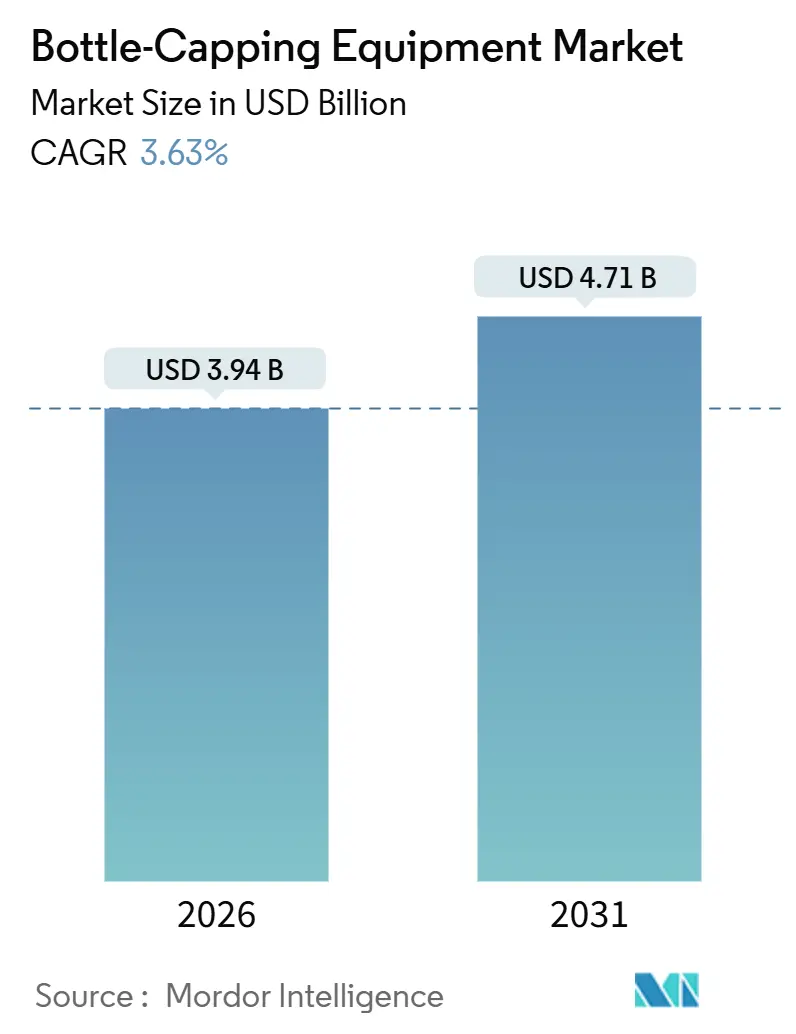

| Market Size (2026) | USD 3.94 Billion |

| Market Size (2031) | USD 4.71 Billion |

| Growth Rate (2026 - 2031) | 3.63% CAGR |

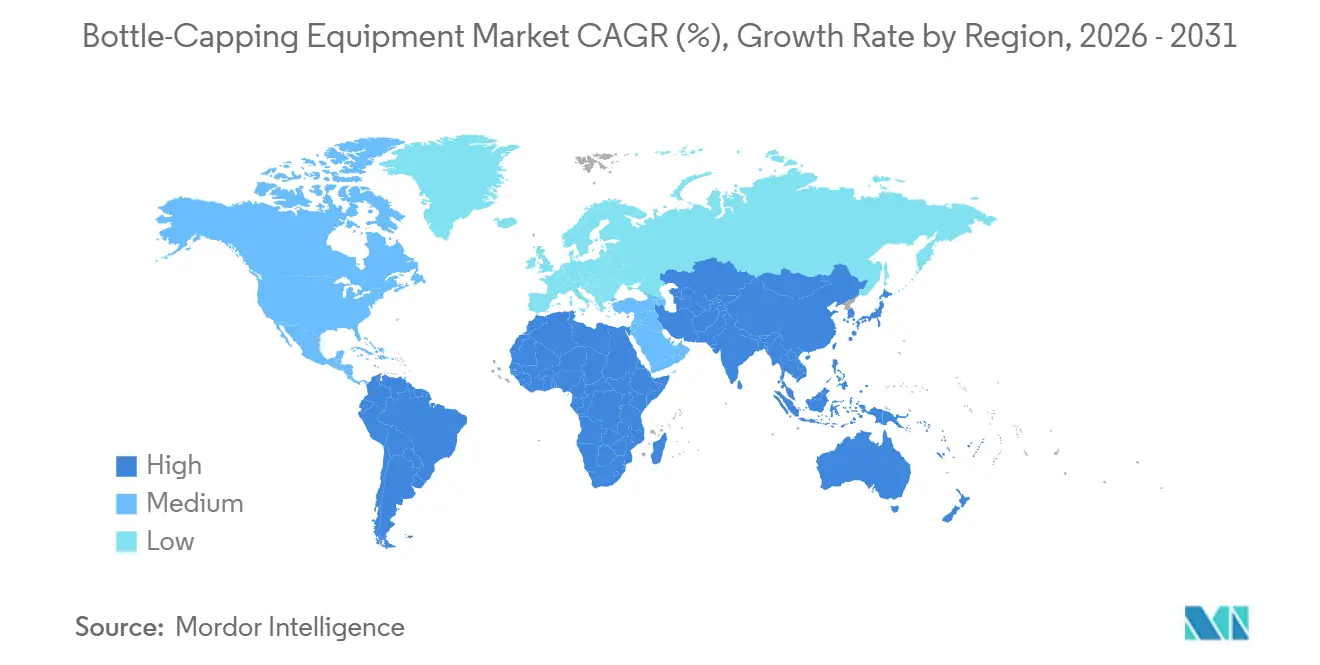

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bottle-Capping Equipment Market Analysis by Mordor Intelligence

The bottle-capping equipment market size is valued at USD 3.94 billion in 2026 and is projected to reach USD 4.71 billion in 2031, reflecting a 3.63% CAGR through the forecast period. Fully automatic, servo-driven platforms are outpacing this headline growth, already holding 68.27% revenue share in 2025 and expanding at 5.72% as beverage and pharmaceutical producers seek validated torque control, rapid changeovers, and predictive-maintenance compatibility. The Asia-Pacific region accounts for 39.51% of 2025 sales and is expected to accelerate at 6.59%, driven by the establishment of greenfield bottling plants, increased contract packaging uptake, and favorable industrial policies. Meanwhile, Europe’s Single-Use Plastics Directive and forthcoming Packaging and Packaging Waste Regulation compress retrofit timelines, pushing OEMs toward tethered-cap-ready heads that avoid throughput penalties. Across North America and Europe, a 67% incidence of moderate-to-severe skilled labor shortages raises demand for closed-loop servo systems that reduce unplanned downtime by 15-25% and log every cap application to FDA 21 CFR Part 11 standards.

Key Report Takeaways

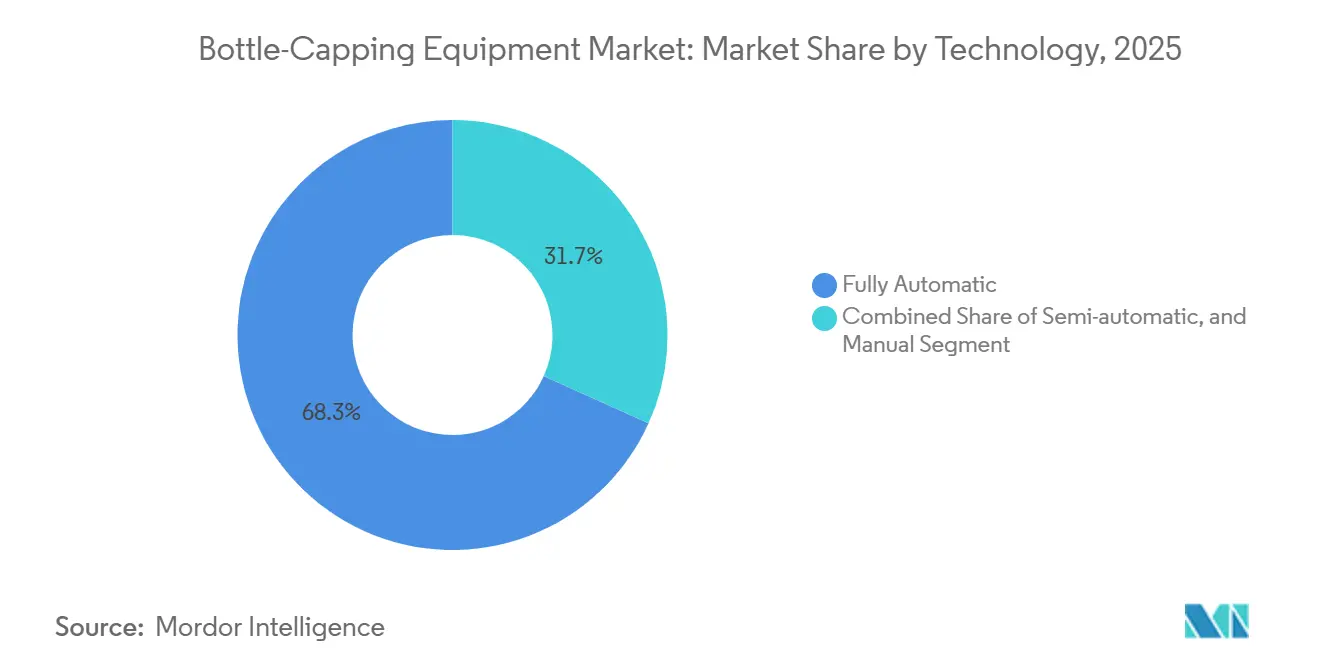

- By technology, fully automatic solutions captured 68.27% of the bottle-capping equipment market share in 2025.

- By cap type, the bottle-capping equipment market size for ROPP closures is projected to grow at a 6.48% CAGR from 2026 to 2031.

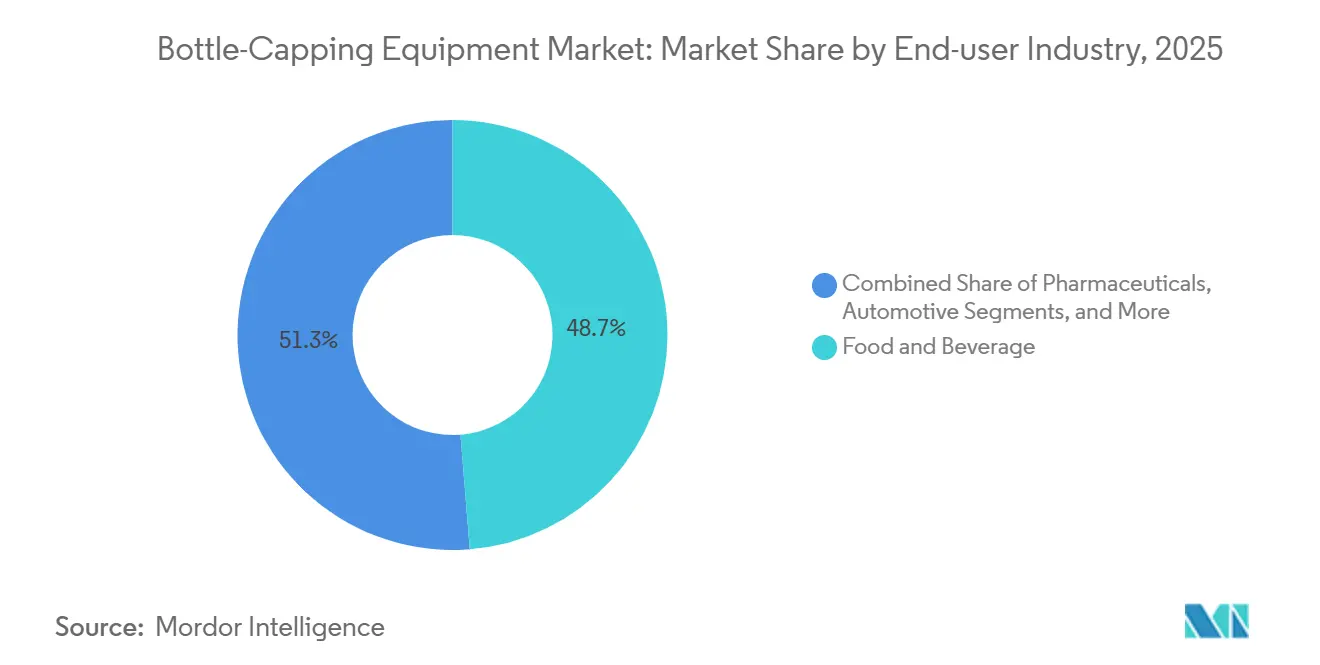

- By end-user industry, food and beverage captured 48.72% of the bottle-capping equipment market share in 2025.

- By geography, the bottle-capping equipment market size in the Asia-Pacific region is projected to grow at a 6.59% CAGR between 2026 and 2031.

Global Bottle-Capping Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in High-Speed Beverage Production Lines | +1.2% | Asia-Pacific core; spill-over to the Middle East and Africa | Medium term (2-4 years) |

| Shift Toward Pharma-Grade Torque-Controlled Cappers | +0.9% | North America and the EU, expanding to India | Long term (≥ 4 years) |

| Demand for Tamper-Evident and Tethered-Cap Compliance | +0.8% | Mandatory EU; voluntary North America and Asia-Pacific | Short term (≤ 2 years) |

| Sustainability Mandates for Lightweight and PCR-Ready Caps | +0.6% | Global, led by EU PPWR | Medium term (2-4 years) |

| Industry 4.0 Retrofits for Predictive Maintenance | +0.5% | North America and EU brownfield sites; greenfield Asia-Pacific | Long term (≥ 4 years) |

| Growth of Contract Packagers in Emerging Markets | +0.7% | Asia-Pacific, South America, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in High-Speed Beverage Production Lines

Per-capita soft-drink consumption continues to rise in India, Indonesia, and Vietnam, prompting beverage OEMs to commission lines capable of topping 80,000 bottles per hour by 2025. Krones’ ErgoBloc L consolidates rinsing, filling, and capping in one servo-synchronized block, increasing speed to 100,000 bottles per hour and reducing changeover time from four hours to 90 minutes. Sidel’s Super Combi, operating at 39,000 bph for aseptic PET, now supplies saline and oral rehydration solution contract manufacturers. Capital outlays of USD 2 million-5 million constrain purchases to multinationals and large domestic beverage groups, but smaller suppliers capture retrofit modules that bring brownfield sites to ISO 22000 cleaning-in-place standards. The bottle-capping equipment market thus benefits from a cascading upgrade cycle that pushes servo precision and vision inspection into mid-tier plants.

Shift Toward Pharma-Grade Torque-Controlled Cappers

Serialization under the Drug Supply Chain Security Act and EU Falsified Medicines Directive embeds torque parameters inside each unique identifier, compelling servo installations that hit ±0.1 newton-meter repeatability. Schreiner MediPharm’s Cap-Lock RFID seals log removal events, augmenting FDA 21 CFR Part 11 compliance. Contract development and manufacturing organizations prefer new modules priced at USD 300,000–500,000 over retrofits, and biosimilar liquid vials with quantities below 50,000 units justify the investment. As ISO 13485 validation extends from devices to drug packaging, demand for proven suppliers rises, layering regulatory risk onto buying decisions across Asia, the Middle East, and South America.

Demand for Tamper-Evident and Tethered-Cap Compliance

The EU Single-Use Plastics Directive requires tethered caps on bottles up to 3 liters from July 2024. Injection-molding hinges thinner than 0.4 mm introduce a shear-failure risk, so bottlers replace pneumatic heads with servo torque modules, which cost USD 30,000-80,000 per line. North American beverage groups are adopting tethered designs ahead of likely state mandates, creating a secondary demand spike. Spirits and wine fillers brace for the 2025/40 EU Packaging Regulation, which extends tamper-evidence requirements to glass containers, thereby widening the addressable market for capping equipment.

Sustainability Mandates for Lightweight and PCR-Ready Caps

France, Germany, and the Netherlands impose escalating fees on closures lacking 25% PCR content by 2025, climbing to 30% by 2031. SACMI’s neck-finish redesign saves 1.2 g of resin per 26/22 mm closure, equivalent to 1,200 fewer plastic units annually for a 1 billion-unit bottler.[1]SACMI Group, “AI Vision and Lightweight Caps,” sacmi.com Guala Closures thins aluminum ROPP caps from 0.24 mm to 0.16 mm, saving 33% metal per unit. PCR resin melt-flow variability triggers investments in closed-loop torque modules that adjust in real time, ensuring seal integrity without over-tightening and complying with ISO 14001 and the New Plastics Economy commitment.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX for Fully Automatic Systems | -0.8% | Global, acute South America and Africa | Short term (≤ 2 years) |

| Skilled-Labor Shortage for Advanced Servo Platforms | -0.6% | North America and the EU; emerging Asia-Pacific | Medium term (2-4 years) |

| Raw-Material and Electronic-Component Price Volatility | -0.5% | Global supply-chain dependencies in Asia | Short term (≤ 2 years) |

| Competition from Alternative Pack Formats | -0.4% | North America and EU consumer segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for Fully Automatic Systems

Price tags of USD 150,000-500,000 deter SMEs, particularly in Latin America and Africa, where financing terms remain restrictive. Semi-automatic lines costing a fraction deliver 15-30 minute changeovers and meet payback expectations within three years for sub-USD 5 million-unit annual volumes. Predictive-maintenance upgrades add another 20-30% to capital budgets, slowing adoption when discount rates outpace efficiency gains.

Skilled-Labor Shortage for Advanced Servo Platforms

A projected 3.8 million open U.S. manufacturing roles by 2033 worsens already tight talent pools for PLC and motion-control specialists. Servo-driven cappers require IEC 61131-3 programmers capable of tuning high-speed profiles; however, community college curricula lag behind demand by 30-40%. Lead times for motors and PLCs extend to 16 weeks, and new 15% component tariffs starting in 2026 risk capital budget overruns.

Segment Analysis

By Technology: Servo Precision Drives Automation Premium

Fully automatic platforms captured 68.27% of 2025 revenue as beverage fillers pursued speeds exceeding 60,000 bottles per hour and pharmaceutical lines sought torque-verification traceability. These systems command capital budgets of USD 2 million to USD 5 million, yet cut the changeover time from four hours to 90 minutes. Semi-automatic units, costing USD 20,000-80,000, anchor short-run contract packaging where setup agility takes precedence over throughput; 40% of contract-packing clients request such lines to serve portfolios exceeding 20 SKUs. Manual benchtop cappers are still used in pilot and craft operations that produce fewer than 50,000 bottles per year.

Vision-inspection add-ons, such as HEUFT’s FinalView II CAP, can scan 100,000 containers per hour, rejecting cross-threaded closures in real-time. Predictive-maintenance gateways reduce downtime by 15-25%, but increase installed costs beyond USD 600,000, a hurdle for mid-sized fillers. Skilled-labor deficits in North America and Europe are steering buyers toward turnkey packages that include remote diagnostics and OEM service contracts, which embed recurring fees but safeguard uptime.

Note: Segment shares of all individual segments available upon report purchase

By Cap Type: ROPP Aluminum Gains on Tamper-Evident Premiumization

Screw caps accounted for 54.39% of the 2025 output, serving mainstream beverages and household chemicals with cost-efficient designs made from PP or HDPE. ROPP closures, however, post a 6.48% CAGR through 2031 as premium spirits and wine migrate to pilfer-proof aluminum that signals authenticity and meets Extended Producer Responsibility rules. AROL’s long-ROPP heads reach 72,000 bph, matching screw-cap speeds while adding consumer-visible integrity bands.

SACMI’s metal-closure lines thin aluminum shells by 33%, aligning ROPP costs with lightweight plastic alternatives. Snap-on formats thrive in cosmetics; Virospack’s magnetic droppers utilize mono-material PP to enhance recyclability, as detailed on Virospack's website EU. Child-resistant designs serve the chemical segment, and cork maintains a niche among legacy wineries; however, growing tethered and tamper-evident mandates are tilting the volume toward servo-tightened screw and ROPP solutions.

By End-user Industry: Pharmaceutical Serialization Outpaces Food and Beverage

Food and beverage drove 48.72% of 2025 demand, yet pharmaceutical buyers deliver a 6.27% CAGR on torque-verified lines that record every closure event. Schreiner MediPharm’s RFID labels add electronic audit layers to biosimilar and cell-therapy vials. Personal-care firms pivot to airless mono-material pumps from Lumson, spurring cappers that handle snap-on and specialty neck finishes.

Automotive and chemical fillers require explosion-proof or child-resistant features, pushing niche suppliers to certify to UN transport rules. Contract packagers fill capability gaps, absorbing outsourced runs and demanding modular heads that change format in under 30 minutes. The bottle-capping equipment market size for contract packagers is projected to widen as multi-SKU portfolios proliferate.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The Asia-Pacific region generated 39.51% of 2025 revenue and is advancing at a rate of 6.59%, driven by urbanization, rising disposable incomes, and policy incentives that support local equipment production. Krones’ INR 3.15 billion Karnataka plant, breaking ground in February 2025, will assemble high-speed lines and create 550 jobs, shortening lead times for Indian fillers. SACMI, with more than 950 cap lines installed in China, unveiled AI vision that trims 30% resin from 26/22 mm neck finishes at CBST 2025. SMI’s expanded Mumbai hub stocks spares and technicians, accelerating service dispatch across South Asia. Regional contract packagers handle 63% of outsourced bottle volumes, necessitating agile cappers that can rapidly swap formats.[2]SMI Group, “Expansion in India,” smigroup.it

North America and Europe face a 67% moderate-to-severe labor shortage, diverting investments into predictive-maintenance retrofits that boost uptime but inflate budgets by 20-30%. The EU’s tethered-cap rule, effective July 2024, precipitated a retrofit sprint, while the 2025/40 Packaging Regulation broadens tamper-evident mandates to wine and spirits. Extended Producer Responsibility fees tied to PCR content lift demand for lightweight, mono-material screw caps that run on servo heads adaptable to variable resin melt flows. North American bottlers adopt tethered closures ahead of pending state laws, generating incremental orders for modular torque upgrades.

South America, the Middle East, and Africa remain early-stage, opportunity-rich territories. Latin American SMEs opt for semi-automatic lines priced USD 20,000-80,000 to serve product portfolios spanning 20-plus SKUs and batch sizes below 50,000 units. Middle Eastern beverage producers expand capacity in Saudi Arabia and the UAE, while African adoption lags due to cold-chain gaps and capital-financing hurdles. National authorities broadly align with Codex Alimentarius, yet enforcement inconsistency tempers immediate demand for advanced torque verification, keeping baseline manual and semi-automatic systems relevant.

Competitive Landscape

Top Companies in Bottle Capping Equipment Market

The bottle-capping equipment market remains moderately fragmented, with no single player exceeding 12%, and the top five players collectively holding a share of under 40%. Krones, Sidel, ProMach, Coesia, and Crown Holdings exploit installed bases to cross-sell digital-twin analytics, embedding multi-year service contracts that heighten switching barriers. Coesia’s June 2024 acquisition of Emmeci expanded its reach in cosmetics and pharma, while ProMach acquired Hamer-Fischbein and Paxiom in 2024 to unify its bagging, palletizing, and capping portfolios.[3]ProMach, “Paxiom and Hamer-Fischbein Deals,” promachinc.com

White space endures in semi-automatic platforms serving sub-10,000-unit runs, where payback expectations cap budgets under USD 80,000. HEUFT’s high-speed vision inspection elevates its profile as a niche disruptor, and SACMI’s upstream dominance in closures eases its forward integration into capping machinery. Strategic moves include Krones’ ErgoBloc L integrations, which compress the line footprint; Sidel’s aseptic PET expansions in Latin America; and SACMI’s AI vision release, which tailors torque to lightweight caps.

Raw-material cost swings and PLC lead-time spikes favor vertically integrated groups that can hedge purchases and stock semiconductors, marginalizing smaller builders during procurement shocks. Compliance costs tied to ISO 22000 and FDA 21 CFR Part 11 validation further protect incumbents, yet agile entrants offering USD 30,000-80,000 retrofit kits carve space below the premium tier.

Bottle-Capping Equipment Industry Leaders

Accutek Packaging Equipment Companies Inc.

Barry-Wehmiller Group, Inc.

AMET Packaging, Inc.

BellatRx Inc.

Coesia S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SACMI showcased AI-driven vision and 30% lightweight cap technology at CBST Shanghai, reaching 950 installed cap lines in China.

- March 2025: Virospack unveiled mono-material magnetic droppers for luxury cosmetics aiming at circular-economy goals.

- February 2025: Krones commenced construction of an INR 3.15 billion (USD 37.8 million) bottling-equipment plant in Karnataka, India, targeting 550 jobs and regional high-speed line assembly.

- February 2025: Antares Vision installed 300 bpm serialization units with torque verification for a North American CDMO.

Global Bottle-Capping Equipment Market Report Scope

Bottle-capping equipment is designed to insert caps onto bottles efficiently. The equipment retrieves caps from a storage tank or container and applies them to bottles. This study examines the revenues generated from the sales of various bottle-capping machines offered by different vendors in the market. Furthermore, the analysis assesses the impact of geopolitical developments on the bottle-capping equipment market, considering prevailing scenarios, key themes, and demand cycles associated with end-user verticals.

The Bottle-Capping Equipment Market Report is Segmented by Technology (Fully Automatic, Semi-automatic, and Manual), Cap Type (ROPP Caps, Screw Caps, Snap-on Caps, Corks, and Other Cap Types), End-user Industry (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, Chemicals, Automotive, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Fully Automatic |

| Semi-automatic |

| Manual |

| ROPP Caps |

| Screw Caps |

| Snap-on Caps |

| Corks |

| Other Cap Types |

| Food and Beverage |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Chemicals |

| Automotive |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Technology | Fully Automatic | ||

| Semi-automatic | |||

| Manual | |||

| By Cap Type | ROPP Caps | ||

| Screw Caps | |||

| Snap-on Caps | |||

| Corks | |||

| Other Cap Types | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Chemicals | |||

| Automotive | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the bottle-capping equipment market in 2026?

The bottle-capping equipment market size is expected to reach USD 3.94 billion by 2026.

Which technology segment is experiencing the fastest growth within bottle-capping solutions?

Fully automatic, servo-driven platforms post a 5.72% CAGR through 2031, outpacing semi-automatic and manual liness.

Why are ROPP closures gaining ground over screw caps?

Premium spirits and wine brands adopt aluminum ROPP caps for tamper evidence, driving a 6.48% CAGR for this closure type.

Which region leads future demand?

Asia-Pacific accounts for 39.51% of 2025 revenue and expands at 6.59% on new beverage plants and contract-packaging uptake.

How are sustainability rules influencing cap designs?

EU mandates on tethered caps and PCR content push lightweight, mono-material closures and torque-adaptive capping heads.

What impact do labor shortages have on equipment choices?

A 67% skilled-labor deficit in North America and Europe accelerates the adoption of predictive-maintenance and remote-diagnostics-ready systems.