Biomarkers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 63.56 Billion |

| Market Size (2031) | USD 107.02 Billion |

| Growth Rate (2026 - 2031) | 10.99% CAGR |

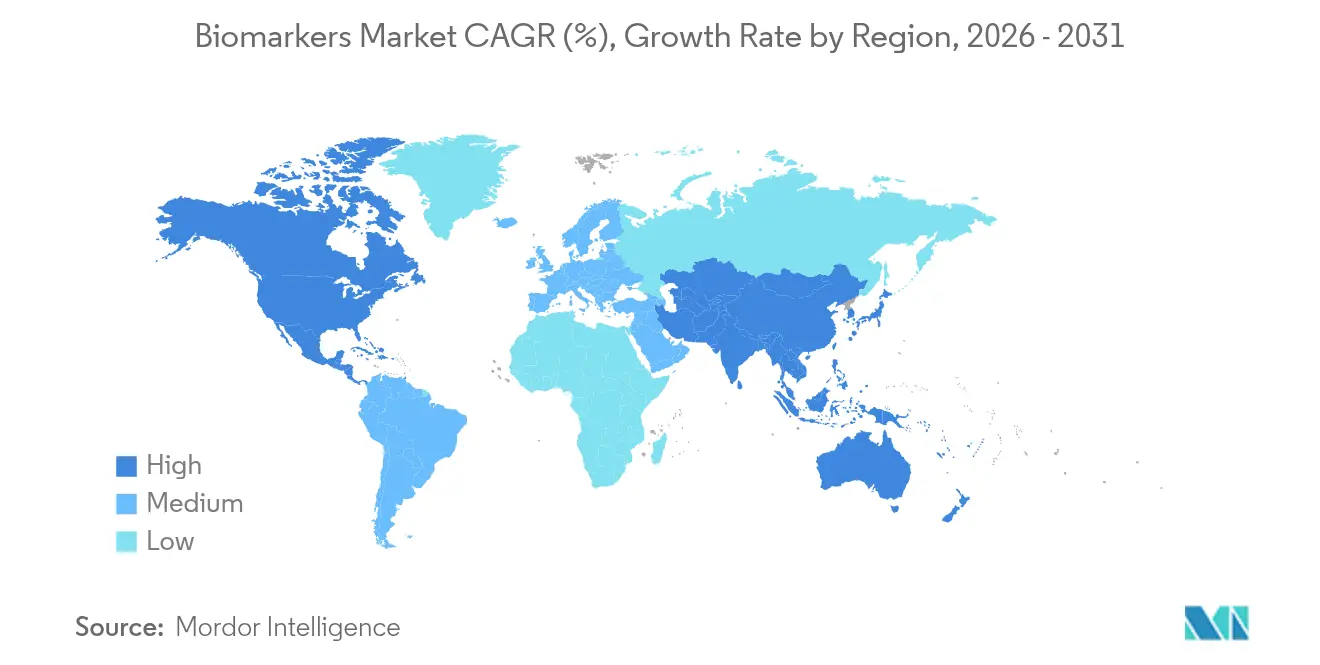

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Biomarkers Market Analysis by Mordor Intelligence

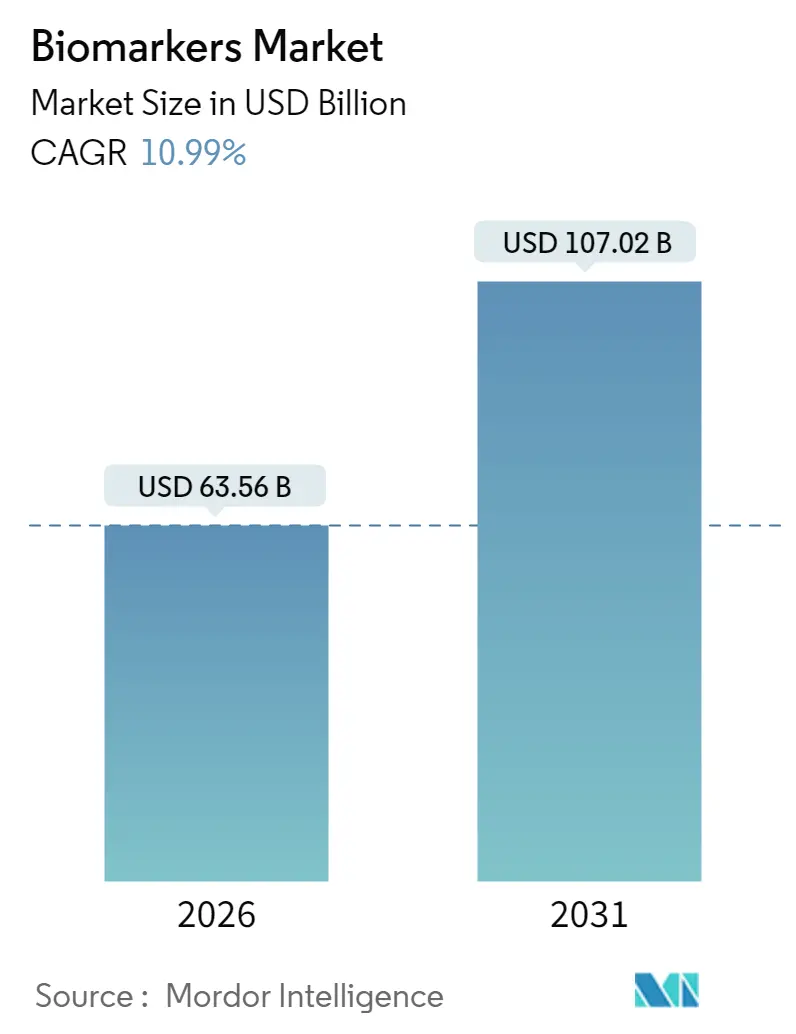

The Biomarkers Market was valued at USD 57.27 billion in 2025 and estimated to grow from USD 63.56 billion in 2026 to reach USD 107.02 billion by 2031, at a CAGR of 10.99% during the forecast period (2026-2031).

Momentum reflects artificial-intelligence-enabled discovery pipelines, wider regulatory acceptance of digital endpoints, and the push for precision medicine across oncology, immunology, neurology, and cardiology. Continued breakthrough-device designations, expanding multi-omics toolkits, and reimbursement pathways that reward targeted therapies fuel uptake of validated tests in routine care. Companion diagnostics now anchor treatment decisions, especially in oncology, where liquid biopsy and DNA methylation assays widen access to early detection and therapy matching. Investments in proteomics platforms, cloud bioinformatics, and real-world evidence solutions position vendors to capture recurring revenue from consumables, services, and software. Yet complex reimbursement policies and data-privacy regulations temper near-term adoption curves.

Key Report Takeaways

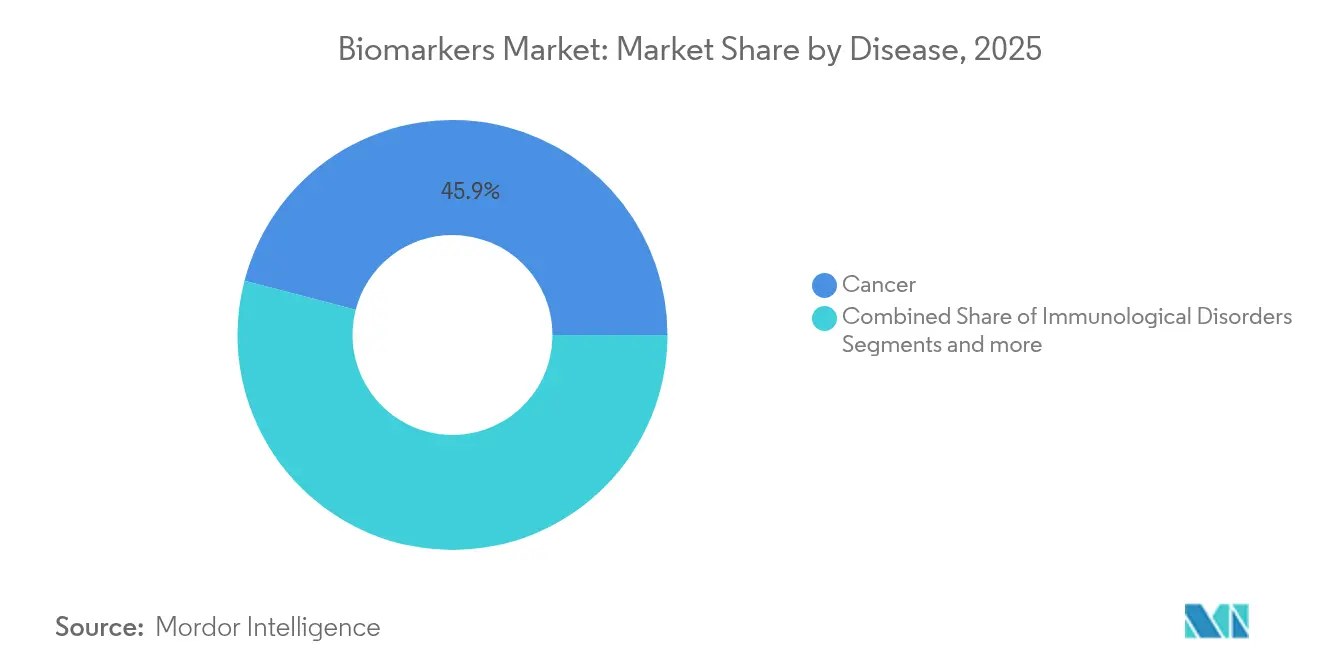

- By disease, cancer led with 45.94% revenue share in 2025; immunological disorders are expanding at an 11.8% CAGR through 2031.

- By biomarker type, efficacy biomarkers held 57.78% of the market share in 2025, while safety biomarkers post the fastest 11.67% CAGR to 2031.

- By mechanism, genetic biomarkers accounted for 46.85% share of the biomarkers market size in 2025; epigenetic biomarkers are set to climb at an 11.7% CAGR.

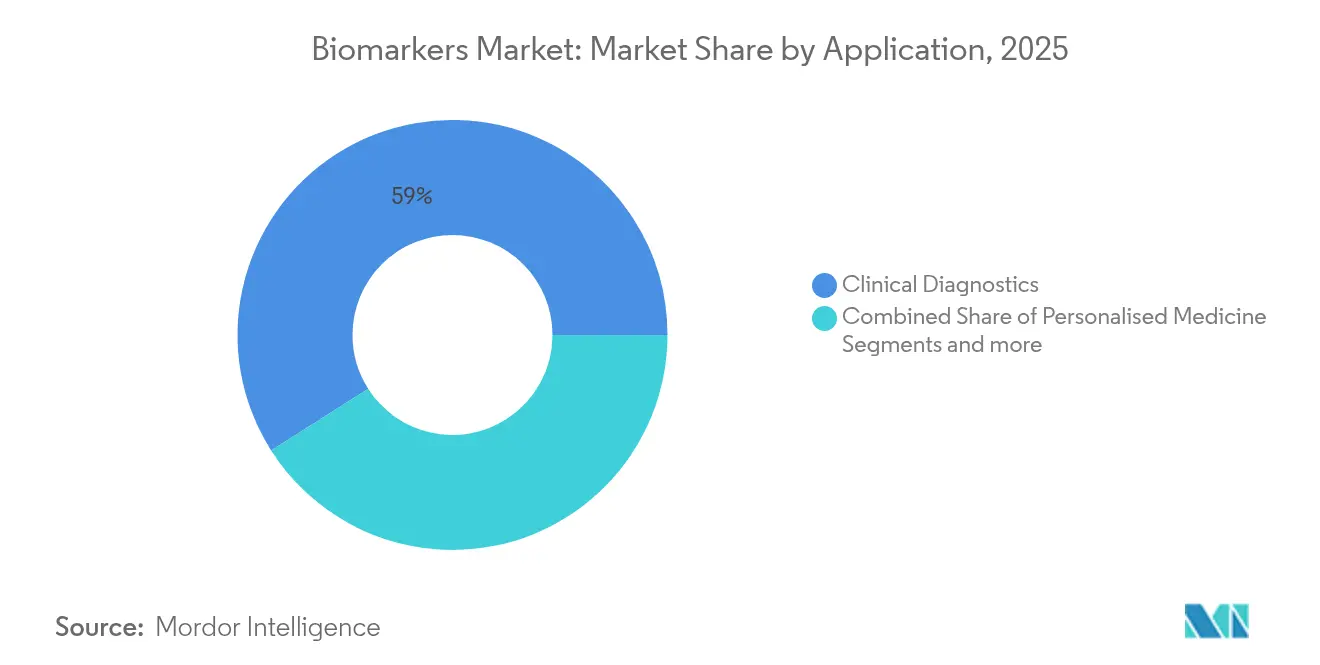

- By application, clinical diagnostics represented 59.02% share in 2025; personalized medicine advances at an 11.78% CAGR during the same horizon.

- By product, consumables made up 53.71% of spending in 2025, whereas services and software revenue is progressing at an 11.79% CAGR.

- By geography, North America commanded 42.35% share in 2025 and Asia Pacific registers the highest 11.72% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biomarkers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Life-Threatening Diseases | +2.8% | Global, with concentration in aging populations of North America & Europe | Long term (≥ 4 years) |

| Growing Demand for Early & Accurate Diagnosis | +2.1% | Global, particularly strong in developed markets | Medium term (2-4 years) |

| Advancements In Multi-Omics Technologies | +1.9% | North America & EU leading, APAC rapidly adopting | Medium term (2-4 years) |

| Expansion Of Companion Diagnostics in Oncology | +1.7% | Global, with regulatory leadership in US & EU | Short term (≤ 2 years) |

| AI-Powered Multi-Modal Biomarker Discovery | +1.4% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Proliferation Of Digital Biomarkers Via Wearables | +1.2% | Global, with consumer adoption leading in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Life-Threatening Diseases

Chronic and life-threatening diseases are accelerating demand for refined biomarker panels. Rheumatoid arthritis registers 200,000 new U.S. cases each year, spurring adoption of 14-3-3 η protein assays that reach 74% sensitivity and 90% specificity for early detection. Age-related disorders amplify the need for minimally invasive screens; for Alzheimer’s, blood-based pTau217 recently obtained FDA breakthrough designation and improves accessibility beyond cerebrospinal fluid testing [1]Roche, “FDA Grants Breakthrough Device Designation to Blood-Based pTau217 Assay.” roche.com . Healthcare systems pivot toward preventive medicine, prompting multiplex platforms capable of measuring markers across oncology, cardiology, and neurodegeneration in a single run. Such breadth keeps the market on a firm growth path.

Growing Demand for Early & Accurate Diagnosis

Early intervention strategies make biomarkers pivotal predictive instruments rather than confirmatory tools. CLAIRITY BREAST, an AI model that forecasts five-year breast-cancer risk from mammograms, illustrates how imaging biomarkers support proactive screening. Liquid biopsy assays detecting circulating tumor-DNA methylation now achieve 96.67% sensitivity for hepatocellular carcinoma within a 24-hour workflow [2]Jialing Sun, "A liquid biopsy approach detects HCC and identifies GJA4 as a potential biomarker for HBV-HCC via plasma cfDNA methylome profiling," Clinical Epigenetics, clinicalepigeneticsjournal.biomedcentral.com. Wearables extend detection beyond clinics, with continuous monitoring of cardiometabolic indicators that trigger timely physician alerts. Artificial-intelligence-augmented analytics shorten interpretation time, easing integration into varied care settings and expanding the biomarkers market.

Advancements in Multi-Omics Technologies

Integrating genomics, proteomics, metabolomics, and epigen omics yields molecular portraits impossible with single-marker assays. Current proteomic platforms quantify 11,000 plasma proteins from microliter samples, enabling organ-specific aging analyses. Illumina’s 5-base chemistry supports simultaneous variant calling and methylation analysis in one workflow, boosting discovery productivity [3]Illumina, “New 5-Base Sequencing Chemistry Accelerates Multi-Omics.” illumina.com . Falling sequencing and mass-spectrometry costs democratize such comprehensive profiling, giving clinical labs new tools to advance precision medicine across the market.

Expansion of Companion Diagnostics in Oncology

Precision oncology standard-of-care status propels companion diagnostics revenue. Illumina’s TruSight Oncology Comprehensive became the first pan-tumor assay covering 500 biomarkers cleared by the FDA for therapy selection. Roche’s VENTANA MET RxDx test identifies non-squamous NSCLC patients eligible for c-MET-targeted treatment, underscoring regulators’ preference for marker-guided prescribing. Pharmaceutical sponsors value biomarker-stratified trials for higher approval odds, further buoying the biomarkers market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Reimbursement & Regulatory Pathways | -1.8% | Global, particularly complex in fragmented healthcare systems | Medium term (2-4 years) |

| High Assay Development & Validation Costs | -1.2% | Global, with higher impact in resource-constrained markets | Long term (≥ 4 years) |

| Data-Privacy Challenges with Real-World Digital Biomarkers | -0.8% | Global, with stricter regulations in EU and emerging frameworks in APAC | Short term (≤ 2 years) |

| Sample-To-Answer Workflow Variability in Low-Resource Labs | -0.6% | Emerging markets and rural healthcare settings globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Reimbursement & Regulatory Pathways

Divergent global rules slow commercialization. The FDA will phase out laboratory-developed-test enforcement discretion over four years, imposing device-level controls on clinical labs. Europe’s In Vitro Diagnostic Regulation tightened evidence demands, while Asia-Pacific requirements remain inconsistent. Payers often require extra real-world evidence, delaying revenue for innovators and marginally cooling biomarkers market expansion.

High Assay Development & Validation Costs

Multi-omics panels must show analytical robustness across patient subgroups, raising study budgets into multimillion-dollar territory. Newly issued bioanalytical‐method-validation guidance further elevates evidence thresholds. Digital endpoints add algorithm-performance studies in diverse real-world settings. These expenses favor well-capitalized firms and can slow new-entrant contributions to the biomarkers market.

Segment Analysis

By Disease: Cancer Dominance Drives Immunological Surge

The cancer segment generated 45.94% of 2025 revenue within the biomarkers market. Decades of investment in genetic and protein markers, combined with fast-track companion diagnostic approvals, sustain leadership. Epigenetic liquid biopsy tests now identify multiple tumor types from a 10 ml blood draw, improving access to early treatment.

Immunological disorders are advancing at an 11.8% CAGR toward 2031, narrowing the gap. Rising autoimmune prevalence and the validation of markers such as 14-3-3 η protein in seronegative rheumatoid arthritis open new clinical workflows. Broader multiplex panels capable of tracking cytokine storms and treatment response fuel long-term growth in this slice of the biomarkers market.

Note: Segment shares of all individual segments available upon report purchase

By Type: Safety Biomarkers Accelerate Amid Efficacy Leadership

Efficacy biomarkers accounted for 57.78% of 2025 spending, reflecting their use in predicting progression, guiding therapy choice, and serving as surrogate endpoints. Oncology and cardiology trials rely on established markers to cut timelines and optimize dosing.

Safety biomarkers climb fastest at 11.67% CAGR as regulators require human-relevant toxicity indicators before market authorization. AI-enabled in-vitro models read renal and hepatic stress signals within hours, supporting earlier attrition decisions. Expansion of these panels underpins risk-mitigation strategies and enlarges the biomarkers market size for pharmacovigilance.

By Mechanism: Epigenetic Innovation Challenges Genetic Dominance

Genetic biomarkers retained 46.85% share of the biomarkers market in 2025, supported by well-established sequencing workflows and clear regulatory guidance. Companion diagnostics based on EGFR, BRAF, and BRCA mutations remain staples in precision therapy.

Epigenetic biomarkers, growing at 11.7% CAGR, are shrinking this gap. DNA-methylation signatures detect early cancer signals months before imaging confirms lesions. Artificial-intelligence models integrate these epigenetic clocks with proteomic data for age-related disease risk scoring. Such capabilities channel additional capital toward the biomarkers market.

By Application: Personalized Medicine Momentum Builds

Clinical diagnostics captured 59.02% share in 2025, reflecting routine cholesterol, HbA1c, and infectious-disease panels that underpin everyday decision making. Hospitals favor consolidated analyzers capable of processing both conventional and novel biomarkers.

Personalized medicine applications expand at an 11.78% CAGR. The biomarkers market size for stratified therapy selection is widening as payers reward biomarker-guided regimens that avoid ineffective drugs. Platforms such as QIAGEN’s QIAstat-Dx bring rapid genotyping to routine outpatient visits, accelerating adoption.

Note: Segment shares of all individual segments available upon report purchase

By Product: Services & Software Innovation Accelerates

Consumables delivered 53.71% of revenue in 2025, driven by steady reagent replenishment across centralized and point-of-care laboratories. Manufacturers sustain margins through proprietary antibodies and assay kits.

Services and software revenue is growing at 11.79% CAGR. Cloud bioinformatics suites translate raw proteomic or genomic data into actionable insights in minutes. GRAIL’s machine-learning pipeline, for instance, analyzes circulating-tumor-DNA patterns to pinpoint tumor origin with high specificity. Such analytical depth raises switching costs and enlarges recurring income opportunities within the biomarkers market.

Geography Analysis

North America held 42.35% of global revenue in 2025 owing to FDA programs that qualify biomarkers for regulatory submissions and streamline payer coverage. Robust reimbursement and an extensive hospital network maintain high test volumes. Academic-industry consortia fast-track translation from bench to bedside, consolidating regional influence in the biomarkers market.

Asia Pacific is advancing at an 11.72% CAGR through 2031. China’s 24-measure regulatory overhaul hastens innovative-device clearance, while Japan’s national biotechnology plan targets 15 trillion yen market output by decade end. Aging demographics and new reimbursement codes for liquid biopsy spur rapid adoption, positioning Asia Pacific as a prime demand center for the biomarkers market.

Europe maintains consistent growth under the In Vitro Diagnostic Regulation’s stringent evidence demands. Cross-border research networks produce large cohorts that validate digital and multi-omics biomarkers for chronic disease management. Middle East, Africa, and South America offer greenfield opportunities as health-system modernization and medical tourism stimulate demand for advanced diagnostics within an emerging biomarkers market ecosystem.

Competitive Landscape

Competition is moderate but intensifying. Thermo Fisher’s USD 3.1 billion purchase of Olink secures deep proteomics content and elevates end-to-end multi-omics offerings. Standard BioTools’ merger with SomaLogic creates a diversified player spanning cytometry, NGS sample prep, and protein detection. Sellers differentiate through proprietary assay menus, regulatory clearances, and data-analytics platforms that bind customers to integrated ecosystems.

Partnerships remain pivotal. Thermo Fisher works with Bayer on companion diagnostics, while QIAGEN aligns with AstraZeneca for targeted therapy panels. Biogen teams with Beckman Coulter and Fujirebio to develop blood-based Alzheimer’s assays. Such alliances distribute risk and shorten time-to-market, widening the biomarkers market reach.

White-space persists in digital biomarkers and AI-optimized trial endpoints. Smaller firms leverage the FDA biomarker-qualification pathway to gain visibility, as seen with Critical Path Institute’s kidney-injury panel that may reshape drug-safety surveillance. The 2025 competitive map therefore blends diagnostics stalwarts, venture-backed analytics specialists, and tech entrants converging on precision-health revenue streams.

Biomarkers Industry Leaders

-

Bio-Rad Laboratories

-

Qiagen

-

F. Hoffmann-La Roche Ltd

-

Thermo Fisher Scientific Inc.

-

Illumina Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Quest Diagnostics joined MD Anderson Cancer Center to create blood-based cancer risk screens that can be scaled through Quest’s nationwide lab network.

- May 2025: Roche won FDA approval for the VENTANA MET (SP44) RxDx assay, the first companion diagnostic to guide Emrelis therapy in MET-positive NSCLC.

- April 2025: Labcorp released Plasma Detect for stage III colon-cancer recurrence risk and PGDx elio plasma focus Dx, the first FDA-authorized kitted pan-solid-tumor liquid biopsy.

- April 2025: Olaris secured investment from Labcorp to expand metabolomics-based myOLARIS tests for kidney‐transplant monitoring.

Global Biomarkers Market Report Scope

As per the scope of the report, a biomarker refers to a biomolecule or gene used to precisely evaluate the body's pharmacologic, pathogenic, and biological procedures. They serve as an early warning system in the body. It can also be stated as a traceable subsite introduced into the body to check or examine the organ's function. It can be measured and evaluated by using blood, urine, or soft tissues.

The biomarkers market is segmented by disease, type, mechanism, and geography. By disease, the market is segmented into cancer, cardiovascular disorders, neurological disorders, immunological disorders, renal disorders, and other diseases. By type, the market is segmented into efficacy biomarkers, safety biomarkers, and validation biomarkers. By mechanism, the market is segmented into genetic, epigenetic, proteomic, lipidomic, and other mechanisms. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD) for all the above-mentioned segments.

| Cancer |

| Cardiovascular Disorders |

| Neurological Disorders |

| Immunological Disorders |

| Renal Disorders |

| Other Diseases |

| Efficacy Biomarkers | Prognostic Biomarkers |

| Predictive Biomarkers | |

| Pharmacodynamic Biomarkers | |

| Surrogate Endpoint Markers | |

| Safety Biomarkers | |

| Validation Biomarkers |

| Genetic Biomarkers |

| Epigenetic Biomarkers |

| Proteomic Biomarkers |

| Lipidomic Biomarkers |

| Others |

| Clinical Diagnostics |

| Drug Discovery and Development |

| Personalised Medicine |

| Disease Risk Assessment |

| Others |

| Consumables |

| Instruments |

| Services and Software |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease | Cancer | |

| Cardiovascular Disorders | ||

| Neurological Disorders | ||

| Immunological Disorders | ||

| Renal Disorders | ||

| Other Diseases | ||

| By Type | Efficacy Biomarkers | Prognostic Biomarkers |

| Predictive Biomarkers | ||

| Pharmacodynamic Biomarkers | ||

| Surrogate Endpoint Markers | ||

| Safety Biomarkers | ||

| Validation Biomarkers | ||

| By Mechanism | Genetic Biomarkers | |

| Epigenetic Biomarkers | ||

| Proteomic Biomarkers | ||

| Lipidomic Biomarkers | ||

| Others | ||

| By Application | Clinical Diagnostics | |

| Drug Discovery and Development | ||

| Personalised Medicine | ||

| Disease Risk Assessment | ||

| Others | ||

| By Product | Consumables | |

| Instruments | ||

| Services and Software | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the biomarkers market?

The biomarkers market is valued at USD 63.56 billion in 2026 and is forecast to reach USD 107.02 billion by 2031.

Which disease segment leads the biomarkers market?

Cancer biomarkers command 45.94% market share, supported by extensive companion diagnostic approvals in oncology.

Why are safety biomarkers growing faster than other types?

Regulatory agencies now emphasize human-relevant toxicity indicators, driving an 11.67% CAGR for safety biomarkers through 2031.

Which region will grow the fastest in the biomarkers market?

Asia Pacific is projected to expand at an 11.72% CAGR, driven by regulatory reforms in China and Japan that speed device approvals.

How is artificial intelligence influencing biomarker development?

AI accelerates multi-modal biomarker discovery, shortens validation cycles, and powers digital biomarkers from imaging and wearable data, broadening precision-medicine applications.

What recent regulatory actions affect laboratory-developed biomarker tests?

The FDA’s proposed rule will phase out enforcement discretion for laboratory-developed tests over four years, aligning them with medical-device regulations and raising evidence requirements.