| Study Period | 2019 - 2030 |

| Market Volume (2025) | 8.72 Million tons |

| Market Volume (2030) | 11.98 Million tons |

| CAGR | 6.56 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Market Major Players")

Market Size")

Bisphenol-A Market Analysis

The Bisphenol A Market size is estimated at 8.72 million tons in 2025, and is expected to reach 11.98 million tons by 2030, at a CAGR of 6.56% during the forecast period (2025-2030).

The Bisphenol A industry is experiencing significant transformation driven by technological advancements and sustainability initiatives. Major industry players are investing heavily in research and development to develop more environmentally friendly alternatives and improve existing products. For instance, in May 2021, SABIC developed a new 4,4'-Bisphenol-A dianhydride (BPADA) powder for polyimide film formulations, targeting applications in 5G flexible printed circuit boards and colorless displays. This technological evolution is reshaping the industry landscape while creating new opportunities for market expansion and product innovation.

The market is witnessing substantial consolidation through strategic mergers and acquisitions, reflecting the industry's maturation and companies' efforts to strengthen their market positions. A notable example is Chang Chun Group's acquisition of Taiwan Prosperity Chemical Corporation (TPCC) in March 2021 for USD 85 million, which added a Bisphenol A production capacity of 107-kilometric tons. Additionally, in October 2021, Mitsubishi Chemical Corporation partnered with Kebotix, a technology platform firm, to develop cleaner chemistry solutions and explore alternatives to traditional Bisphenol A, demonstrating the industry's commitment to sustainable innovation.

Infrastructure development and construction activities across various regions are creating new opportunities for BPA applications. The United Arab Emirates announced plans to invest AED 448 billion (USD 122 billion) in oil and gas infrastructure over the next five years, which is expected to drive demand for flame retardant materials and coatings. Similarly, the expansion of digital infrastructure, exemplified by Amazon Web Services' planned launch of a new infrastructure region in Spain, is creating additional demand channels for BPA-based products in construction and electrical applications.

The electronics and consumer goods sectors continue to be significant growth drivers for the BPA industry, with increasing demand for electronic components and devices. According to industry forecasts, the revenue in Indonesia's household appliances market is projected to reach USD 1,792 million by 2025, growing at a CAGR of 10.97% (2021-2025). This growth in consumer electronics and appliances manufacturing, particularly in emerging economies, is creating sustained demand for BPA-based materials while also driving innovation in product formulations and applications.

Bisphenol-A Market Trends

Strong Demand for Polycarbonate Plastics

The robust demand for polycarbonate plastics continues to drive the bisphenol A (BPA) market, with major manufacturers expanding their production capabilities through significant investments and technological advancements. In March 2024, Covestro AG inaugurated its first industrial-scale plant for polycarbonate copolymers production in Antwerp, Belgium, demonstrating the growing market demand. This expansion was followed by SABIC and Sinopec's strategic collaboration in September 2023, launching a new polycarbonate plant through their joint venture Sinopec SABIC Tianjin Petrochemical (SSTPC), with an annual designed capacity of 260 kilotons, strengthening their position in the Asian market.

The versatility of BPA-based polycarbonates has led to their increased adoption in various applications, particularly in the construction and automotive sectors. These materials are extensively used as glass substitutes in windows, skylights, and architectural applications due to their exceptional properties, including impact resistance, high glass transition temperature, and natural transparency. The growing application in greenhouse construction, especially in European countries such as Germany, France, the Netherlands, and Spain, has created additional demand streams. Furthermore, Covestro's expansion of polycarbonate films production capacity in Thailand in March 2023, exceeding 100,000 metric tons annually, highlights the material's growing importance in identity documents, automotive displays, and electronic applications.

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand for Epoxy Resins from Various End-user Industries

The escalating demand for epoxy resins across multiple industries continues to be a significant driver for the bisphenol A market, particularly in the electronics and construction sectors. The electronics industry's rapid advancement has created substantial demand for epoxy resins in the manufacturing of electrical and electronic components, owing to their superior electrical and mechanical properties. These resins are crucial in producing high-performance electrical and electronic components, offering advantages such as quick cycle times and enhanced protection against dust, moisture, and short circuits. Additionally, their higher thermal conductivity compared to air helps dissipate heat from components more efficiently, extending service life.

The construction industry's growth has further amplified the demand for epoxy resins, particularly in infrastructure development and building materials. Epoxy resins are extensively used in the production of adhesives, plastics, paints, coatings, primers and sealers, flooring, and other construction products. The material's versatility is demonstrated in its application in rotor blade composites for wind turbines, where epoxy resins have enabled blade diameters to increase significantly from 15 meters in the 1980s to 160 meters currently. The development of new technological products and continuous innovation in consumer electronics worldwide has created additional demand streams for epoxy resins, particularly in the manufacturing of electronic devices and appliances.

Segment Analysis: Application

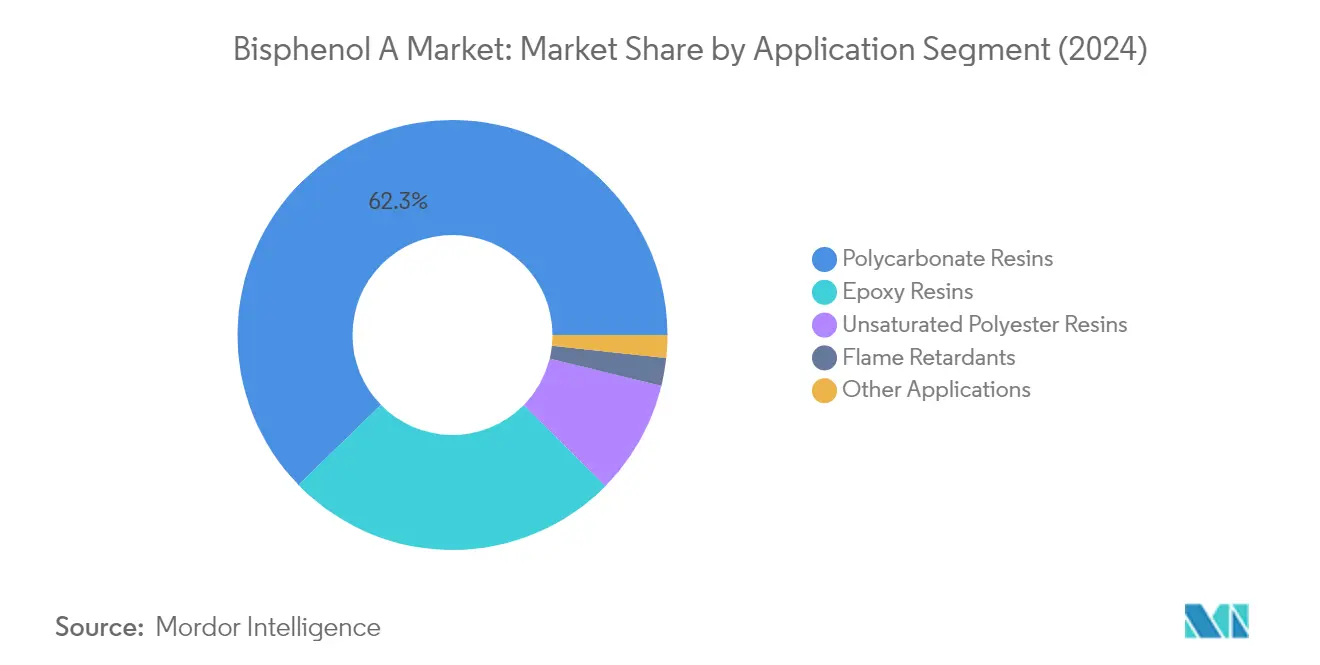

Polycarbonate Resins Segment in Bisphenol A (BPA) Market

The polycarbonate resins segment continues to dominate the global Bisphenol A market, accounting for approximately 62% of the total market volume in 2024. This significant Bisphenol A market share is primarily driven by the extensive use of polycarbonate resins in various end-use industries, including automotive, electronics, construction, and consumer goods. The segment's dominance is further strengthened by the material's unique properties, such as high impact strength, optical clarity, and heat resistance, making it ideal for applications in headlight lenses, bulletproof glasses, electronic device casings, and automotive components. The increasing demand for lightweight and durable materials in the automotive and electronics industries, coupled with growing infrastructure development activities worldwide, continues to fuel the segment's growth.

Flame Retardants Segment in Bisphenol A (BPA) Market

The flame retardants segment is emerging as the fastest-growing application in the BPA market, with a projected growth rate of approximately 6% during the forecast period 2024-2029. This robust growth is primarily attributed to stringent fire safety regulations across industries and increasing awareness about fire protection in buildings and electronic devices. The segment's growth is particularly driven by the rising demand from the construction and electronics sectors, where fire safety requirements are becoming increasingly stringent. The expansion of the automotive and aerospace industries, coupled with the growing emphasis on passenger safety, is further accelerating the adoption of BPA-based flame retardants in these sectors.

Remaining Segments in BPA Market Applications

The remaining segments in the Bisphenol A market include epoxy resins, unsaturated polyester resins, and other applications, each serving distinct industrial needs. Epoxy resins represent a significant portion of BPA consumption, primarily used in coatings, adhesives, and electronic components, benefiting from the growing electronics and construction industries. Unsaturated polyester resins find extensive applications in the marine industry, construction sector, and automotive applications, particularly in composite materials. Other applications include the use of BPA in specialized products such as thermal paper and various industrial materials, though these applications are seeing moderate growth due to increasing regulatory scrutiny and the emergence of alternatives. This comprehensive Bisphenol A market analysis highlights the diverse applications and growth potential within the industry.

Bisphenol A (BPA) Market Geography Segment Analysis

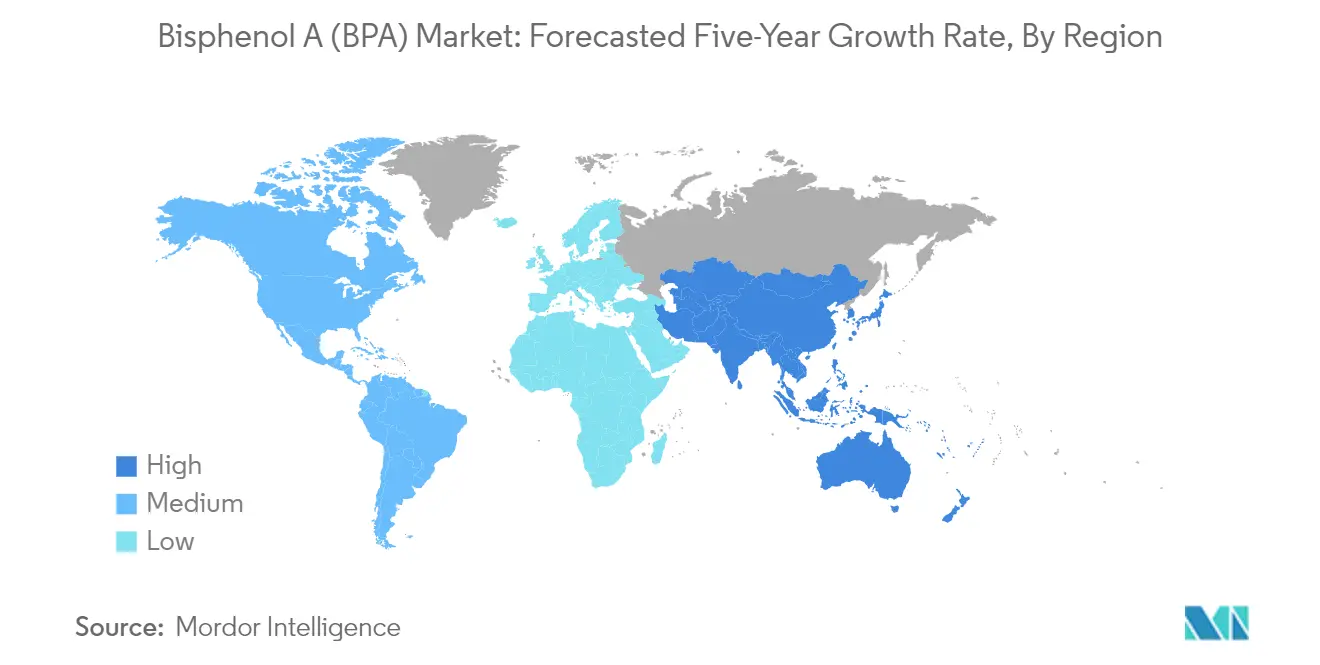

Bisphenol A (BPA) Market in Asia-Pacific

The Asia-Pacific region represents the dominant force in the global Bisphenol A market, driven by robust industrial growth across China, India, Japan, South Korea, and the ASEAN countries. The region's market leadership is supported by extensive manufacturing capabilities, growing end-use industries like automotive and electronics, and continued investments in infrastructure development. The presence of major BPA manufacturers and increasing demand from key application segments like polycarbonate resins and epoxy resins further strengthens the region's market position.

Bisphenol A (BPA) Market in China

China stands as the powerhouse of the Asia-Pacific BPA market, commanding approximately 26% share of the global market. The country's dominance is driven by its massive manufacturing base, particularly in the electronics and automotive sectors. China's robust construction industry, encompassing 20% of global construction investments, continues to fuel demand for BPA-based products. The country's strategic initiatives in expanding polycarbonate production capacities, coupled with growing domestic consumption in various end-use industries, reinforce its position as the regional market leader.

Bisphenol A (BPA) Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 8% during 2024-2029. The country's growth trajectory is supported by rapid industrialization, an expanding manufacturing sector, and government initiatives like "Make in India." The robust growth in construction, automotive, and electronics sectors, coupled with increasing domestic demand for consumer goods, drives the India Bisphenol A market expansion. India's paint industry development and growing focus on infrastructure projects further catalyze market growth.

Bisphenol A (BPA) Market in North America

North America represents a significant market for Bisphenol A, characterized by advanced manufacturing capabilities and high demand from end-use industries. The region's market is primarily driven by the United States, Canada, and Mexico, with a strong presence in the automotive, construction, and electronics sectors. The region's focus on technological advancement and innovation in manufacturing processes continues to shape market dynamics.

Bisphenol A (BPA) Market in United States

The United States dominates the North American BPA market, holding approximately 20% of the global market share. As the second-largest automotive manufacturer globally, the country maintains robust demand for Bisphenol A in various applications. The nation's strong electronics manufacturing base, coupled with significant R&D activities in developing high-end products, reinforces its position as the regional market leader.

Bisphenol A (BPA) Market in Canada

Canada emerges as the fastest-growing market in North America, with an expected growth rate of approximately 5% during 2024-2029. The country's market expansion is driven by increasing investments in construction and infrastructure development projects. The growing focus on sustainable building practices and rising demand from the automotive and electronics sectors further supports market growth.

Bisphenol A (BPA) Market in Europe

The European Bisphenol A market demonstrates a strong presence across Germany, the United Kingdom, Italy, France, and Spain, supported by well-established manufacturing infrastructure and stringent quality standards. The region's market is characterized by an increasing focus on sustainable practices and technological innovations in manufacturing processes. The presence of major automotive and electronics manufacturers, coupled with growing construction activities, drives market growth across the region.

Bisphenol A (BPA) Market in Germany

Germany leads the European Bisphenol A market, supported by its robust automotive and electronics manufacturing sectors. The country's strong industrial base, technological advancement in manufacturing processes, and significant investments in research and development reinforce its position as the regional market leader. The nation's focus on high-quality production and innovation in end-use applications continues to drive market growth.

Bisphenol A (BPA) Market in United Kingdom

The United Kingdom demonstrates the highest growth potential in the European region, supported by increasing investments in construction and infrastructure development. The country's focus on technological advancement in manufacturing processes and growing demand from various end-use industries drives market expansion. The nation's strategic initiatives in developing sustainable solutions and increasing industrial production contribute to market growth.

Bisphenol A (BPA) Market in South America

The South American BPA market, primarily driven by Brazil and Argentina, shows steady growth potential despite economic challenges in the region. Brazil emerges as both the largest and fastest-growing market in the region, supported by its significant manufacturing base and growing demand from various end-use industries. The region's market dynamics are influenced by increasing investments in construction activities, automotive sector development, and growing industrial production.

Bisphenol A (BPA) Market in Middle East & Africa

The Middle East & Africa region, led by Saudi Arabia and South Africa, demonstrates growing potential in the global Bisphenol A market. Saudi Arabia emerges as both the largest and fastest-growing market in the region, driven by significant investments in infrastructure development and industrial expansion. The region's market growth is supported by increasing construction activities, a growing automotive sector, and rising investments in manufacturing capabilities.

Get Analysis on Important Geographic Markets

Download PDF

Bisphenol A Industry Overview

Top Companies in Bisphenol A (BPA) Market

The global Bisphenol A market is led by established players like Covestro AG, SABIC, Chang Chun Group, and Nan Ya Plastics Corporation, who have demonstrated a strong market presence through vertical integration and extensive production capabilities. Companies are increasingly focusing on sustainable production methods, with key players investing in bio-based alternatives and cleaner manufacturing processes. Strategic capacity expansions, particularly in the Asia-Pacific regions, remain a dominant trend as manufacturers aim to meet growing demand from downstream industries. Market leaders are strengthening their positions through technological innovations in production processes and strategic partnerships across the value chain. The industry has witnessed significant investment in research and development activities, particularly in developing environmentally friendly alternatives and improving production efficiency, while maintaining a strong focus on quality control and regulatory compliance.

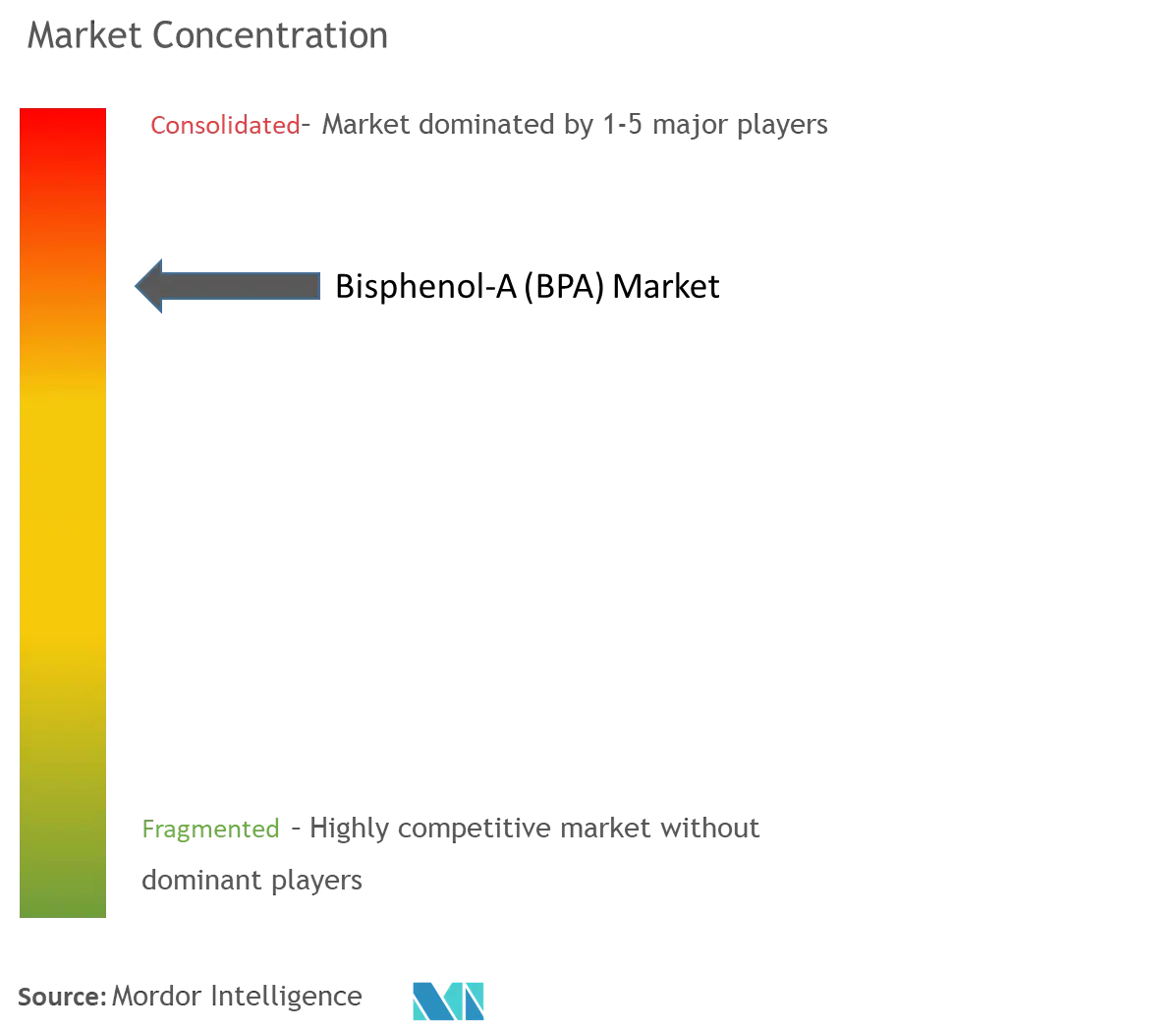

Consolidated Market with Strong Regional Players

The Bisphenol A market exhibits a consolidated structure with the top ten players commanding a significant market share, while regional players maintain a strong presence in their respective territories. Major manufacturers are typically large chemical conglomerates with vertically integrated operations spanning from raw material procurement to end-product manufacturing, particularly in polycarbonate and epoxy resin production. The market has witnessed notable merger and acquisition activities, with companies like Chang Chun Group acquiring Taiwan Prosperity Chemical Corporation and Mitsui Chemicals pursuing majority ownership in joint ventures to strengthen their market positions.

The competitive landscape is characterized by a mix of global chemical giants and regional specialists, with Asian manufacturers, particularly from China, South Korea, and Taiwan, playing increasingly important roles. Companies are focusing on strategic collaborations and joint ventures to enhance their technological capabilities and expand their geographical presence. The industry has seen significant investment in capacity expansions, particularly in emerging markets, while established players in mature markets are focusing on product innovation and sustainability initiatives to maintain their competitive edge.

Innovation and Sustainability Drive Future Growth

Success in the BPA market increasingly depends on companies' ability to address environmental concerns while maintaining operational efficiency. Incumbent players are investing in sustainable production technologies and developing alternatives to traditional BPA products, while new entrants are focusing on niche applications and regional markets to establish their presence. The industry's future competitiveness will be significantly influenced by regulatory compliance capabilities, particularly in regions with stringent environmental and safety regulations, while the ability to maintain cost-effective production amid rising environmental standards will be crucial.

Market players must focus on developing strong relationships with end-users in key industries such as automotive, construction, and electronics, while maintaining flexibility to adapt to changing regulatory landscapes. Companies that can successfully balance environmental sustainability with cost-effective production methods will likely gain competitive advantages. The ability to innovate in response to growing demand for BPA alternatives, particularly in consumer-facing applications, while maintaining strong positions in traditional industrial applications, will be crucial for long-term success. Additionally, companies must develop robust supply chain networks and maintain strong relationships with raw material suppliers to ensure operational stability and cost competitiveness. This is particularly important for Bisphenol A suppliers aiming to secure their position in the market.

Bisphenol A (BPA) Market Leaders

-

Covestro AG

-

SABIC

-

Chang Chun Group

-

Mitsui Chemical Inc.

-

Nan Ya Plastics Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Bisphenol A (BPA) Market News

- March 2023: Teijin Limited launched new biomass-derived Bisphenol-A (BPA) polycarbonate (PC) resin products, which were certified as an ISCC PLUS sustainable product by the International Sustainability and Carbon Certification (ISCC) system to support efforts to achieve carbon neutrality by reducing greenhouse gas (GHG) emissions throughout product lifecycles.

Bisphenol-A Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Soaring Demand from Polycarbonate Sector

- 4.1.2 Increasing Demand from Epoxy Resin Production

-

4.2 Restraints

- 4.2.1 Increasing Regulations in the Food and Beverage Industry

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Feedstock Analysis

- 4.6 Technological Snapshot

- 4.7 Trade Overview

- 4.8 Price Overview

- 4.9 Regulatory Policy Analysis

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 By Application

- 5.1.1 Polycarbonate Resins

- 5.1.2 Epoxy Resins

- 5.1.3 Unsaturated Polyester Resins

- 5.1.4 Flame Retardants

- 5.1.5 Other Applications

-

5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Altivia Petrochemicals

- 6.4.2 Chang Chun Group

- 6.4.3 China National Bluestar (Group) Co. Ltd

- 6.4.4 China Petroleum & Chemical Corporation (SINOPEC)

- 6.4.5 Covestro AG

- 6.4.6 Dow

- 6.4.7 Hexion

- 6.4.8 Idemitsu Kosan Co. Ltd

- 6.4.9 Kumho P&B Chemicals Inc.

- 6.4.10 LG Chem

- 6.4.11 Lihua Yiweiyuan Chemical Co. Ltd

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 Mitsui Chemicals Inc.

- 6.4.14 Nan Ya Plastics Industry Co. Ltd

- 6.4.15 Nippon Steel Chemical & Material Co. Ltd

- 6.4.16 PTT Phenol Company Limited

- 6.4.17 SABIC

- 6.4.18 Samyang Holdings Corporation

- 6.4.19 Teijin Limited

- 6.4.20 Zhejiang Petroleum & Chemical Co. Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Potential Market Demand for Bio-Based BPA

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Bisphenol-A Industry Segmentation

Bisphenol-A (BPA) is a colorless crystalline solid belonging to the organic compound family. It is used primarily as a strengthener in polycarbonate plastics and epoxy resins. BPA is produced industrially by the condensation reaction of phenol and acetone, and it is known for its use in making various consumer goods such as water bottles, sports equipment, CDs, and DVDs.

The Bisphenol-A (BPA) market is segmented by application and geography. By application, the market is segmented into polycarbonate resins, epoxy resins, unsaturated polyester resins, flame retardants, and other applications. The report also covers the market size and forecast for the bisphenol A market in 16 countries across major regions. For each segment, the market sizing and forecast were done based on volume (tons).

| By Application | Polycarbonate Resins | ||

| Epoxy Resins | |||

| Unsaturated Polyester Resins | |||

| Flame Retardants | |||

| Other Applications | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Bisphenol-A Market Research FAQs

How big is the Bisphenol A Market?

The Bisphenol A Market size is expected to reach 8.72 million tons in 2025 and grow at a CAGR of 6.56% to reach 11.98 million tons by 2030.

What is the current Bisphenol A Market size?

In 2025, the Bisphenol A Market size is expected to reach 8.72 million tons.

Who are the key players in Bisphenol A Market?

Covestro AG, SABIC, Chang Chun Group, Mitsui Chemical Inc. and Nan Ya Plastics Corporation are the major companies operating in the Bisphenol A Market.

Which is the fastest growing region in Bisphenol A Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Bisphenol A Market?

In 2025, the Asia Pacific accounts for the largest market share in Bisphenol A Market.

What years does this Bisphenol A Market cover, and what was the market size in 2024?

In 2024, the Bisphenol A Market size was estimated at 8.15 million tons. The report covers the Bisphenol A Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Bisphenol A Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Bisphenol A (BPA) Market Research

Mordor Intelligence delivers comprehensive insights into the Bisphenol A (BPA) industry through detailed market analysis and consulting expertise. Our extensive research covers BPA production processes, technical properties of Bisphenol A, and crucial market dynamics. These include price trends and supply chain analysis. The report provides an in-depth analysis of the Bisphenol A market. It examines key BPA suppliers and production facilities worldwide while tracking current Bisphenol A prices and industry developments.

Stakeholders gain valuable insights through our detailed assessment of BPA trends 2023 and beyond. This is supported by robust data on Bisphenol A production cost factors and market indicators. The report, available as an easy-to-download PDF, includes a thorough evaluation of BPA investments and industry growth patterns. Our analysis encompasses global market dynamics, featuring a detailed examination of Bisphenol A industry segments and regional market variations. This provides stakeholders with actionable intelligence for informed decision-making in this evolving sector.