Bio-polylactic Acid (PLA) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

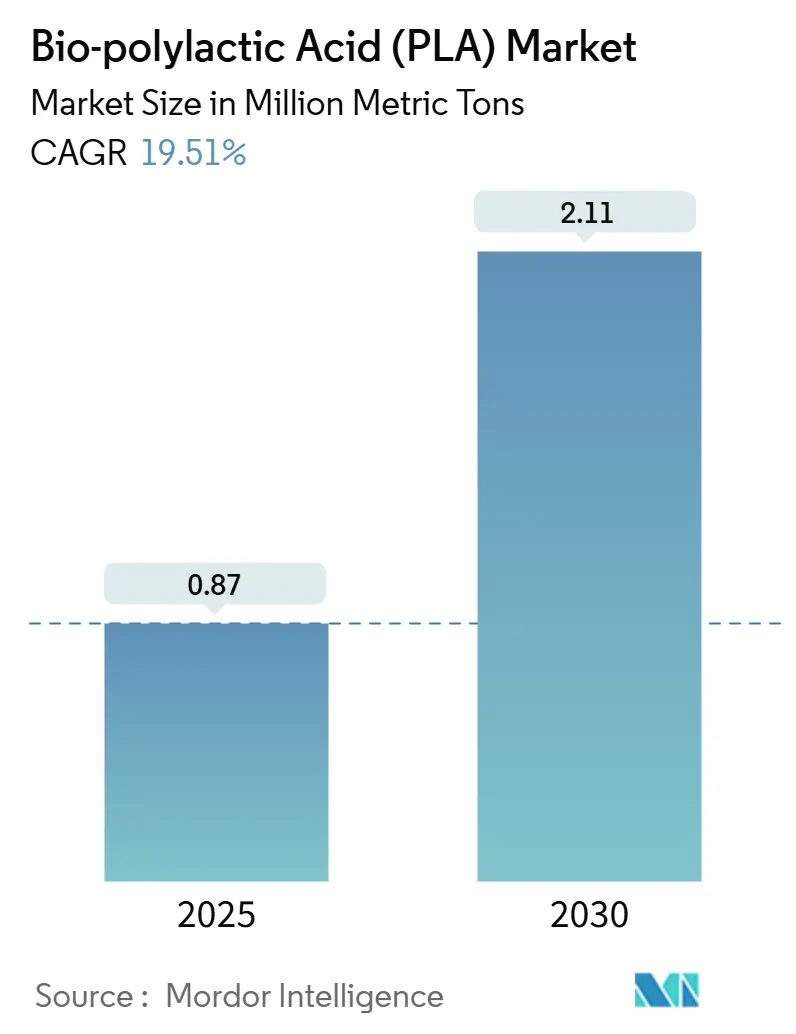

| Market Volume (2025) | 0.87 Million metric tons |

| Market Volume (2030) | 2.11 Million metric tons |

| Growth Rate (2025 - 2030) | 19.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bio-polylactic Acid (PLA) Market Analysis by Mordor Intelligence

The Bio-polylactic Acid Market size is estimated at 0.87 Million metric tons in 2025, and is expected to reach 2.11 Million metric tons by 2030, at a CAGR of 19.51% during the forecast period (2025-2030). Strong legislative pressure on single-use plastics, rapid cost deflation from Asian capacity additions, and breakthrough enzymatic recycling technologies have moved the Bio-polylactic Acid market from a niche to a mainstream materials solution. Demand growth is no longer confined to rigid and flexible packaging, as high-heat automotive interiors, medical devices, and 3D-printed electronics adopt advanced grades that match or exceed petro-polymer performance benchmarks. Sugarcane and sugar beet feedstocks lead raw-material substitution on the back of lower carbon intensity and more stable pricing compared with corn, while geographically the Asia-Pacific production base secures the cost leadership that underpins global competitiveness. Competitive dynamics remain fluid: incumbent producers scale world-class plants close to feedstock sources, and new entrants leverage proprietary depolymerization enzymes to win sustainability-driven contracts in Europe, North America, and Japan.

Key Report Takeaways

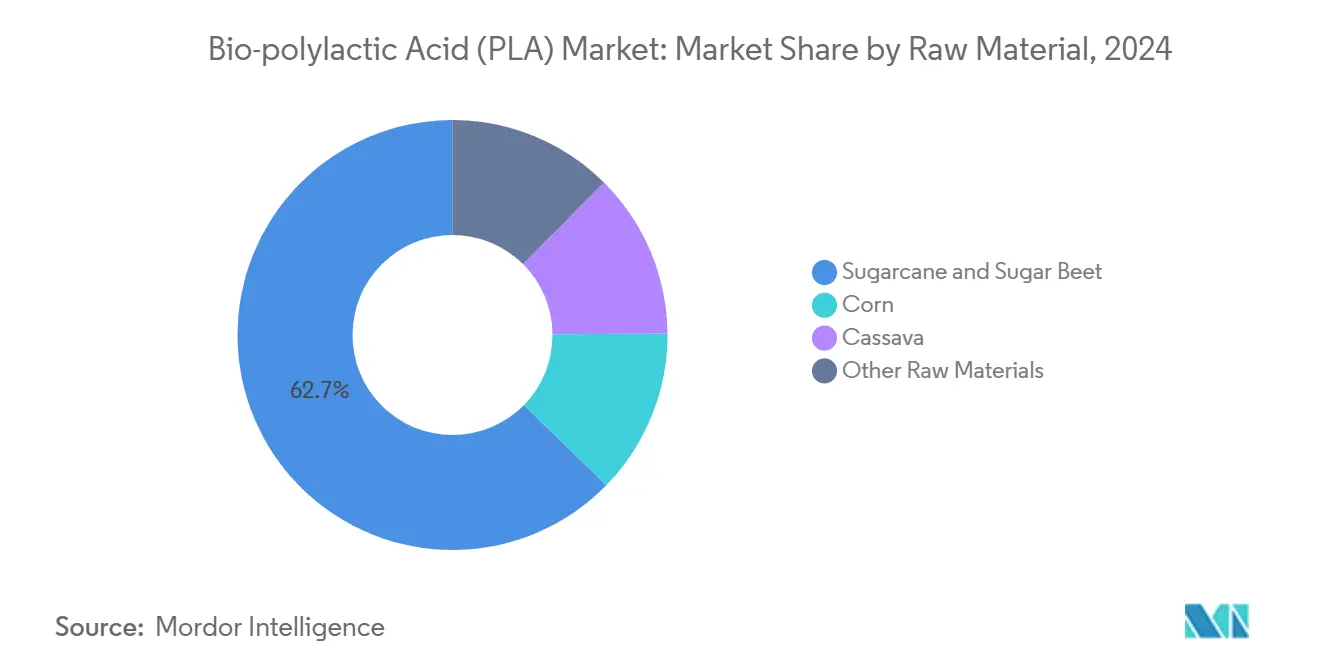

- By raw material, sugarcane and sugar beet held 62.66% of the Bio-polylactic Acid market share in 2024, and the segment is projected to accelerate at a 20.24% CAGR to 2030.

- By form, films and sheets accounted for 84.74% of the Bio-polylactic Acid market size in 2024 and are advancing at a 20.06% CAGR through 2030.

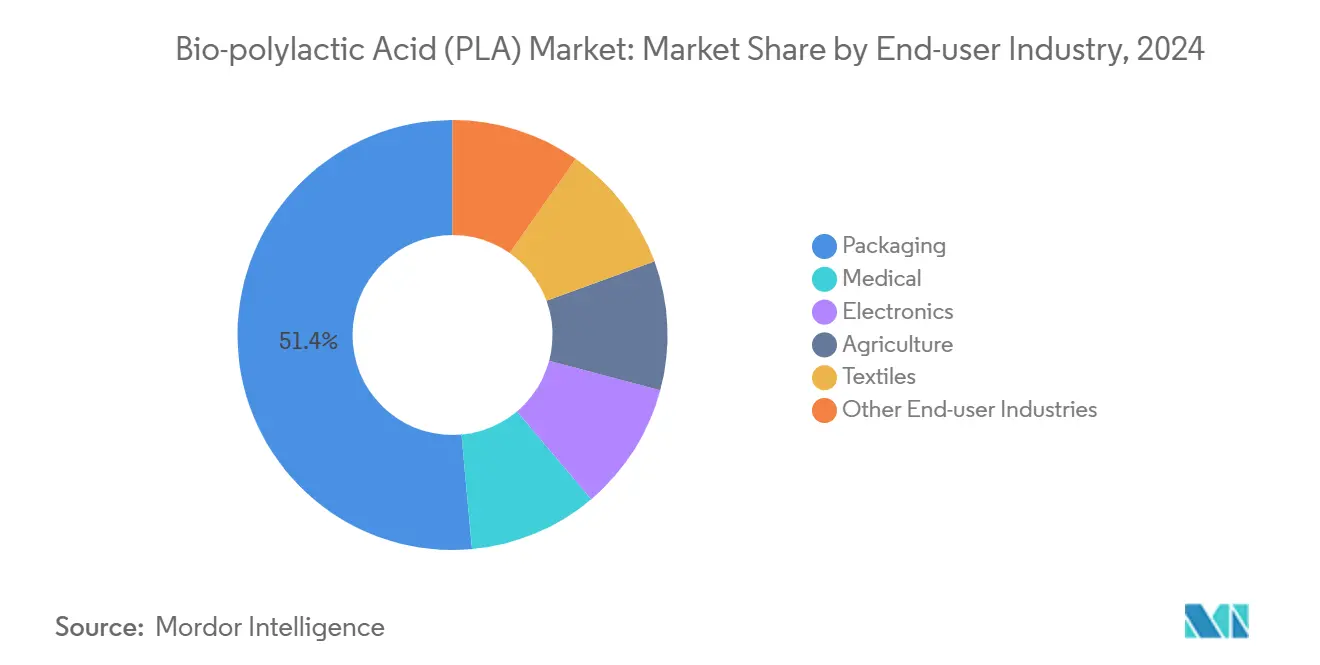

- By end-user industry, packaging captured 51.45% revenue share of the Bio-polylactic Acid market in 2024, while its volume base is forecast to expand at a 22.15% CAGR to 2030.

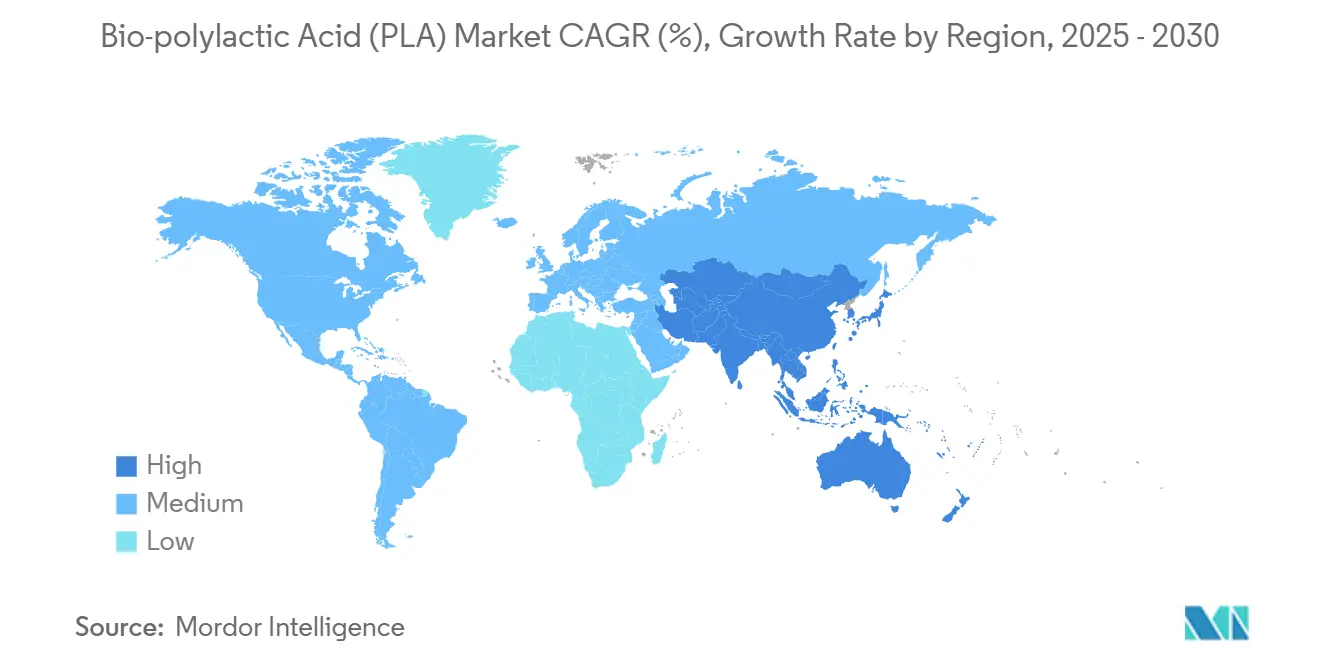

- By geography, Asia-Pacific led with 40.92% Bio-polylactic Acid market share in 2024, and the region exhibits the fastest growth trajectory at 22.68% CAGR through 2030.

Global Bio-polylactic Acid (PLA) Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government bans on single-use plastics and compostable-pack mandates | +4.2% | Global, with early adoption in EU, California, Australia | Short term (≤ 2 years) |

| Chinese capacity surge lowering PLA production cost | +3.8% | APAC core, spill-over to global markets | Medium term (2-4 years) |

| E-commerce meal-kit boom driving demand for compostable films | +2.9% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Emerging closed-loop PLA recycling pilots in EU and Japan | +2.1% | EU and Japan, with technology transfer potential | Long term (≥ 4 years) |

| High-heat PLA adoption in automotive interior composites | +1.8% | Global automotive hubs: Germany, Japan, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Bans on Single-Use Plastics Drive Regulatory Momentum

A cascade of regulations accelerates the Bio-polylactic Acid market demand by making certified compostability a legal requirement for numerous products. California’s AB 1201, effective in 2026, restricts compostable labels to materials that meet USDA National Organic Program standards, effectively removing subpar bioplastics from the shelf. New South Wales' enforcement of extensive single-use restrictions from 2025 prompts rapid substitution toward PLA certified to Australian standards[1]Environmental Protection Authority of New South Wales, “Plastics bans and packaged food and drinks,” epa.nsw.gov.au. The White House Plastic Strategy, announced in 2024, eliminates federal procurement of single-use plastics by 2027, opening institutional channels equivalent to several hundred thousand tons of incremental demand. South Australia’s 2025 ban on non-certified compostable labels further tightens compliance frameworks and shifts purchasing specifications toward high-purity PLA grades.

Chinese Capacity Expansion Reshapes Global Cost Structure

Asia-Pacific hosts the pivotal cost-down phase of the Bio-polylactic Acid market. NatureWorks secured USD 350 million to build a 75,000-ton sugarcane-based plant in Thailand, illustrating the capital intensity required to achieve globally competitive economics. Emirates Biotech selected Sulzer technology for a UAE mega-facility that will commence operations in 2028, further enlarging the Asian and Middle-East footprint. Indian sugar player Balrampur Chini Mills is investing INR 2,000 crores in a 75,000 ton PLA line, exemplifying diversification beyond China while retaining regional feedstock advantages. As larger plants focus on commodity grades, niche producers defend premium pricing through specialty alloy development and certified low-carbon footprints.

E-commerce Packaging Demand Accelerates Compostable Film Adoption

Online grocery, meal-kit, and beverage pod formats are rewriting performance specifications for barrier films. NatureWorks and IMA developed a turnkey compostable coffee pod compatible with leading single-serve systems, proving that PLA can deliver high oxygen barriers and maintain aroma integrity through the supply chain. Studies on PLA/PBAT composites register 92% reductions in oxygen permeability versus neat PLA, satisfying meat and produce shelf-life requirements. Retail logistics giants favor lightweight compostable films to cut freight weight and hit corporate emissions targets, channeling new demand streams into the Bio-polylactic Acid market. Rapid throughput in distribution centers validates PLA’s mechanical toughness under high-speed form-fill-seal operations, a hurdle that restrained adoption just five years ago.

Closed-Loop Recycling Technology Emerges as Competitive Differentiator

Chemical and enzymatic depolymerization breakthroughs transform PLA from a single-use compliant option into a fully circular, high-value polymer. A Nature study embedded an engineered enzyme directly into PLA, achieving complete biodegradation at ambient composting conditions within 24 weeks and setting a new benchmark for end-of-life performance. Hydroxyl carboxylate ionic-liquid catalysis depolymerizes PLA under mild conditions, yielding glycolic acid with recyclable catalysts and no metal residues. The CBE JU-funded ENZYCLE project validates industrial-scale enzyme reactors capable of handling heterogeneous post-consumer streams[2]European Commission, “Innovative Enzyme Technology Leads the Fight Against Plastic Waste,” cbe.europa.eu. Microwave-assisted alkaline hydrolysis reaches 100% depolymerization in under 15 minutes, offering rapid, energy-efficient monomer recovery for repolymerization while protecting optical purity. Producers integrating such technologies can guarantee closed-loop certification, unlocking premium pricing in medical and electronics markets where traceability is paramount.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feed-corn price volatility impacting PLA economics | -2.8% | Global, with acute impact in North America corn belt | Short term (≤ 2 years) |

| Insufficient industrial composting capacity in most regions | -3.2% | Global, particularly acute in developing markets | Medium term (2-4 years) |

| Concentrated IP around enzymatic PLA depolymerisation raises costs | -1.9% | Global technology deployment, licensing bottlenecks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industrial Composting Infrastructure Gaps Constrain Market Realization

Only four out of five tested rigid PLA items achieved full disintegration under simulated composting, and some samples emitted microplastic fragments, revealing performance shortfalls when compost envelope conditions are sub-optimal. Municipal waste managers in the United States report that separating compostable from non-compostable items is financially and operationally unworkable, forcing many loads into landfills despite consumer intentions. The U.S. National Organic Program currently finds that no commercial biodegradable mulch film meets its biobased and degradation requirements, blocking PLA entry into a potentially lucrative agricultural segment. Infrastructure scarcity is even more pronounced in Latin America, South Asia, and Africa where less than 5% of municipal solid waste passes through controlled composting. Until curbside systems scale, claims of biodegradability may ring hollow for policymakers and consumers, periodically slowing the Bio-polylactic Acid market adoption curve.

Concentrated IP Around Enzymatic PLA Depolymerization Raises Costs

Teknor Apex’s acquisition of Danimer Scientific consolidates more than 480 PLA-related patents, including pivotal enzyme cocktails and self-degrading resin grades. High royalty expectations could limit third-party deployment of state-of-the-art depolymerization unless cross-licensing emerges. Producers without internal research and development pipelines must either absorb fee structures or settle for older, less efficient recycling methods. Regulatory incentives in Europe for chemically recycled content place a competitive advantage in the hands of patent holders, potentially stalling broader technology diffusion. The Bio-polylactic Acid market, therefore, grapples with a tension between open-loop drop-in disposal and closed-loop premium accreditation until IP pools become more accessible.

Segment Analysis

By Raw Material: Sugarcane Feedstocks Anchor Cost and Carbon Gains

Sugarcane and sugar beet supplied 62.66% of the Bio-polylactic Acid market share in 2024, rising on a 20.24% CAGR trajectory that signals a deep realignment of raw-material sourcing. Sugarcane fermentation yields lower process CO₂ than corn variants because crop cultivation requires minimal fertilizer and irrigation inputs in tropical geographies. TotalEnergies Corbion’s Rayong line leverages local cane syrup, trimming logistics emissions by 15% compared with imported corn starch and ensuring ISCC PLUS certification that unlocks European eco-label access. Producers in Brazil and Thailand plan to integrate bagasse cogeneration to push life-cycle analysis toward net-negative profiles.

Corn retains meaningful volume in North America because existing wet-milling assets and established enzyme supply chains reduce capital barriers for brownfield PLA retrofits. Cassava obtains attention as a non-food alternative plentiful in Vietnam, Indonesia, and Nigeria; its high starch content and moderate agronomic inputs present a path to low-cost lactic acid when local drying capacity is available. Research demonstrates that molasses feedstocks can cut operating costs by 37% at 100,000-ton scale plants, giving vertically integrated sugar groups a compelling diversification option.

Note: Segment shares of all individual segments available upon report purchase

By Form: Films and Sheets Lock in Packaging Dominance

Films and sheets held 84.74% of the Bio-polylactic Acid market size in 2024 and display a healthy 20.06% CAGR through 2030, mirroring the sustained boom in food service and e-commerce packaging. PLA’s polarity, crystallinity control, and inherent grease resistance make it an ideal substrate for snack lamination and lidding films. Mechanical stiffness provides machinability on high-speed lines without equipment redesign, while compostability logos amplify brand storytelling in crowded supermarket aisles.

Fibers represent a fast-emerging outlet as apparel brands commit to fossil-free supply chains. PLA fiber melt-spinning eliminates solvent use, and blending with lyocell boosts drape and moisture management for sportswear. In medical textiles, nonwoven PLA masks and gowns meet ASTM barrier standards while offering landfill diversion through controlled composting. Coatings exploit PLA’s hydrolytic erosion to deliver time-release agrochemicals and resorbable orthopedic implants, creating premium niches away from commodity film battles. Injection-molding grades formulated with chain extenders enable durable housings for electronics that require UL 94 V-0 flammability ratings, widening the functional scope of the Bio-polylactic Acid market.

By End-User Industry: Packaging Sets the Benchmark for Circular Metrics

Packaging claimed 51.45% of the Bio-polylactic Acid market in 2024 and marches on at a 22.15% CAGR, driven by retailer take-back schemes and mandatory compostable quotas for organic waste streams in Europe. Food contact authorization under EU 10/2011 lists PLA as an approved additive, simplifying compliance for converters. High-clarity salad clamshells demonstrate comparable haze values to PET, allowing brand owners to swap materials without design compromise. Coffee capsule innovators gain patent cover for PLA bodies coupled with paper filters, enabling home compost certification.

Medical demand accelerates as PLA anchors controlled-release scaffolds and resorbable suture lines already cleared by the FDA as GRAS. Drug-eluting stents employing PLA-based matrices report uniform degradation and minimal inflammatory response, satisfying cardiology device endpoints. Electronics leverage carbon-fiber-reinforced PLA filaments in fused deposition modeling to prototype lightweight drone frames with tensile strengths near 48 MPa, fostering rapid iteration cycles.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific commanded 40.92% Bio-polylactic Acid market share in 2024, and its 22.68% CAGR underscores the region’s dual role as the largest consumer and the lowest-cost producer. Thailand’s policy of Board of Investment tax breaks for bioplastics cuts project payback periods to six years, encouraging NatureWorks and regional sugar conglomerates to scale new lines. China’s domestic packaging brands substitute PLA for EPS clamshells to meet 2025 plastic-pollution targets, lifting local demand even as export volumes grow. India’s ethanol-blending push diverts some sugarcane output, but integrated mills capture additional value by fermenting molasses into lactic acid for PLA, stabilizing revenue streams.

North America benefits from clear regulatory impetus, such as the federal procurement phase-out and California’s compostability labeling, yet industrial composting infrastructure remains patchy outside coastal metros. Landfill tipping fees in the Midwest remain low, reducing economic incentives for commercial composters to expand, which tempers Bio-polylactic Acid market penetration despite strong brand owner interest. Collaboration between PLA producers and waste haulers to establish dedicated pickup routes in Seattle and Austin demonstrates scalable blueprints for circular loops.

Europe maintains leadership in closed-loop pilots, with the ENZYCLE project proving technical feasibility at 2,000 ton annual capacity depolymerization plants. Stringent EU packaging levy structures push brand owners to adopt bio-based and recyclable content, thereby supporting a price premium over fossil alternatives. South America and the Middle East and Africa present nascent opportunities: Brazil’s sugar surplus aligns well with PLA economics, while the UAE mega-facility will serve regional converters seeking low-carbon packaging for halal certified foods. Absence of curbside organics collection, however, restricts consumer-side composting benefits, delaying full-cycle adoption.

Competitive Landscape

The Bio-polylactic Acid market is consolidated in nature. Asian startups concentrate on differentiated high-heat or rapid-cycle PLA, aided by provincial grants promoting green chemicals. European mid-caps focus on enzymatic depolymerization plants co-located with beverage-carton recyclers, capturing the value of post-consumer PLA that fails to enter industrial compost streams. Offtake agreements now include closed-loop clauses, requiring producers to accept post-industrial scrap for chemical or enzymatic recycling, thus differentiating offers in competitive tenders. As capacity doubles between 2025 and 2030, producers emphasize application and geographic diversity to defend margins against anticipated price erosion in commodity grades of the Bio-polylactic Acid market.

Bio-polylactic Acid (PLA) Industry Leaders

-

Futerro

-

Jiangxi Keyuan Bio-Material Co. Ltd

-

NatureWorks LLC

-

TotalEnergies

-

Zhejiang Hisun Biomaterials Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Emirates Biotech selected Sulzer technology to build the world’s largest PLA production facility in the UAE, with construction starting 2025 and operations commencing early 2028.

- February 2024: Balrampur Chini Mills announced India’s first industrial bioplastic plant with 75,000 tons annual PLA capacity and INR 2,000 crores (~USD 229.87 Million) investment to support India’s net-zero goal.

Global Bio-polylactic Acid (PLA) Market Report Scope

Bio-Polylactic acid (PLA) is a biodegradable and bio-based aliphatic polyester that can be manufactured from renewable materials such as corn, sugarcane, cassava, and sugar beet pulp. This gives bio-PLA manufacturing a lower carbon footprint in comparison to fossil-based plastics. The bio-polylactic acid market is segmented by raw material, form, end-user industry, and geography. On the basis of raw materials, the market is segmented into corn, cassava, sugarcane and sugar beet, and other raw materials. Based on the form, the market is segmented into fiber, films and sheets, coatings, and other forms. Based on the end-user industry, the market is segmented into packaging, medical, electronics, agriculture, textile, and other end-user industries. The report also covers the market size and forecasts for the market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Corn |

| Cassava |

| Sugarcane and Sugar Beet |

| Other Raw Materials |

| Fiber |

| Films and Sheets |

| Coatings |

| Other Forms |

| Packaging |

| Medical |

| Electronics |

| Agriculture |

| Textiles |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Benelux | |

| Austria | |

| Czech Republic and Slovakia | |

| Poland | |

| Hungary | |

| Switzerland | |

| Nordic | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Raw Material | Corn | |

| Cassava | ||

| Sugarcane and Sugar Beet | ||

| Other Raw Materials | ||

| By Form | Fiber | |

| Films and Sheets | ||

| Coatings | ||

| Other Forms | ||

| By End-user Industry | Packaging | |

| Medical | ||

| Electronics | ||

| Agriculture | ||

| Textiles | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Benelux | ||

| Austria | ||

| Czech Republic and Slovakia | ||

| Poland | ||

| Hungary | ||

| Switzerland | ||

| Nordic | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected global volume for Bio-polylactic Acid by 2030?

Global shipments are forecast to reach 2.11 million metric tons by 2030, growing at a 19.51% CAGR.

Which region will add the largest incremental PLA capacity through 2030?

Asia-Pacific is slated to add most new capacity, anchored by facilities in Thailand, China, India, and the UAE.

Why are sugarcane and sugar beet preferred over corn in PLA production?

They offer lower carbon intensity and more stable pricing, capturing 62.66% share of current feedstock usage.

How fast is the packaging segment expanding within PLA applications?

Packaging volumes are rising at a 22.15% CAGR, supported by single-use plastic bans and e-commerce growth.

What technologies enable closed-loop recycling of PLA?

Enzymatic depolymerization, microwave-assisted hydrolysis, and ionic-liquid catalysis recover monomers for repolymerization.

Page last updated on: