Market Size of BOPP Films Industry

| Study Period | 2019 - 2029 |

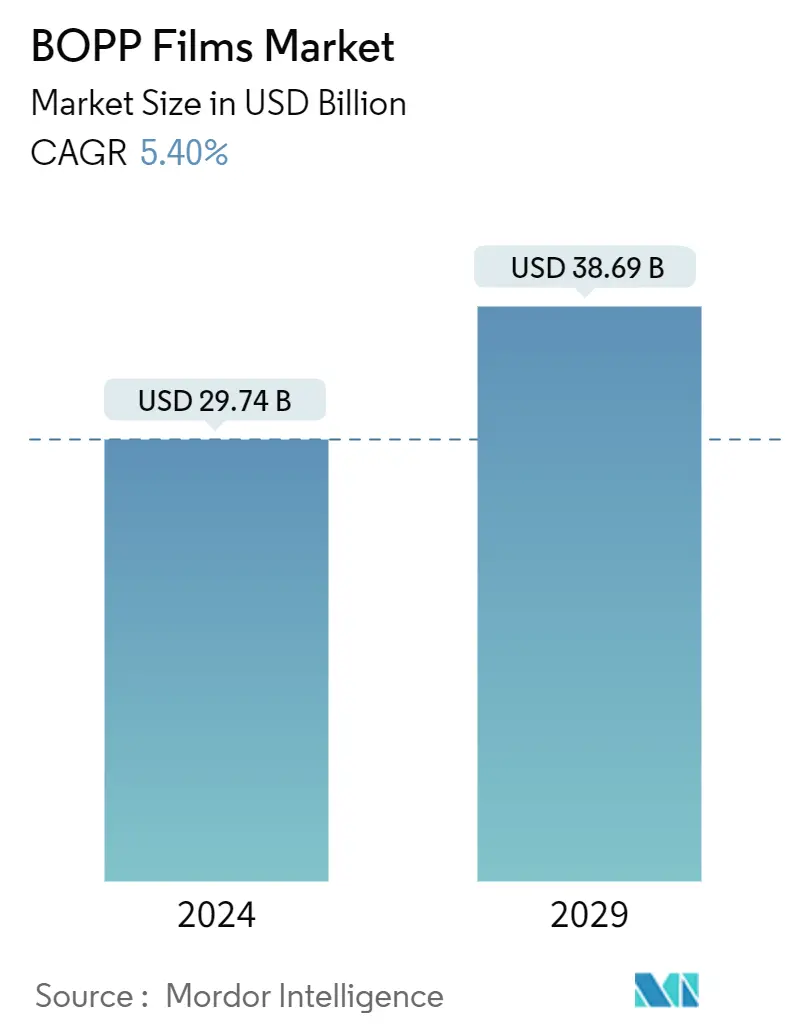

| Market Size (2024) | USD 29.74 Billion |

| Market Size (2029) | USD 38.69 Billion |

| CAGR (2024 - 2029) | 5.40 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

BOPP Films Market Analysis

The BOPP Films Market size is estimated at USD 29.74 billion in 2024, and is expected to reach USD 38.69 billion by 2029, growing at a CAGR of 5.40% during the forecast period (2024-2029).

BOPP film is commonly used for applications that require moisture resistance, optical clarity, and increased tensile strength, such as medical packaging, food and beverage packaging, and personal care product packaging. Several factors contribute to the growth of BOPP (biaxially oriented polypropylene) films, including their versatility, durability, cost-effectiveness, and environmental benefits. The increasing need for flexible packaging solutions in diverse industries, such as food and beverage, pharmaceuticals, and cosmetics, further drives the market’s growth.

- BOPP has become a high-growth film material due to its extreme versatility. BOPP is an essential polypropylene film. It is an effective alternative to waxed paper and aluminum foil. One of the primary factors that has led to BOPP film use and application growth is their relatively low carbon footprint compared to other plastic films. Because of their low melting point, BOPP films require less energy to convert from one form to another.

- At-home food consumption and snacking may remain higher than in the pre-COVID period as more people permanently join the home-office trend. Owing to this, food packaging is expected to continue to be the critical end-use sector for BOPP films. The demand for fine commodity film, usually used in food, pharmaceutical, and other market, is expected to drive future demand. In recent years, the electrical and electronics market has also increased the use of BOPP films in packaging, which are also available in glossy and matte formats.

- In September 2023, Tredegar Corporation sold its flexible packaging films “Terphane” business to Oben Group with a net transaction of USD 116 million. The manufacturing sites are in Cabo de Santo Agostinho, headquartered in São Paulo, Brazil, and exports to 29 countries. With the completion of this transaction, Oben strengthened its place as a global player in the highly competitive flexible films market by increasing the production capacity of BOPET films and offering an opportunity to enlarge the production capacity for other films, especially BOPP, in the United States and Brazil.

- The bags and pouches made of BOPP films are becoming increasingly popular since they are environmentally friendly, reasonably priced, and 100% recyclable. The visual appeal of BOPP bags and pouches adds an extra layer of advertising to the goods used for packaging. The expansion of food and beverage, e-commerce, the improving economy, and increased disposable income contributed to increased consumption of packaged goods (including packaged food), which need packaging to protect the commodities from contamination and damage. This tendency will likely increase the vendor's manufacturing capacity and boost the growth of the market studied over the years.

- In April 2024, Toppan and India-based Toppan Speciality Films (TSF) developed GL-SP, a barrier film that uses biaxially oriented polypropylene (BOPP) as the substrate. GL-SP is a recent addition to the range of products for sustainable packaging in the Toppan Group’s GL BARRIER1 series of transparent vapor-deposited barrier films, which enjoy a significant share of the global market, according to the company. Toppan and TSF will launch sales of GL-SP for packaging dry content, focusing on markets in the Americas, Europe, India, and the ASEAN region.

- The BOPP films market faces several significant challenges that could impact its growth and profitability in the future. These challenges include the availability of substitute packaging materials and the adoption of alternative packaging materials, such as bio-based plastics, compostable materials, and other flexible films, which threaten BOPP films. They could compete for market share if these alternatives offer comparable or superior properties while being more environmentally friendly. In addition, changing consumer preferences and behaviors can influence packaging trends. If consumers demand alternative packaging formats or materials due to health concerns, convenience, or sustainability, the market for BOPP films might be affected.

- The COVID-19 pandemic has significantly impacted the biaxially oriented polypropylene film market. The pandemic caused supply chain disruptions in the market studied due to international trade restrictions, lockdown measures, and transportation challenges. Production facility closures and logistical restrictions caused delays in raw material procurement and finished product delivery, impacting the overall production and distribution of BOPP films. The rapid growth of the country's economy and increasing disposable income lead to a rise in consumer spending. This has propelled the demand for packaged goods, especially in urban areas, where convenience and aesthetics play essential roles. BOPP films offer better printability and visual appeal, making packaging ideal.

- Over the last five years, India's capacity has around doubled, owing to the opening up of its retail sector, an increase in the middle classes, and accompanying consumer spending on packaged food and other commodities. Recent BOPP investments have been substantially high, with a yearly nameplate capacity of more than 45,000 tons. Furthermore, according to the US Department of Agriculture, in 2023, over 549 million metric tons of cow's milk was produced worldwide among various dairy products. In comparison, the production volume of cheese and butter was over 22 and 11 million metric tons in the same year. Such developments in the food sector may create more opportunities in the market studied.

BOPP Films Industry Segmentation

BOPP stands for biaxially oriented polypropylene. BOPP films are thin, flexible plastic made from polypropylene using a biaxial orientation process, which involves stretching the film in both the machine and transverse directions. This process enhances the film's mechanical properties, making it strong, transparent, and resistant to moisture, chemicals, and punctures. The BOPP films market is segmented by end-user vertical (food, beverage, pharmaceutical and medical, industrial, and other end-user verticals) and geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, Italy, Spain, and Rest of Europe], Asia-Pacific [China, Japan, India, Australia, and Rest of Asia-Pacific], Latin America [Brazil, Argentina, Mexico, Rest of Latin America], The Middle East, and Africa [Saudi Arabia, South Africa, Egypt, and Rest of Middle East and Africa]). Furthermore, the disturbance of the factors affecting the market's evolution in the near future, such as drivers and constraints, has been covered in the study. The market sizes and predictions are provided in terms of value in USD for all the above segments.

| By End-user Vertical | |

| Food | |

| Beverage | |

| Pharmaceutical and Medical | |

| Industrial | |

| Other End-user Verticals |

| By Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

BOPP Films Market Size Summary

The BOPP films market is poised for significant growth, driven by the material's versatility and cost-effectiveness. BOPP films are increasingly utilized in packaging applications across various sectors, including food and beverage, pharmaceuticals, and personal care, due to their moisture resistance, optical clarity, and tensile strength. The demand for flexible packaging solutions is further bolstered by the rising trend of at-home food consumption and snacking, a behavior shift that has persisted post-COVID-19. The market is also witnessing innovations, such as the development of barrier films like Toppan's GL-SP, which enhance packaging sustainability. The acquisition of Tredegar Corporation's Terphane business by Oben Group underscores the competitive landscape, as companies strive to expand production capacities and strengthen their global presence.

In addition to the growing demand in traditional sectors, the BOPP films market is experiencing increased adoption in the electrical and electronics industries, where these films are used in packaging and capacitor applications. The market's expansion is supported by the rising consumption of packaged goods, driven by economic growth and increased disposable income, particularly in regions like India and North America. However, the market faces challenges from the availability of alternative packaging materials, such as bio-based and compostable options, which could impact BOPP films' market share. Despite these challenges, the focus on sustainable and recyclable packaging solutions continues to shape the market dynamics, with companies like Cosmo Films and Innovia Films leading innovations in specialty films.

BOPP Films Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Consumers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Impact of Key Macroeconomic Trends on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By End-user Vertical

-

2.1.1 Food

-

2.1.2 Beverage

-

2.1.3 Pharmaceutical and Medical

-

2.1.4 Industrial

-

2.1.5 Other End-user Verticals

-

-

2.2 By Geography

-

2.2.1 North America

-

2.2.1.1 United States

-

2.2.1.2 Canada

-

-

2.2.2 Europe

-

2.2.2.1 United Kingdom

-

2.2.2.2 Germany

-

2.2.2.3 France

-

2.2.2.4 Italy

-

2.2.2.5 Spain

-

2.2.2.6 Rest of Europe

-

-

2.2.3 Asia-Pacific

-

2.2.3.1 China

-

2.2.3.2 Japan

-

2.2.3.3 India

-

2.2.3.4 Australia

-

2.2.3.5 Rest of Asia-Pacific

-

-

2.2.4 Latin America

-

2.2.4.1 Brazil

-

2.2.4.2 Argentina

-

2.2.4.3 Mexico

-

2.2.4.4 Rest of Latin America

-

-

2.2.5 Middle East and Africa

-

2.2.5.1 Saudi Arabia

-

2.2.5.2 South Africa

-

2.2.5.3 Egypt

-

2.2.5.4 Rest of Middle East and Africa

-

-

-

BOPP Films Market Size FAQs

How big is the BOPP Films Market?

The BOPP Films Market size is expected to reach USD 29.74 billion in 2024 and grow at a CAGR of 5.40% to reach USD 38.69 billion by 2029.

What is the current BOPP Films Market size?

In 2024, the BOPP Films Market size is expected to reach USD 29.74 billion.