Market Size of Blood Screening Industry

| Study Period | 2019 - 2029 |

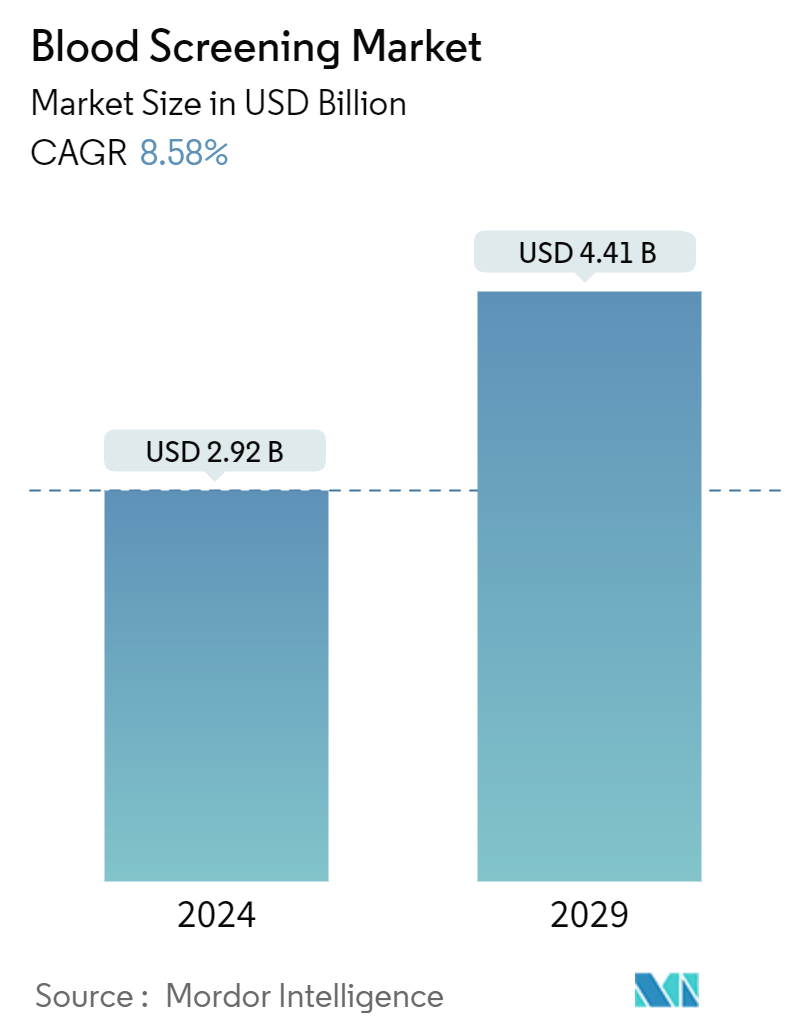

| Market Size (2024) | USD 2.92 Billion |

| Market Size (2029) | USD 4.41 Billion |

| CAGR (2024 - 2029) | 8.58 % |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Blood Screening Market Analysis

The Blood Screening Market size is estimated at USD 2.92 billion in 2024, and is expected to reach USD 4.41 billion by 2029, growing at a CAGR of 8.58% during the forecast period (2024-2029).

- The blood screening market is a pivotal segment within the broader healthcare diagnostics industry, playing a crucial role in ensuring the safety of blood transfusions by detecting infections and other abnormalities. The increasing global demand for safe blood, combined with technological advancements in screening methods, is shaping the future of this market. This analysis delves into the trends, challenges, and future outlook of the blood screening market, highlighting the significance of this industry in the global healthcare landscape.

Technological Advancements and Market Growth

- Nucleic Acid Amplification Tests (NAT): Blood screening involves various techniques, including Nucleic Acid Amplification Tests (NAT), ELISA, and Next-Generation Sequencing (NGS), to detect pathogens like HIV, hepatitis, and other infectious agents. The adoption of advanced blood screening technologies has significantly enhanced the accuracy and speed of blood testing, reducing the risks associated with transfusions. As the global healthcare landscape increasingly focuses on precision medicine and patient safety, these technologies are becoming more integral to the blood screening industry.

- ELISA and NGS Technologies: The evolution of Enzyme-Linked Immunosorbent Assay (ELISA) and Next-Generation Sequencing (NGS) technologies has revolutionized blood screening, allowing for the detection of a broader range of pathogens with greater sensitivity. These advancements have driven the demand for more sophisticated blood screening assays, contributing to the market's expansion. The continued innovation in these technologies is expected to further enhance the capabilities of blood screening diagnostics, supporting industry growth.

- Automation in Blood Screening: Automation has become a key trend in the blood screening market, improving efficiency and reducing human error in laboratories. The integration of automated systems in blood screening processes has not only increased throughput but also enhanced the accuracy of results. This trend is particularly relevant in regions with advanced healthcare infrastructure, where the demand for reliable and high-throughput screening solutions is high. Automation is likely to remain a significant driver of market growth, as laboratories continue to seek ways to improve their operational efficiency.

Strengthening Blood Safety Amid Rising Donations

- Increasing Number of Blood Donations and Transfusion-Related Screenings: The global increase in blood donations is a key factor driving the blood screening market. With more people donating blood, there is a growing need for robust screening processes to ensure the safety of the blood supply. Blood banks and healthcare facilities are implementing advanced screening techniques to handle the higher volume of donations. This trend is particularly evident in regions with strong government support for blood donation programs, where increased public awareness and improved infrastructure have contributed to higher donation rates. As the volume of donations rises, so does the demand for cutting-edge blood screening assays, which are critical in identifying infectious agents and ensuring that transfused blood is safe for recipients.

- Growing Prevalence of Infectious Diseases: The spread of infectious diseases continues to be a significant concern for public health, particularly in regions with limited access to advanced healthcare. The growing incidence of diseases such as HIV, hepatitis B and C, and Zika virus has underscored the need for more stringent blood screening protocols. Governments and healthcare organizations are prioritizing the implementation of comprehensive screening technologies to mitigate the risk of transmitting these infections through blood transfusions. This has led to increased adoption of nucleic acid amplification tests (NAT), chemiluminescence immunoassays (CLIA), and other high-sensitivity techniques in blood screening laboratories. The focus on preventing the spread of infectious diseases through transfusions is driving continuous innovation in blood screening technologies, ensuring that the market remains dynamic and responsive to emerging health challenges.

Challenges in the Evolving Diagnostic Landscape

- Development of Alternative Technologies: The emergence of alternative diagnostic technologies poses a challenge to the traditional blood screening market. Innovations such as point-of-care testing and advanced molecular diagnostics are increasingly being explored as substitutes for conventional blood screening methods. These technologies offer the potential for quicker, more accessible diagnostic solutions, potentially reducing the reliance on centralized blood screening systems. As a result, traditional blood screening companies may face competition from new entrants offering alternative solutions that promise greater convenience and cost-effectiveness. To remain competitive, established blood screening companies must continue to innovate and integrate new technologies into their offerings.

- Lack of Legislation, Regulations, and Policies: In many regions, the absence of comprehensive legislation and regulatory frameworks governing blood screening practices remains a significant barrier to market growth. The lack of standardized policies can lead to inconsistencies in screening procedures, compromising the safety of blood transfusions. This issue is particularly pronounced in low- and middle-income countries, where healthcare infrastructure may be underdeveloped, and regulatory oversight is limited. The absence of clear guidelines can result in gaps in blood safety, putting patients at risk. To address this challenge, international health organizations and local governments must collaborate to establish and enforce robust regulatory frameworks that ensure the consistent and safe application of blood screening technologies.

Blood Screening Industry Segmentation

As per the scope of the report, a blood screening is a laboratory test done on a blood sample taken from a vein in the arm using a hypodermic needle or a fingerprick. Blood screening aims to detect infection markers so that infected blood and blood components are not released for clinical use.

The blood screening market is segmented by product, technology, end user, and geography. By product, the market is segmented into reagents and instruments. By technology, the market is segmented into nucleic acid amplification test (NAT), enzyme-linked immunosorbent assay (ELISA), chemiluminescence immunoassay (CLIA), and enzyme immunoassay (EIA), next-generation sequencing (NGS), and western blotting. By end user, the market is segmented into blood banks, hospitals, and clinical laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| By Product | |

| Reagents | |

| Instruments |

| By Technology | |

| Nucleic Acid Amplification Test (NAT) | |

| Enzyme-linked Immunosorbent Assay (ELISA) | |

| Chemiluminescence Immunoassay (CLIA) and Enzyme Immunoassay (EIA) | |

| Next-Generation Sequencing (NGS) | |

| Western Blotting |

| By End-User | |

| Blood Banks | |

| Hospitals | |

| Clinical laboratories |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Blood Screening Market Size Summary

The blood screening market is poised for significant growth over the forecast period, driven by several key factors. The increasing incidence of infectious diseases and the rising number of blood donations are major contributors to this expansion. Government initiatives and awareness campaigns, such as those led by the World Health Organization, are further bolstering the demand for blood screening and safe transfusions. The market is also benefiting from advancements in diagnostic technologies, including machine-learning models for disease detection, which have gained prominence during the COVID-19 pandemic. Strategic collaborations among market players are expected to enhance the availability of advanced diagnostic tests, thereby supporting market growth. However, the development of alternative technologies and the need for more regulatory frameworks may pose challenges to the market's expansion.

The reagent segment of the blood screening market is anticipated to experience robust growth, fueled by the increasing demand for diagnostic testing due to the prevalence of infectious diseases. The North American market, in particular, is expected to thrive due to high healthcare spending and a well-established healthcare infrastructure. The United States, with its substantial blood transfusion requirements, is a key driver of market growth in the region. The competitive landscape of the blood screening market is characterized by the presence of major players who are actively engaging in strategic initiatives such as mergers, acquisitions, and new product launches to strengthen their market position. These dynamics, coupled with the ongoing influx of innovative products, are expected to propel the market forward over the forecast period.

Blood Screening Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Increasing Number of Blood Donations and Transfusion Related Screenings

-

1.2.2 Growing Prevalence of Infectious Diseases

-

1.2.3 Increasing Government Initiatives

-

-

1.3 Market Restraints

-

1.3.1 Development of Alternative Technologies

-

1.3.2 Lack of Legislation, Regulations, and Policies

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD)

-

2.1 By Product

-

2.1.1 Reagents

-

2.1.2 Instruments

-

-

2.2 By Technology

-

2.2.1 Nucleic Acid Amplification Test (NAT)

-

2.2.2 Enzyme-linked Immunosorbent Assay (ELISA)

-

2.2.3 Chemiluminescence Immunoassay (CLIA) and Enzyme Immunoassay (EIA)

-

2.2.4 Next-Generation Sequencing (NGS)

-

2.2.5 Western Blotting

-

-

2.3 By End-User

-

2.3.1 Blood Banks

-

2.3.2 Hospitals

-

2.3.3 Clinical laboratories

-

-

2.4 Geography

-

2.4.1 North America

-

2.4.1.1 United states

-

2.4.1.2 Canada

-

2.4.1.3 Mexico

-

-

2.4.2 Europe

-

2.4.2.1 Germany

-

2.4.2.2 United Kingdom

-

2.4.2.3 France

-

2.4.2.4 Italy

-

2.4.2.5 Spain

-

2.4.2.6 Rest of Europe

-

-

2.4.3 Asia-Pacific

-

2.4.3.1 China

-

2.4.3.2 Japan

-

2.4.3.3 India

-

2.4.3.4 Australia

-

2.4.3.5 South Korea

-

2.4.3.6 Rest of Asia-Pacific

-

-

2.4.4 Middle East and Africa

-

2.4.4.1 GCC

-

2.4.4.2 South Africa

-

2.4.4.3 Rest of Middle East and Africa

-

-

2.4.5 South America

-

2.4.5.1 Brazil

-

2.4.5.2 Argentina

-

2.4.5.3 Rest of South America

-

-

-

Blood Screening Market Size FAQs

How big is the Blood Screening Market?

The Blood Screening Market size is expected to reach USD 2.92 billion in 2024 and grow at a CAGR of 8.58% to reach USD 4.41 billion by 2029.

What is the current Blood Screening Market size?

In 2024, the Blood Screening Market size is expected to reach USD 2.92 billion.