Market Trends of Boat And Ship MRO Industry

This section covers the major market trends shaping the Boat & Ship MRO Market according to our research experts:

Growing Maritime Fleet Worldwide Is Driving the Market Growth

Maritime transport is the backbone of global trade and the global economy as the world's population continues to grow, particularly in developing countries where low-cost and efficient maritime transport has an essential role in growth and sustainable development.

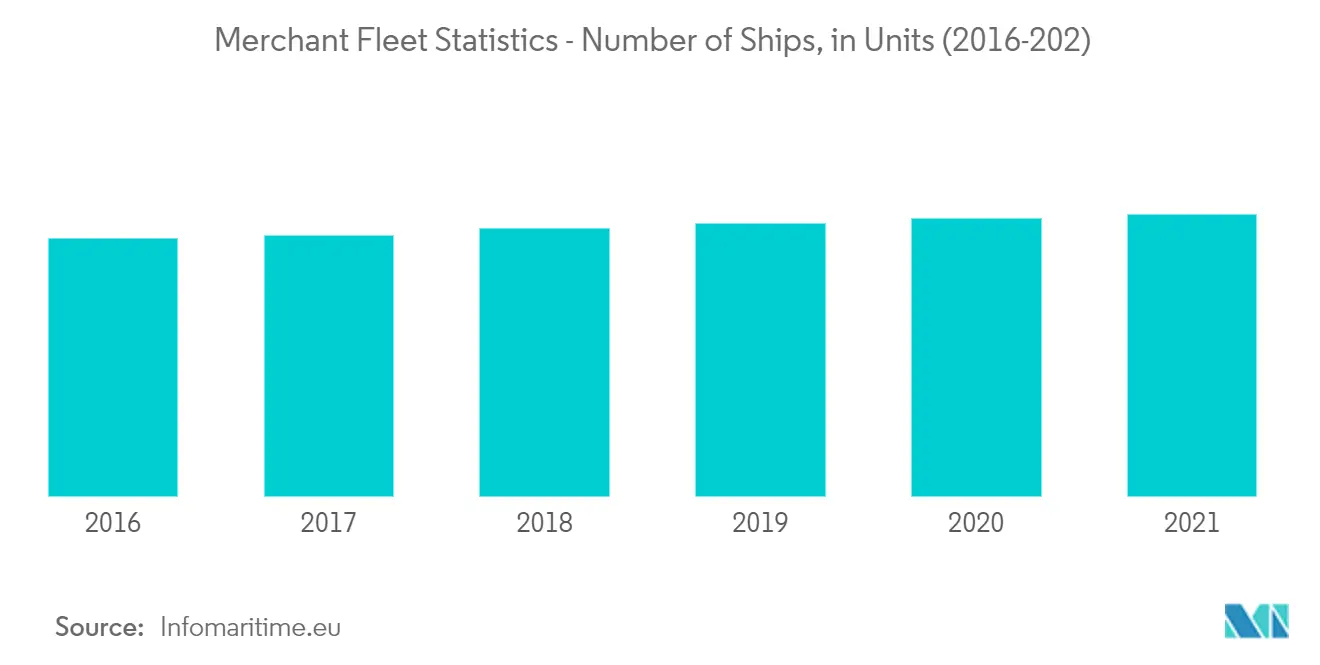

The maritime industry has been growing rapidly over the recent years with the addition of ships to the national fleet and investments being made by both private and government players worldwide.

The world fleet had a carrying capacity of 2.1 billion dwt in January 2021, up by 63 million dwt from the previous year. With the exception of general freight carriers, tonnage has climbed significantly in recent years. Bulk haulers saw a speedy growth. Between 2011 and 2021, their proportion of the overall carrying capacity increased from 39% to 43%, while oil tankers' share decreased from 31% to 29%, and general cargo's share increased from 6% to 4%. Moreover, of the around 56,000 merchant ships trading internationally, around 17,000 ships were general cargo ships, accounting for roughly 30% of the world's merchant fleet.

The average age of fleet and vessel sizes have been increasing over the years to optimize costs through economies of scale. These long-run ships need regular and continuous maintenance checkups, which is expected to result in the boat and ship MRO market witnessing growth during the forecast period.

The top five ship-owning economies accounted for 52% of the global fleet tonnage in January 2021. Greece had the largest market share (18%), followed by China (12%), Japan (11%), Singapore (7%), and Hong Kong SAR (7%). Asian firms possessed half of the world's tonnage. Owners from Europe made up 40% of the total, while those from northern America made up 6%. Companies from Africa, Latin America, and the Caribbean represented a little over 1% of the market, while Oceania had just under 1%.

In terms of dead-weight tonnage, bulk carriers are the youngest vessels, with an average age of 9.28 years, followed by container ships (9.91 years) and oil tankers (10.38 years). On average, general cargo ships are the oldest vessel type (19.46 years).

Apart from these factors, government organizations are entering into joint ventures with other private players globally to enhance their fleet capacity.

In September 2021, Larsen and Toubro (L&T) won a prestigious contract from the British Royal Navy for developing designs for Fleet Solid Support ships. L&T was awarded the contract to build three new Fleet Solid Support (FSS) ships for the British Royal Fleet Auxiliary, the logistics arm of the British Royal Navy.

In July 2021, Cosco Shipping Holdings placed a USD 1.5 billion order for 10 new container ships, extending the carrier's on-order capacity to almost 15% of its in-service fleet. The parent of Cosco Shipping and OOCL announced a USD 876 million order for six 14,092 TEU ships to be delivered between December 2023 and September 2024, and a USD 620 million order for four vessels of 16,180 TEU that will be built by a wholly-owned subsidiary of Cosco and delivered between June and December 2025.

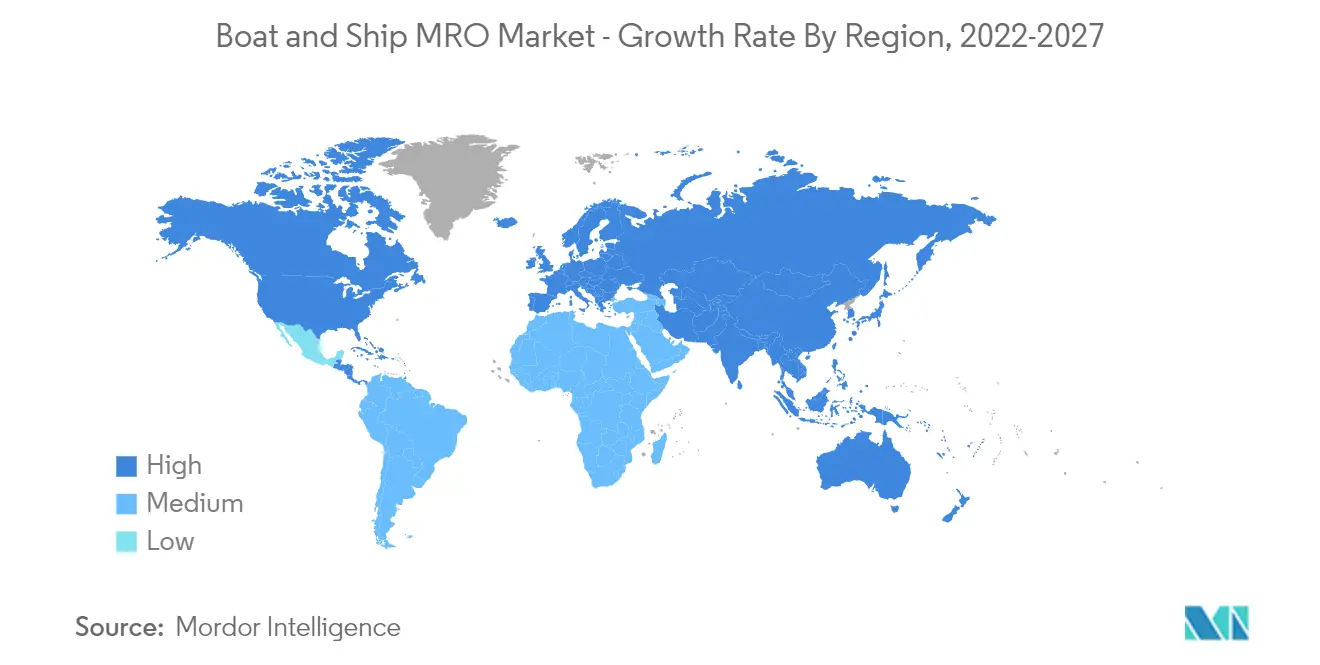

Asia-Pacific to Exhibit the Highest Growth Rate during the Forecast Period

The Asia-Pacific region is home to strong developing economies such as India and China, which are now investing more to boost their international exports. The fishing industry has also boomed in the region due to the large-scale adoption of powerful motorized boats. The countries in the Asia-Pacific region are also investing heavily to modernize their existing naval fleets to counter piracy and sea border violation activities.

A large portion of the fleet present in this region consists of old ships that need timely repairs and maintenance. Indian Navy has witnessed incidents of the untimely breakdown of their vessels over the past few years.

China ranked 2nd globally in terms of spending on the military in 2020. However, the country reduced its defense spending during 2020 by around -1.7% of its GDP. In 2021, the government hiked its defense budget by 6.8% from the previous year. The defense budget crossed the USD 200 billion mark for the first time. There are around 500 different types of vessels and 230 auxiliary ships fleet with the People's Liberation Army of the country. The commercial fleet of the country includes 6,459 units of different marine vessels. The ship maintenance and repairing industry is one of the leading industries in the region. The shipyards in the country handle huge traffic of container carriers and other ships from different parts of the world.

The Indian government is taking necessary steps to boost the ship MRO market by making necessary amendments to the tax slab for the industry. For instance,

In June 2021, the Ministry of Defence announced that it was planning to acquire 24 new submarines, including six nuclear attack submarines, to bolster its underwater fighting capability.

In May 2021, the government announced that it was planning to reduce GST on maintenance, repair, and overhaul (MRO) services in the shipping sector from the current 18% to 5% in order to align the tax rates with competing nations like Singapore, the United Arab Emirates (UAE), and Sri Lanka in the sector.

The presence of a large number of IT and technology firms in the region is fueling the growth of technologies, such as Virtual Reality, Augmented Reality, Mixed Reality, and Extended Reality. These technologies are expected to significantly drive the Boat and Ship MRO market in the region.

With increased spending in the defense sector from the Government of India in procuring the latest technology marine vessels and reforms to boost the ship MRO industry, the demand is expected to grow during the forecast period.